Emerging markets are navigating new risks from tariffs.

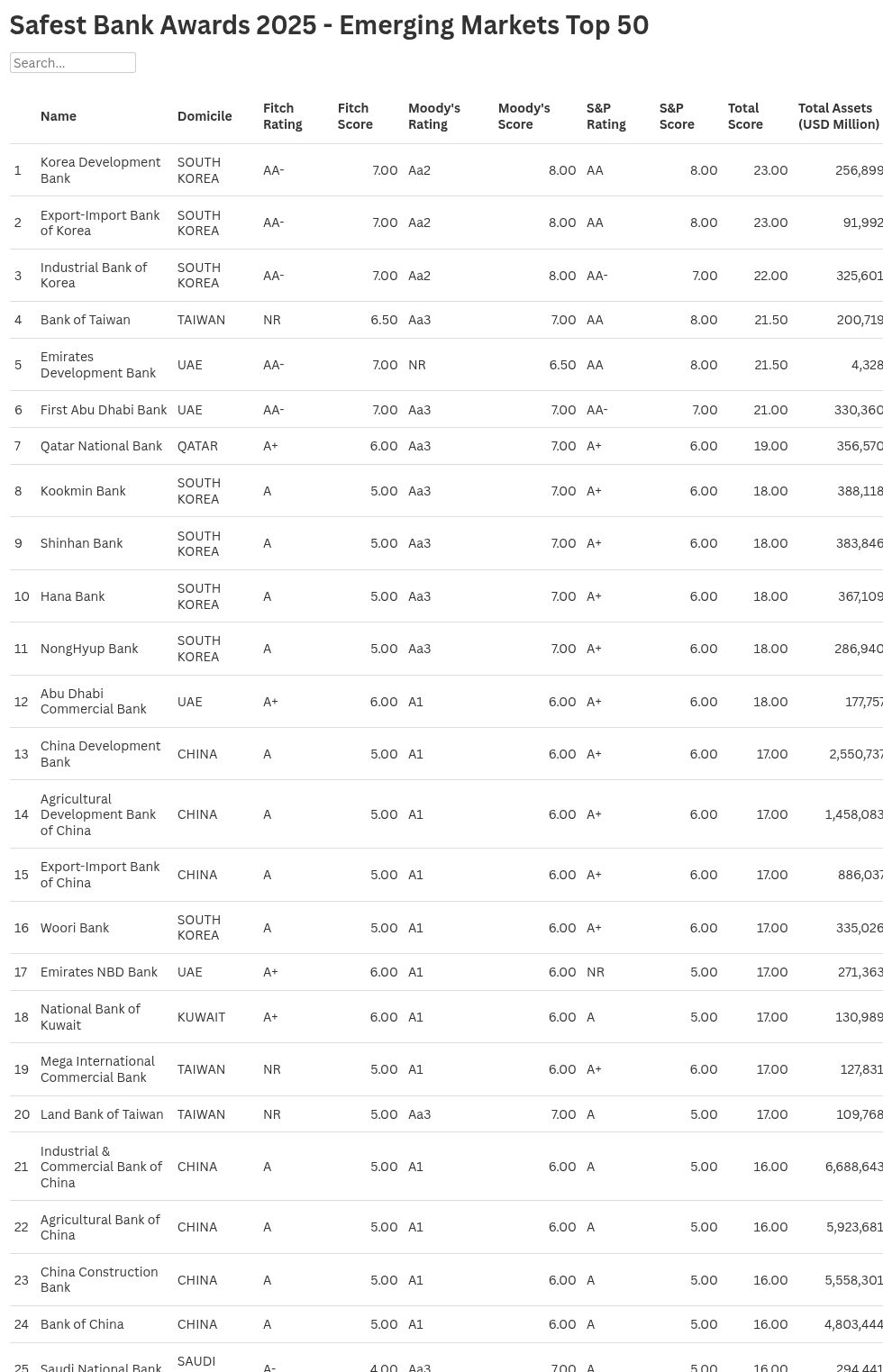

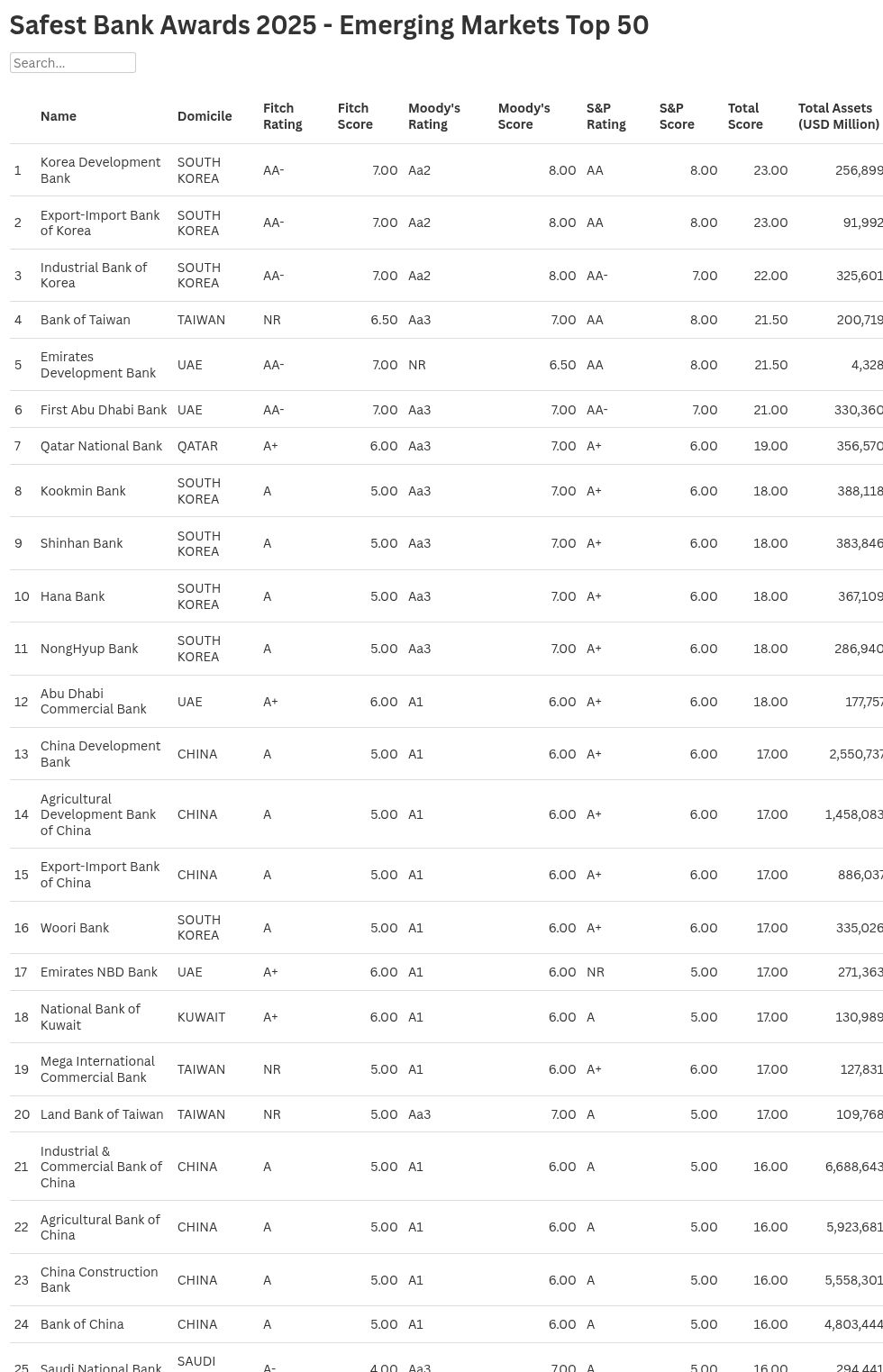

Because many emerging market countries rely heavily on exports, their economies and banking systems face heightened risk from the imposition of US tariffs. With this segment representing some of the largest trading partners of the US, including China, South Korea, and Taiwan, tension surrounding trade negotiations continues to escalate—particularly with China, following the US administration’s most recent threat of 100% tariffs on Chinese imports. Notably, institutions in these three countries represent half of our 50 Safest Emerging Markets banks. South Korean banks claim the top three positions and place nine overall, while China and Taiwan place eight banks each among our rankings.

In every country impacted by US tariff policy, the banking sector must navigate the collateral damage its clients experience due to disrupted trade flows and supply chains. For emerging market economies, the declining value of the US dollar softens some of this impact through relatively cheaper import costs in these markets and eases dollar debt service for those countries and corporations with outstanding dollar-denominated debt. Not surprisingly, emerging market GDP growth expectations have fallen. In the October edition of its World Economic Outlook, the International Monetary Fund forecasts a decline for the emerging market and developing economies from 4.3% in 2024 to 4.2% in 2025 and 4% by 2026.

The GDP decline forecast for China is more pronounced, with 5% growth in 2024 falling to 4.8% in 2025, and further to 4.2% in 2026. An overall deterioration in China’s credit fundamentals prompted Fitch to downgrade the country’s sovereign rating in April to A from A+. As a rationale for the move, the agency cites “a continued weakening of China’s public finances and a rapidly rising public debt trajectory during the country’s economic transition.”

“Sustained fiscal stimulus will be deployed to support growth, amid subdued domestic demand, rising tariffs, and deflationary pressures.”

Fitch Ratings

Fitch adds that “this support, along with a structural erosion in the revenue base, will likely keep fiscal deficits high.” Following this action, the agency downgraded China Development Bank (its ranking fell to No. 13 from No. 8 last year), Agricultural Development Bank of China (to No. 14 from No. 9), and Export-Import Bank of China (to No. 15 from No. 10).

Moody’s upgraded Saudi Arabia’s sovereign ratings in November, with the view that the kingdom’s progress in economic diversification will be sustained, further reducing its exposure to oil market developments and providing a more conducive environment for sustainable development of the country’s nonhydrocarbon economy. Meanwhile, S&P recognized the country’s sustained socioeconomic and capital market reforms with a March 2025 upgrade. Bank upgrades followed, allowing Saudi National Bank to climb to No. 25 in our rankings from No. 35 last year, Al Rajhi moved up to No. 26 from No. 36, and Riyad Bank is now No. 36, up from No. 49.

The kingdom doubled its representation in our rankings to six banks, as Saudi Awwal Bank (No. 41), Banque Saudi Fransi (No. 43), and Arab National Bank (No. 45) are new to the Top 50 this year. Consequently, these moves pushed Ahli Bank, China Merchants Bank, and Banco de Credito e Inversiones from our rankings. Moody’s upgrades provided the catalyst for upward shifts in our rankings. Better credit fundamentals at Emirates NBD Bank, based in the United Arab Emirates (UAE), allowed the bank to rise eight places to No. 17; while Taiwan’s E.SUN Commercial Bank’s improving business franchise, robust risk management, and corporate governance helped move the bank up nine places to No. 30.