This company will be an AI winner over the next five years.

Everyone wants to invest in Nvidia. The computer chip giant now has a market cap of over $4 trillion, making it the largest company in the world. Other technology giants have been left in the dust, trailing the performance of Nvidia shares.

One underrated stock at the moment is Amazon (AMZN -3.07%). Over the last five years, Amazon’s stock is up just 57% compared to Nvidia’s 1,350% gain, with the former’s performance actually trailing the broad market indices such as the S&P 500, which is up 101%. This means this narrative may flip through 2030.

Here’s why investors are underrating Amazon as an artificial intelligence (AI) stock, and why it could be worth more than Nvidia five years from now in 2030.

An AI beneficiary, competing with Nvidia

Amazon is not thought of as a huge AI beneficiary. Or, at least, it doesn’t come to mind first when you think of AI stocks. The company’s cloud computing division — Amazon Web Services (AWS) — is growing slower than the competition from Alphabet and Microsoft. AWS revenue grew 17% year over year last quarter, while Google Cloud and Microsoft Azure both grew over 30%, gaining market share from Amazon.

However, I don’t think AWS should be thought of as an AI loser. It is the largest cloud computing partner of Anthropic, the fast-growing AI start-up. Anthropic has raised over $10 billion in funding for spending on AI workloads, a lot of which will go to AWS.

Anthropic’s revenue is growing rapidly, up from annual recurring revenue (ARR) of $1 billion to start 2025 to $5 billion in August, making it one of the fastest-growing companies in the world. For AWS, this likely means a huge boost in revenue from Anthropic, which will lead to accelerating revenue growth.

On top of a cloud computing partnership, AWS and Anthropic are working closely to build custom computer chips to compete with Nvidia. One of the largest costs to Amazon’s business is buying computer chips from Nvidia. To cut down on these costs, it is building its own line of chips called Trainium, which will be used to train and run Anthropic’s AI tools. This will not only hurt Nvidia’s sales if scaled up over the next five years, but will save on costs for AWS and lead to rising profitability.

Image source: Getty Images.

Efficiency in e-commerce

An area of Amazon’s business even more underrated when it comes to AI is e-commerce and digital media. Amazon has built up a vertically integrated e-commerce network, hosting its own delivery business, web platform, and fulfillment centers to connect buyers and sellers of online goods. Layered on top are its subscription services and advertising.

All these businesses can be helped with AI tools. For one, Amazon is utilizing AI generative content to help small businesses build advertisements to be played on Amazon’s website and its Prime Video service. Growing advertising revenue as a percentage of Amazon’s overall sales will help increase profit margins.

There are plenty of efficiency gains to be made by utilizing AI and robotics in warehouses, cutting down on the need for workers doing manual labor. Moonshot programs in self-driving could help cut down on costs for the delivery network over the long haul.

Today, Amazon’s North American retail operations (a division that houses everything except AWS) had a profit margin of just 7.5% over the last 12 months. These slim margins will start to reverse due to all the efficiencies and high-margin revenue getting layered into the e-commerce division, combined with solid revenue growth and earnings from e-commerce, which will keep soaring in the years to come.

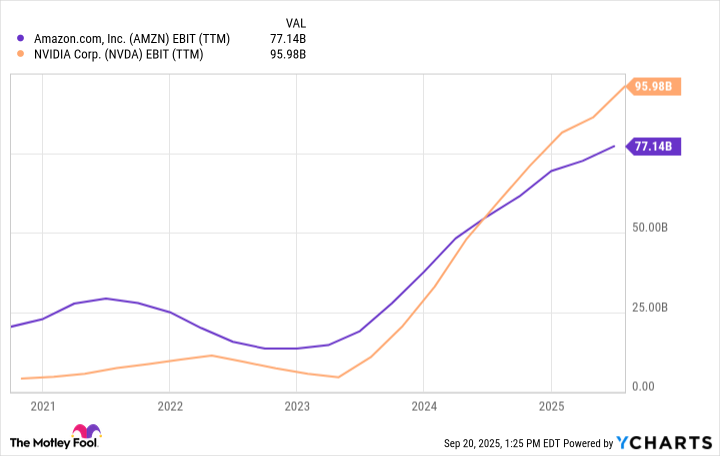

AMZN EBIT (TTM) data by YCharts

Why Amazon can be larger than Nvidia

Looking at earnings before interest income and taxes (EBIT), Amazon and Nvidia are right around the same level. Nvidia’s EBIT is $96 billion, compared to Amazon’s $77 billion. Both figures have grown quickly over the last five years.

Nvidia won’t go bankrupt in the next five years, but its earnings growth may slow. The AI data center boom has been kind to the company’s profitability, and now competitors such as Amazon are trying to build their own chips. Pricing power may come down, and revenue could slow if the semiconductor market hits a cyclical downturn.

On the other side of the equation, Amazon’s EBIT growth will remain strong over the next five years. Revenue will keep chugging higher — especially when considering the Anthropic partnership — and consolidated profit margins will keep expanding. Amazon’s consolidated revenue was $670 billion over the last 12 months, while EBIT margin was just 11.5%. By 2030, revenue can grow to $1 trillion with a 15% EBIT margin, leading to $150 billion in consolidated earnings power for the business.

I believe that will be larger than Nvidia’s earnings in 2030, leading to Amazon surpassing Nvidia in market capitalization.

Brett Schafer has positions in Alphabet and Amazon. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.