YouTube users reported problems streaming content and accessing the app for about 60 minutes before the company resolved the issue.

Published On 16 Oct 202516 Oct 2025

Share

YouTube says it has resolved problems with its website and app after hundreds of thousands of users worldwide self-reported issues with its streaming services.

“This issue has been fixed – you should now be able to play videos on YouTube, YouTube Music, and YouTube TV!” YouTube wrote on X on Thursday morning in Asia.

Recommended Stories

list of 4 itemsend of list

YouTube did not disclose why users reported problems streaming videos for about 60 minutes on Thursday morning, or the global extent of the problem.

Disruptions began just before 7am in East Asia (23:00 GMT, Wednesday) for YouTube, YouTube Music and YouTube TV, according to Downdetector, a website that aggregates website disruptions in real time.

Users from Asia to Europe and North America soon reported problems streaming, accessing the website, and using the apps of YouTube and its affiliates, though error reports were most heavily concentrated in the US, according to Downdetector’s user-generated error map.

Major disruptions were also reported in Japan, Brazil and the United Kingdom, although the extent of the problem is unknown because Downdetector data is based on user-submitted reports and social media.

The number of error reports peaked at 393,038 reports in the US at 7:57am (23:57 GMT) before falling off sharply, according to Downdetector data.

Downdetector reported a smaller number of disruptions for YouTube Music and YouTube TV, which both peaked at fewer than 5,000 error reports in the US over the same period of time.

Between the 10th and 15th of every month, the U.S. Bureau of Labor Statistics (BLS) releases the previous month’s inflation data. This information is used by the Social Security Administration (SSA) to calculate the annual cost-of-living adjustment (COLA).

The BLS was slated to release the September inflation report — the final piece of data needed to unveil the 2026 COLA — at 08:30 a.m. ET on Oct. 15. But due to the federal government shutdown, the most-anticipated announcement of the year has been pushed back.

Social Security’s 2026 COLA reveal will occur on Oct. 24

In its simplest form, Social Security’s COLA is the near-annual “raise” passed along to beneficiaries to offset the impact of inflation (rising prices). If benefits weren’t adjusted for the effects of inflation, Social Security recipients would see their income lose buying power most years.

For the last half-century, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) has served as Social Security’s inflation measuring stick. With more than 200 different spending categories, each with its own unique percentage weightings, the CPI-W can be reported as a single figure by the BLS each month.

The quirk with Social Security’s COLA calculation is that only the months of July, August, and September (the third quarter) matter. The other nine months of the year can be helpful in spotting trends, but they aren’t used in the COLA calculation.

With CPI-W readings from July and August already known, the only puzzle piece missing is September. Unfortunately, most economic data reports from federal agencies are delayed indefinitely during government shutdowns.

However, some BLS staffers are going back to work and will be releasing the September inflation report on Friday, Oct. 24, at 08:30 a.m. ET, according to information provided to CNBC. The SSA will announce the 2026 COLA on Oct. 24, as well.

Based on estimates from nonpartisan senior advocacy group The Senior Citizens League and independent Social Security and Medicare policy analyst Mary Johnson, next year’s COLA is forecast to come in at 2.7% or 2.8%, respectively. This would work out to an extra $54 to $56 per month for the typical retired-worker beneficiary, and $43 to $44 extra each month for the average worker with disabilities and survivor beneficiary.

While little is set in stone — other than the expectation of the BLS reporting the last piece of data needed to calculate the 2026 COLA on Oct. 24 — retirees are very likely getting the short end of the stick with next year’s raise. COLAs have consistently come up short for retirees, and a projected 11.5% increase in the 2026 Medicare Part B premium isn’t going to help.

Image source: Getty Images.

No speculating here! This is the one guaranteed Social Security change for 2026

Though the government shutdown has delayed the release of key pieces of information, such as next year’s COLA, the maximum taxable earnings cap, the maximum monthly payout at full retirement age, and the withholding thresholds tied to the retirement earnings test, there is one Social Security change that’s guaranteed to take place in 2026. However, you’ll have to go to the state level to see it.

Firstly, yes, Social Security benefits may be taxable at the federal and state levels.

Individuals whose provisional income — adjusted gross income (AGI) + tax-free interest + one-half benefits — tops $25,000, or $32,000 for couples filing jointly, can have some of their Social Security income exposed to federal taxation.

When the calendar flips to Jan. 1, 2026, West Virginia will officially become one of 42 states that don’t tax Social Security income.

In the 2022 tax year, West Virginia made Social Security income exempt from state-level taxation for individuals and jointly filing couples with respective AGIs of $50,000 or less and $100,000 or less.

In March 2024, West Virginia’s legislature passed, and its governor signed, a new law that phases out the taxation of Social Security benefits over a three-year period for those folks who didn’t qualify for this previous AGI adjustment.

Beginning in the 2024 tax year, West Virginians who received Social Security benefits and generated more than $50,000 in AGI (or $100,000 in AGI, if filing jointly) saw 35% of their Social Security benefits exempted from state-level taxation. In 2025, this exemption increased to 65% of Social Security income. In 2026, 100% of Social Security income will be exempted at the state level.

West Virginia will join Kansas, Missouri, Nebraska, and North Dakota as states that have shelved the taxation of Social Security benefits since this decade began.

While this has been anything but a normal COLA announcement month for Social Security, the one thing we do know is that Social Security recipients in West Virginia will be all smiles when the new year arrives.

Those annual raises have a major flaw that cannot be overlooked.

There’s one piece of news seniors on Social Security have been itching to get for months now — news of an official cost-of-living adjustment, or COLA, for 2026.

At this point, it’s pretty clear that 2026 is not going to be one of those 0% COLA years. Though there have been 0% COLAs in the past, inflation has risen enough to date that experts can say with confidence that Social Security benefits will, indeed, be going up in the new year. The question is by how much.

Image source: Getty Images.

Current estimates seem to be floating in the 2.7% to 2.8% range. But we won’t know what next year’s COLA is for sure until the Social Security Administration makes its big announcement.

That said, Social Security’s upcoming COLA is probably going to be bad news no matter what it actually amounts to. It’s important to understand why — and take steps to work around that.

Why Social Security’s upcoming COLA probably won’t cut it

There’s a reason not to get too excited about Social Security’s 2026 COLA. That reason boils down to the fact that Social Security COLAs have been failing seniors for decades.

In fact, the Senior Citizens League, an advocacy group, says that seniors on Social Security lost 20% of their buying power between 2010 and 2024 due to insufficient COLAs. So chances are, next year’s COLA won’t keep up with inflation, either.

The problem stems from how Social Security COLAs are calculated. They’re based on annual third-quarter changes to the Consumer Price Index for Urban Wage Earners and Clerical Workers.

Now, let’s look at that index’s name carefully. Notice the terms “urban,” “wage earners,” and “clerical workers.” Do those describe the typical Social Security recipient?

It’s true that plenty of retirees reside in cities. But that’s certainly not a given. In fact, many retirees are able to move outside of cities to lower their costs once they no longer have to worry about proximity to a job.

Many Social Security recipients, by nature, are also not workers. They’re retired. So it’s pretty silly to base Social Security COLAs on an index that measures the costs a different subset of people face.

Advocates have been pushing to base Social Security COLAs on the Consumer Price Index for the Elderly, or CPI-E. But lawmakers haven’t exactly been jumping to make that change, so it’s not one to expect anytime soon.

Prepare to be disappointed now

No matter what raise Social Security recipients end up eligible for in 2026, chances are, it won’t cut it. Plus, if you’re on Medicare as well, any increase in the cost of Part B will eat away at your COLA.

If you want to improve your financial picture for 2026, you can’t sit back and wait for your COLA to take effect for that to happen. Instead, you should take matters into your own hands.

Here are some specific steps to take:

Do a thorough review of your retirement budget

Identify a few expenses you can reduce or even eliminate

Explore options for going back to work, whether as an hourly employee or a gig worker

See if it’s possible to downsize your home or rent out a room for income

Explore moving in with a family member if money is very tight

Review your Medicare plan choices carefully during open enrollment to lower your healthcare costs

There may be other steps you can take to improve your finances, too, and it’s worth exploring them. What you don’t want to do is assume that your Social Security COLA will be the solution to your financial problems.

Even if Social Security’s 2026 COLA is more generous than expected, chances are good that it won’t do the job of keeping up with inflation that it’s supposed to. The sooner you’re able to accept that, the sooner you can start making positive changes that have a real effect.

The State Department says the US has ‘no obligation to host foreigners who wish death on Americans’ after revoking visas over critical social media posts.

The US Department of State says it has revoked the visas of six foreigners over remarks they made on social media about Charlie Kirk, the conservative political activist who was shot dead at a rally in September.

“The United States has no obligation to host foreigners who wish death on Americans. The State Department continues to identify visa holders who celebrated the heinous assassination of Charlie Kirk,” the department said in a post on X on Tuesday evening in the US.

Recommended Stories

list of 4 itemsend of list

The post was followed by a list of screenshots and critical remarks from six social media accounts, which the State Department said belonged to individuals from South Africa, Mexico, Brazil, Paraguay and Mexico.

“An Argentine national said that Kirk ‘devoted his entire life spreading racist, xenophobic, misogynistic rhetoric’ and deserves to burn in hell. Visa revoked,” the State Department tweeted along with a screenshot that had the username blacked out.

The screenshot post said Kirk was now somewhere “hot” – an allusion to religious descriptions of hell.

The United States has no obligation to host foreigners who wish death on Americans.

The State Department continues to identify visa holders who celebrated the heinous assassination of Charlie Kirk. Here are just a few examples of aliens who are no longer welcome in the U.S.:

The news from the State Department came as Kirk was posthumously awarded the Presidential Medal of Freedom on Tuesday by President Donald Trump.

Kirk, who was 31 at the time of his death, was a cofounder of the conservative Turning Point student organisation. He was credited with driving young voters to vote for Trump during last year’s US presidential election.

His death led to a wave of social media commentary on the US left and right about his politics, as Trump elevated him to the status of a “martyr for truth” during a memorial service.

More than 145 people were fired, suspended, or resigned over social media posts or comments about Kirk, according to a New York Times investigation.

US Secretary of State Marco Rubio previously said the Trump administration could revoke the visas of foreign nationals over comments on Kirk, while Deputy Secretary of State Christopher Landau urged internet users to report social media comments of people applying for US visas.

“I have been disgusted to see some on social media praising, rationalising, or making light of the event, and have directed our consular officials to undertake appropriate action,” Landau tweeted in September. “Please feel free to bring such comments by foreigners to my attention so that the [State Department] can protect the American people.”

In light of yesterday’s horrific assassination of a leading political figure, I want to underscore that foreigners who glorify violence and hatred are not welcome visitors to our country. I have been disgusted to see some on social media praising, rationalizing, or making light…

While the State Department has required visa applicants to share their social media handles on their applications since 2019, in June, it added the provision that student applicants must make all their social media accounts public for government vetting.

The move follows a crackdown on international students who supported pro-Palestine protests on university and college campuses across the US under the Trump administration.

In August, a State Department official told Fox News it had revoked more than 6,000 student visas this year.

About two-thirds of visas were revoked because students reportedly broke US law, the Fox News report said, while “200 to 300” were cancelled because they supported “terrorism” or engaged in “behaviour such as raising funds for the militant group Hamas”.

The government shutdown has complicated things, but the COLA is still coming soon.

Every October, the Social Security Administration (SSA) announces the cost-of-living adjustment (COLA) for the upcoming year.

Up until recently, that announcement was supposed to be around Oct. 15 — right after the Bureau of Labor Statistics (BLS) releases September’s inflation report. But with the federal government closed until further notice, it seemed as if that report wouldn’t be released anytime soon.

New information from the BLS, however, suggests we could be getting the COLA announcement sooner than expected. Here’s when it might be coming, what it might be, and how that might affect your retirement.

Image source: The Motley Fool.

When will the new COLA be released?

The SSA calculates the COLA by averaging Consumer Price Index data from July, August, and September. That average is compared to the figure from the same period the year prior, and if it’s higher, the percentage difference will be next year’s COLA.

Before the government shut down, the BLS was expected to release September’s Consumer Price Index data on Oct. 15. But with that office almost entirely furloughed, it was unlikely the report would be published before the government reopened.

However, on Oct. 10, the BLS published an update noting that September’s inflation report would be released on Oct. 24. Generally, the SSA announces the new COLA almost immediately after the BLS inflation report is published.

What might next year’s adjustment be?

We won’t know the official 2026 COLA until the SSA makes the announcement later this month, but nonpartisan advocacy group The Senior Citizens League has estimated that it will land at 2.7%.

That figure is based on already available inflation data, as well as the projected data from September. If September’s numbers are significantly different from the estimates, the COLA may be higher or lower than predicted.

The average retired worker collects just over $2,000 per month in benefits, according to August 2025 data from the SSA. A 2.7% COLA, then, would amount to a raise of around $56 per month.

While any boost in benefits is helpful to a degree, for many retirees, next year’s COLA may be underwhelming. Inflation has stayed stubbornly high throughout the year, and tariffs have also taken a bite out of many retirees’ budgets.

Medicare Part B premiums are also expected to increase from $185 per month this year to a projected $206.50 per month in 2026, according to this year’s Medicare Trustees Report. Because Medicare premiums are typically deducted from Social Security checks, that $21.50 monthly increase will eat up a significant chunk of the COLA raise for the average retiree.

What does this mean for retirees?

It doesn’t hurt to keep an eye out for the COLA announcement to help budget for 2026, but for the most part, retirees may want to avoid relying too heavily on this adjustment to make ends meet.

Again, any extra cash can help pay the bills, especially with many older adults stretched thin financially right now. But with Social Security not going as far as it used to, it may be wise to start finding ways to reduce your dependence on your benefits.

According to a report from The Senior Citizens League, Social Security benefits lost around 20% of their buying power between 2010 and 2024. If you can swing it, finding a source of passive income or going back to work temporarily could have a bigger impact on your budget than any COLA.

This won’t be possible for everyone, but if you can beef up your savings even slightly, you won’t need to worry quite as much about future COLAs falling short. No matter where the 2026 adjustment lands, it’s wise to keep realistic expectations about how far that money will go.

In just a few days, the Social Security Administration (SSA) will be making a huge announcement about changes to the program in 2026. A new earnings-test limit will be shared, as well as the maximum monthly benefit.

Perhaps the most anticipated update the SSA will share, however, is an official cost-of-living adjustment, or COLA, for 2026.

Image source: Getty Images.

Each year, Social Security benefits are eligible for a raise, based on inflation. Without COLAs, beneficiaries would be pretty much guaranteed to lose buying power over time.

Initial projections are calling for a 2.7% COLA for 2026, but that number doesn’t take inflation data from September into account. If inflation rose substantially last month, seniors could be looking at an even larger boost to their Social Security checks in 2026.

While a 2.7% or higher COLA might seem like something to celebrate, you may want to temper your excitement if you count on Social Security for income. That’s because that COLA may not be yours to keep in full.

Will a Medicare increase eat into your COLA?

Seniors who are enrolled in Medicare and Social Security at the same time pay their premiums for Part B, which covers outpatient care, directly out of their monthly benefits. This means that if the cost of Medicare increases in 2026, it will eat into whatever COLA retirees receive.

In 2025, the standard monthly Part B premium rose from $174.70 to $185. But based on projections from the Medicare Trustees released earlier this year, the standard Part B premium for 2026 could be a whopping $206.50 — an increase of $21.50. It also could cause many seniors to lose out on a good chunk of their Social Security raises.

As of August, the average monthly Social Security benefit for retired workers was about $2,008. A 2.7% COLA would result in a boost of about $54 per month. However, if Medicare Part B goes up by $21.50 per month, the typical Social Security benefit might only rise by around $32.50, in practice.

It’s best to have income outside of Social Security

Until the SSA makes an official COLA announcement on Oct. 15, we won’t know for sure what next year’s COLA will amount to. However, even if it’s fairly generous, a large uptick in Part B costs could wipe out much of it.

That’s why it’s important not to be too reliant on Social Security COLAs to keep up with inflation. A better bet? Save well for retirement, and set yourself up with a portfolio of assets that continues to generate income for you.

Those assets could include a mix of stocks and bonds. The stocks should ideally provide growth and income in the form of dividend payments. The bond portion, meanwhile, may be more stable, providing you with steady income you can use to supplement your monthly Social Security checks.

There are other options for generating retirement income, too, like working part-time. And that part-time work doesn’t have to come in the form of a boring job with a strict, preset schedule.

Thanks to the gig economy, you can explore different options for earning some money. You may find that, on top of the extra income being helpful, it’s nice to have a reason to get out of the house on a regular basis and socialize with other people.

No matter what strategy you choose, the key is to have some income outside of Social Security — because while the program’s COLAs do help seniors keep up with inflation to some degree, they also have their fair share of shortcomings.

A Social Security dollar simply isn’t what it used to be.

For most retirees, Social Security is more than just a monthly deposit into their bank accounts. It represents a financial lifeline that helps them make ends meet.

In 2023, Social Security lifted more than 22 million people out of poverty, according to an analysis from the Center on Budget and Policy Priorities (CBPP), and 16.3 million of these recipients were aged 65 and over. If Social Security didn’t exist, the CBPP estimates the poverty rate for adults aged 65 and up would jump nearly fourfold, from 10.1% (with existing payouts) to 37.3%.

Meanwhile, 24 years of annual surveys from Gallup show that 80% to 90% of aged beneficiaries lean on their payouts in some capacity to cover their expenses.

For retirees, few announcements have more bearing than the annual cost-of-living adjustment (COLA) reveal in October. Though Social Security payouts are on track to do something that hasn’t been witnessed in almost 30 years, next year’s “raise” appears set to give retirees the short end of the stick, yet again!

Image source: Getty Images.

What is Social Security’s COLA and why might the 2026 reveal be delayed?

The fabled “COLA” you’ve probably been hearing and reading about over the last couple of weeks is the tool the Social Security Administration (SSA) has on its proverbial toolbelt to keep benefits aligned with inflation.

Hypothetically, if a large basket of goods and services that retirees regularly purchase increases in cost by 2% from one year to the next, Social Security benefits would also need to climb by 2%. Otherwise, these folks would see their buying power decline. Social Security’s COLA attempts to mirror the inflationary pressures that program recipients are facing so they don’t lose purchasing power.

This near-annual raise is based on changes to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which has measured price changes for Social Security since 1975. It has more than 200 individually weighted categories, which allows the CPI-W to be chiseled down to a single figure at the end of each month. These readings can be compared to the prior-year period to determine if prices are collectively rising (inflation) or declining (deflation).

What makes the COLA calculation unique is that only CPI-W readings from July, August, and September (the third quarter) are used to determine the upcoming year’s raise. If the average third-quarter CPI-W reading in the current year is higher than the comparable period last year, prices, as a whole, have risen, and so will Social Security checks in the upcoming year.

The catch with Social Security’s 2026 COLA is that its expected reveal on Oct. 15 may be delayed. The September inflation report is the final puzzle piece needed to calculate the program’s cost-of-living adjustment. However, most economic data releases are delayed during a federal government shutdown, which, in turn, can postpone the Oct. 15 COLA announcement set for 8:30 a.m. ET.

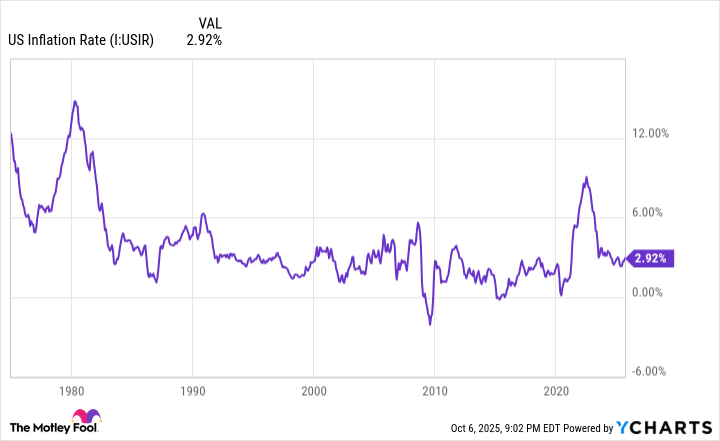

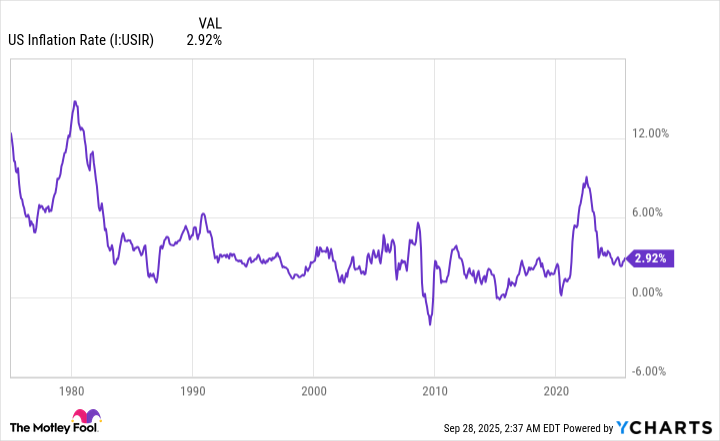

A higher prevailing rate of inflation in recent years has led to beefier annual COLAs. U.S. Inflation Rate data by YCharts.

A first-of-its-century raise is eventually headed retirees’ way

Once the SSA does have the necessary data to calculate and reveal the 2026 COLA, it’s a virtual certainty that beneficiaries will witness history being made.

Over the last four years, Social Security recipients — retired workers, workers with disabilities, and survivor beneficiaries — have enjoyed above-average cost-of-living adjustments. From 2022 through 2025, their Social Security checks grew by 5.9%, 8.7%, 3.2%, and 2.5%, respectively. To put these figures into some sort of context, the average COLA increase over the last 16 years was 2.3%.

Based on two independent estimates that were updated following the release of the August inflation report, a fifth-consecutive year above this 16-year average is expected.

Nonpartisan senior advocacy association The Senior Citizens League (TSCL) has pegged their 2026 COLA forecast at 2.7%, while independent Social Security and Medicare policy analyst Mary Johnson is calling for a slightly higher boost of 2.8%. These two forecasts would imply a roughly $54 to $56 per-month increase in the average retired-worker benefit in the new year.

More importantly, a 2.7% or 2.8% COLA would result in an event that hasn’t been witnessed in almost three decades. From 1988 through 1997, Social Security COLAs vacillated between 2.6% and 5.4%. If the 2026 COLA comes in at 2.5% or above, which looks like a virtual certainty based on independent estimates, it would mark the first time in 29 years that benefits will have risen by at least 2.5% for five consecutive years.

Image source: Getty Images.

The purchasing power of a Social Security dollar isn’t what it used to be

Unfortunately, this potentially history-making moment won’t be fully felt or enjoyed by aged beneficiaries. Though nominal payouts have notably climbed in recent years, the painful reality is that the buying power of Social Security income simply isn’t what it once was.

For example, you might be surprised to learn that the CPI-W isn’t doing retirees any favors. While this index is designed to mirror the inflationary pressures that Social Security’s retired workers are contending with, it has built-in flaws that keep this from happening.

The CPI-W is an index that tracks the cost pressures faced by “urban wage earners and clerical workers,” who, in many cases, are workers under the age of 62. By comparison, 87% of Social Security beneficiaries are 62 and above, as of December 2024.

Aged beneficiaries spend their money differently than workers under the age of 62. Specifically, retirees spend a higher percentage of their budget on medical care services and shelter than younger folks. Even though seniors make up 87% of all Social Security recipients, the CPI-W doesn’t account for the added importance of shelter and medical-care service costs in the COLA calculation.

Furthermore, the trailing-12-month inflation rate for shelter and medical care services has pretty consistently been higher than the annual COLAs beneficiaries have received. According to TSCL, this disparity has played a role in reducing the buying power of Social Security income by 20% from 2010 to 2024. A 2.7% or 2.8% cost-of-living adjustment isn’t going to offset or halt this decline in purchasing power.

To make matters worse, dual enrollees — those receiving Social Security income who are also enrolled in traditional Medicare — are expected to see sizable COLA offsets due to a projected double-digit percentage increase in the Part B premium in 2026.

Part B is the portion of Medicare responsible for outpatient services, and the premium for Part B is commonly deducted from a Social Security recipient’s monthly benefit. An estimate from the 2025 Medicare Trustees Report calls for an 11.5% jump in the Part B premium to $206.20 next year. For lifetime low earners, this increase might gobble up every cent of their projected 2026 COLA.

Regardless of whether or not Social Security’s 2026 COLA is delayed, it’ll mark another year where retirees get the short end of the stick.

Most Social Security recipients will be able to avoid paying taxes on their benefits.

People spend years paying into the Social Security system via payroll taxes. It’s a way of helping to secure somewhat of a financial safety net in your retirement years when you begin receiving benefits. Even if you’re fortunate enough not to need it, it’s a well-earned plus after decades of work and contributions.

Unfortunately, like most other income sources in America, when you receive your Social Security payments, you could potentially owe taxes on them. The good news is that most states don’t tax Social Security benefits. The bad news is that this still leaves others that do. As of October 2025, 41 states do not tax Social Security.

Image source: Getty Images.

Which states don’t tax Social Security benefits?

The following 41 states, along with Washington, D.C., currently do not tax Social Security benefits:

In the past five years, four states have eliminated their Social Security tax, so there’s still hope for people who live in a state with the tax. For example, West Virginians won’t have to pay taxes on benefits beginning in 2026.

You could still owe federal taxes on your Social Security check

Unfortunately, your state’s tax-free status doesn’t exempt you from federal taxes on your Social Security check. Luckily, most people won’t pay anything; however, there are still millions who will. To determine if you’ll be subjected to federal taxes on your Social Security benefits, the IRS considers your combined income, which includes the following:

For example, if your AGI is $15,000, you receive $20,000 annually from Social Security, and you have $200 in nontaxable interest, your combined income would be $25,200 ($15,000 + $10,000 + $200). After calculating your combined income, the following ranges are used to determine how much of your benefits are eligible to be taxed:

Percentage of Taxable Benefits Added to Income

Filing Single

Married, Filing Jointly

0%

Less than $25,000

Less than $32,000

Up to 50%

$25,000 to $34,000

$32,000 to $44,000

Up to 85%

More than $34,000

More than $44,000

Source: IRS.

To see it in action, let’s assume you receive $20,000 annually in benefits, and 50% is eligible to be taxed. In this situation, up to $10,000 would be added to any other income you have and then taxed at your normal income tax rate. It’s helpful to know how the federal tax works, so you don’t mistakenly assume that the IRS is going to take 50% or 85% of your benefits.

Some retirees could see a larger tax deduction

The Trump administration’s “big, beautiful bill” included a provision that provides a temporary tax deduction for eligible people age 65 and older. Single filers are eligible for up to $6,000, while couples filing jointly are eligible for up to $12,000.

To qualify for the full $6,000 deduction, single filers must have a modified adjusted gross income (MAGI) below $75,000. If your MAGI is between $75,000 and $175,000, you’re eligible for a reduced deduction, with the amount depending on where your income falls in the range.

Couples filing jointly must have a MAGI below $150,000 to qualify for the full $12,000. Any couple with a MAGI between $150,000 and $250,000 is eligible for the reduced deduction.

This deduction will remain in place until 2028 and is available even if you take the standard deduction (which would otherwise prohibit you from itemizing your deductions).

The largest US city is among more than 2,000 other municipalities pursuing similar lawsuits.

Published On 8 Oct 20258 Oct 2025

Share

New York City has filed a lawsuit accusing Facebook, Google, Snapchat, TikTok and other online platforms of fuelling a mental health crisis among children by addicting them to social media.

The 327-page complaint filed on Wednesday in federal court in Manhattan seeks damages from Facebook and Instagram owner Meta Platforms, Google and YouTube owner Alphabet, Snapchat owner Snap and TikTok owner ByteDance. It accused the defendants of gross negligence and causing a public nuisance.

Recommended Stories

list of 4 itemsend of list

The city joined other governments, school districts and individuals pursuing about 2,050 similar lawsuits in nationwide litigation in the Oakland, California, federal court.

New York City is among the largest plaintiffs with a population of 8.48 million, including about 1.8 million under age 18. Its school and healthcare systems are also plaintiffs.

Google spokesperson Jose Castaneda said allegations concerning YouTube are “simply not true”, in part because it is a streaming service and not a social network where people catch up with friends.

The other defendants did not immediately respond to requests for comment.

A spokesperson for New York City’s law department said the city withdrew from litigation announced by Mayor Eric Adams in February 2024 and pending in California state courts so it could join the federal litigation.

According to Wednesday’s complaint, the defendants designed their platforms to “exploit the psychology and neurophysiology of youth” and drive compulsive use in pursuit of profit.

The complaint said 77.3 percent of New York City high school students admitted to spending three or more hours a day on “screen time” including TV, computers and smartphones, contributing to lost sleep and chronic school absences.

New York City’s health commissioner declared social media a public health hazard in January 2024, and the city, including its schools, has had to spend more taxpayer dollars to address the resulting youth mental health crisis, the complaint said.

The city also blamed social media for an increase in “subway surfing”, or riding atop or off the sides of moving trains. At least 16 subway surfers have died since 2023, including two girls aged 12 and 13 this month, police data show.

“Defendants should be held to account for the harms their conduct has inflicted,” the city said. “As it stands now, [the] plaintiffs are left to abate the nuisance and foot the bill.”

Millions of retirees are waiting to learn how their benefits could change next year.

The government has been shut down since Oct. 1, after Congress was unable to pass a funding bill for the new fiscal year that started this month. With severe disagreements between Republicans and Democrats, many government agencies will remain closed indefinitely. Only essential services are allowed to continue operating, and government workers who aren’t furloughed are expected to continue working without pay until the shutdown is resolved.

Thankfully for the 70 million Americans receiving monthly Social Security benefits, those payments are considered essential. And for many households that’s the absolute truth. An important aspect of the program for households relying on Social Security to make ends meet is the annual cost-of-living adjustment, or COLA. Without it, many of those recipients would find their finances falling behind the rising prices stemming from inflation.

While payments are continuing amid the shutdown, many may be wondering what it means for next year’s COLA.

Image source: Getty Images.

The key data provider for next year’s COLA is shut down

The Social Security Administration is in charge of calculating the annual COLA, but it relies on data provided by another government agency — the Bureau of Labor Statistics. Every month, the BLS publishes a report detailing changes in the Consumer Price Index, or CPI, which is one of the most common metrics used to assess inflation.

The annual COLA is based on a specific version of the CPI, the CPI for Urban Wage Earners and Clerical Workers (CPI-W). The Social Security Administration takes the average increase in the CPI-W during the third quarter (July through September), and that number becomes the COLA for next year.

Unfortunately, the BLS is not considered an essential service. As a result, it’s not releasing new data, including the jobs report that was supposed to come out the first Friday of the month. The most recent update on its website simply states, “This website is currently not being updated due to the suspension of Federal government services.”

While we received an update on July and August’s CPI readings, September’s is currently scheduled for Oct. 15. If the government shutdown isn’t resolved by then, we’ll face a delay in the release of September’s CPI data, and, as a result, the 2026 COLA calculation. (Even if Congress resolves the shutdown earlier, it could take several days to compile the data and publish the report, resulting in a delay.)

The good news is the BLS likely completed its September data collection to get an accurate picture of price inflation during the last month of the quarter. BLS workers collect data throughout the month, dividing it into 10-day periods. With the government shutdown going into effect on Oct. 1, it likely collected all or most of the data needed to accurately calculate the CPI numbers for September.

That means the government shutdown is unlikely to have any impact on the 2026 COLA, even if the release of the information is delayed.

Here’s how big the 2026 COLA could be

Despite the potential delay, the 2026 Social Security COLA is shaping up to be a relatively large boost to benefits. As mentioned, we already have CPI reports for July and August, and those have provided a pretty clear picture on where inflation is heading.

The July CPI-W reading came in 2.5% higher than last year and the August reading climbed 2.8%. With fairly soft inflation over the summer last year, many expect the inflation rate continued accelerating in September. The Cleveland Fed’s NowCast estimates the September CPI-U reading (which is slightly different than the CPI-W used for the COLA) climbed 3%, up from 2.9% in August.

A similar bump in the CPI-W reading would result in a COLA of 2.7%. That’s in line with analyst expectations from The Senior Citizens League. Independent analyst Mary Johnson and the Committee for a Responsible Federal Budget project a 2.8% COLA.

Either way, Social Security beneficiaries are in line for a bigger raise than 2025’s 2.5% COLA. But that also means that prices have climbed faster this year, leaving many retirees trying to stretch their monthly payments further.

With most of the data available to make a fairly good guess as to what the 2026 COLA will be, retirees can start planning now even though the actual COLA release may be delayed due to the government shutdown.

If you claim Social Security early, you could find yourself wishing you had made a different choice as you cope with smaller monthly benefits.

You’ll make many decisions when preparing for retirement. Choosing when to file for Social Security benefits is one of the most important of those choices.

You have a long period when you could file for benefits, as you can claim as early as 62, but can also wait and increase the amount of your benefits until age 70. Picking the right moment within that eight-year timespan helps you maximize your income and build a more secure retirement.

For many people, an early claim seems like the obvious answer since you can start collecting right away and enjoying the benefits you’ve worked hard to earn all your life. In reality, though, claiming at a young age — and especially before your designated full retirement age — could be something you end up really regretting.

Here’s why.

Image source: Getty Images.

An early claim limits your ability to work

If you start receiving Social Security before your designated full retirement age (FRA), your decision could impact your ability to work because when you earn too much before FRA, your benefit checks are reduced or even eliminated.

For example, in 2025, if you won’t reach FRA during the entire year, then once you earn more than $23,400, you’ll lose $1 in benefits for every $2 earned above that limit. This could quickly lead to your Social Security checks disappearing entirely, since the Social Security Administration withholds full checks when you go above the limit.

This rule prevents double-dipping of benefits and a paycheck in the years before you reach FRA, and it can lead to a lot of hassle if you’re trying to track earnings to avoid losing benefits.

Eventually, you do get credit if checks are withheld, as your benefit is recalculated at your full retirement age to account for the missed money — but the process of slowly recovering the benefits you missed out on due to exceeding the work limits can be very frustrating.

You’ll take a big benefits cut that is permanent

Since you have an eight-year window to claim Social Security, there are rules in place to try to equalize out lifetime benefits so you get the same amount of money no matter when you claim.

One of those rules is that if you claim Social Security benefits before FRA, benefits are reduced by early filing penalties. But if you wait until after FRA, benefits are increased due to delayed retirement credits.

The penalties and credits apply monthly, as you’ll lose 5/9 of 1% of your standard benefit for each of the first 36 months you receive a check ahead of your FRA. If you claim even sooner, you lose an additional 5/12 of 1% for any of the prior months.

The monthly penalties add up to an annual 6.7% reduction from your standard benefit for years one, two, and three. For years four and five when you were collecting early Social Security benefits, the reduction in benefits is 5% annually. This means that a claim at 62 instead of at an FRA of 67 results in a 30% cut to benefits overall. That cut is permanent, and benefits will always be 30% smaller than they would have been had you waited to claim.

If you delayed beyond FRA until 70 instead, though, you’d have increased your benefits by 2/3 of 1% or 8% per year and received more benefits instead of smaller checks.

You’ll shrink your survivor benefits

You are not the only one who could regret your early Social Security claim. Your spouse could as well. When you die, your spouse either gets to keep receiving their own benefit or keep receiving yours. If you were the higher earner in your family and your Social Security benefit is a lot bigger, then keeping your benefit would be better for your surviving spouse.

The problem is, if you claimed Social Security ahead of schedule, you’d have shrunk your benefit — so your surviving spouse would be left with a smaller survivor benefit than they could have had. Since living on a single Social Security check instead of two is hard, your spouse could end up really wishing you hadn’t claimed early.

You stand a good chance of missing out on lifetime income

Finally, research has shown that around 7 in 10 retirees would find themselves with more lifetime income if they delay benefits until 70 instead of claiming at a younger age. If your goal is to maximize the lifetime income Social Security offers so you don’t have to rely as much on your 401(k) or other retirement plans, then you’ll want to avoid shrinking your lifetime income.

That’s especially true as Social Security is a reliable source of funds since there are cost-of-living adjustments built in that help you avoid losing buying power due to inflation.

Ultimately, an early claim is simply not the right option for many. When you are making your retirement plans, think seriously about whether you should prepare to try to put off your Social Security claim. If so, have a plan to do that, such as living on retirement savings until the day comes when you can claim a large benefit and set yourself and your spouse up for a more secure future.

It’s important to know the ins and outs of this often-confusing aspect of Social Security.

There are certain benefits to being married in retirement. For one thing, it’s nice to have somebody’s company at a time when you’re not working and may find yourself getting lonely and bored.

Retirement is also a time when a lot of people try to ramp up on travel. And it can be more enjoyable to have a travel partner than to take your dream trips on your own.

Image source: Getty Images.

When it comes to the financial side of retirement, being married also has its advantages. If you and your spouse each have some savings, you can pool your resources for a larger income.

Plus, if you’re married, it could mean that you’re eligible to receive spousal benefits from Social Security. And that extra money could come in very handy. But if you’re looking to claim spousal benefits from Social Security, it’s important to understand the ins and outs. Here are three misunderstandings you must get to the bottom of if you think spousal benefits are something you’ll end up filing for.

1. You can only claim spousal benefits if you’re married

You may start off retirement as a married couple only to decide to dissolve your relationship a few years down the line. Sometimes, too much togetherness can unveil differences that are just too difficult to overcome.

You might assume that if you get divorced, you won’t be eligible for Social Security spousal benefits. But if you were married for at least 10 years before that divorce, and you’re not remarried, then those spousal benefits should still be on the table.

2. You can only claim spousal benefits if you didn’t work

The nice thing about Social Security is that it will pay spousal benefits to people who didn’t work. But even if you did work, you may still be eligible for spousal benefits.

Let’s say you worked enough to qualify for Social Security, but your wages were much lower than your spouse’s. If the spousal benefit you’re entitled to is greater than the benefit you’re entitled to based on your own earnings record, then you’ll get that spousal benefit.

However, if your personal benefit is the larger number, that’s what Social Security will pay you. This system is more than fair, as it basically allows you to collect whichever benefit puts the most money in your pocket each month. The only thing you can’t do is double dip by collecting a spousal benefit plus your own benefit at the same time.

3. You can grow your spousal benefits by delaying your Social Security claim

If you’re claiming Social Security on your own wage history, there’s an upside to delaying your claim past full retirement age, which is 67 for anyone born in 1970 or later. For each year you do, until you turn 70, your monthly benefit gets a permanent 8% boost.

But when you’re claiming spousal benefits, there’s no sense in delaying past full retirement age. That’s because you can’t grow a spousal benefit the same way you can grow a benefit based on your own earnings record.

Social Security spousal benefits max out at 50% of what your spouse is eligible for at their full retirement age. If you claim them before reaching your full retirement age, they’ll be reduced. But they also can’t grow beyond 50% of what your spouse gets at their full retirement age.

You may end up relying on Social Security to provide quite a bit of your retirement income. So it’s important to understand how the program’s spousal benefits work, especially since they can differ from how regular retirement benefits work. Knowing the rules inside and out could prevent you from making a big mistake you regret later on.

Retired-worker beneficiaries can’t seem to catch a break.

The big day for Social Security’s more than 70 million traditional beneficiaries is right around the corner. Assuming the government shutdown doesn’t delay a key data release, on Oct. 15, the Social Security Administration will unveil a multitude of changes for the upcoming year, with the highlight being the 2026 cost-of-living adjustment (COLA).

For retired-worker beneficiaries, who accounted for more than 76% of all traditional Social Security recipients in August, the income they receive from this all-important program is often vital to their financial well-being. Almost a quarter-century of annual surveys from Gallup shows that 80% to 90% of retirees lean on their monthly Social Security check to cover some aspect of their expenses.

Social Security’s cost-of-living adjustment plays an important role for beneficiaries

Before digging into the nitty-gritty of what’s to come for program recipients, it’s imperative to understand why Social Security’s COLA exists.

The best way to view Social Security’s cost-of-living adjustment is as a near-annual “raise” that accounts for the effects of inflation that beneficiaries are contending with. Hypothetically, if a large basket of goods and services regularly purchased by Social Security beneficiaries increased in cost by 3% from one year to the next, Social Security payouts would also need to climb by the same percentage to avoid a loss of buying power. Social Security’s COLA is the raise that attempts to mirror the effects of rising prices (inflation).

Prior to 1975, there was no formula for calculating COLAs on an annual basis. From the very first payout in January 1940 through the end of 1974, only 11 cost-of-living adjustments were enacted by special sessions of Congress.

The near-annual COLAs we’re used to today began in 1975, which is when the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) was adopted as Social Security’s inflationary measure. The CPI-W is reported as a single figure on a monthly basis, which allows for quick year-over-year comparisons to determine if prices are, collectively, rising (inflation) or declining (deflation).

The quirk with Social Security’s COLA is that only three months of readings factor into the calculation: July, August, and September (i.e., the third quarter). If the average third-quarter CPI-W reading in the current year is higher than the comparable period of the previous year, inflation has taken place and beneficiaries are set for a higher payout. Payouts can stay the same year to year; they are not decreased, even if prices in the measured period drop.

A historic expansion of U.S. money supply sent the prevailing inflation rate and Social Security COLAs soaring. US Inflation Rate data by YCharts.

Independent Social Security COLA estimates for 2026 have been narrowed

Following a decade of anemic cost-of-living adjustments during the 2010s, the last four years have featured above-average COLAs. A historic expansion of U.S. money supply during the earlier days of the COVID-19 pandemic led to the highest prevailing rate of inflation in the U.S. in four decades. The result was a 5.9% COLA in 2022, followed by 8.7% in 2023, 3.2% in 2024, and 2.5% in 2025. To add some context to these payout increases, the average COLA over the previous 16 years is 2.3%.

The encouraging news (at least on paper) for Social Security recipients is that the 2026 COLA is on track to do something that hasn’t been witnessed in 29 years. For the first time since 1988 through 1997, the program’s raise is forecast to reach at least 2.5% for a fifth consecutive year. On a nominal-dollar basis, Social Security beneficiaries have seen their payouts notably increase over the last half-decade.

According to nonpartisan senior advocacy group The Senior Citizens League (TSCL), next year’s COLA is projected to come in at 2.7%. Independent Social Security and Medicare policy analyst Mary Johnson, who retired from TSCL early last year, foresees a slightly more robust payout boost of 2.8% in 2026.

If the assumption is made that one of these two forecasts proves accurate, the average monthly benefit for retired workers would climb by approximately $54 to $56 in 2026. Meanwhile, the average worker with disabilities and average survivor beneficiary would both see their monthly Social Security income rise by $43 to $44, respectively.

Image source: Getty Images.

The dreaded lose-lose scenario is looking likely for most retirees in 2026

The first issue relates to the inherent shortcomings of the CPI-W. While near-annual COLAs are a vast improvement compared to Congress passing along raises without rhyme or reason, the CPI-W is itself far from perfect.

As its full name makes clear, the CPI-W tracks the costs “urban wage earners and clerical workers” are facing. These are typically working-age Americans not currently receiving a Social Security benefit. More importantly, urban wage earners and clerical workers spend their money differently than seniors — and adults aged 62 and over make up 87% of Social Security’s traditional beneficiaries.

Older, retired Americans spend a larger percentage of their monthly budget on shelter and medical care services than working-age folks. Not only does the CPI-W not adequately account for the higher weighting retirees place on these two spending categories, but the trailing-12-month inflation rate for shelter and medical care services has been consistently higher than the COLA passed along to program recipients.

Retirees who are dually enrolled in Social Security and traditional Medicare are also set to lose in the upcoming year.

People who are enrolled in traditional Medicare and Social Security almost always have their Medicare Part B premium automatically deducted from their monthly Social Security payout. Part B is the portion of Medicare responsible for outpatient services.

In 2023 and 2024, the Part B premium rose by 5.9% each year. But based on estimates from the June-published Medicare Trustees Report, the Part B premium is forecast to climb 11.5% to $206.20 per month in the upcoming year. There’s little doubt that this is going to partially or fully offset the impact of next year’s Social Security COLA for most dual enrollees.

Even if the cost-of-living adjustment for 2026 surpasses TSCL’s and Johnson’s respective forecasts, it won’t be enough to pull retirees out of this lose-lose scenario in 2026.

When you see the name Social Security in the news, there’s often a negative context. For example, earlier this year, Social Security was in the news a lot when the program’s Trustees released an update about the program’s finances.

That update wasn’t great, as it looped people into the fact that Social Security may be looking at severe benefit cuts in less than a decade’s time, based on current projections.

Image source: Getty Images.

On Oct. 15, Social Security is likely to be all over the news again. Only this time, it’s not necessarily for a bad reason.

Oct. 15 is when the Social Security Administration (SSA) is expected to announce a number of key changes to the program. It pays to tune in — whether you’re receiving monthly benefits from the program or not.

A COLA will finally be revealed

For months, there’s been speculation about Social Security’s upcoming cost-of-living adjustment (COLA). Many seniors are hoping that 2026’s raise will be more generous than the 2.5% COLA they received at the start of 2025, and there’s some good news in that regard.

Initial estimates are calling for a 2.7% Social Security increase in 2026, which is clearly a notch higher than 2.5%. If inflation picks up in September, as well, Social Security recipients could see an even larger COLA in the new year.

An uptick in inflation isn’t necessarily a good thing. However, the silver lining is that it could drive 2026’s COLA higher.

Other key changes should come to light

An official 2026 COLA announcement may be the main event on Oct. 16, but the SSA will be sharing many key updates that day. For one, workers will want to stay tuned to see what 2026’s wage cap looks like.

In 2025, workers will pay Social Security taxes on up to $176,100 of income. But that number is likely to rise in the new year, a change that higher earners will need to gear up for.

The SSA should also share a new earnings-test limit. That limit applies to people who work while collecting Social Security before reaching full retirement age.

In addition, the SSA will announce how much in earnings it takes to get a single Social Security work credit. You must accumulate at least 40 work credits in your lifetime to be eligible for Social Security benefits in retirement, based on your personal earnings record. The maximum number of credits you can receive per year is four.

Right now, it takes $1,810 in earnings to get a work credit. However, just as the wage cap is expected to increase, so, too, is the value of a work credit.

Be sure to tune in

Clearly, Oct. 15 is an important day for Social Security, whether you’re getting benefits or not. It’s essential to pay attention to all of the changes happening in 2026 so you know what to expect from Social Security in 2026. That way, if any of those changes impact you negatively, such as having to pay taxes on more of your income, you’ll have time to make a game plan.

For 90 years, Social Security has provided Americans with a financial safety net. Today, Americans are concerned about potential cuts to the program.

Surveys may be little more than a snapshot in time, but they can provide an interesting peek into the minds of fellow Americans. This year, as Social Security turns 90, the Bipartisan Policy Center’s (BPC) American Savings Education Council polled Americans on how they feel about the current state of the program. Here’s what they learned.

Image source: Getty Images.

The big issues

Whether they’re just beginning to plan for retirement or have been chipping away at it for years, Americans value Social Security. The following represents their concerns, anxieties, and hopes.

Value of Social Security

93% of Americans surveyed consider Social Security a valuable federal program. In fact, it was rated higher than any other program respondents were asked about.

83% of those asked believe addressing Social Security’s challenges should be a top priority for the current Congress.

According to Jonathan Burks, Executive Vice President of Economic and Health Policy for the BPC: “Americans across the political spectrum agree strongly that Social Security matters, and they want to see bipartisan work to strengthen the program for the future. Now it is up to lawmakers to build on this consensus and do the hard work of forging a path forward.”

Social Security anxiety

74% of the public is concerned that Social Security will run out before they retire, and they won’t have access to the program they have spent decades paying into.

80% of those surveyed are worried that Congress will cut their benefits, particularly because 41% of Americans expect Social Security to be their primary source of income in retirement.

Bipartisan support for a solution

64% of Democrats and 61% of Republicans agree that strengthening Social Security will take bipartisan cooperation.

Losing patience

As the clock winds down on the Social Security trust fund, 67% of those polled say they want Congress to take action soon rather than wait until the situation worsens.

20% of respondents say they want a bipartisan commission created to come up with a comprehensive plan, and they want Congress to approve that plan

Financial realities of aging

71% of those surveyed claimed to be worried about whether they’ll have enough saved to retire comfortably.

67% are concerned about whether they’ll outlive their savings.

68% of 18- to 44-year-olds worry about finding the money to care for elderly relatives.

The current reality

If Congress doesn’t take steps to shore up the Social Security program, it’s expected that the Social Security trust fund will run dry in 2033. At that time, the Social Security Administration would begin across-the-board cuts of 23%. For example, a Social Security recipient with a monthly benefit of $2,000 would see their checks reduced to $1,540.

While it’s impossible to see the future, here are some of the expected consequences of cuts to Social Security:

Increased poverty rates: Given the number of retirees who count on Social Security to pay all or the majority of their living expenses, reductions in benefits are likely to lead to an increase in Americans living in poverty. Even for those retirees who did everything they could to maximize their benefits, cutting funds they earned and have come to count on could be devastating.

Political consequences: No politician wants to be the one responsible for raising taxes or asking people to work longer. That’s natural. However, failure to adequately address the Social Security issue could leave anxious Americans less happy with their elected representatives.

Economic impact: Lower benefits are likely to cause consumers to pull back on spending. This move could have a broader impact on the overall economy as retirees have historically spent their benefits on essential goods and services.

Greater pressure on other programs: Smaller Social Security benefit checks mean more people turning to the different government programs to survive. However, recent cuts to programs like the Supplemental Nutrition Assistance Program (SNAP) and Meals on Wheels could make it more difficult for seniors to receive the assistance they need.

“The only way we get a fix is if the two parties hold hands and jump together,” Shai Akabas, Vice President of Economic Policy at BPC, said in the report. “These results show that the American people understand and support that outcome. It’s time for our elected leaders to follow suit.”

Big news for retirees is on the way in just 17 days.

Seventeen days. That’s how much longer Social Security beneficiaries must wait to find out how big their “raise” will be in 2026.

The Social Security cost-of-living adjustment (COLA) countdown is about to kick into overdrive. But you don’t have to sit on pins and needles in anticipation of the official COLA announcement on Oct. 15, 2025, to have a pretty good feel for what the increase will be.

Image source: Getty Images.

The best COLA prediction right now

If you want to know how big of a Social Security benefit increase to expect, probably the best place to turn is The Senior Citizens League (TSCL). This nonprofit organization has advocated for seniors since 1992, initially as part of The Retired Enlisted Association and then as an independent entity beginning in 1994.

TSCL developed a sophisticated statistical model that projects the next Social Security COLA. This model is updated monthly. It incorporates inflation and unemployment data, as well as the interest rates set by the Federal Reserve.

Earlier this month, TSCL announced its final prediction for the 2026 Social Security COLA. The organization projects an increase of 2.7%, a little higher than the 2.5% COLA given in 2025. It’s also slightly above the average benefit adjustment over the last 20 years of 2.6%.

How much additional money will this COLA give retirees? It depends on your current benefit amount, of course. However, the average increase will be $54 per month if TSCL’s model is right.

What could change by Oct. 15?

The Social Security Administration (SSA) already has most of the data it needs to calculate next year’s COLA. It will receive the last piece on Oct. 15 when the U.S. Bureau of Labor Statistics (BLS) releases its inflation numbers for September.

SSA doesn’t use the most widely followed inflation metric in the BLS report, the Consumer Price Index. Instead, the agency bases the annual Social Security COLA on a different statistic — the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). As its name indicates, this index measures how much prices have increased for blue-collar workers in urban areas.

The COLA is calculated by determining the percentage increase (if any) between the CPI-W for the third quarter of the current year and the CPI-W in the third quarter of the previous year. SSA only needs to plug in the CPI-W for September to crunch the numbers.

Could the actual 2026 COLA that will be announced on Oct. 15 differ from the 2.7% predicted by TSCL? Absolutely. Inflation could be higher in September than anticipated, perhaps due to the impact of tariffs making their way through the U.S. economy. On the other hand, the effects of tariffs could be more muted than TSCL’s model projects, resulting in a lower COLA. Either way, TSCL’s projected number will probably be close to the actual 2026 COLA.

One “gotcha”

Retirees shouldn’t count on having an additional 2.7%, give or take a couple of percentage points, reach their bank accounts, though. There’s one “gotcha” that will likely reduce how much extra money you’ll receive.

Most retirees ages 65 and older have their Medicare premiums automatically deducted from their monthly Social Security benefit payments. Unfortunately, your Medicare Part B premiums will almost certainly be much higher than the expected 2.7% Social Security increase.

The Medicare Trustees project that Part B premiums will rise by 11.6%. This translates to an extra expense of $21.50, enough to wipe out much of the average retiree COLA of $54. The annual Medicare Part B deductible will also likely jump by $31 to $288 next year.

The countdown is on for finding out the exact amounts for the 2026 Medicare Part B premiums and deductibles, too. While the numbers will probably be announced in October, retirees might not learn how their pocketbooks will be impacted as soon as they learn what their Social Security COLA will be.

The world is a confusing and scary place right now. Many of us are anxious wanderers in the wilderness, looking for answers. Is it any wonder that the wellness industry is booming? Into this strange new world comes Jade Chang’s funny and poignant novel “What a Time to Be Alive,” whose protagonist Lola is broke and aimless — until a leaked video transforms her into an instant self-help guru.

Chang, whose first novel, “The Wangs vs. The World,” was a sharp satire on class and ambition, has now turned her gaze to the promise and peril of self-actualization through social media. I sat down with Chang to discuss spiritualism for profit, tech bros and trucker hats.

You’re reading Book Club

An exclusive look at what we’re reading, book club events and our latest author interviews.

(Please note: The Times may earn a commission through links to Bookshop.org, whose fees support independent bookstores.)

✍️ Author Chat

Book jacket of “What a Time to Be Alive” by Jade Chang

(Los Angeles Times illustration; book jacket from Ecco)

This book almost didn’t make it, as you physically lost it.

I started it years ago. I was writing in longhand in a notebook, entire chapters of the book. I lost the notebook and I was devastated. Then I moved on and wrote “The Wangs vs. The World.” It took a long time to get back into writing this new book. By the time I circled back to it, the world had changed so much. I think I have become more generous about things, and the story benefited from it.

Lola, your protagonist, unwittingly becomes an online self-help guru on the basis of a leaked video that is posted on social media. She becomes a sort of accidental wellness expert.

As someone who didn’t grow up with religion, I have always been really fascinated by belief. Why do we want to believe, and how are we compelled to certain beliefs? And it was just kind of fascinating and amazing that people could find so much life in religious stories. As I was developing the story of this novel, I realized that everyone in the digital world takes a page from this book as well, using stories to convert listeners into believers. I think Lola starts out sort of thinking she is in above her head, but by the end, her sincerity shines through. She wants to believe what she is telling others to believe.

Do you think the internet breeds cynicism and has turned us all into an angry mob?

I don’t. The digital world doesn’t make us any different from who we are, but it can throw a lens on certain aspects of our behavior. I think the internet allows us to be our best and worst selves. Think about all those strangers who might contribute to a GoFundMe campaign because someone has had a serious injury and needs to pay their medical bills, which can yield tens of thousands of dollars in some cases. That’s the mob functioning at its best.

But isn’t it a little too easy to pull a con job online?

Yes, it’s easy to be inauthentic online, but it’s important to remember that online performance is a tiny percentage of someone’s life. That’s why I was so interested in writing about the rise of this self-help guru, because usually when these stories are told you only see it from the acolyte’s point of view or the skeptic’s point of view. But we all have to make money, and we all are pulling a little something over on someone at some point — it’s part of surviving in the world.

Lola cauterizes the pain in her personal life by offering panaceas to pain for strangers online, but she affects a false persona to do so.

It’s easy to assume that anything we do, whether it’s on social media or elsewhere online, is performative or fraudulent in some way. RuPaul has a great quote where he says gender is drag. Everything is drag, a performance. Every choice we make is often not reflective of our essential self. You can’t codify identity in clothes or that trucker hat you’re wearing; anything you’re going to choose is going to be influenced by the times in which you live and who you surround yourself with. I can only speak from experience, but I think it’s almost impossible to suppress your true self.

You mentioned how self-help gurus and tech bros have a similar public worldview.

As research for the book, I attended one of Oprah’s Super Soul Sundays at Royce Hall. Every single person that spoke had the same arc: “I was down in the dumps, and then I looked up from that hole and I saw a glimmer in the form of CrossFit,” or drumming, or whatever it was that pulled them up from the brink. Then I went to a TED talk, and these tech gurus are saying the exact same thing. It’s the narrative of our time. I saw that crossover, and I knew I had something to say. I was interested in this internal push and pull of, how much do you give in to this tactic, and how much do you not.

📰 The Week(s) in Books

(Jay L. Clendenin / Los Angeles Times)

Hamilton Cain has mixed feelings about Patricia Lockwood’s autofictional account of the COVID-19 lockdown, “Will There Ever Be Another You,” praising Lockwood’s “rich and kinetic” prose but bemoaning her “self-indulgent and repetitious” narrative.

Steve Henson has a chat with tennis legend Björn Borg about his new memoir, “Heartbeats,” which delves into his heavy cocaine and alcohol use that began shortly after he walked away from the sport at age 26.

Karen Palmer’s harrowing memoir, “She’s Under Here,” “details forgery, a child’s kidnapping, a mental breakdown, struggles to stay afloat — and joy,” writes Bethanne Patrick.

And David A. Keeps reports on the fiscal inequities of the booming audiobook industry: “Many actors are vying for audiobook roles at a time when the talent pool is expanding and casting is becoming a growing topic of debate.”

📖 Bookstore Faves

The Book Jewel, located in the city of Westchester, is just minutes from LAX.

(The Book Jewel)

The Book Jewel is a welcome addition to the neighborhood of Westchester, an expansive bookstore with an excellent selection of fiction and nonfiction titles for locals, or those who might stop by there before catching their flight at nearby LAX. We talked with general manager Joseph Paulsen about the store.

Your store is serving a community that hasn’t had a general interest bookstore in quite some time.

The Book Jewel opened smack-dab in the middle of the global COVID-19 pandemic in August of 2020. Our Westchester community has supported us from Day 1, and we recently celebrated our fifth anniversary. We are the only bookstore in Westchester, and we are locally owned and independent. I live here in Westchester and have raised both of my sons here.

What’s selling right now?

Right now we’re selling tons of children’s literature and graphic novels (“InvestiGators,”Dav Pilkey, etc.). Of course, the ABA Independent Bestsellers. Lots of romantasy.

You are pretty close to LAX. Do you sell a lot of books to travelers?

The travelers give themselves away with their roller bags, and we catch ’em heading out of Los Angeles on the reg! They like long books for long flights. Lots of souvenirs too! We have some unique, local non-book items as well and offer a better vibe than the international terminal.

The Book Jewel is located at 6259 W. 87th St, Los Angeles, CA.

Warren Buffett has spent decades championing the importance of Social Security benefits.

Warren Buffett has built a reputation for studying the landscape and spotting financial issues before others realize there’s a problem. Twenty years ago, at a 2005 Berkshire Hathaway meeting, Buffett was blunt: “I basically believe that anything that would take Social Security payments below their present guaranteed level is a mistake.”

Image source: Getty Images.

The problem has been brewing

Based on any retirement planning you’ve done, you’ll probably not be surprised that the Social Security trust is in serious danger of running dry. The program collects payroll taxes under the Federal Insurance Contributions Act (FICA). Both employees and employers contribute 6.2% of the employees’ wages, up to the annual wage base limit of $176,100.

The money collected today goes toward paying Social Security benefits to current beneficiaries. When the Social Security Administration (SSA) collects more than it pays out, the remaining money goes into the Old-Age and Survivors Insurance Trust Fund (OASI) and is invested in Treasury securities. When the SSA collects less in Social Security payroll taxes than it pays out, the SSA must dip into the trust fund for the money it needs to pay the benefits earned.

According to the SSA’s 2024 Trustees Report, the OASI trust fund is projected to become depleted in 2033, unless Congress intervenes to shore up the program. While several factors have played a role in draining the fund, demographics may be the most critical. In 1960, there were 5.1 workers for every Social Security recipient. Today, that number is just 2.8 and expected to continue falling.

The SSA cannot pay full Social Security benefits once the money invested in Treasury securities is gone. At that point, the Trustees say that Social Security benefits would be reduced by 23%.

Buffett’s proposals to get Social Security back on solid ground

Buffett has been consistent about recommending moderate changes to the program, including:

Remove the taxable earnings cap

As of 2025, Social Security taxes only apply to incomes up to $176,100. For example, a person who earns $400,000 annually only pays Social Security taxes on the first $176,100. No Social Security taxes are collected on the remaining $223,900.

Buffett believes that the U.S. should eliminate this cap so that higher earners can contribute more to the program. This approach would boost Social Security revenue significantly and is unlikely to affect the financial stability of wealthier taxpayers.

Slightly increase payroll taxes

No one enjoys a tax hike, which may help explain why politicians have been so hesitant to suggest them. Politicians want to be seen as the people who cut taxes. There’s only one problem with that: Cutting taxes isn’t always good for the long term. For example, President Donald Trump’s “Big, Beautiful Bill“ expanded the standard deduction for seniors and lowered how much can be collected in taxes on benefits.

Add that to the Social Security Fairness Act signed into law by President Joe Biden in early January 2025. The Social Security Fairness Act eliminated the Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) rules. These two programs decreased the amount that over 3.2 million people — including teachers, police officers, firefighters, and federal employees — were eligible to receive in Social Security benefits.

While each tax break may have come as welcome news to most, the Committee for a Responsible Federal Budget (CRFB) found that they shaved a full year off the expected solvency timeline, meaning money is being drained from the Social Security trust fund at a faster rate than believed just last year.

Buffett suggests a slight boost in Social Security payroll taxes, saying even a modest hike would generate additional funds over time. In addition, a small tax hike would help secure the program’s financial stability without unfairly burdening workers or employers.

Raise the full retirement age (FRA)

In 1960, American men could expect to live to age 66.6 on average, and American women to age 73.1. Today, American men can expect to live to 77.2 on average, and American women to age 82.1. This increase in life expectancy means more years in retirement, and more Social Security benefits paid out. The SSA could stretch the Social Security trust fund further by raising the FRA.

Reduce Social Security benefits for wealthy retirees