SoundHound AI Stock Jumped 23.5% in September — for All the Wrong Reasons

SoundHound AI stock gained 23.5% last month despite mixed reactions to company news. Is it time to jump aboard this AI bandwagon?

Shares of SoundHound AI (SOUN 0.31%) rose 23.5% in September 2025, according to data from S&P Global Market Intelligence. It wasn’t a smooth ride for the artificial intelligence (AI) expert, with several big jumps and a couple of painful drops along the way — but it’s hard to complain about a monthly gain of more than 20%.

The meme stock crowd is back in action

Unfortunately, it looks like SoundHound AI is sliding back into the meme stock phenomenon again.

The big swings in September’s stock chart seem more closely correlated to online discussion volumes than to broader stock market trends — and the spikes didn’t really line up with SoundHound AI’s handful of business-related announcements. It’s an “all talk and no action” sort of thing.

I mean, the company isn’t sitting on its hands. Its business moves just aren’t inspiring bullish price moves. Social media posts are doing more of that work.

Let’s look at the three press releases SoundHound AI shared last month:

-

On Sept. 4, the company released a custom AI agent for Primary Health Solutions, a regional healthcare network near Cincinnati and Dayton, Ohio. The Denise agent delivers quick answers to common questions, online or over the phone. SoundHound AI’s stock rose 7% that day — not too shabby!

-

Sept. 9 saw a 5.4% stock price drop as SoundHound AI acquired Interactions, an agentic AI specialist. This deal should boost the company’s operating profits from the get-go and expand its market reach into new sectors such as retail management and insurance. For what it’s worth, the S&P 500 (^GSPC 0.34%) index rose 0.3% the same day.

-

Finally, Red Lobster ordered a systemwide SoundHound AI solution for its phone ordering services on Sept. 23. This announcement should have started a victory march at SoundHound AI’s headquarters, but the stock didn’t move at all on the news. Instead, a 13% price drop followed over the next two market days. The S&P 500 held steady across this period.

The market reaction on Sept. 4 made sense, but I see the opposite effect around the (arguably more significant) announcements that followed.

Image source: Getty Images.

Great company, but the stock valuation is getting silly again

The meme stock action kind of makes sense. I understand that investors are getting excited about SoundHound AI’s high-quality voice controls and related AI tools. I’m convinced that the company has a bright future, and the shares I’ve been holding since the spring of 2024 should serve me well in the long run.

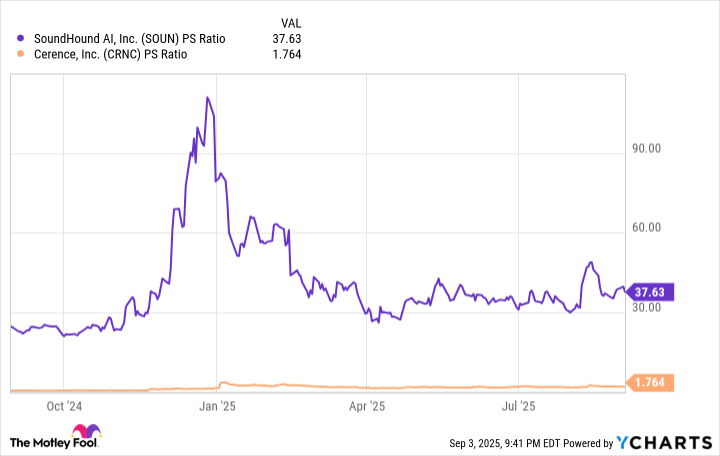

But the recent market action is too optimistic. People are jumping to conclusions, long before SoundHound AI gets a chance to prove its actual market value. On Oct. 1, the stock is up 238% over the last year and 424% in three years. It’s also trading at the nosebleed-inducing valuation of 50 times trailing sales. Profit-based metrics don’t make sense, because the company is deeply unprofitable so far.

So I’m holding on to my existing SoundHound AI shares for the long haul, but I’m not tempted to buy any more at these lofty prices. Check again when this meme-stock rally fades out. It’s too early to ask for stronger sales or positive profit margins.

Anders Bylund has positions in SoundHound AI. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.