For now, the “Magnificent Seven” and select others remain the most popular names in the AI arena.

Over the last few years, companies like Nvidia, Amazon, Alphabet, Microsoft, and Meta Platforms dominated the narrative around artificial intelligence (AI). As the conversation shifted beyond chips and into adjacent applications in data centers and software, names such as Broadcom, Taiwan Semiconductor Manufacturing, and Palantir Technologies also stepped into the spotlight.

It’s no secret that the AI trade remains heavily concentrated within a small circle of big tech giants. But savvy investors know that opportunity doesn’t end with the usual suspects.

So here’s the question: Have you heard of Nebius Group (NBIS 49.20%)? If not, you’re not alone.

This sprawling data center company has flown under the radar — but its unique position in the AI ecosystem could propel it into the spotlight and make it a household name very soon.

Nebius took an unconventional route to the AI revolution

Unlike many of its louder peers, Nebius did not emerge as a flashy start-up or an established tech titan already entrenched in the AI race. Instead, the company traces its roots back to Yandex — a Russian internet conglomerate.

As geopolitical tensions from the Russia-Ukraine war escalated, Yandex moved to divest its noncore assets. From that process, Nebius was spun off, and it was listed on the Nasdaq exchange last October.

Soon after, Nebius completed a capital raise that attracted a particularly notable participant: Nvidia. The undisputed leader in AI chips not only became an investor but also established itself as a strategic ally — lending Nebius a level of credibility that few companies can claim.

At its core, Nebius can be considered a neocloud — a business specializing in building AI infrastructure by constructing data centers and renting out Nvidia’s sought-after graphics processing units (GPUs) to other businesses via the cloud. This model positions Nebius to scale up in lockstep with Nvidia, benefiting as next-generation chips like Blackwell and Rubin enter the market.

Image source: Getty Images.

Nebius is more than GPUs

While infrastructure is its core business, Nebius operates several subsidiaries and also has notable strategic investments.

Toloka is in the business of data labeling, an important component of training datasets for AI models. The company also has exposure to autonomous driving systems and robotics through Avride and maintains a software platform called TripleTen that specializes in educating developers across various AI applications.

Nebius also has an equity stake in ClickHouse, an open-source database management and analytics system.

This diversified ecosystem positions Nebius beyond chips and provides the company with exposure to a number of potentially trillion-dollar ancillary markets as AI workloads become larger and more advanced.

Is Nebius stock a buy right now?

In December 2024, Nebius’s core infrastructure segment closed the year with an annualized run rate of $90 million. Just two quarters later (by June 30), the company’s annual recurring revenue (ARR) run rate surged to $430 million. Even more compelling is that management recently raised full-year guidance to a range of $900 million to $1.1 billion from its prior outlook of $750 million to $1 billion.

On Sept. 8, however, everything changed for Nebius as news broke that the company signed a massive new deal with Microsoft. According to regulatory filings, Nebius “will provide Microsoft access to dedicated GPU infrastructure capacity” at its data center in New Jersey. The contract is worth $17.4 billion and runs through 2031.

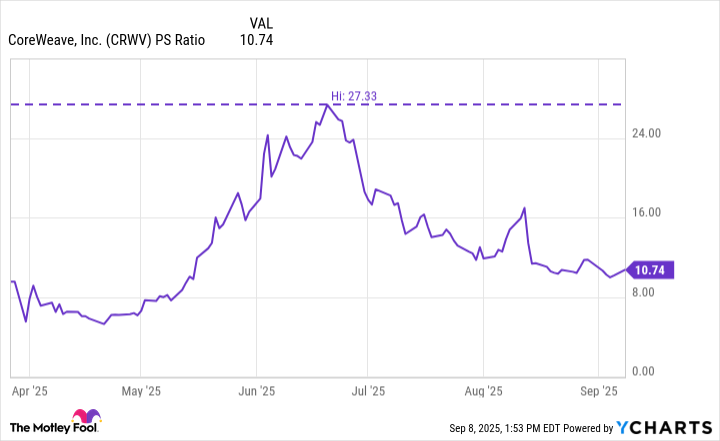

Prior to the deal with Microsoft, Nebius boasted a market capitalization of $15.4 billion — implying a forward price-to-sales ratio of about 14 at the high end of its ARR forecast. For context, that’s about half the multiple CoreWeave commanded at its peak earlier this year following its much-hyped initial public offering.

CRWV PS Ratio data by YCharts

This suggests a couple of takeaways. On one hand, Nebius’s valuation has been swept up in the broader bullish AI narrative — leaving traces of froth. On the other, the stock has remained relatively insulated from the sharp pullbacks seen in more volatile peers like CoreWeave — a dynamic that could play in its favor as it continues to fight for mindshare in an increasingly crowded and competitive market.

Looking ahead, Nebius appears positioned to benefit from secular tailwinds fueling AI infrastructure. Microsoft’s new deal emphasizes that cloud hyperscalers are showing no signs of slowing their capital expenditure, and Nebius is already steadily carving out a role as a beneficiary of that spending.

I think Nebius will be trading materially higher than it is today by next decade as its relationship with Microsoft matures. That makes it, in my view, a compelling buy-and-hold opportunity.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Palantir Technologies. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, Palantir Technologies, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom and Nebius Group and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.