Costco’s ability to sell near-identical Lululemon products could further weigh down the apparel company’s sluggish growth rate.

Lululemon Athletica (LULU -0.80%) is suing Costco Wholesale (COST 1.08%) for selling similar, knock-off products in its warehouses. For the high-end apparel company, how this ends up playing out could be a make-or-break moment for its stock.

Shares of Lululemon are down close to 50% this year as investors have grown concerned with the company’s lackluster growth and worrisome exposure to China. The stock hasn’t been trading at these levels since 2020, and depending on your outlook for the business in the long run, Lululemon could either be a steal of a deal right now, or nothing more than a value trap.

What could end up determining that is its battle with Costco.

Image source: Getty Images.

Why the Costco lawsuit could be critical for Lululemon

Lululemon is alleging that Costco has been selling “dupes” of its products and that they are confusing its customers. The suit claims that Costco has infringed on Lululemon’s intellectual property due to how similar the items are, and that they go beyond just selling similar types of clothing. It says that Costco is also using the same color names, such as “Tidewater Teal,” which Lululemon says, “is an important component” of its business.

If Costco is able to fend off the lawsuit and continue selling the products, it could pose a serious threat to Lululemon’s growth at a time when it’s already struggling to grow sales at a high rate. Consumers have been cutting back on discretionary expenditures and if Lululemon has to also compete against Costco and its low prices, that could exacerbate its current woes.

Many Lululemon pants frequently retail at more than $100, and if consumers can buy similar products at their local Costco, that could hurt the company’s pricing power, possibly forcing it to reduce prices, which would hurt its gross margins and impact its overall level of profitability.

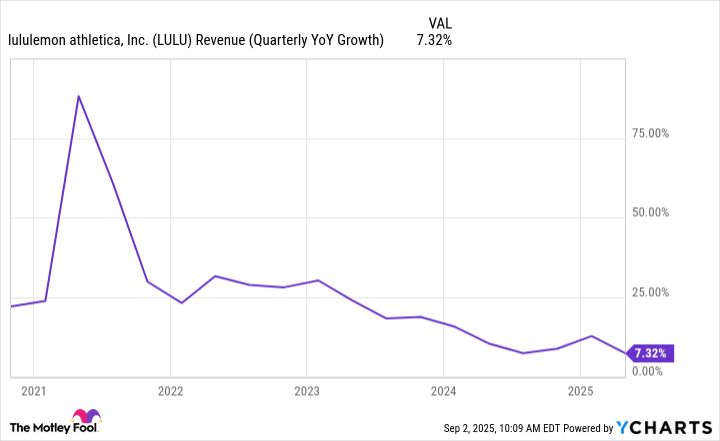

Lululemon’s growth rate has been falling sharply in recent years

In recent quarters, Lululemon has been growing its sales by just single digits, which is down significantly from how well the business did in previous years — when it wasn’t uncommon for its growth rate to be in excess of 20%.

LULU Revenue (Quarterly YoY Growth) data by YCharts

If you factor in the potential for Costco to provide customers with similar-looking products, that could further erode its growth rate in the future. And with tariff uncertainty still looming with respect to China, a key market for Lululemon and where it also imports many of its products from, there are multiple headwinds for investors to consider before buying the retail stock.

Why I’d avoid Lululemon stock right now

Lululemon’s intellectual property and overall competitive advantage faces a big test with its suit against Costco right now. If consumers can buy similar-looking clothing at just a fraction of the price, it could lead to even worse growth prospects for the company in future quarters. And with macroeconomic conditions not looking all that great, consumers may still be tempted to look for lower-priced alternatives. The declining growth rate does seem to suggest that demand may be constrained right now.

Although Lululemon stock may look cheap, trading at a price-to-earnings multiple of around 14, given the uncertainty the business faces in both the short and long term, this is not a company I’d invest in today. It all hinges on how much value consumers place on the brand and the willingness to pay significantly more for Lululemon products. Right now, things aren’t looking too good, and unless Lululemon’s growth prospects drastically improve or it wins its suit against Costco, I’d avoid the stock.

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale and Lululemon Athletica Inc. The Motley Fool has a disclosure policy.