Range Financial Group LLC fully exited its position in Fortinet(FTNT 0.45%), selling 29,944 shares for an estimated $3.2 million, according to an SEC filing dated Oct. 17.

The fund sold its entire position in Fortinet.

The position previously accounted for 1.2% of the fund’s AUM

What happened

According to a filing with the Securities and Exchange Commission dated October 17, 2025, Range Financial Group LLC sold its entire stake in Fortinet. The firm liquidated the 29,944 shares it held, with the estimated value of the transaction based on the quarterly average price totaling $3.2 million. The fund now holds no position in Fortinet.

What else to know

The fund sold out of Fortinet, reducing its exposure from 1.2% of AUM as of June 30, 2025 to zero

Top holdings after the filing:

NYSEMKT: GJAN: $13.9 million (5.0% of AUM) as of Sept. 30

NASDAQ: NVDA: $10 million (3.6% of AUM) as of Sept. 30

NASDAQ: STX: $7.7 million (2.8% of AUM) as of Sept. 30

NYSEMKT: SPLG: $7.2 million (2.6% of AUM) as of Sept. 30

NYSEMKT: PJAN: $7.1 million (2.6% of AUM) as of Sept. 30

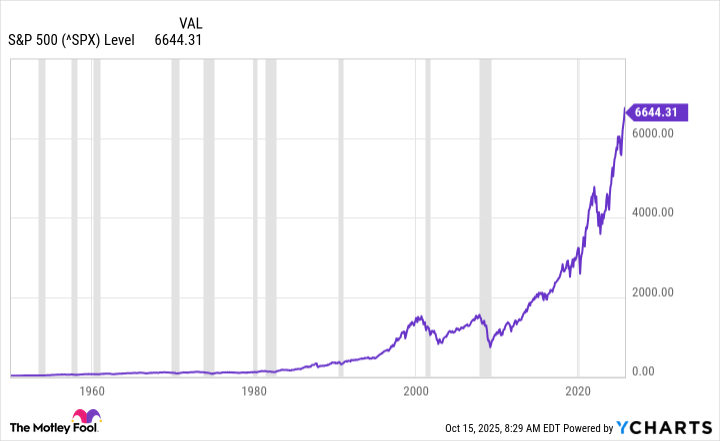

Shares of Fortinet closed at $83.44 on Oct. 17, 2025, up 3.2% over the past year but underperforming the S&P 500’s total return by 12.4 percentage points

Company overview

Metric

Value

Market Capitalization

$63.94 billion

Revenue (TTM)

$6.34 billion

Net Income (TTM)

$1.94 billion

Price (as of market close 10/17/25)

$83.44

Company snapshot

Fortinet, Inc. is a global provider of integrated cybersecurity solutions, offering a broad product portfolio and scalable security infrastructure. The company leverages a mix of proprietary hardware and software to deliver robust network protection and threat mitigation for enterprises of all sizes.

It serves a diverse global customer base across telecommunications, technology, government, financial services, education, retail, manufacturing, and healthcare sectors.

The company generates revenue primarily through hardware and software sales, security subscriptions, technical support, and professional services, leveraging a channel partner distribution model alongside direct sales.

Foolish take

Range Financial sold its entire position after adding shares during the second quarter. During the June 30 through Sept. 30 period, the fund boosted its share ownership from 2.7 million shares to nearly 3.2 million shares.

However, the share sale follows the market’s negative reaction following Fortinet’s second-quarter earnings release on Aug. 6, sending the share price down nearly 22% the following day.

The company reported a 14% revenue increase to over $1.6 billion, the high end of management’s quarterly guidance. The company also reported adjusted diluted earnings per share of $0.64, exceeding its budgeted figure. Management also raised its annual EPS guidance.

Nonetheless, investors focused on Fortinet’s announcement that it has completed 40% to 50% of its planned firewall upgrade cycle. The higher-than-expected figure led to concern that many customers have already upgraded, limiting future revenue growth. Several analysts downgraded their ratings following the announcement.

Glossary

AUM (Assets Under Management): The total market value of investments managed by a fund or investment firm. Liquidated: Sold off an entire investment position, converting it to cash. Exposure: The proportion of a portfolio invested in a particular asset, sector, or market. Channel partner distribution model: A sales approach where products are sold through third-party partners rather than directly to customers. Stake: The amount of ownership or shares held in a company or investment. Quarterly average price: The average price of a security over a three-month reporting period. Reportable U.S. equity assets: U.S. stock holdings that must be disclosed in regulatory filings. TTM: The 12-month period ending with the most recent quarterly report. Security subscriptions: Ongoing service contracts providing access to cybersecurity updates and support. Centralized management: A system that allows control and monitoring of multiple devices or services from a single platform. Endpoint protection: Security solutions designed to protect devices like computers and smartphones from cyber threats. Threat mitigation: Actions or technologies used to reduce or prevent cybersecurity risks.

Lawrence Rothman has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Fortinet and Nvidia. The Motley Fool has a disclosure policy.

LAS VEGAS — Aaron Mahan is a lifelong Republican who twice voted for Donald Trump.

He had high hopes putting a businessman in the White House and, although he found the president’s monster ego grating, Mahan voted for his reelection. Mostly, he said, out of party loyalty.

By 2024, however, he’d had enough.

“I just saw more of the bad qualities, more of the ego,” said Mahan, who’s worked for decades as a food server on and off the Las Vegas Strip. “And I felt like he was at least partially running to stay out of jail.”

He’s no Trump hater, Mahan said. “I don’t think he’s evil.” Rather, the 52-year-old calls himself “a Trump realist,” seeing the good and the bad.

Here’s Mahan’s reality: A big drop in pay. Depletion of his emergency savings. Stress every time he pulls into a gas station or visits the supermarket.

Mahan used to blithely toss things in his grocery cart. “Now,” he said, “you have to look at prices, because everything is more expensive.”

In short, he’s living through the worst combination of inflation and economic malaise he’s experienced since he began waiting tables after finishing high school.

Views of the 47th president, from the ground up

Las Vegas lives on tourism, the industry irrigated by rivers of disposable income. The decline of both has resulted in a painful downturn that hurts all the more after the pent-up demand and go-go years following the crippling COVID-19 shutdown.

Over the last 12 months, the number of visitors has dropped significantly and those who do come to Las Vegas are spending less. Passenger arrivals at Harry Reid International Airport, a short hop from the Strip, have declined and room nights, a measure of hotel occupancy, have also fallen.

Mahan, who works at the Virgin resort casino just off the Strip, blames the slowdown in large part on Trump’s failure to tame inflation, his tariffs and pugnacious immigration and foreign policies that have antagonized people — and prospective visitors — around the world.

“His general attitude is, ‘I’m going to do what I’m going to do, and you’re going to like it or leave it.’ And they’re leaving it,” Mahan said. “The Canadians aren’t coming. The Mexicans aren’t coming. The Europeans aren’t coming in the way they did. But also the people from Southern California aren’t coming the way they did either.”

Mahan has a way of describing the buckling blow to Las Vegas’ economy. He calls it “the Trump slump.”

::

Mahan was an Air Force brat who lived throughout the United States and, for a time, in England before his father retired from the military and started looking for a place to settle.

Mahan’s mother grew up in Sacramento and liked the mountains that ring Las Vegas. They reminded her of the Sierra Nevada. Mahan’s father had worked intermittently as a bartender. It was a skill of great utility in Nevada’s expansive hospitality industry.

So the desert metropolis it was.

Mahan was 15 when his family landed. After high school, he attended college for a time and started working in the coffee shop at the Barbary Coast hotel and casino. He then moved on to the upscale Gourmet Room. The money was good; Mahan had found his career.

From there he moved to Circus Circus and then, in 2005, the Hard Rock hotel and casino, where he’s been ever since. (In 2018, Virgin Hotels purchased the Hard Rock.)

Mahan, who’s single with no kids, learned to roll with the vicissitudes of the hospitality business. “As a food server, there’s always going to be slowdowns and takeoffs,” he said over lunch at a dim sum restaurant in a Las Vegas strip mall.

Mahan socked money away during the summer months and hunkered down in the slow times, before things started picking up around the New Year. He weathered the Great Recession, from 2007 to 2009, when Nevada led the nation in foreclosures, bankruptcies soared and tumbleweeds blew through Las Vegas’ many overbuilt, financially underwater subdivisions.

This economy feels worse.

Over the last 12 months, Las Vegas has drawn fewer visitors and those who have come are spending less.

(David Becker / For The Times)

With tourism off, the hotel where Mahan works changed from a full-service coffee shop to a limited-hour buffet. So he’s no longer waiting tables. Instead, he mans a to-go window, making drinks and handing food to guests, which brings him a lot less in tips. He estimates his income has fallen $2,000 a month.

But it’s not just that his paychecks have grown considerably skinnier. They don’t go nearly as far.

An admitted soda addict, he used to guzzle Dr Pepper. “You’d get three bottles for four bucks,” Mahan said. “Now they’re $3 each.”

He’s cut back as a result.

Worse, his air conditioner broke last month and the $14,000 that Mahan spent replacing it — along with a costly filter he needs for allergies — pretty much wiped out his emergency fund.

It feels as though Mahan is just barely getting by and he’s not at all optimistic things will improve anytime soon.

“I’m looking forward,” he said, to the day Trump leaves office.

::

Mahan considers himself fairly apolitical. He’d rather knock a tennis ball around than debate the latest goings-on in Washington.

He’s not counting on much. “I’m never convinced of anything,” Mahan said. “Until I see it.”

Something else is poking around the back of his mind.

Mahan is a shop steward with the Culinary Union, the powerhouse labor organization that’s helped make Las Vegas one of the few places in the country where a waiter, such as Mahan, can earn enough to buy a home in an upscale suburb like nearby Henderson. (He points out that he made the purchase in 2012 and probably couldn’t afford it in today’s economy.)

Mahan worries that once Trump is done targeting immigrants, federal workers and Democratic-run cities, he’ll come after organized labor, undermining one of the foundational building blocks that helped him climb into the middle class.

“He is a businessman and most businesspeople don’t like dealing with unions,” Mahan said.

There are a few bright spots in Las Vegas’ economic picture. Convention bookings are up slightly for the year, and look to be strengthening. Gaming revenues have increased year-over-year. The workforce is still growing.

“This community’s streets are not littered with people that have been laid off,” said Jeremy Aguero, a principal analyst with Applied Analysis, a firm that provides economic and fiscal policy counsel in Las Vegas.

“The layoff trends, unemployment insurance, they’ve edged up,” Aguero said. “But they’re certainly not wildly elevated in comparison to other periods of instability.”

That, however, offers small solace for Mahan as he makes drinks, hands over takeout food and carefully watches his wallet.

If he knew then what he knows now, what would the Aaron of 2016 — the one so full of hope for a Trump presidency — say to the Aaron of today?

Mahan paused, his chopsticks hovering over a custard dumpling.

Why Domino’s may deliver market-beating returns to the investment giant.

As many stock market observers know, Warren Buffett‘s Berkshire Hathaway has been a net seller of stocks. The most notable sale has been Apple. That position made up over 40% of the portfolio at one time, but the share has since fallen to around 22%.

What investors need to understand is that the selling does not mean Buffett’s team isn’t buying stocks at all. One notable recent purchase has been Domino’s Pizza (DPZ -0.03%). The stock’s past gains and its value proposition have likely inspired this investment, and such optimism warrants a closer look at the business and the stock to see if it is a suitable choice for average investors.

Image source: Getty Images.

Berkshire Hathaway and Domino’s

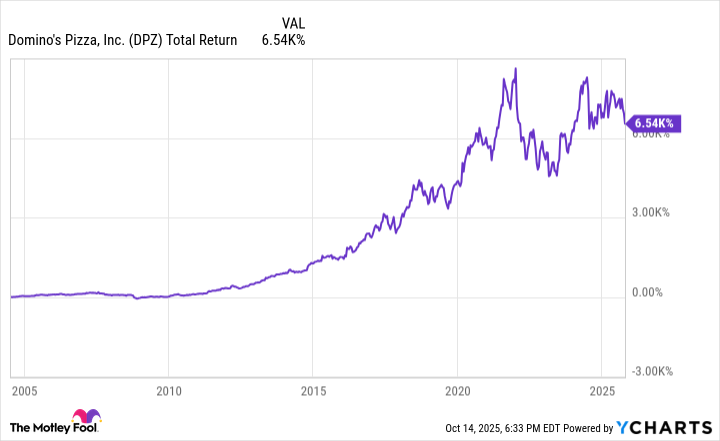

Domino’s has returned more than 6,500% in stock gains and dividend payments since it went public in 2004. Most investors, including Berkshire Hathaway, have missed out on most of those gains, but Berkshire’s bets could indicate that significant upside remains.

Buffett’s company began buying Domino’s shares in the third quarter of 2024 and has increased its position size in every quarter since that time. Today, it holds just over 2.6 million shares, or about 7.75% of the outstanding shares.

Another possible factor in Berkshire’s investment in Domino’s is that it is the world’s largest pizza chain, boasting 21,750 locations globally as of the end of fiscal Q3. Despite that success, investors may question why an investor would want to get into a business like pizza, which at least in theory, has low barriers to entry.

However, no other pizza business has grown to the same size, and one can find the kinds of competitive advantages that attract investors like Buffett when looking at Domino’s more closely.

One key part of Domino’s is its franchise model. This enables the chain to open a large number of locations with a relatively small amount of capital, leveraging high brand recognition to drive business.

Moreover, it offers a digital-first approach, which makes ordering easier and capitalizes on route planning for faster deliveries. Additionally, an efficient supply chain helps standardize food quality and costs, increasing consistency across locations.

Furthermore, despite a global footprint, Domino’s adapts its menu to suit local tastes, and new offerings such as parmesan-stuffed crust or added customization options keep its customers coming back to Domino’s.

The financial case for Domino’s

Buffett’s team was likely also drawn by its financial metrics. Indeed, with its global footprint, the maturity of the business appears to make it more of a value stock.

In the first nine months of fiscal 2025 (ended Sept. 8), revenue of $3.4 billion rose by 4%. Nonetheless, during that time, its free cash flow of $496 million surged 32% higher over the same timeframe. Gains on assets and lower capital expenditures bolstered that cash position.

Additionally, that free cash flow easily covered the company’s $119 million in dividend costs in the first nine months of the fiscal year. At $6.96 per share, its 1.6% dividend yield is well above the 1.2% average for the S&P 500. Buffett’s team also probably liked its 13-year history of payout hikes, a trend that makes further annual payout hikes likely to continue.

Investors should also take note of the pizza chain’s valuation. Its P/E ratio of 25 is below the company’s five-year average earnings multiple of 30. Also, since its P/E ratio has not fallen significantly below 25 since the early 2010s, one can assume that Domino’s stock sells at a reasonable price.

Should you follow Berkshire Hathaway into Domino’s stock?

Given the state of the company, investors can likely make a prudent move by following Berkshire Hathaway into Domino’s stock.

Indeed, a 6,500% total return over the stock’s history may cause some prospective buyers to shy away, particularly because of the competitive nature of the pizza industry.

However, Domino’s brand recognition and its focus on franchising, operational efficiency, and a robust supply chain give the company a competitive advantage. Moreover, investors can buy the stock at a relatively reasonable price and collect an above-average dividend yield.

In the end, even if Domino’s does not generate excitement, the stock is likely to cook up rising dividends and market-beating returns over time.

You can make a strong argument that buying the S&P 500 index is a good choice today, but maybe you should consider some value stocks, too.

The S&P 500 index (SNPINDEX: ^GSPC) is trading near all-time highs. Since the Vanguard S&P 500 Index ETF(VOO 0.60%) tracks the S&P 500, it is also trading near all-time highs. And it could still be a smart move to buy the index via an investment in the exchange-traded fund.

But there might be a smarter choice, if you take valuations into consideration. Which is where another Vanguard exchange-traded fund (ETF) comes into play. Here’s what you need to know.

Just get started

One of the biggest things any investor can do is get started. So if you have $1,000 to invest and you’ve never done so before, it could be a very good idea to just buy the market. By default, that would be the S&P 500 index for most investors. And then you should just keep buying the market every single month to benefit from dollar-cost averaging.

Image source: Getty Images.

Since all of the products that track the same index basically do the same thing, the Vanguard S&P 500 ETF is going to be a top choice. With an expense ratio of just 0.03%, it is one of the cheapest ways to gain exposure to the S&P. Why pay more for the same basic service? As the chart below shows, the market has recovered from even the worst bear markets and then moved on to reach even higher highs.

If you have $1,000 or $10,000 (or even more) to invest, just getting started is going to be the smartest move. Then, keep going and never look back.

Sure, in the near term, you might suffer through some paper losses. But over the long term, history suggests you’ll still make out just fine. If buying when things are expensive is just too much for you, however, you might find that the Vanguard Value ETF(VTV 0.51%) is an even smarter choice.

Why go the value route?

A $1,000 investment in the Vanguard Value ETF will buy you around five shares of the exchange-traded fund. What you will end up owning is a portfolio of large U.S. companies that have valuations that are low relative to the broader market. With the S&P 500 near all-time highs, that’s not an insignificant issue.

Putting some numbers on this might help. The Vanguard Growth ETF(VUG 0.56%), the opposite extreme from the value ETF, has an average price-to-earnings ratio of around 40. That’s pretty expensive, but you would expect that, given its focus on growth.

The Vanguard S&P 500 Index ETF has an average P/E of about 29. Still pretty high, thanks to the fact that some very large technology stocks (which tend to be growth-focused) are driving its performance. The Vanguard Value ETF’s average P/E is a little under 21. It wouldn’t be fair to call 21 cheap, but it is most certainly cheaper than both the S&P 500 and Vanguard Growth ETF.

The same trend exists with the price-to-book-value ratio (P/B). The Vanguard Growth ETF comes in with a P/B ratio of 12.5, the Vanguard S&P 500 Index ETF sits at 5.2, and the Vanguard Value ETF is the lowest on the valuation metric at just 2.8. While it won’t necessarily save you from a bear market, focusing on value stocks when growth is in favor could soften the pain of a deep downturn.

Get started first, but consider a value component when you do

To reiterate the theme here, the most important investment decision you can make is to start investing in the first place. The second one is to keep it up even when times get tough on Wall Street. But if you have already made those choices, then maybe it makes sense to consider taking a more nuanced approach with what you choose to buy.

If all you have is $1,000 to start, perhaps consider splitting it between the S&P 500 Index ETF and the Value ETF, to lean you toward cheaper stocks. If you already have a portfolio, then the smartest move could be to put a grand into just the Value ETF to help diversify you away from the growth stocks that are leading the market into the nosebleed seats.

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Vanguard Index Funds-Vanguard Growth ETF, Vanguard Index Funds-Vanguard Value ETF, and Vanguard S&P 500 ETF. The Motley Fool has a disclosure policy.

Seeing which company a big tech player is investing in is a wise move by investors.

Quantum computing is becoming a popular investment theme in the market, but there’s just one problem: It’s still a few years away from commercial relevance. This makes it nearly impossible to predict which company will be a major winner in this field. Adding to the difficulty of quantum computing investing is that the technology is incredibly complicated and can be difficult to understand. However, not investing in quantum computing could be a massive mistake for your portfolio’s future returns.

So, what should investors do? One advantage investors can get in this investment sector is looking at which competitors have strong backers. Amazon(AMZN -0.61%) is one tech giant that is investing in this space and is backing one of the leading pure plays: IonQ(IONQ -3.92%). This gives IonQ a vote of confidence from one of the biggest companies in the world, making IonQ an intriguing stock to invest in.

Amazon owns a small amount of IonQ

We know that Amazon is investing in IonQ from its Form 13F, which informs investors what other stock holdings Amazon has because its investment portfolio is greater than $100 million. As of its last report filed for Q2 holdings, Amazon holds nine stocks, with IonQ being one of them.

Amazon holds just over 850,000 shares of IonQ. While that may sound like a lot, that’s only about 0.3% of IonQ’s total shares outstanding. So, Amazon isn’t a controlling party in IonQ; it’s just an investor like you and me (although it has a lot more capital than you and me).

Just because Amazon doesn’t own 10% or so of the company doesn’t mean this isn’t an insignificant investment. Amazon clearly likes what it saw, and with Amazon having more technical prowess than the average investor, I think this makes IonQ an intriguing quantum computing investment.

One thing that sets IonQ apart from its competitors is the path it’s taking. While most quantum computing players are using superconducting technology, which requires cooling a particle to nearly absolute zero, IonQ uses a trapped-ion approach, which can be performed at room temperature. Furthermore, the trapped-ion technique is inherently more accurate than superconducting, which is a trade-off for slower processing speeds.

Because the biggest hurdle in quantum computing technology is accuracy, I think IonQ is one of the more compelling investment options right now, as it is the leader in this category, holding two world records.

This makes IonQ my top option in the quantum computing investment world. But is the stock worth buying right now?

An investment in IonQ will be volatile

IonQ has had an incredible run over the past few months as quantum computing investing has risen in popularity. The stock is up around 90% since the start of September, which is a massive movement considering that we’re still years away from viable quantum computing technology.

Most companies in this realm point toward 2030 as the turning point for quantum computing adoption, and IonQ is no different. Earlier this year, IonQ’s CEO Peter Chapman gave investors the projection that the company will be profitable with sales approaching $1 billion by 2030. That’s still five years away, which is a long time to wait and hold the stock to see if IonQ is an eventual winner in the quantum computing arms race.

With how much attention quantum computing has gotten in recent weeks, it’s impossible to tell where the stocks involved in this sector will head. It’s possible that there is a quantum computing investing mania ongoing, and the stocks continue to rise at an irrational pace.

It’s also possible that the stock could be ripe for a sell-off, especially after the past few weeks of strong gains. However, as long-term investors, we need to avoid that noise. If you’re buying IonQ stock now, you need to have the mindset of buying and holding through at least 2030, regardless of what the roller coaster ride of the stock market is like.

If you’re confident in IonQ, buying today makes sense, but your measure of success cannot be the stock price; it must be the company’s announcements. If IonQ wins the quantum computing arms race, the stock will be a winner over the long term, but keep in mind that it will be incredibly volatile along the way.

Contrary to a common assumption, not every investment forces you to make a major either/or trade-off. You can have (most of) the best of both worlds.

If you’re looking for a low-maintenance income-generating investment that you can buy and hold indefinitely, an exchange-traded fund (ETF) is an obvious choice. And you’ve certainly got plenty of options.

Not all dividend ETFs are the same, though. There are better options than others. In fact, if you’re looking for a great all-around dividend-paying exchange-traded fund to buy and hold forever, one stands out above them all.

And it’s probably not the one you think it is.

More to the matter than mere yield

If you’ve done any amount of digging into dividend ETFs as a category, then you likely already know that the Schwab U.S. Dividend Equity ETF(SCHD 0.79%) currently boasts a trailing yield of 3.9%. That’s huge for a fund of this size and ilk (quality blue chip stocks), even topping the 2.5% yield you can get from the Vanguard High Dividend Yield ETF(VYM 0.44%) at this time.

Image source: Getty Images.

There’s more to the matter than merely plugging into a fund when its yield hits a particular number, however. Is the current dividend sustainable? Does it have a history of growing its payouts enough to keep up with inflation? Is the ETF also producing enough capital appreciation? When you start asking these questions, the Schwab U.S. Dividend Equity fund doesn’t exactly shine. It has underperformed the S&P 500(^GSPC 0.53%) as well as most of the other major dividend funds since 2023, for instance, mostly because the Dow Jones U.S. Dividend 100 index that it mirrors doesn’t hold many — if any — of the tech stocks that have been lifted by the artificial intelligence megatrend.

That’s not inherently a bad thing, mind you. There may well come a time when these technology stocks struggle more than most while demand reignites for the components of the Dow Jones U.S. Dividend 100. Nevertheless, even factoring in its above-average dividend, the Schwab U.S. Dividend Equity ETF’s lingering subpar overall performance has made it tough to own for a while now. There’s also no obvious reason to think that relative weakness will soon end.

The best all-around choice

So which fund is the ideal all-around buy-and-hold “forever” dividend ETF? For many income-minded investors, it’s going to be the iShares Core Dividend Growth ETF(DGRO 0.53%).

It’s not a particularly popular fund. It has less than $35 billion in its asset pool, for perspective, versus more than $100 billion for the massive Vanguard Dividend Appreciation ETF(VIG 0.27%). Schwab’s U.S. Dividend Equity ETF is more sizable as well, with about $70 billion under management. You can also find yields better than DGRO’s current trailing yield of just under 2.2%.

Don’t let its smallish size and average yield fool you, though. The iShares Core Dividend Growth ETF packs enough punch where it counts the most. And it’s capable of packing this punch indefinitely.

This fund tracks the Morningstar US Dividend Growth Index. Like all of Morningstar‘s dividend growth indexes, this one only includes companies that have a track record of at least five straight years of annual payout hikes. It also excludes the highest-yielding 10% of stocks based on the premise that an unusually high yield can be a warning that trouble’s brewing for a business. In this vein, the index also excludes stocks of companies that pay out more than 75% of their earnings in the form of dividends.

Where the Morningstar US Dividend Growth Index really differentiates itself, however, is in the size of each position it holds. Although no holding is allowed to make up more than 3% of its total portfolio, its positions are weighted in proportion to the value of the stocks’ dividend payments. End result? This ETF’s biggest positions right now are Johnson & Johnson, Apple, JPMorgan Chase, Microsoft, and ExxonMobil. That’s an incredibly diverse group of stocks, although the fund’s other 392 holdings aren’t any less diverse.

Sure, many of these holdings don’t exactly boast massive dividend yields. Plenty of them do have impressive yields, though, and the ones that don’t are supplying value via price appreciation. It’s the balanced weighting of these different kinds of stocks that makes this ETF such a reliable overall performer.

The irony? Despite holding many low-yielding tickers of companies that don’t exactly prioritize their dividend payments, this fund’s quarterly per-share payment has nearly tripled over the course of the past decade. You’d be hard-pressed to find better from an ETF that also produces this kind of capital appreciation.

No compromise needed

None of this is to suggest that it would be a mistake to own any other income-focused exchange-traded fund. There are perfectly valid reasons for investing in something like the Schwab U.S. Dividend Equity ETF at this time, for instance, such as an immediate need for an above-average yield. It’s also not wrong to own more than one kind of dividend ETF, diversifying your investment income streams.

If you just want a super-simple dividend income option that you can buy and hold forever, though, the iShares Core Dividend Growth ETF is a fantastic but often overlooked choice. Unlike too many other investment options, with DGRO, you don’t have to sacrifice too much growth in exchange for reliable dividend income, or vice versa. It’s a balance of (nearly) the best of both worlds.

The only thing you can’t really get from the iShares Core Dividend Growth fund is a hefty starting dividend yield, but most long-term investors will consider that a fair trade-off.

JPMorgan Chase is an advertising partner of Motley Fool Money. James Brumley has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple, JPMorgan Chase, Microsoft, Vanguard Dividend Appreciation ETF, and Vanguard Whitehall Funds-Vanguard High Dividend Yield ETF. The Motley Fool recommends Johnson & Johnson and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Joel R Mogy Investment Counsel (JMIC) disclosed in an October 16, 2025, SEC filing that it sold 20,929 Adobe shares during Q3 2025.

This was an estimated $7.51 million trade based on the average price for Q3 2025.

What happened

Joel R Mogy Investment Counsel reported a reduction in its position in Adobe(ADBE 1.30%), selling 20,929 shares during Q3 2025.

The estimated value of the sale, based on the average closing price for Q3 2025, was approximately $7.51 million.

The position now stands at 50,664 shares as of Q3 2025, according to the firm’s SEC Form 13-F filed on October 16, 2025.

What else to know

The fund’s post-sale Adobe stake represents 0.98% of its $1.83 billion reportable U.S. equity AUM as of September 30, 2025, down from 1.60% in the previous period

JMIC’s top holdings after the filing:

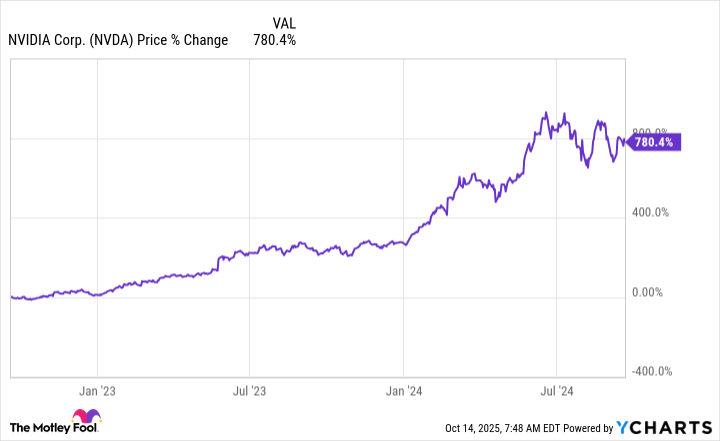

Nvidia: $257.28 million (14.1% of AUM) as of September 30, 2025

Alphabet: $158.37 million (8.68% of AUM) as of September 30, 2025

Apple: $155.49 million (8.52% of AUM) as of September 30, 2025

Microsoft: $148.56 million (8.14% of AUM) as of September 30, 2025

Costco Wholesale: $91.43 million (5.0% of AUM)

As of October 15, 2025, Adobe shares were priced at $330.63, marking a one-year decline of 34.9% and underperforming the S&P 500 by 49 percentage points.

Company Overview

Metric

Value

Revenue (TTM)

$23.18 billion

Net Income (TTM)

$6.96 billion

Price (as of market close 10/15/25)

$330.63

One-Year Price Change

-34.92%

Company Snapshot

Adobe offers software solutions, including Creative Cloud, Document Cloud, and a suite of digital experience and publishing tools; primary revenue is generated through recurring subscription services.

It operates a cloud-based, subscription-driven business model, selling directly to enterprises and end users as well as through a global partner network.

The company serves content creators, marketers, enterprises, and creative professionals across industries worldwide.

Adobe Inc. is a leading global software company specializing in creative, document, and digital experience solutions.

Foolish take

Joel R Mogy Investment Counsel (JMIC) had been steadily accumulating shares over the last few years, with the firm having a 2.5% portfolio allocation in Adobe just two years ago.

However, the company has sold shares of Adobe in the last two quarters — and heavily in its latest quarter.

With Adobe’s stock down 52% from its all-time high, it certainly seems as though JMIC is worried about the long-term future of the company.

Adobe has become an artificial intelligence (AI) battleground stock lately. The market seems torn as to whether the AI revolution will empower — or completely disrupt — the company’s creative operations.

For instance, OpenAI recently launched its Sora 2 model that lets users create short video clips from text. It doesn’t take a wild leap to imagine how this could directly hinder Adobe’s video editing and software businesses.

That said, Adobe has grown sales by 11% over the last year and is seeing the professional use cases for its video capabilities remain as robust as ever. Furthermore, the company has its Adobe Firefly unit, which is its own generative AI offering for creators — so it’s not exactly being blindsided by peers like OpenAI.

Trading at just 15 times free cash flow, Adobe could be a tremendous value investment at today’s price, but it looks like JMIC doesn’t want to risk waiting to find out if the company gets disrupted or not.

Glossary

AUM (Assets Under Management): The total market value of all investments managed by a fund or investment firm. Form 13-F: A quarterly SEC filing by institutional investment managers disclosing their equity holdings. Q3: The third quarter of a company’s fiscal year, typically covering July through September. Reportable U.S. equity assets: U.S. stocks and related securities that must be disclosed in regulatory filings. Top holdings: The largest individual investments in a fund’s portfolio, usually ranked by market value. Stake: The ownership interest or number of shares a fund or investor holds in a company. Subscription-driven business model: A model where customers pay recurring fees for ongoing access to products or services. Global partner network: A group of companies or organizations worldwide that help distribute or sell a firm’s products. TTM: The 12-month period ending with the most recent quarterly report.

Josh Kohn-Lindquist has positions in Adobe, Alphabet, Costco Wholesale, and Nvidia. The Motley Fool has positions in and recommends Adobe, Alphabet, Apple, Costco Wholesale, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Iconic ITV medical expert Dr Hilary Jones has opened up about how he is set to depart the network after working there for 36 years as a string of cuts will see workforce sliced in half

Dr Hilary Jones has opened up about the end of his ITV career(Image: Ken McKay/ITV/REX/Shutterstock)

Lorraine star Dr Hilary Jones has opened up about his departure from the hit ITV show after being on the air for 36 years. Hilary is leaving after it was announced that the morning offering is set to be cut to 30 minutes long from January.

The reduced schedule will see it air for just 30 weeks of the year instead of 52. The 72-year-old medical specialist has also confessed that he thinks there won’t be any money for him to have a leaving party.

He explained, “I’m still working there until December 31, and then I’m a free agent. It’s liberating from the constraints of a news programme presenter. I’ll probably come back as a guest presenter now and then.”

He then clarified further why the changes to the popular show are happening, as he mentioned that many people are having to move on. He said, “People are being very sensitive to the fact that some people are having to move on.

“A lot of people are being redeployed elsewhere or in the same role. ITV, like everyone else, are having to make changes.” Talking to The Sun, as he was asked if ITV would be throwing a leaving party for those being made redundant, he said: “It would be lovely if they did, but we will wait and see on that one because money is tight.

“Certainly, there are groups of us who feel we’re part of a family, so we will all be going out anyway, whether they pay or not. We are quite happy to dip into our own pockets.”

Attending the Best Hero awards, Hilary also clarified, “I think people at work know where they stand, and many saw changes coming.”

The changes will see the workforce on ITV Studios’ daytime operations cut in half as they try to claw back financial losses. Recent financial results for the network showed their profits are down by 30 per cent in the first half of this year.

Meanwhile, TV presenter Lorraine Kelly has described the cuts to her show as “heartbreaking” as she opened up for the first time about her show being slashed. The star also vowed to continue on her self-titled programme amid previous speculation she was prepared to walk away.

Speaking to The Mirror she said, “I don’t see me going anywhere until people get fed up, you know? Until people say, I’ve had enough of that one. It’s really heartbreaking to split up the team, a lot of my team have been with me for more than 20 years and they’re my friends.

“I’ve grown up with them. They were babies when they started with me and now they’ve got babies of their own.” Lorraine said she was pleased that a lot of the team had since been redeployed on other shows.

She added, “It’s been difficult with the cuts, it’s been hard. I’m a lot happier about it now but it was honestly and genuinely all about the team. I wasn’t annoyed or angry about this for me..it was about the team.”

On October 17, 2025, hedge fund TB Alternative Assets Ltd. disclosed a new position in Strategy(MSTR 2.12%), formerly known as MicroStrategy, acquiring 126,000 shares for an estimated $40.6 million.

IMAGE SOURCE: GETTY IMAGES.

What happened

According to a filing with the Securities and Exchange Commission dated October 17, 2025, TB Alternative Assets Ltd. disclosed a new position in Strategy during the third quarter ended September 30, 2025. The fund reported owning 126,000 shares worth $40.6 million. The purchase corresponds to an estimated $40.6 million transaction value, calculated using average prices for the reporting period ended September 30, 2025.

What else to know

This new position represents 6.1% of TB Alternative Assets Ltd.’s reportable U.S. equity AUM as of September 30, 2025.

TB Alternative Assets’ top holdings after the filing are:

META: $76.97 million (11.5% of AUM) as of September 30, 2025

GOOG: $58.56 million (8.8% of AUM) as of September 30, 2025

INTC: $51.26 million (7.7% of AUM) as of September 30, 2025

PDD: $45.72 million (6.8% of AUM) as of September 30, 2025

MSTR: $40.60 million (6.1% of AUM) as of September 30, 2025

As of October 16, 2025, shares were priced at $283.84, up 34.3% over the past year and outperforming the S&P 500 by 32.8 percentage points during the same period.

Company Overview

Metric

Value

Revenue (TTM)

$462.32 million

Net Income (TTM)

$4.73 billion

Price (as of market close October 16, 2025)

$283.84

One-Year Price Change

34.3%

Company Snapshot

Strategy provides enterprise analytics solutions, enabling organizations to derive insights from data at scale. The company leverages its robust software platform and specialized services to address complex business intelligence needs for large enterprises.

Strategy offers enterprise analytics software, including a software platform with features such as hyperintelligence, data visualization, reporting, and mobile analytics.

The company generates revenue primarily through software licensing, support services, consulting, and education offerings for enterprise clients. It serves a diversified customer base across industries such as retail, finance, technology, healthcare, and the public sector.

Foolish take

Hedge fund TB Alternative Assets’ investment in Strategy shares is noteworthy for a few reasons. The buy represents an initial position in the stock. Moreover, the hedge fund went big with the purchase, putting Strategy shares into its top five holdings. Lastly, those top holdings are dominated by tech stocks, and although Strategy began as a data analytics software platform, it’s now more of a cryptocurrency play.

Strategy became the first publicly-traded company to buy Bitcoin as part of its capital allocation strategy back in 2020. Since then, it has transformed into “the world’s first and largest Bitcoin Treasury Company,” according to Strategy.

As of July 29, the company holds 3% of all Bitcoin in existence. This brought its Q2 total assets to $64.8 billion with $64.4 billion of that in digital assets. As a result, Strategy’s fortunes rise and fall with the value of the cryptocurrency rather than its software products.

So far, the gamble has paid off. As Bitcoin’s value has risen, so has Strategy’s stock. And now, the company is leveraging its cryptocurrency holdings to offer various Bitcoin-related investment vehicles.

TB Alternative Assets may have found this new direction for the former MicroStrategy a compelling case for investing in the stock. If you’re seeking exposure to Bitcoin, Strategy offers a unique take, and with the stock down from its 52-week high of $543 reached last November, now may be a good time to buy.

Glossary

13F AUM: The total market value of U.S. equity securities reported by an institutional investment manager in quarterly SEC filings. Position: The amount of a particular security or asset held by an investor or fund. Stake: The ownership interest or share held in a company by an investor or fund. Holding: A security or asset owned by an investor or fund, often listed in portfolio disclosures. Outperforming: Achieving a higher return compared to a specific benchmark or index over a given period. Enterprise analytics: Software and tools that help organizations analyze large-scale data to support business decision-making. Business intelligence: Technologies and strategies used to analyze business data and support better decision-making. Software licensing: The practice of granting customers the right to use software under specific terms and conditions. Support services: Assistance provided to customers for software maintenance, troubleshooting, and technical issues. Consulting: Professional advisory services that help organizations implement and optimize software or business processes. TTM: The 12-month period ending with the most recent quarterly report. Reportable U.S. equity AUM: The portion of assets under management invested in U.S. stocks that must be disclosed in regulatory filings.

Robert Izquierdo has positions in Alphabet, Intel, and Meta Platforms. The Motley Fool has positions in and recommends Alphabet, Bitcoin, Intel, and Meta Platforms. The Motley Fool recommends the following options: short November 2025 $21 puts on Intel. The Motley Fool has a disclosure policy.

Investment advisor Paradiem, LLC disclosed a new purchase of Owens Corning(OC 0.58%), adding 85,047 shares in Q3 2025, an estimated $12.48 million trade based on the average price for the quarter ended Sept. 30, 2025.

IMAGE SOURCE: GETTY IMAGES.

What happened

According to a filing with the Securities and Exchange Commission dated October 17, 2025, Paradiem, LLC increased its stake in Owens Corning substantially during the third quarter. The fund acquired 85,047 additional shares, bringing its total position to 94,067 shares, with a quarter-end reported value of $13.31 million.

What else to know

Paradiem, LLC’s addition brings Owens Corning to 3.1% of 13F reportable assets as of Q3 2025.

Paradiem’s top holdings after the filing as of September 30, 2025 are:

NASDAQ:LRCX: $27.44 million (6.4% of AUM)

NYSE:TEL: $19.53 million (4.55% of AUM)

NYSE:VLO: $17.87 million (4.2% of AUM)

NYSE:LMT: $16.13 million (3.76% of AUM)

NYSE:CAT: $15.79 million (3.7% of AUM)

As of October 17, 2025, shares of Owens Corning were priced at $126.96, with a one-year change of -33.04%, underperforming the S&P 500 by 45.03 percentage points.

Company Overview

Metric

Value

Revenue (TTM)

$11.74 billion

Net Income (TTM)

$333.00 million

Dividend Yield

2.17%

Price (as of market close 2025-10-17)

$126.96

Company Snapshot

Owens Corning is a leading global manufacturer specializing in insulation, roofing, and fiberglass composite products, with a diversified revenue base across construction and industrial end markets. The company leverages its scale and integrated operations to deliver essential building materials to a broad customer base.

Owens Corning manufactures and markets insulation, roofing, and fiberglass composite materials across three segments: composites, insulation, and roofing. It generates revenue through direct sales and distribution of building materials, glass reinforcements, insulation products, and roofing components to construction and industrial markets worldwide.

The company serves insulation installers, home centers, distributors, contractors, and manufacturers in residential, commercial, and industrial sectors.

Foolish take

Financial services company Paradiem upped its stake in Owens Corning in a big way. The stock went from 0.3% of the fund’s holdings to 3.1% in Q3. This action demonstrates a belief in Owens Corning despite shares being down significantly from the 52-week high of $214.53 reached last November.

Owens Corning stock is down this year due to macroeconomic conditions, such as higher interest rates and persistent inflation, which caused a slowdown in the construction sector. The company also underwent changes, such as divesting businesses in China and South Korea, to sharpen its focus, particularly on the North American and European markets.

Despite these factors, Owens Corning delivered 10% year-over-year sales growth in the second quarter to $2.75 billion. And its moves to divest less profitable businesses resulted in Q2 diluted earnings per share increasing 34% year over year to $3.91 for its continuing operations.

With the company’s stock down but its financials looking solid, Paradiem may have taken the opportunity to scoop up shares. After all, the Federal Reserve is widely expected to cut interest rates soon, which can help to stimulate the construction industry. These factors make Owens Corning a compelling investment, especially while its stock is down.

Glossary

13F reportable assets: Assets that institutional investment managers must disclose quarterly to the SEC, showing certain equity holdings. AUM (Assets Under Management): The total market value of investments that a fund or manager oversees on behalf of clients. Stake: The ownership interest or number of shares held in a particular company by an investor or fund. Quarter-end: The last day of a fiscal quarter, used as a reference point for financial reporting. Dividend Yield: Annual dividends paid by a company divided by its share price, expressed as a percentage. TTM: The 12-month period ending with the most recent quarterly report. Filing: An official document submitted to a regulatory authority, often containing financial or ownership information. Segments: Distinct business divisions within a company, often based on product lines or markets served. Distribution: The process of delivering products from manufacturers to end customers or intermediaries. End markets: The industries or customer groups that ultimately use a company’s products or services.

Robert Izquierdo has positions in Caterpillar. The Motley Fool has positions in and recommends Lam Research. The Motley Fool recommends Lockheed Martin and Owens Corning. The Motley Fool has a disclosure policy.

Would the Dodgers have paid $4 million for Shohei Ohtani’s production on Friday night?

“Maybe I would have,” team owner Mark Walter said with a laugh.

Four million dollars is how much Ohtani has received from the Dodgers.

Not for the game. Not for the week. Not for the year.

For this year and last year.

Ohtani could be the greatest player in baseball history. Is he also the greatest free-agent acquisition of all-time?

“You bet,” Walter said.

Even before Ohtani blasted three homers and struck out 10 batters over six scoreless innings in a historic performance to secure his team’s place in the World Series, the Dodgers were a target of complaints over the perception they were buying championships. Their payroll this season is more than $416 million, according to Spotrac.

During the on-field celebration that followed the 5-1 victory over the Milwaukee Brewers in Game 4 of the National League Championship Series, manager Dave Roberts told the Dodger Stadium crowd, “I’ll tell you, before this season started, they said the Dodgers are ruining baseball. Let’s get four more wins and really ruin baseball!”

What detractors ignore is how the Dodgers aren’t the only team that spent big dollars this year to chase a title. As Ohtani’s contract demonstrates, it’s how they spend that separates them from the sport’s other wealthy franchises.

The New York Mets spent more than $340 million, the New York Yankees $319 million and the Philadelphia Phillies $308 million. None of them are still playing.

The Dodgers are still playing, and one of the reasons is because of how opportunistic they are.

When the Boston Red Sox were looking for a place to dump Mookie Betts before he became a free agent, the Dodgers traded for him and signed him to an extension. When the Atlanta Braves refused to extend a six-year offer to Freddie Freeman, the Dodgers stepped in and did.

Something else that helps: Players want to play for them.

Consider the case of the San Francisco Giants, who can’t talk star players into taking their money.

The Giants pursued Bryce Harper, who turned them down. They pursued Aaron Judge, who turned them down. They pursued Ohtani, who turned them down. They pursued Yoshinobu Yamamoto, who turned them down.

Notice a pattern?

Unable to recruit an impact hitter in free agency, the Giants turned their attention to the trade market and acquired a distressed asset in malcontent Rafael Devers. They still missed the postseason.

The Dodgers don’t have any such problems attracting talent. Classified as an international amateur because he was under the age of 25, Roki Sasaki was eligible to sign only a minor-league contract this winter. While the signing bonuses that could be offered varied from team to team, the differences were relatively small. Sasaki was urged by his agent to minimize financial considerations when picking a team.

Sasaki chose the Dodgers.

Players such as Blake Snell, Will Smith and Max Muncy signed what could be below-market deals to come to or stay with the Dodgers.

There is also the Ohtani factor.

Ohtani didn’t want the team that signed him to be financially hamstrung, which is why he insisted that it defer the majority of his 10-year, $700-million contract. The Dodgers are paying Ohtani just $2 million annually, with the remainder owed after he retires.

Without Ohtani agreeing to delayed payments, who knows if the Dodgers would have signed the other pitchers who comprise their dominant rotation, Yamamoto, Snell and Tyler Glasnow.

None of this is to say the Dodgers haven’t made any mistakes, the $102 million they committed to Trevor Bauer a decision they would certainly like to take back.

But the point is they spend.

“We put money into the team, as you know,” Walter said. “We’re trying to win.”

Nothing is stopping any other team from making the financial commitments necessary to compete with the Dodgers. Franchises don’t have to make annual profits to be lucrative, as their values have skyrocketed. Teams that were purchased for hundreds of millions of dollars are now worth billions.

Example: Arte Moreno bought the Angels in 2003 for $183.5 million. Forbes values them today at $2.75 billion. If or when Moreno sells the team, he will receive a huge return on his investment.

The calls for a salary cap are nothing more than justifications by cheap owners for their refusal to invest in the civic institutions under their control.

The Dodgers aren’t ruining baseball. They might not do everything right, but as far as their spending is concerned, they’re doing right by their fans.

There’s no guesswork to it — the underlying math is actually quite cut and dried.

Social Security was never meant to make up the entirety of anyone’s retirement income. The fact is, however, some people are collecting surprisingly big checks. This year’s maximum-possible monthly payment is $5,108, or $61,296 per year. That’s almost as much as the median salary U.S. workers are currently taking home, according to data from the Bureau of Labor Statistics.

How did they do it, and what will it take for you to do it as well? Here’s how to get the very most you can out of the government-managed entitlement program.

Image source: Getty Images.

1. A minimum of 35 years’ worth of work-based taxable income

There are three components to your future Social Security benefits. One of them the sheer number of years you earned taxable income as an employee. You’ll need to work for at least 35 years to maximize your payments.

See, when calculating your monthly benefit, the Social Security Administration looks at your inflation-adjusted income in your 35 highest-earning years. You don’t have to work a full 35 years to claim benefits, to be clear. It’s just that for any year less than 35 that you don’t earn any reported income, the program fills in those blanks with a value of $0, dragging down your annual average.

Conversely, working more than 35 years won’t necessarily help, since you only get credit for your best 35. There may still be an upside to working more than 35 years though. If you didn’t earn a great deal of money in some of them but are making good money now, you’ll be replacing some of those lower-earning years with higher-earning ones, raising your overall average of your top 35.

2. Strong earnings for at least 35 of those years

It’s not just a matter of making good money for a minimum of 35 years though. You must earn well above average earnings for that length of time, reaching or eclipsing Social Security’s taxable income threshold in each of those.

And these thresholds are pretty high. This year, for instance, the program doesn’t stop increasing your FICA tax liability until you reach earnings of $176,100. Here’s the minimum amount of taxable wages you would have needed to earn each and every year going all the way back to 1986 to max out your future benefits payments.

Year

Taxable Income

Year

Taxable Income

1986

$42,000

2006

$94,200

1987

$43,800

2007

$97,500

1988

$45,000

2008

$102,000

1989

$48,000

2009

$106,800

1990

$51,300

2010

$106,800

1991

$53,400

2011

$106,800

1992

$55,500

2012

$110,100

1993

$57,600

2013

$113,700

1994

$60,600

2014

$117,000

1995

$61,200

2015

$118,500

1996

$62,700

2016

$118,500

1997

$65,400

2017

$127,200

1998

$68,400

2018

$128,400

1999

$72,600

2019

$132,900

2000

$76,200

2020

$137,700

2001

$80,400

2021

$142,000

2002

$84,900

2022

$147,000

2003

$87,000

2023

$160.200

2004

$87,900

2024

$168,600

2005

$90,000

2025

$176,100

To be clear, although you pay into Social Security’s pool of funds via taxes on wages up to these amounts, you don’t pay additional FICA taxes above and beyond these amounts (although you do pay ever-rising income tax the more money you make, since tax rates rise the more you earn). The program stops taxing you beyond these levels because it wouldn’t offer you any additional benefit in return. Again, the absolute ceiling is $5,108 per month.

3. Waiting until you turn 70 to claim benefits

Finally, although you can initiate your Social Security retirement benefits as soon as you turn 62, doing so would dramatically reduce the size of your check by as much as 30% of your intended benefit at their full retirement age, depending on when you were born. Even claiming benefits at your official full retirement age, however, still wouldn’t get you to the maximum-possible benefit. To secure the maximum amount of $5,108, you must until you reach the age of 70 to begin your Social Security payments. That will improve the size of most people’s payments by 24% (if not more) above their payment if claiming at their full retirement age.

Just know that there’s no point in waiting any longer than this to file, since Social Security stops adding credit for delaying your benefits beyond the age of 70. In fact, there’s good reason to claim pretty soon after you reach this point. The Social Security Administration will back pay you some of what it owes you if you don’t file right away. But it will only give you a maximum of six months’ worth of back pay, no matter how long after you turn 70 you claim your retirement benefits.

Prioritize what you can control

You know there’s no way you’re going to qualify for this amount? That’s OK. Most people don’t. Fewer than 20% of recipients see monthly checks of more than $3,000, in fact.

Don’t let that discourage you though. Even modest wage-earners can put themselves in a far better financial situation with their own savings than they’d ever be able to achieve with Social Security. Most calculations of Social Security contributions’ effective rate of return only put the figure in the mid-single-digits, versus the stock market’s average annual gain of around 10%.

Besides, Social Security was never meant to be anyone’s sole source of retirement income anyway. Do what you reasonably can to max it out, but mostly stay focused on maximizing the growth of your own personal retirement nest egg.

The company reports its latest earnings numbers next month, and investor expectations are likely low.

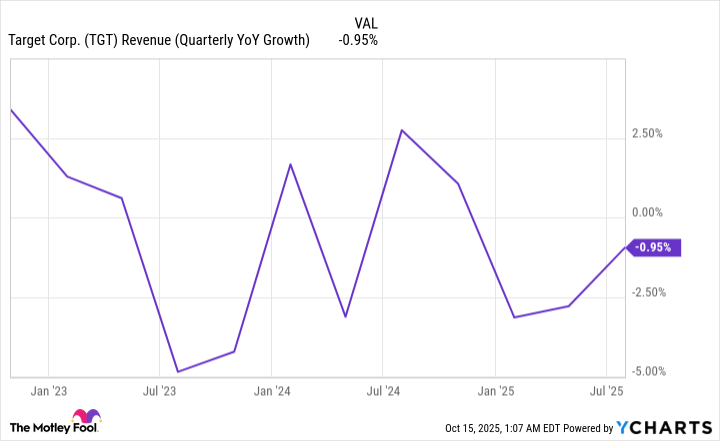

There hasn’t been much of a reason for investors to be excited about Target (TGT 0.80%) stock this year. The company’s financials have been underwhelming, and with the business heavily dependent on discretionary spending for its growth, there hasn’t been much hope that things will get better anytime soon, given the state of the economy.

This year, the stock is down more than 30% as it has continued to hit new lows on the way down. But it offers a high-yielding dividend of 5.2% and with an incredibly low valuation, it could make for an intriguing contrarian play. With earnings coming up on Nov. 19, should you consider taking a chance on the retail stock before it posts its latest numbers?

Image source: Getty Images.

Will the upcoming quarter be more of the same for Target?

To say things haven’t been going well for Target in recent years is an understatement. Sales have been sluggish and the company has been struggling to generate any kind of growth whatsoever. Consumers have been tightening up their budgets and spending less on discretionary purchases as concerns about tariffs and the economy as a whole have been affecting many retailers.

In the company’s most recent quarter, which ended on Aug. 2, its net sales were down by a little less than 1%, totaling $25.2 billion. And what was even more problematic is that with expenses rising, Target’s net earnings fell by a whopping 22%, to $935 million.

The worry is that retailers haven’t felt the full impact of tariffs just yet, which could mean more bad news for Target’s business in the future. But in a way, that bearish outlook could work to the stock’s advantage.

Expectations appear low for Target

Target’s stock has been in a prolonged tailspin this year. And if the company doesn’t give investors much reason for optimism in its upcoming earnings report, it could be on track for an even worse year than in 2022, when the stock market crashed and its shares plummeted by 36%.

The retail stock trades at a lowly 10 times its trailing earnings, and even when factoring in analyst expectations, its forward price-to-earnings multiple is not much higher at 11. There’s plenty of bearishness priced into the stock, which could make it easier for Target not to disappoint investors; any bit of positive news could give this beaten-down stock some much-needed life.

The bar is definitely low given the discount Target trades at, and it hasn’t been this cheap in years.

I wouldn’t buy Target’s stock just yet

Target is a good long-term buy and I believe it can recover. But it’s also undergoing a change in CEO, macroeconomic conditions are far from ideal for its business, and there’s been a flurry of negativity around the stock this year. Given all those factors, I don’t see a reprieve coming just yet, as the economy is still on shaky ground and there’s little reason to expect a turnaround at this stage.

If you’re a long-term investor, you may want to consider taking a position in the stock, but only if you’re prepared for a turbulent ride and are willing to wait for at least a couple of years for economic conditions to improve.

The safer option is to wait and see what the company’s strategy looks like under its new CEO, Michael Fiddelke, who takes over in February and to reevaluate the stock at that point. With so much uncertainty around the business, there simply isn’t an overwhelming reason to buy shares of Target today. It could be a while before the business can turn things around, and in the meantime, there are better growth stocks to invest in.

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Target. The Motley Fool has a disclosure policy.

These tech companies are benefiting from growing investment in AI chips and software.

Artificial intelligence (AI) represents a major opportunity for businesses across industries to develop products faster and cheaper than ever before. The race to gain a data-driven edge on the competition is fueling massive investment across the entire tech supply chain from data centers to software.

Many of the key players enabling this new industrial revolution are already valued at over $1 trillion market caps. But as governments and businesses continue to invest in this technology, there are two AI enablers that are still valued under $500 billion that could be worth buying today. Here’s why growing competition in AI could propel these companies into the trillion-dollar club.

1. Palantir Technologies

Palantir(PLTR 0.11%) started as a government contractor, providing AI-powered software for intelligence and counterterrorism efforts. But now its software is experiencing insatiable demand in the private sector. Companies are seeing significant cost savings, which means Palantir can benefit from companies scrambling to adopt AI solutions to remain competitive.

If one company in an industry uses Palantir to gain operating efficiencies, it creates a competitive advantage. This pushes more businesses to consider investing in Palantir’s platforms or risk falling behind. This can explain in part why Palantir’s U.S. commercial revenue has exploded this year, nearly doubling year over year in the second quarter.

Palantir closed its highest quarter yet of total contract-value bookings of $2.3 billion, representing a year-over-year increase of 140%. It is signing bigger deals while also seeing existing customers continue to spend more, leading to a healthy 128% net-dollar retention rate.

Palantir is effectively a tool that improves a company’s profits. Its software is expensive relative to alternative software vendors, but Palantir still expects accelerating growth next quarter. This signals it has a competitive edge. Palantir’s ontology-based system creates a digital twin of a company’s operations, helping managers make sense of unorganized data for better decision making.

Importantly, Palantir is converting revenue into very high margins that are driving robust growth in earnings and free cash flow. This is one reason why the stock has performed so well and may continue to outperform Wall Street’s expectations.

For what it’s worth, widely followed tech analyst Dan Ives at Wedbush Securities sees Palantir stock hitting a market cap of $1 trillion in the next three years. Keep in mind, the stock trades at an expensive valuation, so market sentiment will play a role in how the stock performs in the near term. Given the potential for volatility in the share price, investors should plan on holding it for at least 10 years. Long term, the savings and efficiencies Palantir brings to other companies could make it one of the most valuable companies in the world.

Image source: Advanced Micro Devices.

2. Advanced Micro Devices

The companies providing the chips for AI continue to benefit from increasing competition among the leading model builders. OpenAI just announced a deal to deploy six gigawatts of chips, which amounts to hundreds of thousands, from Advanced Micro Devices(AMD -0.52%) over the next several years.

OpenAI’s ChatGPT is the most popular AI model with over 700 million weekly active users. But to meet growing demand, it has to expand its compute capacity to compete with rivals, including xAI’s Grok and Google Gemini, which also continue to invest in more infrastructure. This growing competition will benefit AMD.

OpenAI’s deal with AMD validates the capabilities of its upcoming pipeline of graphics processing units (GPUs). AMD’s data center business has not been growing as fast as Nvidia‘s, but it is expected to accelerate over the next year, and the deal with OpenAI is a catalyst.

While Nvidia’s GPUs have been widely used by data centers for powering large AI training loads, AMD’s chips have an advantage in handling small-to-medium-sized AI tasks. This is by design. AMD’s Instinct family of GPUs feature a high amount of memory bandwidth that makes them well suited for the AI inference market, which CEO Lisa Su believes is going to be much bigger than AI training.

OpenAI will deploy the first gigawatt of AMD Instinct MI450 GPUs in the second half of 2026. Analysts currently expect AMD’s revenue to grow 28% in 2025 before increasing by 26% in 2026, according to Yahoo! Finance. Earnings should grow even faster due to the high margins of data center GPUs.

The stock currently has a market cap of $350 billion. Assuming the stock continues to trade around the same price-to-earnings (P/E) multiple, AMD has a good chance to reach a $1 trillion market cap by 2030. Wall Street analysts expect earnings to grow at an annualized rate of 34%, which is enough to generate outstanding returns for investors.

John Ballard has positions in Advanced Micro Devices, Nvidia, and Palantir Technologies. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Nvidia, and Palantir Technologies. The Motley Fool has a disclosure policy.

Credit card debt can bury you in interest. However, there are tools to help you take control.

U.S. credit card balances have surged in the past several years, from $787 billion in Q2 2021 to $1.2 trillion in Q2 2025. Though the pace of increases has slowed in 2025, average credit card interest rates still hover around 25%, leading to balances that swell faster than many can pay them down.

Image source: Getty Images.

Debt can happen at any age

There’s never a good time to get caught up in high-interest debt, but the situation is particularly critical when that debt prevents you from investing for retirement. Regardless of your current age, the last thing you want to do is give up aspects of your retirement because you can’t afford them.

Due to soaring inflation, retirees outspend their annual incomes by more than $4,000, according to data from the Bureau of Labor Statistics. With limited options to bridge that financial gap, more are turning to credit cards to cover everyday expenses. In fact, 41% of households headed by someone between the ages of 65 and 74 carry credit card debt. Few of these households likely expected to depend on credit cards as they planned for retirement.

But it’s not just those who’ve reached retirement age who depend on credit cards. Experian offers this overview of average credit card debt by age:

Age

Average credit card balance

Generation Z

(born 1997-2012)

$3,493

Millennials

(born 1980-1996)

$6,961

Generation X

(born 1965-1979)

$9,600

Baby Boomer

(born 1946-1964)

$6,795

Silent Generation

(born 1928-1945)

$3,445

What credit card debt means to retirement

Let’s say you’re 55, part of Generation X, and owe $9,600 in credit card debt. If your cards carry an average annual percentage rate (APR) of 25% and you make monthly credit card payments totaling $300, it will take you 54 months to pay the cards off. Worse, you’ll spend $6,384 on interest.

Now, imagine that your credit card debt didn’t exist, and you invested that $6,384 instead. Assuming an average annual return of 7%, it would be worth $12,558 in 10 years, $17,614 in 15 years, and $24,704 in 20 years. That’s assuming you never contribute another penny to the investment. It may not be a fortune, but any money invested can be combined with Social Security and other sources of income to help you in retirement.

Whether you’re an experienced or beginner investor, freeing up the money currently spent on monthly credit card payments is one of the surest ways to bolster your retirement savings.

The trick is to get your credit card debt under control. Here are three ideas to get you started.

1. Look into a consolidation loan

Consider a personal loan with a lower interest rate than you’re paying on your credit cards (ideally, much lower). Use that loan to pay off your credit cards and then make regular monthly payments until the loan is paid off in full.

Again, let’s say you owe $9,600 in credit card debt. The personal loan you land has an APR of 11%. By making the same monthly payment of $300, the loan will be paid off in 39 months rather than the 54 months it would have taken to pay down the credit cards. Better yet, you’ll spend $1,815 in interest, saving you $4,569.

2. Take advantage of a pay-down option

Snowball and avalanche methods are two of the most popular ways to pay off existing debt. Here’s how they work:

Snowball method: Prioritize paying off your smallest debt first while continuing to make minimum payments on your other debts. Once the smallest debt is paid off, move to the next smallest balance, adding the money you were putting toward the first debt to pay down the second debt at a faster clip. Once the second smallest debt is paid off, move on to the third smallest, and so on. With each debt you pay off, you have more money available to pay toward the next one, creating a snowball effect.

Avalanche method: Prioritize paying off the debt with the highest interest rate (regardless of balance). Once the debt with the highest rate is paid off, move to the debt with the next highest interest rate, and so on. Like the snowball method, each debt you pay off gives you more money for the next debt.

3. Consider a debt management plan

Debt management plans (DMPs) consolidate your credit card debt into a single monthly payment. Typically offered through certified credit counseling agencies, DMP counselors work on your behalf to:

Help you determine how much you can afford to pay each month.

Negotiate with your creditors to adjust your repayment terms.

Accept your monthly payment and distribute it to your creditors.

While DMPs may be an effective way to climb out of debt, they can initially hurt your credit score, so be sure you understand the pros and cons before entering a DMP agreement.

Credit card debt is not insurmountable, but it does take effort to conquer. The sooner you do that, the sooner you can make progress toward your ideal retirement. Whether that’s fishing every day, visiting your grandkids, or retiring to a beach in a foreign country, it’s your dream to build.

This broad-market index gives investors a taste of everything — even more than the S&P 500.

Even Warren Buffett, the greatest stock picker of all time, endorses low-cost, broad-market index funds and exchange-traded funds for most retail investors. This is because most investors don’t have the time to deeply research individual stocks, while broader-market indexes tend to win over time, with 8% to 10% long-term returns on average.

While large banks were the first to create index funds for their institutional clients, Vanguard was the first to offer diversified index funds to the public in 1976. Today, Vanguard is one of just a few major asset managers offering accessible, extremely low-cost index funds, costing investors just a handful of basis points in fees.

After the market’s strong recovery from April’s “Liberation Day” tariff fiasco, here’s the Vanguard fund I’d recommend today.

Buy the total market

Today, technology stocks, particularly around the AI buildout, have soared to very high valuations. Interestingly, some of the largest stocks in the world that have gone up the most, defying the law of large numbers, leaving large indexes like the Nasdaq-100 or even S&P 500(^GSPC 0.53%) the most concentrated they’ve ever been in recent history.

Of course, there is a good reason why growth-oriented, large-cap technology stocks have soared over the past six months and even the last few years: artificial intelligence. The prospect of generative AI could very well lead to the next industrial revolution; meanwhile, only the largest, best-funded, most technically advanced companies likely have a chance to compete. Therefore, it’s no surprise the “Magnificent Seven” stocks only seem to be getting stronger.

That being said, valuation matters, and the widening gulf between the largest tech stocks and smaller stocks in other sectors is huge. Furthermore, once AI technology is honed and widely distributed, every business in every sector of the economy should be able to benefit from GenAI.

So while investors shouldn’t abandon AI tech stocks en masse, now would also be a good time to look at other types of stock in left-behind sectors. That makes this Vanguard ETF an excellent choice today.

Image source: Getty Images.

Vanguard Total Stock Market Index Fund

The Vanguard Total Stock Market Index Fund(VTI 0.51%) is my recommendation for index investors looking to put money to work today. As the name implies, this index tracks the entire stock market, including large-, mid-, small-, and even micro-cap stocks — the entire investing universe in the U.S.

Of course, a broad-market index will also have high weightings of the large-cap tech stocks discussed. Yet while investing in the total market index fund will still give investors some exposure to the AI revolution, those stocks will have a smaller weight than other index funds, such as the Vanguard S&P 500 ETF(VOO 0.60%). For instance, in the VTI, the largest stock in the market, Nvidia, has a 6.5% weighting, whereas Nvidia sports a 7.8% weighting in the VOO, which tracks the S&P 500, and a 9.9% weighting in the Invesco QQQ Trust(QQQ 0.73%), which tracks the Nasdaq-100.

Meanwhile, the total market fund will give a larger weight to smaller stocks in other cheaper sectors of the economy, which may outperform if there is a rebalancing and reversion to the mean. This is what happened in the early 2000s, when technology stocks crashed over the course of three years, but cheaper value stocks in other sectors of the market went on to outperform.

Currently, the VTI trades at a weighted average 27.2 times earnings, with a 1.14% dividend yield. It has risen 13.9% year to date, which is a strong performance, albeit behind that of the VOO and QQQ. Its expense ratio is 0.03%, which is so minuscule the fund is practically free.

Torn between momentum and value? Buy everything

The VTI is therefore a nice middle ground between those who are enthusiastic about the general prospects for AI technology, but are squeamish about tech stocks’ sky-high valuations relative to lower-priced sectors today. Therefore, it’s a great choice for investors looking to allocate money to stocks in October as part of their investment plan.

Billy Duberstein and/or his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia, Vanguard S&P 500 ETF, and Vanguard Total Stock Market ETF. The Motley Fool has a disclosure policy.

Nvidia stock has skyrocketed over the past few years amid excitement about the company’s AI dominance.