“I am going to Istanbul on Monday for breast augmentation. I cannot wait, my boobs right now are really big for me.

“I’ve lost quite a bit of weight and I just can’t have this anymore.

“So I found the best surgeon in Istanbul.”

I’d go on Big Brother again – and let my daughters do it – but I’m not doing OnlyFans, says Imogen Thomas

She continued: “I had a great video consultation with him and I’m flying out. I’m getting them done.

“I’m going smaller and I’m getting an uplift and I cannot wait to show you guys the results in my dresses, in my workout wear. I cannot wait to feel body confident again.

“Like the excitement is literally unreal. I can’t believe I found the time to go for a start, which is great.”

Imogen ended by saying: “So yeah, cannot wait to show you guys. It’s something that I’m super excited about and yeah, you’re going to see a lot in the next few days.”

Big Brother winners from over the years

Since launching in 2000, reality TV juggernaut Big Brother has crowned several champions over the years. Let’s take a look back at some of them.

The former glamour model remained in the spotlight ever since her stint in the famous house and even had an affair with a VERY famous footballer.

The former Miss Wales lasted 86 days in the Big Brother house, becoming good pals with the late Nikki Grahame and fellow Welshman Glyn Wise, who finished runner-up behind Pete Bennett.

As soon as she was evicted she was commanding five-figure sums for racy lads’ mag shoots — and was named Wales’s Sexiest Woman.

She was also seen at the swankiest showbiz parties and dated high-profile footballers, including a heavily publicised affair with married Wales and Man Utd star Ryan Giggs, who placed a gagging order on her.

Once news of the relationship broke, she publicly apologised for the affair.

At the time, she said: “I called it off a million times but he kept coming back.

“He knew it was wrong as well, he said as much, but he was pursuing me.”

The mum-of-two insisted that fame “doesn’t last forever” and urged new reality stars to “take every opportunity” that comes their way.

“What you get offered take because beggars can’t be choosers at the end of the day,” Imogen said.

“When I was on the show, there were so many magazines that I could be modelling for and I was for like 10 years straight. I had so many contracts with them.”

She continued to the Metro: “Yes, you’ve got social media and I work on that now and I’m making thousands a post but brands are a little bit more cautious now and they don’t want to be paying the money anymore.

“So for me, I would just say take whatever you can get and make good of the situation because it does dry out.”

She also told The Sun: “I came off the show and I just started working from day one. It was amazing, I made a lot of money.

“It was just all a bit surreal because I went in as a hostess and came out just making all this money and being wanted by everyone.

“It was pretty crazy to get your head around. But I loved it.

“I was in there for three months, no contact with the outside world, then all of a sudden everyone knows you, and you’ve got to get used to the fame.”

6

The reality star shared that she wanted to get a breast reduction after she lost a bit of weightCredit: Instagram

6

She flew to Istanbul for her surgeryCredit: Instagram

6

Imogen thanked her followers for their supportCredit: Instagram

6

She confessed her boobs were “too big for me”Credit: instagram

People approaching retirement should consider whether delaying benefits is worth the monthly increase.

For 90 years, Social Security has provided millions of Americans with a financial lifeline in retirement, helping to keep many Americans above the poverty line. That’s why deciding when you want to claim benefits is such a crucial decision because it permanently affects how much you’ll be receiving in monthly benefits.

As of the end of 2024, the average monthly benefit for someone aged 70 was $2,148.12, or approximately $25,777 annually. For men, the average benefit at that age is $2,389.95, and for women, it’s $1,909.42 (the difference is due to the disparity in lifetime earnings).

Image source: Getty Images.

How claiming at 70 affects your monthly benefit

For anyone born in 1960 or later, your full retirement age (FRA) is 67. This is the age at which you can receive your full monthly benefit amount, known as your primary insurance amount (PIA). Starting at your PIA, the Social Security Administration calculates your monthly benefit based on whether you claim before or after your FRA.

By delaying benefits past your FRA, you increase your monthly benefit by 2/3 of 1% monthly, or 8% annually. You can delay benefits and receive this increase until you reach age 70; after that, your monthly benefit is no longer increased, so that’s realistically the latest age you should claim benefits.

For example, if your PIA was $2,000 at your FRA (assuming it’s 67), delaying benefits until 70 would increase your monthly amount by 24%, taking it to $2,480. This increase, along with the annual cost-of-living adjustment (COLA), is why the average benefit is higher at 70 than at younger ages.

The federal government needs to act fast to save one of the country’s most important social programs.

As of July, over 53 million Americans receive Social Security retirement benefits. A good number of these recipients rely on the Social Security program for most or, in some cases, all of their retirement income, so it’s hard to overstate just how important the program continues to be.

According to the Nationwide Retirement Institute 2025 Social Security Survey, over 60% of Social Security recipients feel as though they’d be financially vulnerable if there were cuts to Social Security benefits. That’s not too surprising, given how much people rely on the social program.

However, what may be surprising is just how soon cuts to Social Security benefits could happen at the current pace of deficit that the program is running on.

Image source: Getty Images.

How Social Security funding works

Before discussing the likelihood of Social Security benefit cuts, it’s essential to understand how the program is funded, which is through payroll taxes. The current rate is 12.4%, with employers and employees paying 6.2% each, and self-employed people paying the full 12.4%.

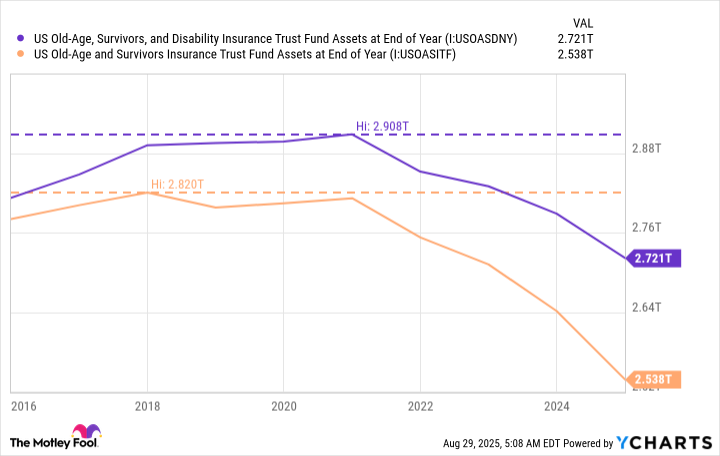

This tax revenue is put into the Social Security Trust Fund, which consists of the Old-Age and Survivors Insurance (OASI) Trust Fund and the Disability Insurance (DI) Trust Fund. The OASI program pays benefits to retirees, their families, and survivors of deceased recipients; the DI program pays benefits to disabled workers and their families.

The idea is that working-age people pay into the system to support current retirees, with the understanding that once they’re retired, they’ll be on the receiving end of this support.

What’s the likelihood of benefits being cut?

The Social Security Administration’s (SSA) 2025 Social Security Trustees Report highlighted that the Social Security program cost $1.485 trillion in 2024, while generating only $1.418 trillion in revenue, leaving a $67 billion deficit for the year. Both major Social Security trust funds have experienced a decline over the past decade.

The same report noted that the OASI trust fund could be depleted by 2033, which would leave the SSA with the ability to pay only 77% of its expected benefits. Considering the number of recipients from the Nationwide report who said cuts would make them financially vulnerable, this is, to put it lightly, far from ideal.

If the current depletion rate continues, the Social Security Trust Fund could be underfunded by more than $25 trillion through 2099 (the DI Trust Fund reserves are not projected to become depleted during this period). If no changes are made, Social Security would need to cut benefits by about 23% beginning in 2034.

According to the Nationwide study, 83% of respondents are concerned about Social Security’s long-term viability, and 74% are worried that the program’s funding could run out in their lifetime. Unfortunately, at the current pace and lack of concrete solutions, these concerns are justified.

What’s causing the current Social Security deficit?

There isn’t a single reason for the current Social Security deficit, but there are four main causes contributing to the problem. The first is that baby boomers are retiring in large numbers, and there aren’t enough tax-paying workers paying into the Social Security program.

The second “problem” is that people are living longer, meaning they’re collecting benefits longer, increasing how much Social Security has to pay out each year. This is good for people, but bad for Social Security.

We’ve also seen an increase in high earners, which means less of their income is being taxed and paid into the program. In 2025, the most income that’s subject to the Social Security payroll tax is $176,100. Any money earned above that is free from the tax.

The last problem is that before the interest rate hike a couple of years ago, interest rates spent a long period at historically low rates. This is a problem for Social Security because the reserves are put into Treasury bonds to earn interest. Low interest rates mean less money earned on these reserves.

All hope isn’t lost

To end on a more positive note, it’s worth pointing out that this isn’t the first time that Social Security has faced funding issues, and in previous times, the federal government has been able to “fix” the issue.

The American political environment is a bit more unpredictable nowadays, so I can’t say for certain if the same will happen. However, given the program’s importance to the livelihoods of millions of Americans, one would assume that it would become a priority for politicians on both sides of the aisle.

Many Americans are making a simple (but costly) Social Security mistake.

If you’re planning to take Social Security in 2025, you’re likely nearing retirement. While that’s an exciting chapter in life, even small mistakes can sometimes throw a wrench in your plans — so it’s critical to ensure you have a strong plan heading into your senior years.

There’s not necessarily a right or wrong Social Security strategy, but there is one aspect that trips many retirees up: knowing how your claiming age will affect your lifetime benefit.

Your benefit will be locked in for life

The age you file for benefits will have an immediate and lifelong impact on your benefit amount. However, many people are unaware of just how much their decision will affect their monthly income.

Image source: Getty Images.

According to a 2025 survey from the Nationwide Retirement Institute, only 21% of U.S. adults can correctly name their full retirement age (FRA) — which is the age at which you’re entitled to your full benefit based on your work history. Your FRA will depend on your birth year, but everyone’s will fall between ages 66 and 67.

Filing before your FRA will result in a reduced payment, which is also a point of confusion for many people. The survey found that 40% of Americans believe that if they file for benefits early, their payments will automatically go up once they reach their FRA. In reality, though, these reductions are permanent, and those smaller payments will be locked in for life.

These reductions can be significant, too. If you have an FRA of 67 years old, filing at 62 will slash your checks by 30%. The average retired worker receives around $588 less per month at age 62 compared to age 67, according to 2024 data from the Social Security Administration.

Age

Average Monthly Benefit Among Retired Workers

62

$1,342

63

$1,364

64

$1,425

65

$1,611

66

$1,764

67

$1,930

68

$1,980

69

$2,040

70

$2,148

Data source: Social Security Administration. Table by author.

Not knowing exactly how your age will affect your lifetime benefit amount is a simple mistake to make, so you’re in good company if you’re among the 40% of Americans in this boat. But if you’re heading into retirement expecting your benefit to increase by hundreds of dollars per month in a few years, it could be a costly mistake.

The best move you can make right now

Before you begin claiming benefits, one of the best things you can do is check your estimated benefit amount.

You can do this by reviewing your statements through your mySocialSecurity account online, where you’ll see an estimate of your future benefit based on your real earnings. This is also a prime opportunity to double-check that your earning history is correct, because if there’s any information missing or incorrect, it can affect your benefit amount.

The estimate you see on your statements is your full benefit amount, or the payment you’ll receive by filing at your FRA. From there, you can determine exactly how your claiming age will affect the size of your checks.

Age You File for Benefits

Monthly Benefit Reduction for Those With an FRA of 67 Years Old

62

30%

63

25%

64

20%

65

13.3%

66

6.7%

67

0% (full benefit amount)

Data source: Social Security Administration. Table by author.

You can also file for benefits at any age between birthdays, but for every month you claim before your FRA, your benefits will be reduced slightly more. By having at least a rough estimate of how much will be deducted, it will be easier to plan accordingly.

Keep in mind, too, that if you’re filing after your FRA (up to age 70), that will also alter your benefit. If you have an FRA of 67 and you file at 70, you’ll collect your full benefit, plus a bonus of 24% per month.

There’s no right or wrong time to take Social Security, but it is important to know how that decision will affect your benefit. When you know what to expect from Social Security heading into retirement, you can rest easier knowing you’re as prepared as possible.

Based on projections, retirees should prepare for a larger increase than in 2025, but it still may not be good enough.

On Aug. 14, 1935, President Franklin D. Roosevelt signed the Social Security Act into law, intending to provide financial security during the Great Depression. More than four years later, in January 1940, the first monthly Social Security checks were sent out. Since then, the program has grown tremendously to be one of America’s largest and most important.

In the 90 years that Social Security has been in place, it has benefited hundreds of millions of retirees. In fact, the program will make over $1.6 trillion in payments to around 72 million beneficiaries, including those receiving retirement benefits, disability benefits, and survivor benefits.

Image source: Getty Images.

A lot has changed with Social Security over the past 90 years. If you’re a current recipient, you can attest to how much continues to change — including eligibility, benefit calculations, and full retirement ages. But arguably the most important change happens annually with the cost-of-living adjustment (COLA).

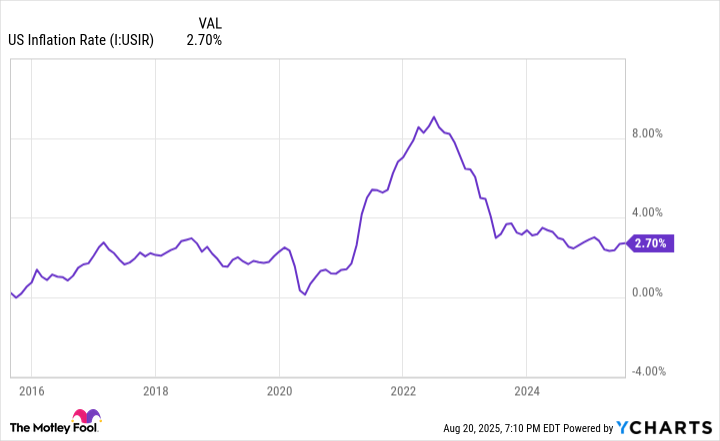

The annual COLA was put in place in 1972 to help retirees deal with inflation while receiving fixed monthly benefits. The official COLA percentage will be announced on Oct. 15, but retiree advocacy group The Senior Citizens League (TSCL) has routinely put out projections to help retirees plan ahead.

In its latest estimate released this month, TSCL has the upcoming COLA at 2.7%. Although the projection shouldn’t be taken as a guarantee, it’s worth taking a deeper dive into how the COLA works and what a 2.7% adjustment could mean for retirees.

How the annual COLA is determined

To determine the yearly COLA, the Social Security Administration (SSA) looks at a specific measure of inflation called the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). It’s published monthly by the Bureau of Labor Statistics (BLS) and takes into account the price of goods and services like food (groceries and restaurants), transportation (vehicles, gas, and public transportation), housing (rent and utilities), and healthcare (services, prescriptions, and insurance premiums).

The SSA uses a three-step process to come up with the specific percentage to set as the COLA:

Calculate the CPI-W average for the third quarter (July, August, and September) of the current year.

Calculate the same average for the previous year.

Set the percentage increase as the COLA for the upcoming year (rounding it up to the nearest 0.1%).

For example, the third-quarter CPI-W average in 2024 was 308.729, and the average in 2023 was 301.236. That 2.43% increase is how we ended up with the 2.5% COLA for 2025.

If the CPI-W decreases or stays the same, there is no COLA, and benefits remain unchanged. It’s not common, but it has happened (in 2010, 2011, and 2016).

A benefits increase sounds like a good thing for Social Security, and for the most part, it is. However, a major (and valid) complaint has been that the COLA isn’t typically enough to truly offset the effects of inflation.

According to TSCL, Social Security recipients have lost around 30% of their purchasing power since 2000. This means every $100 in benefits received in 2000 would only buy $70 worth of goods and services today. From 2010 to 2024, TSCL says that Social Security benefits lost 20% of their purchasing power; that’s far from ideal.

If TSCL’s 2.7% COLA estimate turns out to be true, the average monthly benefit would increase from $2,007 (July’s average) to $2,061. A $54 monthly increase is better than no increase, but retirees have likely seen their monthly expenses increase by more than that.

There aren’t any concrete plans in place to change how the SSA calculates the annual COLA. In the meantime, it’s best for retirees to assume that benefits alone may not fully keep up with inflation, and make efforts to adjust their spending accordingly.

John McGing couldn’t reach a human. That might be business-as-usual in this economy, but it wasn’t business; he had called the Social Security Administration, where the questions often aren’t generic and the callers tend to be older, disabled, or otherwise vulnerable Americans.

McGing, calling on behalf of his son, had an in-the-weeds question: how to prevent overpayments that the federal government might later claw back. His call was intercepted by an artificial intelligence-powered chatbot.

No matter what he said, the bot parroted canned answers to generic questions, not McGing’s obscure query. “If you do a key press, it didn’t do anything,” he said. Eventually, the bot “glitched or whatever” and got him to an agent.

It was a small but revealing incident. Unbeknownst to McGing, a former Social Security employee in Maryland, he had encountered a technological tool recently introduced by the agency. Former officials and longtime observers of the agency say the Trump administration rolled out a product that was tested but deemed not yet ready during the Biden administration.

“With the new administration, they’re just kind of like, let’s go fast and fix it later, which I don’t agree with, because you are going to generate a lot of confusion,” said Marcela Escobar-Alava, who served as Social Security’s chief information officer under President Joe Biden.

Some 74 million people receive Social Security benefits; 11 million of those receive disability payments. In a survey conducted last fall, more than a third of recipients said they wouldn’t be able to afford such necessities as food, clothing, or housing without it. And yet the agency has been shedding the employees who serve them: Some 6,200 have left the agency, its commissioner told lawmakers in June, and critics in Congress and elsewhere say that’s led to worse customer service, despite the agency’s efforts to build up new technology.

Take the new phone bot. At least some beneficiaries don’t like it: Social Security’s Facebook page is, from time to time, pockmarked with negative reviews of the uncooperative bot, as the agency said in July that nearly 41% of calls are handled by the bot.

Lawmakers and former agency employees worry it foreshadows a less human Social Security, in which rushed-out AI takes the place of pushed-out, experienced employees.

Anxieties across party lines

Concern over the direction of the agency is bipartisan. In May, a group of House Republicans wrote to the Social Security Administration expressing support for government efficiency, but cautioning that their constituents had criticized the agency for “inadequate customer service” and suggesting that some measures may be “overly burdensome.”

The agency’s commissioner, Frank Bisignano, a former Wall Street executive, is a tech enthusiast. He has a laundry list of initiatives on which to spend the $600 million in new tech money in the Trump administration’s fiscal 2026 budget request. He’s gotten testy when asked whether his plans mean he’ll be replacing human staff with AI.

“You referred to SSA being on an all-time staffing low; it’s also at an all-time technological high,” he snapped at one Democrat in a House hearing in late June.

But former Social Security officials are more ambivalent. In interviews with KFF Health News, people who left the agency — some speaking on the condition of anonymity for fear of retribution from the Trump administration and its supporters — said they believe the new administration simply rushed out technologies developed, but deemed not yet ready, by the Biden administration. They also said the agency’s firing of thousands of employees resulted in the loss of experienced technologists who are best equipped to roll out these initiatives and address their weaknesses.

“Social Security’s new AI phone tool is making it even harder for people to get help over the phone — and near impossible if someone needs an American Sign Language interpreter or translator,” Sen. Elizabeth Warren (D-Mass.) told KFF Health News. “We should be making it as easy as possible for people to get the Social Security they’ve earned.”

Spokespeople for the agency did not reply to questions from KFF Health News.

Using AI to automate customer service is one of the buzziest businesses in Silicon Valley. In theory, the new breed of artificial intelligence technologies can smoothly respond, in a human-like voice, to just about any question. That’s not how the Social Security Administration’s bot seems to work, with users reporting canned, unrelated responses.

The Trump administration has eliminated some online statistics that obscure its true performance, said Kathleen Romig, a former agency official who is now director of Social Security and disability policy at the left-leaning Center on Budget and Policy Priorities. The old website showed that most callers waited two hours for an answer. Now, the website doesn’t show waiting times, either for phone inquiries (once callback wait time is accounted for) or appointment scheduling.

While statistics are being posted that show beneficiaries receive help — that is, using the AI bot or the agency’s website to accomplish tasks like getting a replacement card — Romig said she thinks it’s a “very distorted view” overall. Reviews of the AI bot are often poor, she said.

Agency leaders and employees who first worked on the AI product during the Biden administration anticipated those types of difficulties. Escobar-Alava said they had worked on such a bot, but wanted to clean up the policy and regulation data it was relying on first.

“We wanted to ensure the automation produced consistent and accurate answers, which was going to take more time,” she said. Instead, it seems the Trump administration opted to introduce the bot first and troubleshoot later, Escobar-Alava said.

Romig said one former executive told her that the agency had used canned FAQs without modifications or nuances to accommodate individual situations and was monitoring the technology to see how well it performed. Escobar-Alava said she has heard similarly.

Could automation help?

To Bisignano, automation and web services are the most efficient ways to assist the program’s beneficiaries. In a letter to Warren, he said that agency leaders “are transforming SSA into a digital-first agency that meets customers where they want to be met,” making changes that allow the vast majority of calls to be handled either in an automated fashion or by having a human return the customer’s call.

Using these methods also relieves burdens on otherwise beleaguered field offices, Bisignano wrote.

Altering the phone experience is not the end of Bisignano’s tech dreams. The agency asked Congress for some $600 million in additional funding for investments, which he intends to use for online scheduling, detecting fraud, and much more, according to a list submitted to the House in late June.

But outside experts and former employees said Bisignano overstated the novelty of the ideas he presented to Congress. The agency has been updating its technology for years, but that does not necessarily mean thousands of its workers are suddenly obsolete, Romig said. It’s not bad that the upgrades are continuing, she said, but progress has been more incremental than revolutionary.

Some changes focus on spiffing up the agency’s public face. Bisignano told House lawmakers that he oversaw a redesign of the agency’s performance-statistics page to emphasize the number of automated calls and deemphasize statistics about call wait times. He called the latter stats “discouraging” and suggested that displaying them online might dissuade beneficiaries from calling.

Warren said Bisignano has since told her privately that he would allow an “inspector general audit” of their customer-service quality data and pledged to make a list of performance information publicly available. The agency has since updated its performance statistics page.

Other changes would come at greater cost and effort. In April, the agency rolled out a security authentication program for direct deposit changes, requiring beneficiaries to verify their identity in person if what the agency described in regulatory documents as an “automated” analysis system detects anomalies.

According to documents accompanying the proposal, the agency estimated about 5.8 million beneficiaries would be affected — and that it would cost the federal government nearly $1.2 billion, mostly driven by staff time devoted to assisting claimants. The agency is asking for nearly $7.7 billion in the upcoming fiscal year for payroll overall.

Christopher Hensley, a financial adviser in Houston, said one of his clients called him in May after her bank changed its routing number and Social Security stopped paying her, forcing her to borrow money from her family.

It turned out that the agency had flagged her account for fraud. Hensley said she had to travel 30 minutes to the nearest Social Security office to verify her identity and correct the problem.

Tahir writes for KFF Health News is a national newsroom that produces in-depth journalism about health issues and is one of the core operating programs at KFF — the independent source for health policy research, polling, and journalism.

The big reveal is less than two months away, but there are already some clues about next year’s raise.

For people who reach retirement without much savings, Social Security can be a true lifeline. And it’s people in that situation who tend to be very reliant on the program’s cost-of-living adjustments (COLAs).

Social Security benefits are eligible for a COLA each year. That doesn’t mean they’re guaranteed to get one, though.

Image source: Getty Images.

If there’s no rise in inflation from one year to the next, benefits don’t increase. Thankfully, though, the worst thing that happens is that they stay put. Social Security benefits can’t be adjusted downward, even if there’s a drop in inflation year over year.

At this point, many Social Security recipients are eager to know what raise they’ll be getting in 2026. And unfortunately, it’s too soon to have an official answer.

Social Security COLAs are based on third-quarter inflation data. This means that until data from September comes in, a COLA can’t be calculated. It’s for this reason that the Social Security Administration won’t be able to announce a COLA until Oct. 15.

However, based on inflation data so far, there are clues as to what year’s COLA might be. Whether you’re happy with the number, though, depends on how you look at things.

What we know about 2026’s Social Security COLA so far

In 2025, Social Security recipients saw their benefits increase by 2.5%. And many seniors were unhappy with that small a raise.

So far, next year’s COLA is potentially looking to be more promising. The Senior Citizens League, an advocacy group, is estimating that 2026’s raise will come in at 2.7%.

Of course, this number could wiggle upward or downward, depending on what inflation has in store for August and September. But either way, there’s a good chance seniors on Social Security will get a slightly larger raise in 2026 than they did this year.

Should you be happy with a 2.7% COLA?

That depends. On one hand, it’s higher than this year’s raise, and it’s not nothing. There have been many COLAs in the past that were much smaller (including a number of 0% COLA years).

On the other hand, 2.7% is hardly a large boost. If you’ve been struggling to keep up with your living expenses, you may find that a 2.7% Social Security COLA doesn’t do all that much for you.

But there’s another silver lining to a 2.7% COLA, or something in that vicinity. A moderate COLA is an indication that inflation isn’t rising at such a rapid pace.

There’s fear that in the coming months, tariffs will drive living costs up — not just for seniors, but Americans on a whole. If next year’s COLA ends up somewhere in the ballpark of 2.7%, it will be an indication of economic stability.

Think about your lifestyle carefully if you’re COLA-dependent

All told, you’ll have to wait until mid-October to see what the official word is on next year’s COLA. But if you’re worried it won’t be enough, it may be time to reassess your financial situation.

Think about the things you spend money on and the value they bring you. You may not be able to cut back on food or electricity, but you may be able to sell a nicer car and replace it with a cheaper one. Or you may be able to give up a car altogether if you live in a walkable neighborhood and no longer have a job to commute to on a daily basis.

Another thing worth considering is part-time work if you’re able to do it. Not only might that give you something to do with your time, but it could also improve your finances a lot more than a Social Security COLA — even a larger one.

VICK Hope has spoken out for the first time since welcoming her son last month.

The DJ, who is married to Calvin Harris, shared a series of new pictures of her baby boy and told fans she was “utterly besotted.”

2

Vick Hope has returned to social media after giving birthCredit: instagram

2

The star shared some stunning pics with her sonCredit: instagram

Alongside the stunning images her home birth in Ibiza, where the couple have a house, she said: “Our beloved baby boy Micah Nwosu Wiles completed his journey to us on Sunday 20th July in a beautiful, powerful home birth here in Ibiza, surrounded by love and nature and chickens.

“Emerging from our little newborn bubble to say happy first month Micah, you are magical and we are so utterly besotted with you.”

At the start of August, Calvin revealed Radio 1 star Vic had given birth with his own post.

He wrote: “20th of July our boy arrived. Micah is here!

“My wife is a superhero and I am in complete awe of her primal wisdom!

The new account comes as Trump has three times delayed implementing a ‘sell or ban’ law for the Chinese-owned app.

The White House has launched an official TikTok account, even as the future of the Chinese-owned social media app in the United States remains uncertain due to legislation passed by the US Congress last year.

The official White House account’s first post on Tuesday was a 27-second video featuring a voiceover from President Donald Trump, saying: “Every day I wake up determined to deliver a better life for the People all across this nation. I am your voice.”

The account’s description read: “Welcome to the Golden Age of America”.

TikTok, which remains owned by Chinese technology company ByteDance, is popular among young people, and has an estimated 170 million users in the US.

Trump has so far delayed the implementation of a 2024 law that ordered TikTok to either to sell to non-Chinese buyers or be banned in the US, with three 90-day extensions.

The US House of Representatives voted 352 to 65 in favour of the “sell or ban” bill in March 2024, with widespread support from both Republicans and Democrats.

The latest extension delaying the ban is due to expire in early September.

“My Administration has been working very hard on a Deal to SAVE TIKTOK, and we have made tremendous progress,” Trump posted on the Truth Social network, which he owns, in April.

Few representatives questioned the bill to ban TikTok at the time it was passed, although then-Democratic representative Barbara Lee asked why only one company was being singled out in an attempt to address problems that relate to social media companies more broadly.

“Rather than target one company in a rushed and secretive process, Congress should pass comprehensive data privacy protections and do a better job of informing the public of the threats these companies may pose to national security,” Lee had posted on the social media platform X.

Although the vast majority of both Democratic and Republican representatives supported the “sell or ban” bill, many members of both parties have used the TikTok platform for campaigning and official communications.

Both Democratic nominee Kamala Harris and Republican nominee Trump used the app to campaign in the 2024 Presidential election.

On Tuesday, the US state of Minnesota joined a wave of states suing TikTok, alleging the social media giant preys on young people with addictive algorithms that trap them into becoming compulsive consumers of its short videos.

Minnesota is also among dozens of US states that have sued Meta Platforms for allegedly building features into Instagram and Facebook that addict people. The messaging service Snapchat and the gaming platform Roblox are also facing lawsuits by some other states alleging harm to children.

Jackie Chan wielding panda bear plushies at the 89th Academy Awards. Brad Pitt serving duck face at the 92nd. Anya Taylor-Joy’s otherworldly hair flip just last year. These are some of the most iconic Glambot videos shot by director Cole Walliser, who has been operating E!’s high-speed red carpet camera, a staple of awards season, since 2016.

It was a much different entertainment landscape then, before #MeToo and #AskHerMore, the latter of which Walliser says he’s inoculated from by virtue of the slo-mo clips the Glambot generates. “For better or worse, it doesn’t allow me to ask more!” he chuckles from his Venice Beach office six weeks out from this year’s Emmys, which will be Walliser’s 10th, though he admits he’s ignorant of the nominees. “I try to stay tuned out to who’s nominated and who’s coming because I don’t want to get nervous,” he tells The Envelope.

Walliser, whose résumé includes music videos for Pink, Katy Perry and Tinashe and commercials for CoverGirl cosmetics, saw early on with Glambot that celebrity culture was poised to break out beyond red carpet telecasts and tabloid magazines: “If I look forward five years, what’s the climate going to be?” he recalls thinking. “It was very clear that it was going to be more on socials. So I thought, ‘If I start now I can be [ahead] of the curve.’”

Nor is he concerned about the growing presence of influencers in the awards space, whether in the form of now-regular campaign stops like “Hot Ones” and “Chicken Shop Date” to the red carpet itself. After all, Glambot is the ultimate short-form content, coming in at one second apiece, and helped pave the way for such successors.

“Part of what people gravitate to with the Glambot is the candid [nature of it],” Walliser says. “There’s a barrier that is broken down that people seem to enjoy.”

It took him a few years to arrive at the synergy between slow-motion clips and behind-the-scenes content that gives the Glambot a second life on social media during the six months outside of the awards season churn.

“It happened organically,” Walliser says, when he asked his assistant to be prepared to take a photo of him and Chan, whom Walliser grew up watching in Vancouver, if the opportunity arose. Ultimately, “it didn’t feel right, so I didn’t ask for a picture.” But unknown to Walliser, his assistant had been surreptitiously filming footage of Walliser directing Chan. He asked her to do it a few more times with other big celebrities. “Seeing how it works in real time was kind of interesting, so I cut it together and put it [online].

“It wasn’t until the 2020 awards season that I really dialed into what the behind-the-scenes content would be,” he continues. “Then the pandemic hit, so I was at home editing my footage and putting it on socials, and that’s when it exploded.”

Now the rise of TikTok and influencers has changed celebrities’ relationship with social media and the entertainment ecosystem at large. The Glambot remains, but it jostles for red carpet real estate alongside streamers and indeed celebs themselves, revealing their looks on Instagram or filming “Get Ready With Me” videos for fashion glossies like “Vogue” and “Elle.”

Does Walliser think the Glambot will go the way of “E! News”?

“Until celebrities are doing their at-home Glambots as good as I am on the red carpet, there’s still job security!” he says with a laugh. Still, the collaboration function on Instagram has been a godsend. “There was a switch when [celebrities] started going, ‘How do I get this? I want to post it.’”

Walliser’s employer’s flagship pop culture program was canceled last month after 32 years on the air, which he calls an “entertainment tragedy.” But whether exemplified by media companies’ pivot to video, then back to print, then back to video again, or broadcasting conglomerates’ mergers and spin-offs, Walliser believes the show, or at least the service it performs, could make a comeback.

“I think at some point we’re going to revalue these information curators that we trust and love because there’s too much content to do it on our own,” he says.

In the meantime, Walliser exudes serenity as he warms up for the Emmys before the hectic triple whammy of the Golden Globes, the Grammys and the Academy Awards in the new year: “I don’t have a life until after the Oscars.”

Until then, he’ll be hoping to capture the bold-faced names who’ve so far eluded the Glambot, including Rihanna, Leonardo DiCaprio, Bradley Cooper and Beyoncé. There’s always a chance — Bey’s Christmas Day NFL halftime performance is nominated for four Emmys.

Indeed, Wissa has been expecting the Bees to agree his move to Tyneside this week after the west London side completed the signing of Dango Ouattara from Bournemouth.

However, according to sources, Brentford are still hesitating in allowing Wissa to leave amid suggestions they now value him above their original £40m asking price.

Reports suggest Brentford now value Wissa, who did not feature for the club during pre-season, at £60m.

As a result, the ongoing conflict between Wissa and Brentford has escalated, with the forward removing all photographs of him playing or training for the club from his official Instagram page.

Tottenham are also interested, but as things stand Newcastle’s move is more advanced. It now remains to be seen whether Brentford sanction his sale before the transfer deadline.

Wissa has scored 49 goals in 149 appearances for the Bees.

In April 2025, the Human Rights Court in Kenya issued an unprecedented ruling that it has the jurisdiction to hear a case about harmful content on one of Meta’s platforms. The lawsuit was filed in 2022 by Abraham Meareg, the son of an Ethiopian academic who was murdered after he was doxxed and threatened on Facebook, Fisseha Tekle, an Ethiopian human rights activist, who was also doxxed and threatened on Facebook, and Katiba Institute, a Kenyan non-profit that defends constitutionalism. They maintain that Facebook’s algorithm design and its content moderation decisions made in Kenya resulted in harm done to two of the claimants, fuelled the conflict in Ethiopia and led to widespread human rights violations within and outside Kenya.

The content in question falls outside the protected categories of speech under Article 33 of the Constitution of Kenya and includes propaganda for war, incitement to violence, hate speech and advocacy of hatred that constitutes ethnic incitement, vilification of others, incitement to cause harm and discrimination.

Key to the Kenyan case is the question whether Meta, a US-based corporation, can financially benefit from unconstitutional content and whether there is a positive duty on the corporation to take down unconstitutional content that also violates its Community Standards.

In affirming the Kenyan court’s jurisdiction in the case, the judge was emphatic that the Constitution of Kenya allows a Kenyan court to adjudicate over Meta’s acts or omissions regarding content posted on the Facebook platform that may impact the observance of human rights within and outside Kenya.

The Kenyan decision signals a paradigm shift towards platform liability where judges determine liability by solely asking the question: Do platform decisions observe and uphold human rights?

The ultimate goal of the Bill of Rights, a common feature in African constitutions, is to uphold and protect the inherent dignity of all people. Kenya’s Bill of Rights, for example, has as its sole mission to preserve the dignity of individuals and communities and to promote social justice and the realisation of the potential of all human beings. The supremacy of the Constitution also guarantees that, should there be safe harbour provisions in the laws of that country, they would not be a sufficient liability shield for platforms if their business decisions do not ultimately uphold human rights.

That a case on algorithm amplification has passed the jurisdiction hearing stage in Kenya is a testament that human rights law and constitutionality offer an opportunity for those who have suffered harm as a result of social media content to seek redress.

Up to this point, the idea that a social media platform can be held accountable for content on its platform has been dissuaded by the blanket immunity offered under Section 230 of the Communications Decency Act in the US, and to a lesser extent, the principle of non-liability in the European Union, with the necessary exceptions detailed in various laws.

For example, Section 230 was one of the reasons a district judge in California cited in her ruling to dismiss a case filed by Myanmar refugees in a similar claim that Meta had failed to curb hate speech that fuelled the Rohingya genocide.

The aspiration for platform accountability was further dampened by the US Supreme Court decision in Twitter v Taamneh, in which it ruled against plaintiffs who sought to establish that social media platforms carry responsibility for content posted on them.

The immunity offered to platforms has come at a high cost, especially for victims of harm in places where platforms do not have physical offices.

This is why a decision like the one by the Kenyan courts is a welcome development; it restores hope that victims of platform harm have an alternative route to recourse, one that refocuses human rights into the core of the discussion on platform accountability.

The justification for safe harbour provisions like Section 230 has always been to protect “nascent” technologies from being smothered by the multiplicity of suits. However, by now, the dominant social media platforms are neither nascent nor in need of protection. They have both the monetary and technical wherewithal to prioritise people over profits, but choose not to.

As the Kenyan cases cascade through the judicial process, there is cautious optimism that constitutional and human rights law that has taken root in African countries can offer a necessary reprieve for platform arrogance.

Mercy Mutemi represents Fisseha Tekle in the case outlined in the article.

The views expressed in this article are the author’s own and do not necessarily reflect Al Jazeera’s editorial stance.

State Department move comes as Israel’s war and induced-famine in Gaza reach new extremes, with 61,827 killed so far.

The United States has announced that it is halting all visitor visas for people from Gaza pending a “a full and thorough” review, a day after social media posts about Palestinian refugees sparked furious reactions from right-wingers.

The Department of State’s move on Saturday came a day after far-right activist and Trump ally Laura Loomer posted on X that Palestinians “who claim to be refugees from Gaza” entered the US via San Francisco and Houston this month.

“How is allowing for Islamic immigrants to come into the US America First policy?” she said on X in a later post, going on to report further Palestinian arrivals in Missouri and claiming that “several US Senators and members of Congress” had texted her to express their fury.

Republican lawmakers speaking publicly about the matter included Chip Roy of Texas, who said he would inquire about the matter, and Randy Fine of Florida, who described the alleged arrivals as a “national security risk”.

By Saturday, the State Department announced it was stopping visas for “individuals from Gaza” while it conducted “a full and thorough review of the process and procedures used to issue a small number of temporary medical-humanitarian visas in recent days”. It did not provide a figure.

All visitor visas for individuals from Gaza are being stopped while we conduct a full and thorough review of the process and procedures used to issue a small number of temporary medical-humanitarian visas in recent days.

The US issued 640 visas to holders of the Palestinian Authority travel document in May, according to the Reuters news agency. B1/B2 visitor visas permit Palestinians to seek medical treatment in the US.

Loomer greeted Saturday’s State Department announcement with glee.

“It’s amazing how fast we can get results from the Trump administration,” she said on Saturday, though she later posted that more needed to be done to “highlight the crisis of the invasion happening in our country”.

While I appreciate the State Department and @marcorubio issuing this statement, I want to press even harder to highlight the crisis of the invasion happening in our country.

The visas and arrivals of GAZANS to US airports isn’t new. This has been drastically increasing in speed… https://t.co/mI5APTairz

The decision to cut visas comes as Israel intensifies its attacks on Gaza, where at least 61,827 people have been killed in the past 22 months, with the United Nations warning that “widespread starvation, malnutrition and disease” are driving a rise in famine-related deaths.

Israeli Prime Minister Benjamin Netanyahu has been pushing to seize Gaza City as part of a takeover of the Strip, forcibly displacing hundreds of thousands of Palestinians to concentration zones.

United States President Donald Trump has marked the 90th anniversary of Social Security with a defence of his administration’s policies toward the programme — and attacks on his Democratic rivals.

On Thursday, Trump signed a presidential proclamation in the Oval Office, wherein he acknowledged the “monumental” importance of the social safety-net programme.

“I recommit to always defending Social Security,” the proclamation reads.

“To this day, Social Security is rooted in a simple promise: those who gave their careers to building our Nation will always have the support, stability, and relief they deserve.”

But Trump’s second term as president has been dogged by accusations that he has undermined programmes like Social Security in the pursuit of other agenda items, including his restructuring of the federal government.

What is Social Security?

Social Security in the US draws on payroll taxes to fund monthly payments to the elderly, the spouses of deceased workers, and the disabled. For many recipients, the payouts are a primary source of income during retirement.

The programme is considered widely popular: In 2024, the Pew Research Center found that 79 percent of Americans believe Social Security should not be cut in any way.

Additionally, four out of 10 people surveyed sided with the view that Social Security should be expanded to include more people and more benefits.

But the programme faces significant hurdles to its long-term feasibility.

Last year, the Social Security Administration (SSA) published a report that found the costs for old-age, disability and survivors’ insurance outstripped the programmes’ income.

It noted that the trust funds fuelling those programmes “are projected to become depleted during 2033” if measures are not taken to reverse the trend.

At Thursday’s Oval Office appearance, Trump sought to soothe those concerns, while taking a swipe at the Democratic Party.

“ You keep hearing stories that in six years, seven years, Social Security will be gone,” Trump said.

“And it will be if the Democrats ever get involved because they don’t know what they’re doing. But it’s going to be around a long time with us.”

He added that Social Security was “going to be destroyed” under his Democratic predecessor, former President Joe Biden, a frequent target for his attacks.

Criticism of Trump’s track record

But Trump himself has faced criticism for weakening Social Security since returning to the White House for a second term in January.

Early on, Trump and his then-adviser Elon Musk laid out plans to slash the federal workforce and reduce spending, including by targeting the Social Security Administration (SSA).

In February, the Social Security Administration said it would “reduce the size of its bloated workforce and organizational structure”, echoing Trump and Musk’s rhetoric.

The projected layoffs and incentives for early retirement were designed to cut Social Security’s staff from 57,000 to 50,000, a 12.3-percent decrease.

Under Trump, the Department of Government Efficiency (DOGE) has also announced plans to pare back Social Security’s phone services, though it has since backtracked in the face of public outcry.

In addition, Musk and Trump have attacked Social Security’s reputation, with the former adviser telling podcast host Joe Rogan, “Social Security is the biggest Ponzi scheme of all time.”

The two men even claimed Social Security is paying benefits to millions of long-dead individuals, though critics point out that those claims do not appear to be true.

The COBOL programming system used by the Social Security Administration marks incomplete entries with birthdates set 150 years back, according to the news magazine Wired. Those entries, however, generally do not receive benefits.

The Office of the Inspector General overseeing the Social Security Administration has repeatedly looked into these older entries. It confirmed that these entries are not active.

“We acknowledge that almost none of the numberholders discussed in the report currently receive SSA payments,” a report from 2023 said.

It also indicated that the Social Security Administration would have to pay between $5.5m and $9.7m to update its programming, though the changes would yield “limited benefits” in the fight against fraud.

Still, Trump doubled down on the claim that dead people were receiving benefits on Thursday.

“We had 12.4 million names where they were over 120 years old,” Trump said. “There were nearly 135,000 people listed who were over 160 years old and, in some cases, getting payments. So somebody’s getting those payments.”

Questions after ‘One Big Beautiful Bill’

Critics have also questioned whether Trump’s push to cut taxes will have long-term effects that erode Social Security.

In July, Trump’s signature piece of legislation, the so-called One Big Beautiful Bill Act (OBBBA), cemented his 2017 tax cuts. It also increased the tax deductions for earners who rely on tips or Social Security benefits.

But groups like the Committee for a Responsible Federal Budget, a bipartisan think tank, estimate that the One Big Beautiful Bill Act will shorten the timeline for Social Security’s insolvency.

“The law dictates that when the trust funds deplete their reserves, payments are limited to incoming revenues,” the committee said in late July.

“For the Social Security retirement program, we estimate that means a 24 percent benefit cut in late 2032, after the enactment of OBBBA.”

Still, Trump has repeatedly promised to defend Social Security from any benefit cuts. He reiterated that pledge in Thursday’s appearance.

“American seniors, every single day, we’re going to fight for them. We’re going to make them richer, better, stronger in so many different ways,” Trump said.

“But Social Security is pretty much the one that we think about, and we love it, and we love what’s happening with it, and it’s going to be good for 90 years and beyond.”

More than 69.9 million Americans received Social Security benefits as of July.

The challenge brought on by the trade group alleges that the age verification law is a violation of free speech

The United States Supreme Court has declined to put on hold a Mississippi law requiring that users of social media platforms verify their age and that minors have parental consent.

The high court made the decision on Thursday not to accept the challenge by NetChoice, a trade group that included tech giants such as Meta, Facebook and Instagram’s parent company, Alphabet which owns YouTube, and Snapchat.

The justices denied a request to block the law while the Washington-based tech industry trade association’s legal challenge to the law, which, it argues, violates the US Constitution’s protections against government abridgement of free speech, plays out in lower courts.

Justice Brett Kavanaugh in a statement about the court’s order said the Mississippi law was likely unconstitutional, but that NetChoice had not met the high bar to block the measure at this early stage of the case.

In a statement, Paul Taske, co-director of the NetChoice Litigation Center, said Kavanaugh’s view “makes clear that NetChoice will ultimately succeed” in its challenge. Taske called the Supreme Court’s order “an unfortunate procedural delay.”

NetChoice had turned to the Supreme Court after the New Orleans-based 5th US Circuit Court of Appeals let the law take effect even though a judge found it likely runs afoul of the First Amendment.

NetChoice sued in federal court in 2024 in a bid to invalidate the law, which was passed unanimously in the state legislature amid concern by lawmakers about the potential negative effects of social media use on the mental health of children.

Its emergency request to the justices marked the first time the Supreme Court was asked to consider a social media age-verification law.

The law requires that a social media platform obtain “express consent” from a parent or guardian of a minor before a child can open an account. It also states that regulated social media platforms must make “commercially reasonable” efforts to verify the age of users.

Under the law, the state can pursue civil penalties of up to $10,000 per violation as well as criminal penalties under Mississippi’s deceptive trade practices law.

Multiple lawsuits

US District Judge Halil Suleyman Ozerden in Gulfport, Mississippi, last year blocked Mississippi from enforcing the restrictions on some NetChoice members.

Ozerden issued a second order in June pausing the rules against those members, including Meta and its Instagram and Facebook platforms, Snapchat and YouTube.

The 5th Circuit on July 17 issued a one-sentence ruling that paused the judge’s order, without explaining its reasoning.

Courts in seven states have preliminarily or permanently blocked similar measures, according to NetChoice.

Some technology companies are separately battling lawsuits brought by US states, school districts and individual users alleging that social platforms have exacerbated mental health problems. The companies have denied wrongdoing.

NetChoice said the social media platforms of its members already have adopted extensive policies to moderate content for minors and provide parental controls.

In its request to the Supreme Court, the state told the justices that age-verification and parental consent requirements “are common ways for states to protect minors”.

In May, Texas passed a law requiring Apple and Alphabet’s Google to verify the age of users of their app stores.

Russia accuses popular messaging apps of facilitating crime and sabotage as Moscow’s online restrictions tighten amid war in Ukraine.

Russia has announced restrictions on voice calls made on the WhatsApp and Telegram messaging apps, the latest moves by Moscow to tighten its control over the internet.

The curb on calls is set to impact WhatsApp’s estimated 96 million monthly users in Russia and Telegram’s more than 89 million users, according to Russian media monitoring service Mediascope.

In a statement on Wednesday, Russia’s media and internet regulator, Roskomnadzor, justified the measure as necessary for fighting crime.

“According to law enforcement agencies and numerous appeals from citizens, foreign messengers Telegram and WhatsApp have become the main voice services used to deceive and extort money, and to involve Russian citizens in sabotage and terrorist activities,” the regulator said.

“Repeated requests to take countermeasures have been ignored by the owners of the messengers,” it said.

Moscow wants the online messaging services to provide access to user data upon request from law enforcement.

“Access to calls in foreign messengers will be restored after they start complying with Russian legislation,” Roskomnadzor said.

While authorities said only voice calls on the platforms were restricted, users in Russia also reported that video calls were also affected.

Since the beginning of Russia’s full-scale invasion of Ukraine in 2022, Moscow has been expanding control over the Russian part of the internet. Security services have frequently claimed that Ukraine was using Telegram to recruit people or commit acts of sabotage in Russia.

The Russian government adopted a law last month punishing online users for searching content deemed illicit by authorities. Plans are also in place for popular messaging services to be replaced by a domestic Russian app called Max, which critics fear will allow authorities access to the data.

A WhatsApp spokesperson said in a statement that the encrypted messaging app “defies government attempts to violate people’s right to secure communication, which is why Russia is trying to block it from over 100 million Russian people”.

In a statement sent to the AFP news agency, Telegram said that it “actively combats misuse of its platform, including calls for sabotage or violence, as well as fraud”, and removes “millions of pieces of harmful content every day”.

Telegram, which was developed by Russian tech entrepreneur Pavel Durov, faces longstanding accusations in several countries, including Russia, of not doing enough against criminal users.

We claim to value privacy, but surrender it daily, often without knowing.

We say we care about privacy, but this episode examines whether our actions reflect that.

In The Privacy Paradox, we unravel the disconnect between our stated values and our digital behaviour.

From mindless clicks to routine app permissions, this episode exposes how everyday online habits feed a vast, invisible data economy, often without our knowledge or consent.

Franklin Delano Roosevelt had a clear mind about the value of Social Security on Aug. 14, 1935, the day he signed it into law.

“The civilization of the past hundred years, with its startling industrial changes, has tended more and more to make life insecure,” he said in the Oval Office. “We can never insure 100 per cent of the population against 100 per cent of the hazards and vicissitudes of life, but we have tried to frame a law which will give some measure of protection to the average citizen and to his family against … poverty-ridden old age.”

He called it a “cornerstone in a structure which is being built but is by no means complete.” FDR envisioned further programs to bring relief to the needy and healthcare for all Americans. Some of that happened during the following nine decades, but the structure is still incomplete. And now, as Social Security observes the 90th anniversary of that day, the program faces a crisis.

This is about whether we redefine a relationship between individuals and government that we’ve had since 1935. We say that what was done was wrong then, and it’s wrong now.

— Cato’s Michael Tanner sets forth the rationale for killing Social Security (in 2005)

If there are doubts about whether Social Security will survive long enough to observe its centennial, those have less to do with its fiscal challenges, the solutions of which are certainly within the economic reach of the richest nation on Earth. They have more to do with partisan politics, specifically the culmination of a decades-long GOP project to dismantle the most successful, and the most popular, government assistance program in American history.

From a distance, the raids on the program’s customer service infrastructure and the security of its data mounted by Elon Musk’s DOGE earlier this year looked somewhat random.

Newsletter

Get the latest from Michael Hiltzik

Commentary on economics and more from a Pulitzer Prize winner.

You may occasionally receive promotional content from the Los Angeles Times.

Fueled by abject ignorance about how the program worked and what its data meant, DOGE set in place plans to cut the program’s staff by 7,000, or 12 percent, and to close dozens of field offices serving Social Security applicants and beneficiaries. This at a time when the Social Security case load is higher than ever and staffing had already approached a 50-year low.

That has been conservatives’ long-term plan — make interactions with Social Security more involved, more difficult and more time-consuming in order to make it seem ever less relevant to average Americans’ lives. Once that happened, the public would be softened up to accept a privatized retirement system.

Get the inefficient government off the backs of the people, the idea goes, so Wall Street can saddle up. George W. Bush’s privatization plan, indeed, was conceived and promoted by Wall Street bankers, who thirsted for access to the trillions of dollars passing through the system’s hands.

This was never much of a secret, but it simmered beneath the surface. But Treasury Secretary Scott Bessent, speaking at a July 30 event sponsored by Breitbart News, said the quiet part out loud. Referring to a private savings account program enacted as part of the GOP budget reconciliation bill Trump signed July 4, Bessent said, “In a way, it is a back door for privatizing Social Security.”

The private accounts are to be jump-started with $1,000 deposits for children born this year through 2028, to be invested in stock index mutual funds; families can add up to $5,000 annually in after-tax income, with withdrawals beginning when the child reaches 18, though in some cases incurring a stiff penalty.

I asked the Treasury Department for a clarification of Bessent’s remark, but didn’t receive a reply. Bessent, however, did try to walk the statement back via a post on X in which he stated that the Trump accounts are “an additive benefit for future generations, which will supplement the sanctity of Social Security’s guaranteed payments.”

Sorry, Mr. Secretary, no sale. You’re the one who talked about “privatizing Social Security” at the Breitbart event. You’re stuck with it.

Plainly, an “additive” benefit would have nothing to do with Social Security. How it would “supplement the sanctity” of Social Security benefits isn’t apparent from Bessent’s statement, or the law. Still, we can parse out the implications based on the long history of conservative attacks on the program.

In 1983, the libertarian Cato Journal published a paper by Stuart Butler and Peter Germanis, two policy analysts at the right-wing Heritage Foundation, titled “Achieving a ‘Leninist’ Strategy—i.e., for privatizing Social Security. From Lenin they drew the idea of mobilizing the working class to undermine existing capitalist structures.

Cato’s “Leninist” strategy paper explicitly advocated encouraging workers to opt out of Social Security by promising them a payroll tax reduction if they put the money in a private account.

IRAs, the authors asserted, would acclimate Americans to entrusting their retirements to a privatized system. They advocated an increase in the maximum annual contribution and its tax deductibility.

“The public would gradually become more familiar with the private option,” they wrote. “If that did happen, it would be far easier than it is now to adopt the private plan as their principal source of old-age insurance and retirement income.” In other words, it would provide a backdoor for privatizing Social Security.

(Germanis has since emerged as a cogent critic of conservative economics. Butler served at Heritage until 2014 and is currently a scholar in residence at the Brookings Institution; he told me in March that he still believes in parallel systems of private retirement savings as we have today, but as “add on” savings rather than a substitute for Social Security.)

Cato, a think tank co-founded by Charles Koch, has never relinquished its quest to privatize Social Security; the notion still occupies pride of place on the institution’s web page devoted to the program.

In 2005, when I attended a two-day conference on the topic at Cato’s Washington headquarters, Michael D. Tanner, then the chair of Cato’s Social Security task force, explained that Cato wasn’t concerned so much with the system’s fiscal and economic issues as with its politics. Its goal, he stated frankly, was to unmake FDR’s New Deal.

“This is about whether we redefine a relationship between individuals and government that we’ve had since 1935,” he told me. “We say that what was done was wrong then, and it’s wrong now. Our position is that people need to be responsible for their own lives.”

Yet forcing dramatic change on a program so widely trusted and appreciated is a heavy lift. That’s why Republicans have tried to downplay their intentions. Back in 2019, for instance, Sen. Joni Ernst (R-Iowa) talked about the need to hold discussions about Social Security’s future “behind closed doors.”

Secrecy was essential, Ernst said, “so we’re not being scrutinized by this group or the other, and just have an open and honest conversation about what are some of the ideas that we have for maintaining Social Security in the future.”

As I observed at the time, that was a giveaway: The only time politicians take actions behind closed doors is when they know the results will be massively unpopular. Raising taxes on the rich to pay for Social Security benefits? That discussion can be held in the open, because the option is decisively favored in opinion polls. Cut benefits? That needs to be done in secret, because Americans overwhelmingly oppose it.

Curiously, Trump and his fellow Republicans seem to think that attacking Social Security is an electoral winner. Possibly they’ve lost sight of the program’s importance to the average American.

Among Social Security beneficiaries age 65 and older, 39% of men and 44% of women receive half their income or more from Social Security. In the same cohort, 12% of men and 15% of women rely on Social Security for 90% or more of their income.

Notwithstanding that reality, Commerce Secretary Howard Lutnick recently asserted that delays in sending out Social Security checks or bank deposits would be no big deal.

“Let’s say Social Security didn’t send out their checks this month,” Lutnick said. “My mother-in-law, who’s 94 — she wouldn’t call and complain…. She’d think something got messed up, and she’ll get it next month.” He claimed that only “fraudsters” would complain.

I had a different take. Mine was that even a 24-hour delay in benefit payments would have a cataclysmic fallout for the Republican Party. It would be front-page news coast to coast. There would be nowhere for them to hide.

While bringing misery to millions of Americans, a delay — which would be unprecedented since the first checks went out in 1940 — would be a gift for Democrats, if they knew how to use it.

Where will we go from here? The current administration has already done damage to this critically-important program. An acting commissioner Trump installed briefly interfered with the enrollment process for infants born in Maine—an important procedure to ensure that government benefits continue to flow to their families—because the state’s governor had pushed back against Trump in public.

In July, the newly-appointed Social Security commissioner, Frank Bisignano, allowed a false and flagrantly political email to go out to beneficiaries and to be posted on the program’s website implying that the budget reconciliation bill relieved most seniors of federal income taxes on their benefits. It did nothing of the kind.

To the extent that Social Security may face a fiscal reckoning in the next decade, the most effective fix is well-understood by those familiar with the program’s structure. It’s removing the income cap on the payroll tax, which tops out this year at $176,100 in wage income.

Up to that point, wages are taxed at 12.4%, split evenly between workers and their employers. Above the ceiling, the tax is zero. Remove the cap, and make capital gains, dividends and interest income subject to the tax, and Social Security will remain fully solvent into the foreseeable future.

Trump and his fellow Republicans don’t seem to understand how most Americans view Social Security: as an “entitlement,” not because they think they’re getting something for nothing, but because they know they’ve paid for it all their working lives.

As much as the system’s foes would like it to go away, as long as the rest of us remain vigilant against efforts to “redefine a relationship between individuals and government” established in 1935, we will be able to celebrate its 100th anniversary 10 years from now, in 2035.

U.S. President Donald Trump speaks during a press conference in the James S. Brady briefing room at the White House in Washington, D.C., on Monday, the same day he posted on Truth Social that gold will not face tariffs. Photo by Bonnie Cash/UPI | License Photo

Aug. 11 (UPI) — President Donald Trump said Monday in a Truth Social post that there will be no tariffs on gold.

The post said: “A Statement from Donald J. Trump, President of the United States of America: Gold will not be tariffed!”

He did not elaborate further.

Gold futures closed 2.48% lower at $3,404.70 per ounce after the announcement, CNBC reported.

The precious metal hit a record high Friday, after U.S. Customs and Border Protection ruled that 1 kilogram and 100 ounce gold bars from Switzerland would face Trump’s 39% tariff against the country.

These gold bars are used to back contracts on The Commodity Exchange, or COMEX. The exchange is the main futures market for gold, silver and other metals.

The ruling would have applied to any country exporting gold bars to the United States, according to the Swiss Precious Metal Association. So gold bars would have been subject to the prevailing U.S. tariff rate against their country of origin.

The Swiss Precious Metal Association warned Friday that the customs ruling “may negatively impact the international flow of physical gold.”

“The imposition of tariffs on these gold cast products makes it economically unviable to export them to the U. S., thereby eliminating any future trade deficit arising from gold exports,” the press release said.

A sprawling social club centering on racquet sports — the ubiquitous pickleball and rising padel, a blend of tennis and squash — is making its way to downtown L.A. next summer.

With the cheeky name Ballers, the club will be housed in the former Macy’s building at The Bloc, which spans 100,000 square feet. It will be equipped with 18 pickleball courts and four padel courts — marking the first pickleball and padel courts to open in the DTLA area, according to the founders. The club will also feature five golf simulators, two soccer pitches, a high-end retail shop, two full bars, a restaurant and a recovery zone outfitted with a sauna and cold plunge area.

Membership packages for the social sports club will start at $99 per month and come with perks such as advanced booking windows, access to the recovery lounge and invites to exclusive events. Nonmembers will still be welcome to enjoy the social spaces and book courts for fees between $15 to $25 per hour.

“[We wanted] to bring the country club to the city in an elevated, fun way,” said Ballers CEO David Gutstadt.

Ballers L.A. will be the third Ballers location — the first will debut in Philadelphia later this month and the second will open in Boston later this year. The founders, who are behind hospitality projects like the Fitler Club and Equinox Hotels, have plans to expand to 50 locations across the country within the next seven to 10 years. Ballers has received financial backing from an all-star roster of professional athletes including tennis icons Andre Agassi, Kim Clijsters and Sloane Stephens, pickleball champion Connor Garnett and 76ers star Tyrese Maxey.

Earlier this year, Macy’s at the Bloc was deemed one of the retailer’s “underproductive” locations and closed its doors, leaving downtown L.A. without a department store for the first time in over 150 years. This evolution of the space follows a trend of retail stores transforming into “experiential” spaces — companies are tapping into consumers’ hunger for communal experiences and new hobbies. In 2023, indoor pickleball venue Pickle Pop opened in Santa Monica, in part to try to revive ailing Third Street Promenade.

When designing Ballers’ Los Angeles club, co-founder and chief creative officer Amanda Potter said it was important that the venue be accessible in location and price so that anyone could visit and try the racquet sports.

In addition to sports offerings, the venue will feature a restaurant and two full bars.

(Ballers)

While the popularity of pickleball has skyrocketed since the COVID-19 pandemic, Potter said not everyone is familiar with it, citing a 2023 study by the Association of Pickleball Professionals which found that less than 10 percent of Angelenos had tried the sport that year. “It’s a sport that people are still getting acquainted with, so we don’t want to have that barrier to people trying our sports by saying it’s members-only,” Potter said.

Garnett, who started playing pickleball about three years ago, said he was eager to become involved with the Ballers’ project.

“You don’t have to be great at pickleball to come out here,” he said. “You don’t have to be great at padel. It’s just really an inclusive way to get people active and on their feet.”

While there is no set opening date for Ballers L.A., the founders say it will launch in the late summer of 2026.