Walmart was once a small regional player, too.

Consumer staples retail may seem like an unexciting business. Still, certain superior retail business models have gone on to generate massive market returns. Such was the case with Walmart (WMT -1.20%), which went on to become a 100-bagger stock over a 40-year period between 1972 and 2012.

These stocks look inevitable in retrospect, but who would have thought that a low-margin general store started in rural Arkansas would go on to become the international juggernaut Walmart is today?

For young investors looking for the next big thing in an unassuming package, this convenience store company bears striking similarities to Walmart at this stage.

Casey’s General Stores: small towns, blockbuster returns

Casey’s General Stores (CASY 0.65%) was founded in 1959 in Ankeny, Iowa, and went public in 1983. Despite operating across the Midwest for 65 years, Casey’s has still expanded only within the middle of the country, from North Dakota and Texas in the West to Ohio and Florida in the East, counting 2,895 total stores as of the end of July.

That may sound like a lot, but Casey’s are typically scattered about small towns, with two-thirds of their stores in towns with fewer than 20,000 residents.

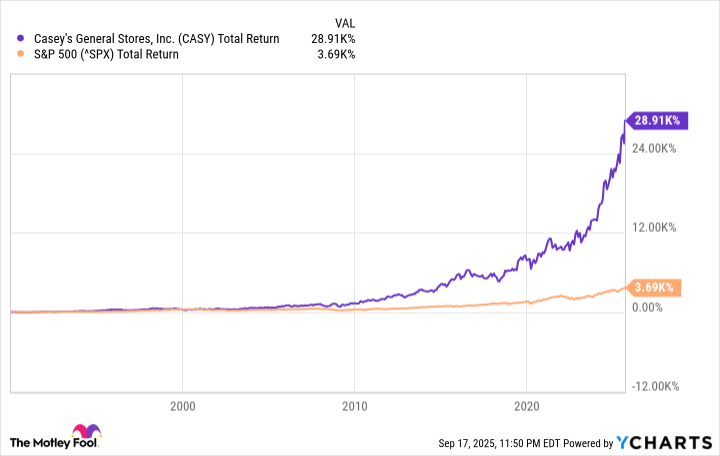

Despite its small-town flavor, Casey’s has had a remarkable run as a public company. Since the beginning of 1990, Casey’s stock has appreciated 289 times over, including dividends, compared with just a 37 times total return for the S&P 500 Index. That’s nearly 8 times relative outperformance!

CASY Total Return Level data by YCharts.

How did this small-town convenience store, which doesn’t exactly display tech-like growth, generate such returns?

Casey’s winning business model

Casey’s didn’t invent the gas station, the convenience store, or the quick-service food market. However, it appears Casey’s has figured out how to do all three well in one convenient locality — and to do it efficiently.

The big differentiator is fresh food — specifically, pizza. It may come as a surprise to some, especially those living on the coasts, that Casey’s is the fifth-largest pizza chain in the United States. Casey’s began offering fresh pizza in 1984, then took those learnings to expand its fresh food offerings. Casey’s now offers prepared food for all dayparts, along with groceries and other general merchandise, including even Casey’s own private label brands.

Those sales are much higher-margin than gasoline, making Casey’s a highly profitable business compared with peers. “Inside the store” sales accounted for 27% of total revenues and 63% of total gross profits, respectively, during the last quarter.

Convenience store operators aren’t typically experts in fresh food, but Casey’s ability to sell fresh food well gives it a lot of advantages. It can offer gasoline at highly competitive prices due to higher-margin inside sales, while lower gasoline prices increase traffic.

Casey’s has also vertically integrated its operations, owning all three of its major distribution centers and 60% of its fuel delivery tankers, which streamlines costs. Casey’s then invests those savings in leading technology, rewards, and data, which further increase frequency.

While not revolutionary, Casey’s found an advantage in delivering fresh food in a convenience store format, then maximized productivity by doubling down on the advantages that model brings. That has resulted in 6.7% operating margins over the past 12 months — pretty good for convenience retail that sells low-margin gasoline — and a 17.1% return on equity, which is also impressive for a store that sells a lot of low-margin gas.

Image source: Getty Images.

Is it too late to buy, though?

Some might look at Casey’s returns and think they’ve missed the boat. And it’s true that a 290 times return probably isn’t in the cards for those who buy now.

However, you can still earn above-average returns on a stock that has already gone up a lot. In 1994, investing legend Peter Lynch noted that investors could have waited until 10 years after Walmart’s initial public offering (IPO) to buy the stock and still made 35 times one’s money. While it wasn’t the 500 times returns you got when buying at the IPO, that’s still a really great return — and, of course, Walmart has continued to appreciate a lot since 1994.

Meanwhile, it does appear that Casey’s still has a strong runway to grow, even in the Midwest. In its recent investor presentation, management noted that within 500 miles of Casey’s three existing distribution centers, 75% of towns with between 500 and 20,000 residents don’t yet have a Casey’s General Store.

The overall convenience store industry also remains fairly fragmented, with the 10 largest convenience store brands making up 63% of the industry and the remaining 37% dispersed over 500 other owners. That means scaled leaders like Casey’s can pick up market share by buying smaller stores in proven locations and converting them, which Casey’s has been doing.

Time is the friend of the wonderful business

Casey’s stock certainly isn’t cheap, trading at 36 times earnings. However, Warren Buffett once said, “Time is the friend of the wonderful company, the enemy of the mediocre.” For those with a long-term perspective, one can do worse than picking up Casey’s shares today. At a market cap of just over $20 billion, Casey’s still has the potential to grow many times over.