This growth stock is a no-brainer buy if you have $200 to spare right now.

Buying and holding solid growth stocks for a long time is a tried and tested way of making money in the stock market. This philosophy not only allows investors to capitalize on disruptive and secular growth trends but also helps them benefit from the power of compounding.

Nvidia (NVDA -4.84%) is a classic example of what a smart growth stock can do for your portfolio. Anyone who bought just $200 worth of this semiconductor stock five years ago is now sitting on massive gains, as that investment is now worth $2,700. Nvidia is still a solid investment despite such outstanding growth in recent years.

Shares of Nvidia are now trading under $200 each (at around $185 as of this writing), thanks to the stock splits executed by the company in recent years. So if you have just $200 in investible cash, buying Nvidia with that money could turn out to be a smart move. Let’s look at the reasons why.

Nvidia’s AI-fueled growth isn’t going to stop anytime soon

Artificial intelligence (AI) has been the single most important catalyst for Nvidia’s surge. As the world was wowed by the abilities of OpenAI’s ChatGPT in November 2022, Nvidia’s graphics processing units (GPUs) were working behind the scenes to train the large language model (LLM) powering the chatbot.

Since then, LLMs have been deployed for building not just chatbots, but also for other tasks such as language translation, text generation, text summarization, image generation, writing code, automating workflows, and content creation, among other things. Businesses and governments are using the help of AI models to improve their efficiency and productivity.

Nvidia is at the center of this AI revolution because its GPUs have been the go-to choice for hyperscalers and cloud infrastructure providers looking to tackle AI workloads. This is evident from Nvidia’s commanding share of 92% in AI data center GPUs. Of course, competition from the likes of Broadcom and AMD could be a thorn in Nvidia’s side in the future, but there is ample opportunity for all the players in the AI chip market to make a lot of money in the coming years.

Citigroup estimates that AI infrastructure spending by major technology companies is likely to exceed $2.8 trillion through 2029, with half of that spending expected to take place in the U.S. itself. That’s a big jump from the investment bank’s earlier forecast of $2.3 trillion. This massive spending is going to be fueled by the growth in AI compute demand.

The enterprise and sovereign demand for AI compute has been robust. According to a survey conducted by the Federal Reserve Bank of St. Louis, workers using generative AI applications are 33% more productive each hour.

Cloud computing capacity available at major hyperscalers and other infrastructure providers is greatly outpaced by demand. Oracle, Amazon, Microsoft, Alphabet, and others are sitting on massive revenue backlogs of more than $1 trillion. So it can be safely said that AI spending over the next four years has the potential to hit Citigroup’s $2.8 trillion mark.

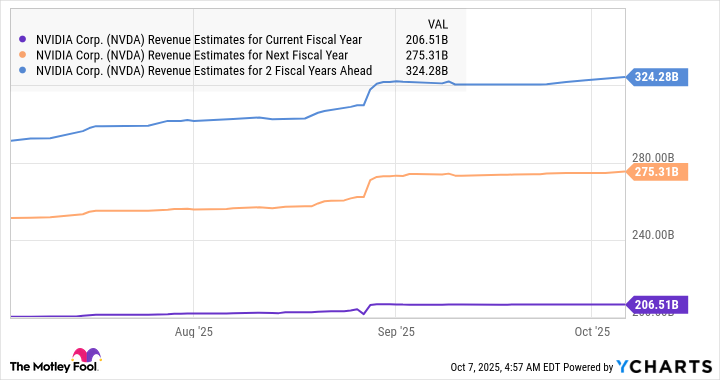

Nvidia is expected to generate $206.4 billion in revenue in the current fiscal year, an increase of 58% from the previous year. So the company still has a lot of room for growth considering that the annual AI spending over the next five years is likely to clock a run rate of $560 billion, according to Citigroup’s estimates. Analysts have therefore become more bullish about Nvidia’s potential growth in the coming fiscal years.

NVDA Revenue Estimates for Current Fiscal Year data by YCharts

The valuation makes the stock a no-brainer buy

The above chart tells us that Nvidia can keep growing at healthy rates despite having already achieved a high revenue base. Not surprisingly, the company’s bottom-line growth is expected to exceed the broader market’s.

For instance, Nvidia’s projected earnings growth rates of 50% for the current fiscal year and 41% for the next fiscal year are much higher than the S&P 500 index’s expected earnings growth rates of 9% and 14%, respectively. Given that Nvidia is now trading at 30 times forward earnings, investors are getting a good deal on this AI stock. It is available at a slight discount to the tech-heavy Nasdaq-100 index’s earnings multiple of 33.

All this makes Nvidia a smart growth stock to buy with just $200, as this company has the potential to witness a significant jump in its market cap over the next five years that could help multiply that investment substantially.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Microsoft, Nvidia, and Oracle. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.