STRICTLY pro Lauren Oakley has QUIT social media just a day before the first live show – saying “everyone has feelings”.

The dancer, who is partnered with football manager Jimmy Floyd Hasselbaink this series, urged viewers to not troll the stars.

3

Lauren Oakley has quit social media just a day before the first live showCredit: Louis Wood

3

The pro dancer is partnered with football manager Jimmy Floyd HasselbainkCredit: BBC

Lauren, 34, shared a message with her followers before she takes a break from her X platform while the show is on.

She wrote: “Live show tomorrow. That’s me deleting X for now, have fun everyone. Enjoy the show. Don’t be mean. Everyone has feelings and everyone is trying their best. Think before you type. Love.”

Last series Lauren stepped in for Amy Dowden as her replacement after health concerns and danced withJLSsinger JB Gill.

Taking to the stage for the inaugural Icons Week, the pair blew the judges away and received an incredible 39 points.

Jimmy Kimmel’s emotional Tuesday return to his late-night hosting perch at ABC gave his program its largest audience ever in its regular 11:35 p.m. time period, despite not airing for nearly a quarter of U.S. households.

An average of 6.26 million viewers tuned in to watch “Jimmy Kimmel Live!” as the comedian addressed his suspension that became a free speech cause celebre, according to Nielsen. ABC had pulled the show “indefinitely” starting Sept. 17 following blowback over Kimmel’s remarks about the shooting death of right-wing activist Charlie Kirk.

The only times “Jimmy Kimmel Live!” has scored higher ratings were when it aired special episodes after the Oscars and the Super Bowl. Preliminary numbers for Tuesday’s show didn’t include streaming.

The program delivered strong numbers despite not airing on 60 network affiliates covering 23% of U.S. television households. Television station ownership groups Nexstar and Sinclair kept the program off their ABC-affiliated outlets even as Walt Disney Co.-owned ABC resumed production.

By late Wednesday, 15 million people had watched Kimmel’s monologue and a comedy bit with actor Robert De Niro on YouTube, where ABC made it available shortly after it aired on TV. ABC said a total of 26 million people watched the monologue across YouTube and social media platforms.

Kimmel clearly grasped that his return would be a historic moment in the annals of late-night TV, as his network-imposed hiatus became a global news story and sparked a widespread debate about free speech and the role of government regulators.

He opened with the line, “Before I was interrupted” — the same words “Tonight” show host Jack Paar used in 1960 when he returned from a monthlong walkout. Paar left his program after NBC censors cut a water closet joke from his monologue, which became one of the biggest TV industry controversies of that era.

Kimmel was pulled off the air the same day Federal Communications Commission Chair Brendan Carr took aim at the host’s Sept. 15 monologue, in which Kimmel said MAGA Republicans were using Kirk’s death to “score political points” and were trying to categorize suspected shooter Tyler Robinson as “anything other than one of them.”

Carr, who oversees regulations for broadcast stations, called Kimmel’s remarks “the sickest conduct possible” and called for ABC to act. He threatened to go after TV stations’ licenses if it failed to do so.

During his opening monologue, Kimmel got choked up when he told viewers it was “never my intention to make light of the murder of a young man” when he discussed the right wing’s response to the shooting.

But Kimmel went on to chastise Carr, showing his social media postings in recent years that gave unequivocal support to the 1st Amendment and condemning the censorship of TV hosts and commentators.

Since becoming FCC chair under the Trump administration, Carr has joined the president in denouncing his late-night critics.

While Kimmel was contrite regarding Kirk, he showed no mercy for Trump in the monologue addressing the matter that took much of the show, a clear indication that he won’t be changing his tone. He also continued to promote free speech, saying the government attempts to stifle voices such as his are “un-American” and “so dangerous.”

Kimmel also expressed gratitude to politically-right-leaning politicians and commentators who expressed dismay over his removal from the air, including Ted Cruz and Joe Rogan.

Trump reacted harshly to Kimmel’s return. In a Truth Social post, he said he may file another lawsuit against ABC. The network paid a $16-million settlement last year after “Good Morning America” co-host George Stephanopoulos mistakenly said Trump was found liable of of sexual assault instead of sexual abuse.

A letter signed by several dozen former employees of ABC, which was obtained by The Times, praised Disney Chief Executive Bob Iger’s decision to return Kimmel to the air, but warned “it must be the first step in a concerted effort to defend free speech and press freedom against political intimidation.”

“The $16 million settlement with Donald Trump, combined with the absence of a strong public defense of ABC News journalists under attack, has emboldened Administration efforts to intimidate the press,” said the letter, which included the signatures of former ABC News correspondents Sam Donaldson, Chris Bury, Ned Potter, Judy Muller and Brian Rooney.

Nexstar is still keeping “Jimmy Kimmel Live!” off its ABC affiliates. A Nexstar representative said Wednesday the company is having “productive discussions with executives at the Walt Disney Company, with a focus on ensuring the program reflects and respects the diverse interests of the communities we serve.”

A representative for Sinclair, which preempted “Jimmy Kimmel Live!” in markets such as Seattle and Washington, D.C., said in a statement that the company is also monitoring the situation before deciding to return the program to its ABC station program lineups.

Marlon Wayans is putting up a “defensive run-stopping front” after his latest film received negative reviews from critics.

The actor took to his Instagram account over the weekend to promote his latest film, “HIM,” which hit the big screen Friday, and told fans to form their own opinions on the project. The movie currently holds a 29% score with critics on Rotten Tomatoes.

“An opinion does not always mean it’s everyone’s opinion. Some movies are ahead of the curve,” Wayans said. “Innovation is not always embraced and art is to be interpreted and it’s subjective.”

The post include screen grabs from the Rotten Tomatoes pages of his other movies that have been classified “rotten” by the website but were later embraced by audiences like 2004’s “White Chicks,” the first two films in the “Scary Movie” franchise, 2013’s “A Haunted House” and 1996’s “Don’t Be a Menace to South Central While Drinking Your Juice in the Hood.” The post ends with a screen grab of the “HIM” Rotten Tomatoes page.

“I’ve had a career of making classic movies that weren’t critically received and those movies went on to be CLASSICS. So don’t take anyone’s opinion just go see for yourself,” Wayans added.

So far, audiences have given the film a 58% on Rotten Tomatoes.

The Times film critic, Amy Nicholson, credited the the film for its “stylishly” craftsmanship but said it was lacking plot.

Murdoch will be part of a group of US investors – including Trump allies – trying to take over TikTok’s US operations.

Published On 21 Sep 202521 Sep 2025

Share

United States President Donald Trump has said media executive Lachlan Murdoch will join a group of American investors seeking to take control of TikTok’s operations in the United States.

In an interview on the Fox News programme Sunday Briefing, Trump said the proposed deal would transfer TikTok’s American assets from Chinese parent company ByteDance to US ownership. He described those involved as prominent people and “American patriots”.

Recommended Stories

list of 4 itemsend of list

“I think they’re going to do a really good job,” Trump said, adding that TikTok had helped him expand support among young voters during the 2024 election campaign.

One of the proposed investors – Larry Ellison, the co-founder of the tech firm Oracle – is a prominent Republican donor. Lachlan Murdoch’s father Rupert has backed right-wing causes and parties for decades, but has a complicated relationship with Trump, who is currently suing him.

The initiative would give Trump’s allies in corporate America influence over a platform with about 170 million US users, one of the most widely used apps shaping political and cultural debate.

Lachlan Murdoch, the chief executive of Fox Corp, recently consolidated control of his family’s media empire, which includes Fox News and the Wall Street Journal, after settling a long-running legal dispute with his siblings. Trump said the 94-year-old Rupert Murdoch may himself also be involved in the deal.

Murdoch’s media outlets attract right-leaning audiences, but they have occasionally clashed with Trump. The US president’s lawsuit against Rupert Murdoch and the Wall Street Journal is for defamation over a July report linking him to the late financier and convicted sex offender Jeffrey Epstein. The newspaper has defended its reporting.

Other business figures named by Trump include Dell Technologies CEO Michael Dell, who, along with Ellison, has previously been connected to discussions on TikTok’s future.

US law passed under the administration of former US President Joe Biden requires ByteDance to divest its TikTok operations, with both Democrats and Republicans supporting the legislation due to security concerns that Beijing could have access to American users’ data.

However, the spotlight on TikTok has also been linked to growing support for Palestinians and opposition to Israel among young Americans, with many pro-Israeli politicians blaming the popular app for the shifting tide.

Trump’s Secretary of State Marco Rubio called for a ban on TikTok soon after the beginning of Israel’s war on Gaza, calling the app biased towards anti-Israel content.

Trump had proposed to ban TikTok during his first term as US president, signing two executive orders in August 2020 that were aimed at restricting the app. However, the US president did a U-turn, pledging to “save” the popular app during his 2024 re-election campaign.

The Trump administration has since tied negotiations over TikTok to wider trade talks with China.

China has consistently denied claims by US lawmakers that Beijing pressures apps like TikTok to collect personal information for the state.

It has been a wild year for Social Security so far.

If you’ve been on Social Security for a while, changes to the program may not seem all that unusual to you. Each year, the government makes updates to benefits and the formula used to calculate them. But 2025 hasn’t been an ordinary year. Several unusual changes have already taken place, and a few more are set to go into effect by the end of December.

They may not all affect you, but chances are, at least one will have a pretty significant impact on your budget as we move into 2026.

Image source: Getty Images.

1. The Social Security Fairness Act’s passage

Congress passed the Social Security Fairness Act (SSFA) in January. This law eliminated two longstanding Social Security provisions — the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO) — that had previously reduced the amount of benefits that would be paid to people who received pensions from employers that didn’t pay into Social Security on their behalf.

As a result of this change, many former teachers, firefighters, police officers, and other government workers saw their benefits jump this spring, with some getting an additional $1,000 or more each month.

The Social Security Administration finished making these benefit adjustments back in July. If you were affected, you should have been notified of the change, and you’ve likely already begun receiving your new, larger benefit checks.

2. Overpayment recovery rate increase

In March 2024, the Biden administration made a change to how Social Security dealt with overpayments: If, for some reason, an individual was found to have received more than they were due, the agency would withhold at most 10% of each of their future checks until all of the overpayment was recovered. The goal of spreading out the repayment period this way was to avoid putting unnecessary financial hardship on retirees.

Early in 2025, President Donald Trump reversed that move, reverting the Social Security overpayment recovery rate from 10% per check back to 100%. This gave the government permission to withhold the entirety of your checks until it recouped its money. However, a few weeks later, he cut the recovery rate to 50%.

Overpayments are uncommon, but if this happens to you, losing half your checks for any period could still be devastating. However, if it will be a hardship, you can file a request for a lower repayment recovery rate.

3. The end of paper check delivery

The Social Security Administration announced in July that on Sept. 30, it would stop sending paper checks to beneficiaries. This change will save the government about $0.35 per payment while also improving the speed and security with which funds are distributed.

If you’re currently receiving paper Social Security checks, you can switch to direct deposit into a bank account or request a Direct Express Card. This is a prepaid debit card that the government will automatically load your Social Security benefit onto each month. You can change the method by which you receive your payments by logging into your my Social Security account or by contacting the Social Security Administration.

4. Reduced Social Security benefit taxes for some

Trump’s “big, beautiful bill” made several major changes to the tax code, including adding a new deduction for seniors worth up to $6,000 for single adults and up to $12,000 for married couples. This is on top of the standard deductions for those filing statuses and the existing senior tax deduction.

Contrary to what some sources claimed, this change did not eliminate or modify the existing taxes on Social Security benefits. However, a tax deduction will reduce your taxable income for the year, so you could pay taxes on a little less of your Social Security benefits than you would have before.

5. Cost-of-living adjustment (COLA)

The Social Security Administration will announce the size of its next cost-of-living adjustment (COLA) on Oct. 15. This will take effect with the December 2025 payment, which will go out to beneficiaries in January 2026.

Based on current estimates for U.S. inflation during the third quarter, the COLA will come in at around 2.7%. That would increase the average monthly benefit of $2,008 (as of August) by $54.

Once the COLA is official, you will be able to calculate how much it will add to your 2026 benefits. But you should also get a personalized COLA notice in December. You can use that information to begin planning your budgets for 2026.

There is no single age that applies to all Americans, but you can shoot for the “perfect” age based on your specific set of circumstances.

In 1991, Social Security’sfull retirement age (FRA) was 65, yet the average retirement age in the U.S. was 57. Today, FRA hovers around 67 with the average American retiring at 62.

According to North American Community Hub Statistics (NCHstats), a source of health data, there’s a gap between the expected age of retirement (67) and the actual age (62), often due to health issues, caregiving needs, and layoffs. In other words, despite the desire a person may have to maximize their Social Security benefits, life can get in the way.

Image source: Getty Images.

What is the perfect age to begin collecting Social Security?

Unfortunately, there is no one-size-fits-all answer. The best time for you to retire may differ significantly from the ideal time for a friend, coworker, or family member. What matters is when you’reready to retire.

For example, suppose you’rethe primary earner in your family, and you have a spouse and children who depend on you for financial support. If that’s the case, you may want to maximize the amount they’re eligible to collect in survivors benefits by waiting to retire at FRA or later. Survivors benefits entitle your dependents to continue receiving a percentage of the benefit you were collecting (or would have qualified for) at the time of your death. By retiring earlier, you reduce the amount your family will collect after your passing.

Meanwhile, someone with health complications may decide they want to file for Social Security much sooner. With a shorter life expectancy, they’re more likely to maximize what they get from the program with an early claim.

Discovering the right retirement age for you

The ideal age for you depends mainly on factors like your financial needs, health, and overall retirement goals. Here are a few more scenarios to consider.

Early retirement: You can begin collecting benefits as early as 62, but the sooner you file, the smaller your benefit will be. However, if you need the income to actually retire, 62 may be right for you.

Full retirement age (between 66 and 67): Waiting until this age allows you to receive your full benefit. If you retire before this point, you’ll need to rely exclusively on your retirement savings to cover your expenses for a few years. For many people, waiting until FRA may be just right.

Delayed retirement: If you can put off claiming benefits until age 70, you’ll receive the maximum amount possible based on your work history. This could be the right move if you had a late start saving for retirement, live in a high-cost-of-living area, or want to hold onto more of your savings in order to pass it down to your heirs.

Questions to ask yourself

If you’re not quite sure when you would like to retire, here are five questions that can help you get a sense of your best move.

When am I eligible for Medicare coverage? Medicare eligibility begins at age 65. If you’re considering retirement before that, make sure you have another dependable source of health insurance.

What do I enjoy most in life?Let’s say you love to travel or treat the grandchildren to special activities. Those things cost money, so you must ensure your post-retirement income is adequate.

Do I have a plan for life after retirement? If your job is what you love and you don’t have a clear idea of what you would do as a retiree, it’s a good sign that you can wait.

Would a trial retirement work for me? If you’re still unsure of when (or if) you want to retire, find out if your employer will allow you to transition to a part-time schedule or go on sabbatical to try it out.

Do I simply want to leave my current job? If so, you may want to “semi-retire” by leaving your current job and taking on a new one. Depending on your age, the Social Security Administration may hold back a portion of your monthly benefits (although you’ll get them back after reaching FRA), but you’ll still have the chance to try something new.

Some people live for the day they can retire, while others can’t imagine what they would do with themselves. Whichever camp you fall into, it’s essential to have a plan and understand when retirement is a realistic option.

There’s some good news related to the Trump administration’s concerted attack on the Social Security Administration: Thus far, it doesn’t appear to have significantly affected the delivery of benefits. Checks are still going out and payments into beneficiaries’ bank accounts are still arriving on time.

Beyond that, however, the system is going to hell.

While Social Security appears to still be working well — superficially — under the surface the agency is suffering through a period of unprecedented turmoil. That’s the gist of a new report by Kathleen Romig and Devin O’Connor, Social Security experts at the Center on Budget and Policy Priorities.

Serious data security lapses, evidently orchestrated by DOGE officials, currently employed as SSA employees,…risk the security of over 300 million Americans’ Social Security data.

— Social Security whistleblower Chuck Borges

Under the Trump administration, Romig and O’Connor observe, the Social Security Administration’s regional office staff “have been mostly eliminated, robbing front-line staff of key supports.” Headquarters staffing has been cut by nearly half, including technology experts. Field office and call center staff also have been eviscerated.

Few departments within SSA have been spared — not even the office tasked with helping members of Congress assist their constituents with Social Security issues and helping to develop legislation.

Newsletter

Get the latest from Michael Hiltzik

Commentary on economics and more from a Pulitzer Prize winner.

You may occasionally receive promotional content from the Los Angeles Times.

The so-called Office of Legislation and Congressional Affairs was cut to three employees from 50. Constituent caseworkers in congressional offices have been receiving “bounce-back emails and no-replies from legislative liaison offices that were previously responsive to congressional inquiries,” according to a letter sent by 50 Democratic House members to the SSA in July.

Even Republicans, who generally have been willing to go along with the administration’s rampage through agency budgets, raised the alarm about customer service failures at SSA, noting in a legislative markup that “there are significant service delivery challenges at SSA that are impacting critical services that millions of Americans count on. “

The agency’s staffing problems may be simmering under the surface, but it translates into chronically poor customer service. “Inadequate staffing at SSA directly harms the retirees, people with disabilities, and bereaved families the agency is responsible for serving,” Romig and O’Connor report.

“Because there aren’t enough workers in SSA’s local offices, applicants wait over a month on average for an appointment. Because there aren’t enough people answering the agency’s 800 number, most callers wait over two hours on average for an answer, as of early August,” they write. “Because there aren’t enough disability examiners, applicants wait eight months for an initial decision on their eligibility for disability benefits, with an additional seven-month wait for those who appeal.”

Meanwhile, more information has emerged about the incursion of untrained representatives of Elon Musk’s budget-cutting DOGE service into Social Security’s most carefully guarded databases. The outcome has been the exposure of workers’ and beneficiaries’ private personal information to outsiders, all without adequate oversight.

I’ve been following Trump’s campaign against Social Security from the outset. Although Trump has promised repeatedly that “we’re not touching Social Security,” actions speak louder than words, and his unconcern about the program, if not his outright hostility, have been screaming from the rooftops.

Among the weapons Trump could use to undermine the program, as I wrote, was “starving the program of administrative resources — think money and staff.” As it happened, Sure enough, within a month of Trump’s inauguration, the program announced plans to reduce its employee base to 50,000 from 57,000.

Its press release about the reduction referred to the program’s “bloated workforce.” That sounded like a cheap gag, since the truth is that the agency has been hopelessly understaffed for years.

The DOGE team showed its ignorance and incompetence at every turn, issuing inaccurate assertions about fraud at Social Security and then instituting operational changes that had no effect on fraud but inconvenienced thousands of beneficiaries. In March, for example, a DOGE employee went on Fox News with the claim that 40% of phone calls to the agency to change direct deposit information came from fraudsters. As a result, the agency mandated that such changes had to be made in person or online.

The true statistic misinterpreted by DOGE was that 40% of direct deposit fraud is connected with phone calls, not that 40% of all calls to change bank information is fraudulent. After the dime dropped at DOGE, the restriction was rescinded.

Since then, the Trump administration has acted from time to time as if the Social Security Administration is an arm of the White House. In March, it shut down SSA services in Maine because the state’s governor had challenged Trump face-to-face over his policies. (The decision was promptly reversed, but then-Acting Commissioner Leland Dudek admitted that he had taken the step in retaliation for the governor’s conflict with Trump.)

In April, Trump tried to dragoon Social Security into his anti-immigrant campaign by declaring some 6,300 purportedly illegal immigrants to be “dead” in program records, even though they were very much alive. The administration said its goal was to deny the workers benefits, though under the law noncitizens without legal residency in the U.S. can’t collect benefits, even if they’ve made payroll contributions to the program.

The biggest threat to the public’s confidence in Social Security may be the administration’s raid on its secure databases, starting with a rampage by DOGE documented by then-Chief of Staff Tiffany Flick.

More has come out since Flick filed her account in court. Last month, Chuck Borges, formerly the program’s chief data officer, filed a whistleblower affidavit outlining his concerns about “serious data security lapses, evidently orchestrated by DOGE officials, currently employed as SSA employees, that risk the security of over 300 million Americans’ Social Security data.”

DOGE, Borges reported, created “a live copy of the country’s Social Security information” and placed it in a digital platform that could be easily accessed by those without authorization.

At issue is the so-called NUMIDENT database, which includes the “name, … place and date of birth, citizenship, race and ethnicity, parents’ names and social security numbers, phone number, address, and other personal information” of every applicant for a Social Security card.

“Should bad actors gain access to this cloud environment,” Borges asserts, “Americans may be susceptible to widespread identity theft, may lose vital healthcare and food benefits, and the government may be responsible for re-issuing every American a new Social Security Number at great cost.”

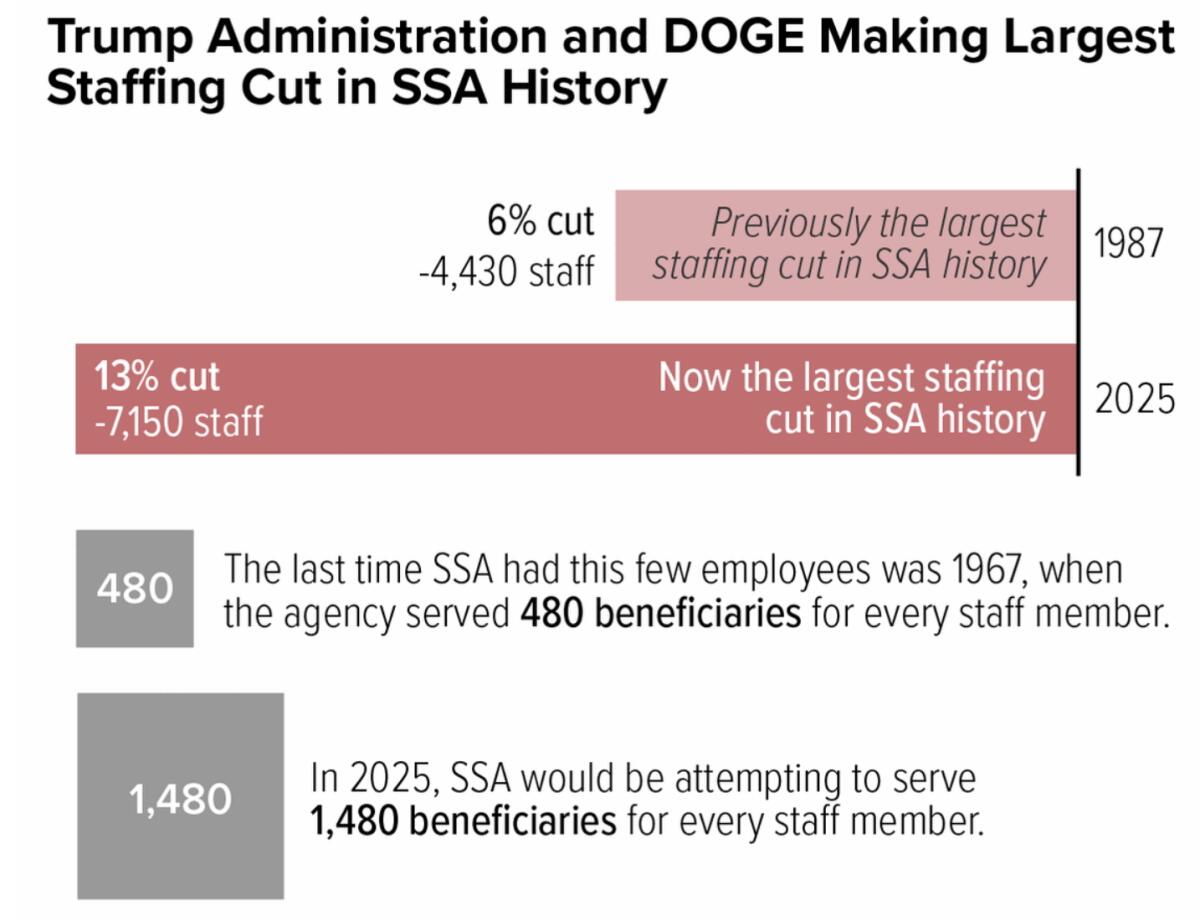

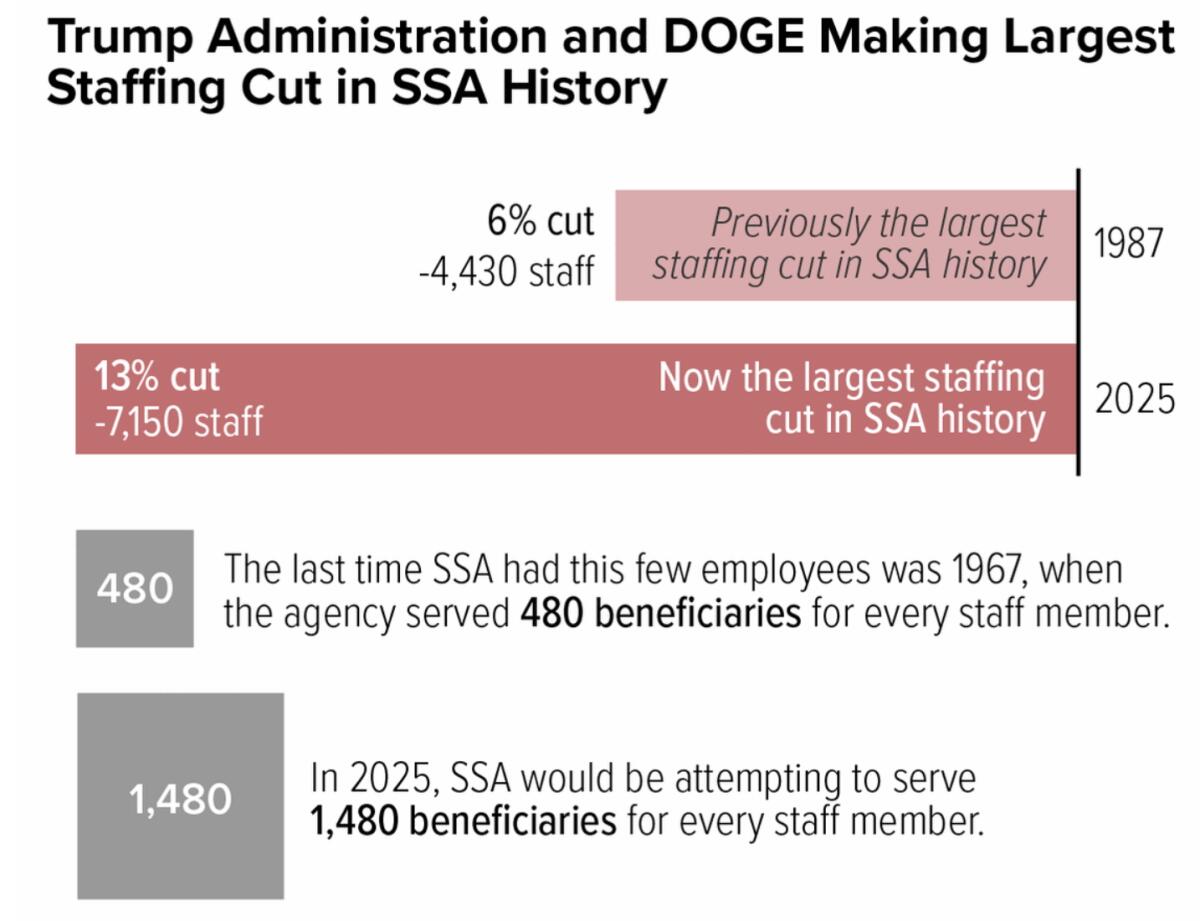

Trump has instituted the largest staffing cut in Social Security history, while the caseload per employee is higher than ever

(Center on Budget and Policy Priorities)

A federal court shut that access and activity down. But in June it was overruled by the Supreme Court, which unaccountably granted DOGE members access to the agency database “in order for those members to do their work.”

SSA didn’t respond to my request for comment on these issues or on increasing concern about the program’s functioning under its recently installed commissioner, Frank Bisignano.

Bisignano has been issuing self-congratulatory press releases boasting about improvements to customer service metrics at the agency — for example, phone answer times cut to an average of six minutes, down from 30 minutes last year. A press release issued in July attributed the improvement to “focused technology enhancements and process engineering.”

In fact, according to Romig and O’Connor, it’s more likely that the improvement happened because the agency reassigned 1,000 staffers from field offices, where they served clients face-to-face, to answering phones. The reassignments, Romig and O’Connor observed, “likely is coming at a steep cost to the rest of the agency’s work.”

At least 2,000 field office employees already had been pushed out by DOGE, so removing an additional 1,000 workers from the field only “deepens problems for people seeking in-person service — which were already considerable.”

Indeed, back in April the agency itself acknowledged that more than three dozen field offices around the country were in dire condition, suffering staff losses of 25% to 33% from DOGE’s “voluntary” resignation program that resulted in the loss of more than 7,000 workers overall, or 13% of the payroll.

Over the last decade or so, Lawmakers on Capitol Hill have been wringing their hands over what they say is Social Security’s impending fiscal crisis, caused by the exhaustion of its trust fund reserve sometime in the next decade. But that’s still the subject of conjecture.

What’s more certain is that the congressional cheeseparing and the DOGE raid that have produced the largest staffing cut in the program’s history — at a time when its caseload is at record size and is destined to grow even further — loom as a greater threat to most workers and beneficiaries.

“To raise customer service to acceptable levels, Congress must not only provide SSA with sufficient funding but also forcefully push back against the Administration’s current mismanagement of its existing resources,” Romig and O’Connor maintain.

They’re right. Isn’t it time for Capitol Hill to take firm, bipartisan action to protect America’s most important government service from its enemies?

We’re about a month away from an official number, but estimates for next year’s COLA are moving higher.

Social Security may be the most valuable retirement asset most Americans have. The pension for retired workers accounted for 20% of families’ total wealth in 2022, according to a study by the Congressional Budget Office. That’s based on a calculation valuing all future payments at present value.

Those future payments get a boost every year, which could make them even more valuable to Americans. The annual cost-of-living adjustment (COLA) helps benefits keep up with inflation. And while we won’t have the official 2026 COLA number until mid-October, it looks like it’ll come in higher than what analysts anticipated at the start of the year.

But a bigger COLA isn’t necessarily reason for Social Security recipients to celebrate. Here’s what retirees need to know.

Image source: Getty Images.

What’s pushing the 2026 COLA higher?

The annual COLA is based on a standard measure of inflation published every month by the Bureau of Labor Statistics called the Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W.

The CPI-W is one of several Consumer Price Index measurements the government publishes. The BLS surveys thousands of businesses and households across the country to collect pricing data on over 200 line items. Those prices are then indexed to a standard price from when the BLS first started collecting data, and weighted according to typical spending patterns of the group the index is supposed to follow. In the case of the CPI-W, the basket of goods represents the spending of working-age adults living in cities.

The Social Security Administration calculates the COLA by taking the average year-over-year increase in the CPI-W during the third quarter, i.e. July, August, and September. The BLS just published August’s CPI numbers on Sept. 11, with the CPI-W climbing 2.8% year over year. That follows a 2.5% increase in July. The final reading to determine the 2026 COLA will come out on Oct. 15.

Based on expectations for that reading, both The Senior Citizen’s League and independent analyst Mary Johnson have published their expectations for next year’s COLA. The former expects it to come in at 2.7% while the latter expects retirees to receive a 2.8% bump. Both estimates are higher than the 2.5% initial estimate The Senior Citizen’s League published before the start of the year.

The reasons for a higher COLA are bad news for 70 million beneficiaries

A bigger-than-expected raise is usually great news for those receiving it, but in the case of Social Security’s 70 million beneficiaries, it signals a challenging economic environment.

The biggest challenge is that the CPI-W doesn’t perfectly match the spending of most seniors. Most people don’t spend their money in retirement the same way they did when they were working age. They probably commute less and spend less on new clothing. They probably have different dining habits. And it’s almost certain that their medical bills have climbed higher as they grow older.

To that end, some of the biggest expenses seniors face are climbing faster than the overall CPI-W numbers. Medical care services were notably 4.2% higher this August than the year before. While gasoline prices were down, utilities were way up. Shelter expenses climbed 3.6%. Despite a 2.7% or 2.8% raise coming in January, most seniors have seen their real cost of living climb much more over the past year.

Rising medical costs are most prominently seen in the Medicare Trustees’ estimate for next year’s Medicare Part B premium. They expect the program will have to charge a standard monthly premium of $206.20 next year, an 11.5% increase from 2025. For those keeping track, that far outpaces the expectations for Social Security’s COLA. Beneficiaries age 65 and older enrolled in Medicare will see that amount come right out of their new monthly payments.

The Senior Citizens League contends this situation isn’t unique to this year’s COLA. It ran a study that estimates the buying power of someone’s benefits who started Social Security in 2010 has decreased 20% through 2024.

The best economic environment for Social Security has historically been slow, steady, and predictable inflation. Under the current administration, which has gone back and forth on trade policies numerous times since the start of the year, prices have become anything but predictable. While many businesses have taken preemptive steps to curb and delay the impact of tariffs, the costs will eventually get passed through to consumers. That could result in even more pain for those on a fixed income next year.

While a 2.7% or 2.8% raise might be bigger than anticipated, many seniors may find that it doesn’t go far enough next year.

Your retirement budget isn’t ready until you’ve accounted for this.

You’re ready for a change of pace — not just leaving the workforce, but moving to another state or country in order to start fresh. While exciting, you’re probably also prepared for some challenges, like learning your way around your new neighborhood and coming up with a new retirement budget.

Though you might not expect it, you could also face Social Security challenges that affect your benefit delivery or how far your checks go. Fortunately, you can minimize the difficulty these issues pose by planning for them well in advance.

Image source: Getty Images.

Moving to another state

Moving to another state won’t change the monthly Social Security check you’re entitled to, whether you’re receiving a retirement or spousal benefit. But it could affect how far your checks go. For example, if you move from a city with a high cost of living to a rural area where living expenses are cheaper, you might find that your checks go further than they would in your current city. On the other hand, if you move to a pricier area, you may have to pay for more of your expenses out of your own pocket.

Moving could also put you at risk of or help you avoid state Social Security benefit taxes. Only nine states still have these, and each has its own rules that determine who owes these taxes. It’s possible to live in a state with a Social Security benefit tax and not pay any state taxes on your checks. But it’s worth reaching out to your new state’s department of taxation or an accountant in that state to learn how it could affect your tax bill.

You could also find yourself owing federal Social Security benefit taxes wherever you go. These depend on your provisional income — your adjusted gross income (AGI), plus any nontaxable interest you have from municipal bonds and half your annual Social Security benefit. If you’re forced to spend more due to a higher cost of living in your new home, this could increase your AGI and your provisional income, potentially forcing you to pay more in federal income taxes.

Moving to another country

If you decide to move to another country, you sidestep the issue of state Social Security benefit taxes. Depending on where you go, you might also be able to secure a lower cost of living to help your benefits go further.

You will still be responsible for paying federal Social Security benefit taxes if your provisional income is high enough. And you could also run into an accessibility issue if you retire in certain countries.

The Social Security Administration can pay you via direct deposit or a prepaid debit card in most parts of the world. However, if you retire in the following countries, you may not be able to receive your benefit payments:

Azerbaijan

Belarus

Kazakhstan

Kyrgyzstan

Tajikistan

Turkmenistan

Uzbekistan

You may be able to petition the Social Security Administration to make an exception for you if you agree to certain restricted payment terms.

This isn’t an option for those who choose to retire in Cuba or North Korea, however. There, you cannot get Social Security benefits at all.

If you retire in a country where the U.S. government won’t send Social Security checks, you may still be able to receive all your back payments if you later move from that country to a place where the Social Security Administration can send benefits again.

It’s best to contact the Social Security Administration directly if you have any questions about how your move could affect your Social Security checks. This way, you’ll be able to get a personalized answer and then you can adjust your budget accordingly.

The United States and China have reached a framework agreement to transfer TikTok’s ownership to US control.

Officials from both countries made the announcement on Monday.

Recommended Stories

list of 4 itemsend of list

The short-form video app was set to be banned in the US by Wednesday if its owner ByteDance did not agree to sell the company to a US-based operation or if the US did not extend a pause of the ban, which the White House has already done three times, most recently in June.

US President Donald Trump applauded the deal, which will be confirmed when he discusses it with his Chinese counterpart President Xi Jinping on Friday.

“A deal was also reached on a “certain” company that young people in our Country very much wanted to save,” Trump wrote on his social media platform Truth Social on Monday.

“The relationship remains a very strong one!!!”

The White House declined to outline the terms of the deal, which was negotiated during trade talks between the two countries in Madrid. The two-day meeting, which wrapped up on Monday, was the latest in a slew of negotiations that began in May.

“We’re not going to talk about the commercial terms of the deal. It’s between two private parties, but the commercial terms have been agreed upon,” US Treasury Secretary Scott Bessent told reporters.

Bessent and US Trade Representative Jamieson Greer, who was also part of the trade delegation in Madrid, said China wanted concessions on trade and technology in exchange for agreeing to divest from the popular social media app.

“Our Chinese counterparts have come with a very aggressive ask,” Bessent said, adding, “We are not willing to sacrifice national security for a social media app.”

“TikTok’s divestment agreement not only keeps the app running in the US, but is also expected to help de-escalate a tense trade standoff and lay groundwork for further trade talks between the US and China,” Maria Pechurina, director of international trade at Peacock Tariff Consulting, told Al Jazeera. “Both US and Chinese delegations explicitly linked the fate of TikTok to progress on tariff reductions and related trade concessions during their conversations in Madrid.”

The deal comes despite the US pushing other nations to impose tariffs on China over purchases of Russian oil, which Bessent said was discussed briefly with the US’s Chinese counterparts.

Experts warn to be wary of the deal being set until Xi and Trump speak on Friday.

“It’s important to note that the Chinese often see the signing of a deal as the beginning, and not the end, of any negotiations. The devil would lie in the details behind the optics. Also expect much haggling on important details that may take years,” Usha Hayley, a professor of international business at Wichita State University who specialises in Chinese industry, told Al Jazeera.

“The deal, when reached, would reflect the convergence of technology, national security, and geopolitics,” said Hayley. “TikTok sits at the centre of US concerns about data access, influence over public discourse, and Beijing’s reach into global tech. Washington is stating that the US views digital platforms as strategic assets, not private businesses.”

TikTok did not respond to Al Jazeera’s request for comment.

The looming ban

Trump proposed banning TikTok during his first term as US president, signing two executive orders in August 2020 that were aimed at restricting the app.

In April 2024, under then-President Joe Biden, the White House signed a law formally banning TikTok unless it sold its US operations. The ban was supposed to take effect on January 19, the last day of the Biden administration. Biden said he would not enforce the ban and said that he would leave that decision to the next administration.

Two days before the January deadline, on January 17, the Supreme Court stepped in to weigh in on TikTok’s challenge to the law and upheld the law. The app went dark briefly before the ban was paused during the early days of Trump’s subsequent presidency.

The pause was initially for 90 days and was later extended multiple times throughout the year.

The cultural importance to Trump

TikTok’s cultural relevance has grown significantly in recent years, serving both as a tool for organising and activism, and as a platform to reach the public, particularly young voters. In April 2024, the pro-Trump videos on TikTok were nearly double those supporting Biden, who was then the Democratic nominee, the New York Times reported, citing TikTok’s internal data.

Trump’s broader use of newer media was widely cited as a factor in his 2024 election victory. His campaign regularly engaged with right-leaning podcasts and influencers — such as Joe Rogan and Theo Von — to reach conservative audiences. It also targeted disillusioned men, who were drawn to influencers promoting traditional notions of masculinity, often conflated with conservative viewpoints.

A Pew Research Center study from November found that news influencers — defined as those who discuss “current events and civic issues” and have at least 100,000 followers across any social media platform – are more likely to lean conservative. A separate report from Pew in February found that news influencers posted more content supporting Trump than former Vice President Kamala Harris, Trump’s 2024 election opponent: 28 percent for Trump versus 24 percent for Harris.

TikTok’s role in spreading far-right narratives is not limited to US politics. The platform has reportedly influenced German state elections, contributing to the rise of far-right leaders, and has similarly affected far-right candidates in Poland, Sweden, and France.

Understanding just where your retirement plans stand has never been easier.

Not to brag, but I’ve always suspected that my love of financial planning may be unrivaled. While my husband believes it’s a sickness, I’ve always enjoyed putting together a household budget (even when the money was not flowing). And, as I recently confessed to a friend, I’m really into retirement planning.

That’s probably why mySocialSecurity has become one of my most visited sites. It didn’t feel like my birthday or anything. Still, I did feel a little jolt of excitement upon learning the Social Security Administration (SSA) just added new features to its mySocialSecurity site.

Decades ago, when I first started planning for a retirement that felt a millennium away, I’d search the house for our latest Social Security statements, grab a notebook, pen, and calculator, and find a comfortable place to calculate. I probably could have learned two foreign languages and how to play the cello in the time I spent grappling with all the “what ifs.”

That was pre-internet, and I didn’t have the information needed to create a long-term retirement plan that approached reality. But then, a bunch of geniuses contributed to the invention of the internet, and by 2012, the SSA had launched mySocialSecurity. While it was helpful back then, it’s become a masterful tool for anyone serious about retirement planning.

Image source: Getty Images.

Latest additions

The mySocialSecurity site has always offered helpful tools, but the SSA is upping its game with these new additions:

Retirement calculator

The retirement calculator lets you compare month-by-month benefit estimates for ages 62 through 70. If you’re thinking about retiring at age 63 years and 6 months, it will take mere seconds for the calculator to indicate your monthly benefit at 63 years and 6 months. The best thing about the retirement calculator is how it takes the fantasy out of retirement planning by helping you decide when you can realistically afford to retire.

Age-based fact sheet

The age-based fact sheet explains the relationship between your birth year and full retirement age. It spells out when you’ll reach full retirement age (FRA), the age at which you’re entitled to 100% of your Social Security benefits. It also shows what happens if you claim benefits at age 62 instead and how much your monthly benefit will be permanently reduced. Finally, the age-based fact sheet allows you to see how much your monthly benefit amount will increase if you delay claiming benefits past your FRA, up to age 70.

Earnings-based fact sheet

This fact sheet addresses how working while receiving Social Security benefits will impact your payments. While there’s no impact if you collect Social Security after FRA, this is where you’d visit to learn how much the SSA will deduct from your benefits if you continue to work before FRA kicks in.

Benefit verification letter

The benefit verification letter spells out which benefits you currently receive. Whether you want it for your records or to provide proof of benefits to a third party, you can access the letter simply by logging into the site.

Form SSA-1099

So you’ll never lose track of how much you’ve received in Social Security benefits, the SSA provides easy access to your SSA-1099, a tax form that reports your annual benefits. This information helps determine if your benefits are taxable and how much to report on your federal tax return.

Check your claim status

Whether you’ve filed for Medicare for the first time or you’re ready to collect Social Security, your claim status provides up-to-date information regarding where your claim stands.

Request a replacement card

If you’ve ever lost your Social Security card, you may have experienced a moment of panic, wondering what to do. I’ve never actually misplaced mine, mostly because I’m afraid my parents will rise from the grave to remind me how important it is to protect it. Mom and Dad might have taken it a little easier on me if they knew how easy the SSA would make it to replace a card.

Planning for retirement

Here’s how mySocialSecurity makes retirement planning less labor-intensive for me. I suspect you’ll find even more interesting ways to use it.

Budget coordination: The personalized retirement benefit estimate clarifies how much I expect to receive at each age. I use that information to coordinate with other savings and investments to develop a retirement plan that will fit our budget.

Earnings history: There’s a feature showing how much income I’ve claimed since my first job. I use it to double-check that SSA got my income right after I file taxes. Given that my Social Security benefits are calculated based on that earnings history, it’s important to know they got it right.

Connect with the SSA: I can use the site to contact the SSA and update my personal information. One day, when I’m collecting Social Security, I’ll be able to use it to view direct deposit information, check out special notices, and ensure the appointed representative payee is who I want it to be (the person who will manage my benefits if I’m incapable of doing so).

I understand that retirement planning may not be everyone’s cup of tea. However, I compare it to taking a moment to stop midway through a cross-country trip, just to see where I am and how much farther I have to go.

Social Security was never intended to cover all of your expenses in retirement. Investing in growth stocks like Nvidia today could help you bridge the gap in your budget down the road.

Many retired Americans rely heavily on Social Security checks for their income, but often, those payments don’t stretch far enough to cover all of their expenses. According to government data, in 2025, the average Social Security benefit is just $1,976 per month.

If that doesn’t sound like much, that’s because it isn’t. A recent study projected that by 2040, 32.6 million U.S. households with retirement-age individuals could have an average cash shortfall of more than $7,000 annually. That gap between retirement income and retirees’ needs is a big reason why many Americans will need to do more to build their own portfolios of investments, rather than trying to rely on Social Security benefits alone.

If you’re on the hunt for stocks that could help you build wealth over the long haul that you can eventually tap in retirement, there are a few compelling reasons to make Nvidia(NVDA 0.43%) one of your picks.

Image source: Getty Images.

Why Nvidia could continue to be a good long-term investment

Nvidia has become a common go-to investment among both tech enthusiasts and average investors over the past few years, as the company is benefiting from a steep increase in spending on artificial intelligence infrastructure. Nvidia’s graphics processing units (GPUs) dominate the artificial intelligence (AI) data center market — it sells an estimated 70% to 95% of all AI chips for infrastructure.

In Q2, the company’s data center revenue jumped 56% year over year to $41 billion, and its non-GAAP earnings per share jumped 54% to $1.05. Eventually, Nvidia’s customers could slow their spending on its hardware — particularly if AI doesn’t deliver the results those companies are hoping for — but that day hasn’t come yet. Nvidia CFO Colette Kress estimates that tech companies will invest up to $4 trillion into AI data centers over the next five years.

And it’s not just AI data centers that could fuel Nvidia’s future growth. The company’s tech is already being used in autonomous vehicles, and advances in the robotics industry could create another expanding new market for it in the coming years. Some estimates forecast that the global autonomous vehicle market will grow to more than $2 trillion over the next five years, and Nvidia CEO Jensen Huang said recently that robotics (including autonomous vehicles) and AI represent a “multitrillion-dollar growth opportunity” for his company.

Though Nvidia stock has already soared by more than 1,100% over the past three years, the combination of its dominance in AI data center processors and its emerging opportunities in robotics and autonomous vehicles suggests it will remain a good long-term investment.

More growth could be ahead for Nvidia, but keep this in mind

While no single stock should make up the majority of your portfolio, investing in Nvidia could give future retirees a way to benefit from the massive transition toward AI systems that’s currently underway. While the chipmaker doesn’t currently pay a meaningful dividend, investors can eventually sell their holdings in retirement to supplement their incomes.

Planning for retirement can be challenging, and as you approach retirement age, it’s generally a good idea to reduce your exposure to stocks and other higher-risk investments. While Nvidia’s share price may continue to climb in the years ahead, it’s important to remember that it’s still a tech company, and tech stocks often go through periods of unusual volatility.

This shouldn’t be too much of a concern if you’ve got a long way to go before retirement, but remember that as you age, you’ll want to shift the balance of the allocations in your well-diversified portfolio toward less risky holdings.

Chris Neiger has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool has a disclosure policy.

As airlines are getting stricter with their baggage restrictions, travellers are coming up with inventive ways to pack more while paying less – but there’s one trick experts are urging people not to risk doing

Experts urge against this viral packing trick (Image: Getty Images/iStockphoto)

There are so many different travel ‘hacks’ circulating on social media – but experts urge travellers not to follow the viral pillowcase luggage trick as it’s not worth the risk.

Many of us are guilty of overpacking when going away, so it’s no wonder we’re always looking at ways to pack more and keep within the allowed size and weight limit for our luggage without paying more.

However the viral pillowcase hack, that sees travellers stuffing an empty pillowcase with extra clothes rather than bags when boarding a plane could come at a risk that experts advise people not to follow.

The packing hack could still land you with a hefty fine (stock photo)(Image: Getty Images/iStockphoto)

As airlines become stricter on their hang luggage rules, Amanda Parker from Netflights has shared her thoughts. She said: “Passengers are cunningly avoiding these strict hand luggage limits and avoiding paying up to £150 in extra fees by taking advantage of an empty pillowcase.

“Travellers are using a standard pillowcase, removing the pillow inside, and instead using it as a secret storage compartment for extra clothes. Travellers rely on airlines not counting a pillow as an additional item when boarding, so by stuffing a standard pillowcase with soft clothing items like T-shirts and jumpers, they’re essentially creating a travel ‘pillow’ that they hope to sneak through.”

However the expert said “airlines are cracking down on sneaky flight hacks” and said you might want to think twice about testing this hack on your next flight.

“An overly stuffed pillowcase bursting with clothes can raise suspicion, and if you’re already boarding the plane with maximum baggage, then your pillow can be flagged as extra.” Amanda said what works for one airline may not for another as different airlines cabin baggage rules vary.

She added: “By risking the pillowcase hack, you could risk holding up the boarding process or being denied boarding entirely if you can’t pay the fee. Some low-cost airlines state that any item used to carry belongings, even if disguised, must be treated as luggage,” and advised before jetting off to always check the baggage allowance rules with the correct bags.

The expert said airlines issue fines for overweight baggage due to the fact that the heavier a plane is, the more fuel it burns. “So every kilogram of baggage increases the plane’s weight, which directly impacts fuel consumption.

“Since fuel is one of the biggest costs for airlines, they want to limit unnecessary weight, and charging for excess baggage is one way to do it.”

Help us improve our content by completing the survey below. We’d love to hear from you!

Jessie Wallace has returned to social media with a series of NTA snapsCredit: instagram

6

She posted pics of her in high spirits after being caught in tears at the partyCredit: instagram

6

Jessie fled in floods of tears at the celeb-packed bashCredit: The Sun

Before she was left in tears, she was seen dancing with her co-stars and being labelled as the “life and soul of the party”.

Now, Jessie has taken to Instagram to share a collection of snaps from the evening and has made no reference to the reasoning behind her tearful exit.

The Kat Slater star, 53, shared images from both before, after and during the NTA ceremony in which she could be seen beaming from ear-to-ear.

Keeping coy about her tearful antics, Jessie captioned the snaps: “What a great night! Thank you to everyone who voted for@bbceastendersand my pal Steve and the gorgeous@jacjossayou are AMAZING!

Read More on Jessie Wallace

“Love all me EE faaaaaaamily.”

Jessie cuddled up to many of her co-stars in the pics including Michelle Ryan and Jacqueline Jossa.

She even included a shot from the after-party in which she could be seen with Love Island host Maya Jama.

Jessie’s night turned eventful unexpectedly when she was seen running through the after-party in tears.

Jessie, 53, had been seen in high spirits during Wednesday night’s ceremony at London’s O2 Arena.

She was later spotted at the official after-party with her colleagues, including Scott and former co-star Charles Venn.

EastEnders star suddenly bursts into tears at NTAs after-party leaving onlookers baffled

An onlooker said: “Jessie was the life and the soul of the party and was on a high after they’d picked up their big award.

“She was seen chatting with Charles and a few other people and was having a real laugh.

“But then suddenly out of nowhere she just burst into tears in front of everyone.

“Scott was like a superhero and just scooped her out and took her out of the party.

“No one could work out why Jessie was in tears. People just looked a bit baffled.”

6

Jessie hasn’t spoken about her tearful displayCredit: instagram

6

Scott Maslen escorted her outCredit: The Sun

6

Jessie had a fun-filled night at the NTAsCredit: Alamy

Maxing out your Social Security benefits in 2026 would require doing two big things.

In 2025, the maximum monthly Social Security benefit is $5,108 per month. It’s not 100% clear exactly how large the maximum monthly benefit will be in 2026, but based on current estimates of benefit increases, it could be somewhere around $5,245.97.

That’s a huge benefit amount to collect each month. So, how can you earn the maximum benefit in 2026? Here’s what you would need to do.

Image source: Getty Images.

A big income is needed to max out your 2026 benefit

If you want to work toward earning the maximum Social Security benefit in 2026, the first thing that you need to do is to earn a pretty large salary.

Social Security benefits are based on average wages in the 35 years you earn the most. There is a cap on the amount of wages that count in this benefits formula, though. Specifically, income up to the “wage base limit” is subject to Social Security tax and is counted in the benefits formula, and income above that threshold is not.

If you want the maximum benefit, you need a 35-year career history of earning an income equal to or above the wage base limit. In 2025, that limit was $176,100. It’s likely to increase to $183,600 in 2026 as the amount goes up most years due to the effects of inflation.

You’ll need to make sure your salary is equal to or above these numbers to be on track to get the maximum benefit.

You’ll need to put off your Social Security claim

There’s also another thing you’ll have to do if you want the maximum possible Social Security benefit to supplement the savings in your retirement plans. Specifically, you are going to need to make plans to wait until you are 70 to claim your Social Security benefits.

Waiting until 70 means waiting until after your full retirement age, and means waiting a full eight years to claim benefits after first becoming eligible for them at 62. You have to wait this long because earning the wage base limit or higher for 35 years only puts you on track for the highest possible standard Social Security benefit.

You’ll have to raise that standard benefit as much as possible by maxing out your delayed retirement credits if you want the overall maximum benefit. These delayed retirement credits increase your standard Social Security checks until age 70, when you can’t earn any more credits.

If you follow these two steps, then you will be on track for the maximum monthly Social Security benefit in 2026. You’ll have a good amount of extra money coming from Social Security to add to the distributions from your 401(k) and build the secure retirement you deserve.

Unfortunately, many people don’t do either of these things, much less both of them. Earning the maximum benefit is really hard, as you have to be among the country’s top earners for a long time and not need your retirement benefits until pretty late in life.

If you can’t do this, you’ll need to be realistic about what Social Security benefits you’ll get when you do your retirement planning. The reality is that Social Security replaces only around 40% of pre-retirement income, and the rest needs to come from accounts like your 401(k) and IRA. So, while you can work toward maxing out your benefit, also be sure you are saving plenty of money in case you fall short.

Cabinet spokesman and Minister of Communication and Information Technology Prithvi Subba Gurung said early on Tuesday that the government had rolled back the social media ban imposed last week.

Recommended Stories

list of 4 itemsend of list

“We have withdrawn the shutdown of the social media. They are working now,” Gurung told the Reuters news agency.

At least 19 people were killed and more than 100 were injured in clashes with Nepalese security forces after thousands of young people took to the streets on Monday to protest against corruption and the government’s ban on social media platforms.

The government had blocked 26 social media sites, including WhatsApp, Facebook, Instagram, LinkedIn and YouTube.

This is a breaking news story. More to follow soon.

At least 13 people have been killed and dozens are injured in Nepal after demonstrations against a government social media ban led to clashes between protesters and security forces.

Thousands heeded a call by demonstrators describing themselves as Generation Z to gather near the parliament building in Kathmandu over the decision to ban platforms including Facebook, X and YouTube.

Nepal’s Minister for Communication Prithvi Subba told the BBC police had had to use force – which included water cannons, batons and firing rubber bullets.

The government has said social media platforms need to be regulated to tackle fake news, hate speech and online fraud.

But popular platforms such as Instagram have millions of users in Nepal, who rely on them for entertainment, news and business.

Demonstrators carried placards with slogans including “enough is enough” and “end to corruption”.

Some said they were protesting against what they called the authoritarian attitude of the government.

As the rally moved into a restricted area close to parliament, some protesters climbed over the wall.

“Tear gas and water cannons were used after the protesters breached into the restricted area,” police spokesman Shekhar Khanal told the AFP news agency.

A Kathmandu district office spokesperson said a curfew was imposed around areas including the parliament building after protesters attempted to enter.

Last week authorities ordered the blocking of 26 social media platforms for not complying with a deadline to register with Nepal’s ministry of communication and information technology.

Since Friday, users have experienced difficulty in accessing the platforms, though some are using VPNs to get around the ban. So far, two platforms have been reactivated after registering with the ministry following the ban.

Nepal’s government has argued it is not banning social media but trying to bring them in line with Nepali law.

Before you take benefits early, understand all the drawbacks.

There’s a reason 62 tends to be a common age to sign up for Social Security — it’s the earliest age you’re allowed to take benefits. If you’re thinking of filing for Social Security at 62, it’s important to understand exactly what that means for you and your family financially. Here are three key pieces of information to keep in mind.

1. You’ll reduce your monthly benefits for life

You’re entitled to your complete Social Security benefit without a reduction at full retirement age, which is 67 for anyone born in 1960 or later. You can start getting those benefits at 62, but the Social Security Administration will reduce them if you sign up before full retirement age.

Image source: Getty Images.

One thing you must know is that any reduction in Social Security you face by claiming early is a permanent one. And if you sign up at 62 with a full retirement age of 67, you’re looking at slashing your monthly benefits by 30% for life. If you don’t have a lot of retirement savings, that’s a hit you may not be able to afford easily.

2. You’ll leave your spouse with a smaller survivor benefit

If you’re married, the financial decisions you make regarding your retirement can significantly impact your spouse. And that extends to Social Security.

If you’re the higher earner in your household, your spouse might depend heavily on Social Security survivor benefits if they end up outliving you. But if you claim benefits at 62 and reduce them substantially in the process, it could mean leaving your spouse with that much less money once you’re no longer around. That could cause them a world of stress and make it difficult for them to keep up with their expenses.

3. You’ll be subject to an earnings test if you’re still working

You don’t have to stop working to claim Social Security. And once you reach full retirement age, you can earn any amount of money from a job without it negatively impacting your Social Security benefits if you’re collecting them.

But if you claim Social Security before full retirement age, you’ll be subject to an earnings test if you’re still working. And exceeding its limit could result in withheld benefits.

In 2025, you can earn up to $23,400 without risking the withholding of your Social Security benefits. Beyond that point, you’ll have $1 in Social Security withheld per $2 of earnings.

Now you should know that if you have benefits withheld for exceeding the earnings-test limit, they’re not forfeited completely. You should get the money back in the form of larger monthly benefits once full retirement age arrives.

However, it may not make sense to reduce your benefits by claiming them at 62 only to then have most of that income source withheld due to earning too much. Run the numbers to see how much Social Security, if any, you’re likely to lose temporarily.

Though it’s easy to see why 62 is such an appealing age to file for Social Security, it may not be the optimal age for you. Or maybe it is. The key, either way, is to understand the ramifications of taking benefits that early and to make sure you’re prepared to deal with the aftermath.

Evans added: “It appears that my appearance on game day seems to be offending some people… and to that I’m so not sorry.

“Myself, my team and all the incredible female athletes from around the world are currently in the middle of the biggest Women’s Rugby World Cup, celebrating the best of the best and being supported by thousands of people, including young boys and girls that are finally seeing what is possible in this incredible game.

“Yes, Wales unfortunately haven’t been at our best but I’m not here to make excuses for that.

“What I will say – the bows in my hair, the tape around my arm, the eyelashes and full face of make-up I choose to wear, has no bearing on my ability, my passion or fight for this game.

“This game allows space and room for every boy and girl, whatever their haircut, body shape or look they wish to wear on and off the field. ‘It’s not a rugby look’ – a rugby player is no longer defined by your gender or what you look like. ‘It’s childish’ – but to all those young girls it’s understanding you don’t have to compromise who you are to fit into a stereotype.

“In an old-school, man’s game, I’m bringing a bit of Barbie to the party.

“To all those that aren’t a fan, that is OK. To all the support and love – thank you. Don’t worry, I won’t be changing.”

Wales conclude their World Cup campaign on Saturday in their final group game against Fiji.

Even those far from retirement should know about this.

One critical thing every retiree (if not every American) needs to know about Social Security in 2025 is that the program is in trouble.

Some scary headlines may have you believing it’s going to run out of money completely and will soon be unable to pay retirees anything, but that’s not the case. As long as workers keep paying into the system, there will be funds to pay retirees. But not enough funds, unless some changes are made.

Image source: Getty Images.

The problem is that with people living longer and often retiring earlier, Social Security is no longer running a surplus. The ratio of workers to Social Security beneficiaries has shrunk over time, from 8.6 in 1955 to 3.3 in 1985 to 2.7 in 2023 — and it’s projected to fall to 2.3 by 2036.

Fortunately, there are multiple ways to fix Social Security’s shortfall. For starters, the tax on our earnings for Social Security could be increased. Even a fraction of a percentage more would deliver a big infusion to Social Security’s coffers. Another fix is to raise — or eliminate — the cap on earnings that are taxed for Social Security. The cap is currently $176,100.

The bottom line is that as we plan for our retirements, we shouldn’t count on receiving the full benefits to which we’re entitled, though we can certainly hope for that. It can’t hurt to let your elected officials know that you’d like Social Security strengthened, too. And in the meantime, save and invest effectively for retirement, perhaps aiming to set up multiple income streams.