Article content

TORONTO — dynaCERT Inc. (TSX: DYA) (OTCQB: DYFSF) (FRA: DMJ) (“dynaCERT” or the “Company”) is pleased to announce the appointment of John Amodeo effective immediately.

Though cloud giant Oracle came within a stone’s throw of reaching the psychologically important $1 trillion valuation mark, another company is better suited to beat it to the punch.

On Wall Street, market cap serves as a differentiator of good and great businesses. While there are plenty of budding small- and mid-cap companies, businesses with valuations in excess of $10 billion have (more often than not) demonstrated their innovative capacity and backed up their worth to Wall Street.

But among this class of proven businesses is a truly elite group of 11 public companies that have reached the psychologically important trillion-dollar valuation plateau, not accounting for the effects of inflation over time (looking at you, Dutch East India Company). These 11 indelible titans include all seven members of the “Magnificent Seven,” Broadcom, Berkshire Hathaway, Taiwan Semiconductor Manufacturing, and Saudi Aramco, the latter of which doesn’t trade on U.S. exchanges.

Image source: Getty Images.

Last week, integrated cloud applications and cloud infrastructure services provider Oracle (ORCL 3.33%) came within a stone’s throw of becoming the 12th public company to reach at least a $1 trillion valuation before retreating. While the rise of artificial intelligence (AI) makes it a logical candidate to eventually surpass a market cap of $1 trillion, there’s another industry leader that’s ideally positioned to become Wall Street’s next trillion-dollar stock.

Following the closing bell on Sept. 9, Larry Ellison’s company delivered nothing short of a jaw-dropper with its fiscal 2026 first-quarter operating results.

It’s exceptionally rare when a megacap company moves by a double-digit percentage in a single trading session. At one point on Sept. 10, Oracle stock was higher by more than 40% and peaked at a market cap of $982 billion. Though it’s given back $150 billion in market value since its Sept. 10 peak, it closed out the week with a 25% gain, which isn’t shabby at all.

The hoopla surrounding Oracle has to do with its updated remaining performance obligations (RPO) forecast — RPO is essentially a backlog of future revenue based on contracts signed — and projected growth ramp for its high-margin Oracle Cloud Infrastructure (OCI) segment. OCI offers on-demand cloud-computing services, which can run AI workloads on private, public, and hybrid clouds, and also leases out AI compute.

On a year-over-year basis for the quarter ended Aug. 31, Oracle announced its RPO jumped 359% to $455 billion on the heels of signing four multibillion contracts during the fiscal first quarter. During the company’s conference call, CEO Safra Catz singled out privately held OpenAI and xAI, as well as Magnificent Seven members Meta Platforms and Nvidia, as some of these significant cloud contracts.

What’s perhaps even more impressive than the growth of Oracle’s backlog is its projected ramp in sales from OCI. Catz laid out a stunning growth forecast that calls for:

Catz and Oracle co-founder/Chief Technology Officer Larry Ellison have outlined a clear path to outsized growth that the company has lacked since the dot-com days. However, a wait-and-see approach from investors may be preferred in the quarters to come given that Oracle has missed Wall Street’s earnings per share consensus in three of the last four quarters. This could stall its efforts to quickly join the elite trillion-dollar club.

Image source: Getty Images.

Considering how Wall Street lives and breathes anything having to do with AI, you might be thinking a tech company is the next logical candidate to reach the trillion-dollar plateau. But what if I told you that time-tested retailer Walmart (WMT 0.14%), which closed out last week with a market cap of $825 billion, has an inside path to a $1 trillion valuation?

On the surface, things might not seem perfect for the retail industry. Recent job market revisions point to a potentially weakening U.S. economy.

At the same time, the effects of President Donald Trump’s tariff policies have begun to show up in monthly inflation reports. Between May and August, the trailing-12-month inflation rate, based on the Consumer Price Index for All Urban Consumers (CPI-U), rose by 67 basis points to 2.92%. When coupled with a weakening job market, rising inflation ignites fears of stagflation, which is a worse-case scenario for the Federal Reserve.

These scenarios are typically bad news for most retailers — but Walmart isn’t “most retailers.”

For decades, Walmart’s success has derived from its focus on value and convenience. When times are tough or uncertain in America, people turn to Walmart for a good deal on groceries, toiletries, and countless other items. If Trump’s tariffs are eventually ruled legal by the Supreme Court and remain in place, their inflationary impact is only going to drive more consumers, including affluent shoppers, into Walmart stores. Even if the company eats a portion of these tariffs, the benefit from increased foot traffic more than outweighs its sacrifice.

To build on this low-cost/value point, Walmart undeniably uses its size to its advantage. It has deep pockets and purchases products in bulk to lower its per-unit cost. This allows it to undercut mom-and-pop shops and national grocery chains on price and keeps consumers confined to its ecosystem of products and services (especially when they live close to a supercenter).

Another key to Walmart’s success has been its embrace of technology. Promoting its online retail channels and Walmart+ subscription service helped lift global e-commerce sales by 25% during the fiscal 2026 second quarter (ended July 31), and has pushed its U.S. e-commerce operations into the profit column. It’s also leaning into AI as a way to improve supply chain management and improve order fulfillment times.

It would only take a 21% move higher for Walmart to become the 12th public company to reach $1 trillion, and it looks to be in an ideal position to do so.

Sean Williams has positions in Meta Platforms. The Motley Fool has positions in and recommends Berkshire Hathaway, Meta Platforms, Nvidia, Oracle, Taiwan Semiconductor Manufacturing, and Walmart. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

For well under $100, you can buy one share of this under-the-radar AI exchange-traded fund (ETF) that looks poised to continue to outperform the market.

For this article, I asked myself: Where would I start investing if I had less than $100 to invest?

Image source: Getty Images.

This answer to my question popped into my head: I’d want a concentrated exchange-traded fund (ETF) focused on leading and profitable companies heavily involved in artificial intelligence (AI), but with enough differences among themselves.

Why an ETF? Because I’d not want to put all my (investing) eggs in one basket.

Why AI? Because it’s poised to be the biggest secular trend in many decades or even generations.

Why concentrated? Because I believe if investors are going to buy a very diversified ETF, they might as well buy the entire market, so to speak, and buy an S&P 500 index ETF. Indeed, buying an S&P 500 index fund is a good idea for many investors, and recommended by investing legend Warren Buffett. That said, over the long run, I think an AI ETF full of only leading and profitable companies will beat the S&P 500 index.

And bingo! There is such an ETF — the Roundhill Magnificent Seven ETF (MAGS 1.92%). It has seven holdings — the so-called “Magnificent Seven” stocks: Alphabet (GOOG 4.38%) (GOOGL 4.53%), Amazon (AMZN 1.42%), Apple (AAPL 1.06%), Meta Platforms (META 1.18%), Microsoft (MSFT 1.01%), Nvidia (NVDA -0.10%), and Tesla (TSLA 3.54%). This ETF closed at $62.93 per share on Friday, Sept. 12.

These megacap stocks (stocks with market caps over $200 billion) were given the Magnificent Seven name a couple of years ago by a Wall Street analyst due to their strong growth and large influence on the overall market. The name comes from the title of a 1960 Western film.

Two other main traits I like about this ETF:

Since its inception in April 2023 (almost 2.5 years), the Roundhill Magnificent Seven ETF has returned 160% — 2.4 times the S&P 500’s 65.9% return.

Stocks are listed in order of current weight in portfolio. Keep in mind the ETF is rebalanced quarterly to make stocks equally weighted.

|

Holding No. |

Company |

Market Cap |

Wall Street’s Projected Annualized EPS Growth Over Next 5 Years |

Weight (% of Portfolio) |

1 Year/ 10-Year Returns |

|---|---|---|---|---|---|

|

1 |

Alphabet | $2.9 trillion | 14.7% | 17.72% | 55.9% / 677% |

|

2 |

Nvidia | $4.3 trillion | 34.9% | 15.00% | 49.3% / 32,210% |

|

3 |

Apple | $3.5 trillion | 8.8% | 14.13% | 5.6% / 812% |

|

4 |

Tesla | $1.3 trillion | 13.4% | 13.81% | 72.3% / 2,270% |

|

5 |

Amazon | $2.4 trillion | 18.6% | 13.30% | 22% / 762% |

| 6 | Meta Platforms | $1.9 trillion | 12.9% | 13.16% | 44.3% / 725% |

| 7 | Microsoft | $3.8 trillion | 16.6% | 12.76% | 20.3% / 1,250% |

|

Overall ETF |

N/A |

Total net assets of $2.86 billion |

N/A |

100% |

40.5% / N/A |

|

N/A |

S&P 500 |

N/A |

N/A |

N/A |

19.2% / 300% |

Data sources: Roundhill Magnificent Seven ETF, finviz.com, and YCharts. EPS = earnings per share. Data as of Sept. 12, 2025.

All these companies are profitable leaders in their core markets, and heavily involved in AI. Nvidia produces AI tech that enables others to use AI, while the other companies mainly use AI to improve their existing products and develop new ones.

Alphabet’s Google is the world leader in internet search. Its cloud computing business is No. 3 in the world, behind Amazon Web Services (AWS) and Microsoft Azure. The company also has other businesses, notably its driverless vehicle subsidiary, Waymo. (You can read here why I believe Nvidia is the best driverless vehicle stock.)

Nvidia is often described as the world’s leading maker of AI chips — and that it is. But it’s much more. It’s the world leader in supplying technology infrastructure for enabling AI. It’s also the global leader in graphics processing units (GPUs) for computer gaming.

Apple’s iPhone holds the No. 2 spot in the global smartphone market, behind Samsung. However, it dominates the U.S. market. The company’s services business is attractive, as it consists of recurring revenue and has been steadily growing.

Amazon operates the world’s No. 1 e-commerce business and the world’s No. 1 cloud computing business. It also has many other businesses, notably its Fresh and Amazon Prime Now (Whole Foods) grocery delivery operations.

Meta Platforms operates the world’s leading social media site, Facebook, as well as Instagram, Threads, and messaging app WhatsApp.

Microsoft’s Word has long been the world’s leading word processing software. Word is part of Microsoft Office, a suite of popular software for personal computers (PCs). Its Azure is the world’s second-largest cloud computing business.

Tesla remains the No. 1 electric vehicle (EV) maker, by far, in the U.S. despite struggling recently. In the first half of 2025, China’s BYD surpassed Tesla as the world’s leader in all-electric vehicles by number of units sold. CEO Elon Musk touts that the company’s robotaxi and Optimus humanoid robot businesses will eventually be larger than its EV sales business.

In short, the Roundhill Magnificent Seven ETF is poised to continue to benefit from the growth of artificial intelligence. Technically, it doesn’t have a long-term history. But if it had existed many years ago, it’s easy to tell that its long-term performance would be very strong because the long-term performances of all its holdings have been anywhere from great to spectacular.

Beth McKenna has positions in Nvidia. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends BYD Company and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

A peer across the Pacific Ocean has purchased the rights to one of the biotech’s pipeline drugs.

On Monday, investors clearly saw excellent value in the stock of Ocugen (OCGN 11.68%), a biotech that concentrates on treatments for eye disorders. They traded the company’s shares up by more than 12%, on the back of a fresh licensing agreement signed with a peer in Asia. That 12% absolutely trounced the 0.5% rise of the S&P 500 index today.

Ocugen announced that it has signed a licensing deal with Kwangdong Pharmaceutical in South Korea. Under the terms of the arrangement, Kwangdong will own the exclusive rights throughout South Korea for OCU400, an investigational drug targeting retinitis pigmentosa (RP). This is a disorder of the retina that causes progressive loss of vision.

Image source: Getty Images.

For the license, Ocugen is to be paid up-front fees and near-term development milestones amounting to as much as $7.5 million. The healthcare company can also earn milestones of $1.5 million for each $15 million of sales through Kwangdong. Ocugen said that if and when commercialized, OCU400 could hit sales of at least $180 million in the first 10 years of being on that market.

Lastly, the American company stands to earn royalty payments of 25% of the net sales of the drug in South Korea.

Ocugen’s hopes for the drug seem quite realistic, given that — according to its research — roughly 7,000 people in South Korea suffer from RP. And that’s the potential in only one country; if the drug is successfully brought to market elsewhere, this might be only the tip of the iceberg.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Your retirement budget isn’t ready until you’ve accounted for this.

You’re ready for a change of pace — not just leaving the workforce, but moving to another state or country in order to start fresh. While exciting, you’re probably also prepared for some challenges, like learning your way around your new neighborhood and coming up with a new retirement budget.

Though you might not expect it, you could also face Social Security challenges that affect your benefit delivery or how far your checks go. Fortunately, you can minimize the difficulty these issues pose by planning for them well in advance.

Image source: Getty Images.

Moving to another state won’t change the monthly Social Security check you’re entitled to, whether you’re receiving a retirement or spousal benefit. But it could affect how far your checks go. For example, if you move from a city with a high cost of living to a rural area where living expenses are cheaper, you might find that your checks go further than they would in your current city. On the other hand, if you move to a pricier area, you may have to pay for more of your expenses out of your own pocket.

Moving could also put you at risk of or help you avoid state Social Security benefit taxes. Only nine states still have these, and each has its own rules that determine who owes these taxes. It’s possible to live in a state with a Social Security benefit tax and not pay any state taxes on your checks. But it’s worth reaching out to your new state’s department of taxation or an accountant in that state to learn how it could affect your tax bill.

You could also find yourself owing federal Social Security benefit taxes wherever you go. These depend on your provisional income — your adjusted gross income (AGI), plus any nontaxable interest you have from municipal bonds and half your annual Social Security benefit. If you’re forced to spend more due to a higher cost of living in your new home, this could increase your AGI and your provisional income, potentially forcing you to pay more in federal income taxes.

If you decide to move to another country, you sidestep the issue of state Social Security benefit taxes. Depending on where you go, you might also be able to secure a lower cost of living to help your benefits go further.

You will still be responsible for paying federal Social Security benefit taxes if your provisional income is high enough. And you could also run into an accessibility issue if you retire in certain countries.

The Social Security Administration can pay you via direct deposit or a prepaid debit card in most parts of the world. However, if you retire in the following countries, you may not be able to receive your benefit payments:

You may be able to petition the Social Security Administration to make an exception for you if you agree to certain restricted payment terms.

This isn’t an option for those who choose to retire in Cuba or North Korea, however. There, you cannot get Social Security benefits at all.

If you retire in a country where the U.S. government won’t send Social Security checks, you may still be able to receive all your back payments if you later move from that country to a place where the Social Security Administration can send benefits again.

It’s best to contact the Social Security Administration directly if you have any questions about how your move could affect your Social Security checks. This way, you’ll be able to get a personalized answer and then you can adjust your budget accordingly.

One pundit believes the share price could rise in excess of 50%.

Monday was a good day to be invested in Scholar Rock (SRRK 6.19%) stock. The clinical-stage biotech received a nod from an analyst initiating coverage on its shares, a move that sent its price more than 6% higher across the day. That rate was well higher than the 0.5% increase of the S&P 500 index.

Well before market open, Leerink Partners’ Mani Foroohar launched his coverage of Scholar Rock, rating the healthcare stock as an outperform (i.e., buy) at a price target of $51 per share. That anticipates considerable growth in the value of the company’s equity, as it’s — coincidentally — more than 51% higher than Scholar Rock’s most recent closing price.

Image source: Getty Images.

The biotech’s leading investigational drug is apitegromab, an add-on therapy that targets a disorder called spinal muscular atrophy (SMA). According to reports, Foroohar’s main source of optimism is the prospects for the drug, which is currently being reviewed for approval by both the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA, a regulator for the European Union).

In his inaugural note on Scholar Rock, the analyst also waxed bullish on the background of the company’s team, characterizing it as the most experienced in the commercialization of rare diseases among its covered healthcare stocks.

If Scholar Rock can win approval from one or both of those major regulators for apitegromab, it would be well positioned for success. However, I need to caution that getting the green light isn’t enough for a biotech — a new medicine must be effectively rolled out and marketed if it’s going to have any chance at success. So far, though, the indications look good for the company.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Share prices of IBM have nearly doubled in just three years. Investors are excited by the company’s shift into hot technologies.

International Business Machines (IBM 1.15%), which is usually referred to by its ticker IBM, is a global icon in the technology sector. The company has a surprising ability to change with the times, and it’s been doing so for more than 100 years now. Indeed, when IBM was founded back in 1911, it made things like scales and clocks. Today, it makes all sorts of equipment, including quantum computers, and it supports the cloud computing industry, which is the backbone of artificial intelligence (AI).

Even after a fairly sizable drawdown since July, shares of IBM still trade up around 20% or so over the past year. Over the trailing three years, the stock has nearly doubled in price. That’s a pretty sizable return and highlights the fact that Wall Street is obsessed with IBM shares again. As noted, the company has shifted into key areas like quantum, cloud computing, and AI.

Image source: Getty Images.

But what’s special about IBM is that it hasn’t always been focused on these areas. Just a few years ago, investors pretty much hated the stock because it was out of step with the technology sector. The concern about IBM was so bad that between 2012 and 2020, the stock actually lost roughly half of its value. Contrarian investors with a long-term view, however, realized that IBM had updated its business many times before.

The business revamp was difficult and took many years. It involved a large corporate spin-off, asset sales, and acquisitions, the largest of which was Red Hat. But IBM did what needed to be done to remain relevant. So while IBM is popular again because of its current business focus, the real reason to be obsessed with IBM for long-term investors is its proven ability to change with the world around it.

Reuben Gregg Brewer has positions in International Business Machines. The Motley Fool has positions in and recommends International Business Machines. The Motley Fool has a disclosure policy.

The red-hot nuclear energy stock is up a staggering 330% in 2025.

With investor sentiment around nuclear energy gathering momentum by the day, Oklo (OKLO 12.02%) has become unstoppable. The nuclear energy stock surged 11.9% today to all-time highs of $92.48 per share, as of 1 p.m. ET Monday.

Oklo stock has risen a jaw-dropping 330% in 2025 so far, as of this writing. Yes, you read that right, and today, you may thank President Donald Trump for sending the red-hot stock to a new all-time high.

Image source: Getty Images.

In a press statement released this morning, the U.K. government of revealed a flurry of deals that it will sign with the U.S. this week during Trump’s state visit to the nation. The U.K. government says it is the “golden age of nuclear power.”

The landmark partnership between the U.S. and the U.K. called the Atlantic Partnership for Advanced Nuclear Energy seeks to speed up the development and deployment of nuclear energy projects in both countries. The list of projects to be inked include multibillion-dollar deals, including plans to build up to 12 advanced modular reactors and develop data centers powered by small modular reactors (SMRs) in the U.K.

Although most of the deals are between private companies for now, the partnership will open the U.K. market to U.S. nuclear energy players, potentially paving the way for billions of dollars in investments between the two countries.

Investors believe Oklo could benefit, too, especially given its relationship with the U.S. Department of Energy (DOE).

Oklo is developing a small, modular fast-fission nuclear power plant called the Aurora powerhouse that can supply clean nuclear energy 24/7 and can even use recycled fuel. Oklo already has a site permit from the DOE to set up a commercial plant in Idaho, is in a DOE reactor pilot program, and has fuel supply agreements with the DOE, among other things.

Oklo is also focused on nuclear waste recycling. Just days ago, the company announced plans to build a $1.68 billion fuel recycling facility in Tennessee.

Oklo’s multifaceted relationship with the DOE and recent partnerships for data centers have sent the stock to the moon. The attention isn’t unwarranted, but with its market capitalization already crossing $13 billion, the valuations for a start-up that could still take years to commercialize its first product and generate any revenue look too stretched for comfort now.

Neha Chamaria has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Momentum traders love Pony AI stock today. Should you?

Shares of Pony AI (PONY 9.21%), which aims to use artificial intelligence to direct driverless vehicles for robotaxi services in China and elsewhere, soared as much as 12% in early trading Monday before retreating a bit in the afternoon — all on no obvious news.

As of 12:10 p.m. ET, Pony AI stock is still up a solid 10%.

Image source: Getty Images.

Pony bills itself as “a global leader in achieving large-scale commercialization of autonomous mobility” — but “leader” seems like a relative term.

Despite sporting a market capitalization well in excess of $5 billion, Pony did less than $86 million in revenue over the past year…and lost nearly $320 million in the process. What’s more — and strangely for a growth stock — the rate at which Pony’s revenues are growing resembles less a gallop and more a slow trot. After surging briefly in 2022, this start-up‘s sales have grown just 25% over the last two and a half years, a growth rate of less than 10% per year.

Losses, on the other hand, have more than doubled over the same period.

About 10 days ago, Pony issued a press release that suggests things could soon improve. The company says it’s partnering with Qatar’s largest transportation service provider, Karwa, to roll out a robotaxi service in that country. Apparently it has already begun testing robotaxis on public roads in Doha, the capital of Qatar.

Pony calls this a “significant milestone” — and it may turn out to be. But time is running short for Pony. With $600 million in the bank and a cash burn rate of $140 million per year, Pony has about four years to prove it can earn a profit. Until that happens, Pony stock remains a sell for me.

Rich Smith has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Investors are looking forward to Wednesday’s Federal Reserve rate decision.

Shares of Opendoor Technologies (OPEN 5.24%) were moving higher today, even as there was no news out on the volatile online home flipper.

Instead, investors seemed to be looking forward to Wednesday’s rate decision from the Federal Reserve, which will include commentary and a forecast on future rate cuts. Investors widely expect the central bank to cut the federal funds rate by 25 basis points on Wednesday. CEO Kaz Nejatian also began his first day on the job.

As of 10:33 a.m. ET, Opendoor stock was up 11.5%.

Image source: Getty Images.

Since its business is so closely tied to the housing market, few stocks seem to have more to gain from falling rates than Opendoor does, as housing is likely to bounce back as rates come down.

In addition to the expected rate cut of 25 basis points, we’ll also get some insight into the direction of future rate cuts, as the Fed will also release its quarterly “dot plot” projections, in addition to Fed chair Jerome Powell’s commentary at the press conference.

Back in June, the Fed had forecast 50 basis points of cuts this year, but that forecast could change as the labor market has softened substantially in the last couple of months.

New Opendoor CEO Kaz Nejatian is also starting in the job today, and co-founder Keith Rabois is back as chairman, which is likely to accelerate changes in the business.

Opendoor’s volatility will almost certainly continue through the coming weeks and months, as it’s turned into a meme stock, but one with a legitimate chance at a turnaround now with new leadership in place and interest rates expected to fall.

Expect the stock to swing on Wednesday as well. While the rate cut is likely priced in at this point, the stock will move based on commentary and the forecast from the Fed.

Jeremy Bowman has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

As the consumer investment world grows, the bank has a lot to gain.

Bank of America (BAC 0.71%) is one of the largest banks in the world, operating in the U.S. and more than 35 countries worldwide. By market cap, it’s the second-most valuable bank in the world, trailing only JPMorgan Chase. In the past five years, Bank of America has outperformed the S&P 500, with total returns close to 125% in that span, compared to the index’s 112% (through Sept. 12).

Even with Bank of America’s market-beating returns over the past five years, the next five years could continue the same momentum. The reason comes down to one factor: its consumer investment business.

Image source: Getty Images.

The consumer investment business involves standard brokerage accounts, wealth management, and financial advisory services. In the fourth quarter of 2024, Bank of America’s consumer investment assets crossed the $500 billion mark for the first time in the company’s history.

The company noted that this amount has doubled every five years, and it expects to hit $1 trillion in the next five years. In the second quarter of this year, it reached around $540 billion (up 13% year over year).

Hitting this mark won’t guarantee that Bank of America’s stock will soar (nothing guarantees that), but the growth of its consumer investment business means it will earn much more fee-based income and see higher margins than from other revenue sources like traditional lending. This should be a nice boost to Bank of America’s profitability, especially as we anticipate interest rates getting lowered over the next few years, which could impact the bank’s main revenue source.

Bank of America is an advertising partner of Motley Fool Money. JPMorgan Chase is an advertising partner of Motley Fool Money. Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends JPMorgan Chase. The Motley Fool has a disclosure policy.

Published on 15/09/2025 – 15:34 GMT+2

•Updated

15:53

A French liberal MEP has gathered signatures from 20 other lawmakers for a letter seen by Euronews calling on the European Commission to review its commitment made under the EU-US trade agreement to purchase US energy.

In the document— soon to be sent to Commission President Ursula von der Leyen, Trade Commissioner Maroš Šefčovič, and Energy Commissioner Dan Jørgensen—the MEPs led by Christophe Grudler of Renew call on the EU executive to reconsider its pledge to buy $750 billion worth of US energy products over the next three years.

These products include liquefied natural gas (LNG), oil, nuclear fuels, and small modular reactors (SMRs). The signatories argue the deal will undermine the EU’s climate goals, industrial competitiveness, and strategic sovereignty.

“Increasing LNG imports from US shale gas directly undermines our climate agenda and our methane emissions regulation,” the letter says, adding: “LNG is highly polluting when liquefied, shipped across the Atlantic and regasified. Such dependence is a climate time-bomb.”

The initiative was launched by Christophe Grudler, a French MEP from the liberal Renew group.

The letter also warns that beyond energy concerns, the deal risks exposing the EU to “political blackmail”, the US demanding changes to EU climate policies, including the Carbon Border Adjustment Mechanism, under which the bloc will apply levies on the carbon footprint of foreign imports from 1 January 2026.

The energy purchase commitment forms part of the EU-US agreement reached over the summer.

Some MEPs view the arrangement as deeply unbalanced, given that the US continues to impose 15% tariffs on EU goods, while the EU has agreed to make major investments in the US, including in the energy and defence sectors.

In their letter to the Commission, MEPs also slam what they describe as the “economic imbalance” created by the pledge to purchase $250 billion’s worth of energy over three years.

The letter describes this figure as “astronomical” adding: “To put this in perspective, the entire Competitiveness Fund proposed in the MFF amounts to €362 billion over seven years. How can we ask European companies to massively buy from the US while urging them to strengthen our competitiveness at home?”

The inclusion of US small modular reactors in the deal has also raised concerns among MEPs.

“At a time when the EU is building its own SMR supply chain, opening the door to US competitors is total nonsense.”

They further stress that commercial decisions “should remain the prerogative of companies, not be preempted by political pledges.”

Understanding just where your retirement plans stand has never been easier.

Not to brag, but I’ve always suspected that my love of financial planning may be unrivaled. While my husband believes it’s a sickness, I’ve always enjoyed putting together a household budget (even when the money was not flowing). And, as I recently confessed to a friend, I’m really into retirement planning.

That’s probably why mySocialSecurity has become one of my most visited sites. It didn’t feel like my birthday or anything. Still, I did feel a little jolt of excitement upon learning the Social Security Administration (SSA) just added new features to its mySocialSecurity site.

Decades ago, when I first started planning for a retirement that felt a millennium away, I’d search the house for our latest Social Security statements, grab a notebook, pen, and calculator, and find a comfortable place to calculate. I probably could have learned two foreign languages and how to play the cello in the time I spent grappling with all the “what ifs.”

That was pre-internet, and I didn’t have the information needed to create a long-term retirement plan that approached reality. But then, a bunch of geniuses contributed to the invention of the internet, and by 2012, the SSA had launched mySocialSecurity. While it was helpful back then, it’s become a masterful tool for anyone serious about retirement planning.

Image source: Getty Images.

The mySocialSecurity site has always offered helpful tools, but the SSA is upping its game with these new additions:

The retirement calculator lets you compare month-by-month benefit estimates for ages 62 through 70. If you’re thinking about retiring at age 63 years and 6 months, it will take mere seconds for the calculator to indicate your monthly benefit at 63 years and 6 months. The best thing about the retirement calculator is how it takes the fantasy out of retirement planning by helping you decide when you can realistically afford to retire.

The age-based fact sheet explains the relationship between your birth year and full retirement age. It spells out when you’ll reach full retirement age (FRA), the age at which you’re entitled to 100% of your Social Security benefits. It also shows what happens if you claim benefits at age 62 instead and how much your monthly benefit will be permanently reduced. Finally, the age-based fact sheet allows you to see how much your monthly benefit amount will increase if you delay claiming benefits past your FRA, up to age 70.

This fact sheet addresses how working while receiving Social Security benefits will impact your payments. While there’s no impact if you collect Social Security after FRA, this is where you’d visit to learn how much the SSA will deduct from your benefits if you continue to work before FRA kicks in.

The benefit verification letter spells out which benefits you currently receive. Whether you want it for your records or to provide proof of benefits to a third party, you can access the letter simply by logging into the site.

So you’ll never lose track of how much you’ve received in Social Security benefits, the SSA provides easy access to your SSA-1099, a tax form that reports your annual benefits. This information helps determine if your benefits are taxable and how much to report on your federal tax return.

Whether you’ve filed for Medicare for the first time or you’re ready to collect Social Security, your claim status provides up-to-date information regarding where your claim stands.

If you’ve ever lost your Social Security card, you may have experienced a moment of panic, wondering what to do. I’ve never actually misplaced mine, mostly because I’m afraid my parents will rise from the grave to remind me how important it is to protect it. Mom and Dad might have taken it a little easier on me if they knew how easy the SSA would make it to replace a card.

Here’s how mySocialSecurity makes retirement planning less labor-intensive for me. I suspect you’ll find even more interesting ways to use it.

I understand that retirement planning may not be everyone’s cup of tea. However, I compare it to taking a moment to stop midway through a cross-country trip, just to see where I am and how much farther I have to go.

Multifactor verification and other precautions are becoming essential as AI enables more sophisticated scams.

Video and phone call freezes are typically attributed to poor service or some exterior cause. But if you notice unusual white hairs around the edge of your CFO’s beard just before a freeze, and when the call resumes seconds later, the beard is once again jet black, should you follow his instructions to transfer funds?

Perhaps, but not without further verification. Fraudsters, aided by AI applications, may one day—soon, even—perfect so-called deepfake audio and video calls. But even now, “tells” can indicate something is amiss, and the temporary freeze could actually be AI’s doing.

“I was recently testing a platform that had a feature designed to help hide artifacts, glitches, or synching issues,” recalls Perry Carpenter, chief human risk management strategist at KnowBe4, a security awareness and behavior change platform. “The program would freeze the video on the last good deepfake frame to protect the identity of the person doing the deepfake. It’s clear that some attackers are using adaptive strategies to minimize detection when their deepfakes start to fail.”

“There should never be an immediate need to wire a large amount of money without first verifying [it].”

Perry Carpenter, Chief Human Management Strategist, KnowBe4

To what extent such attacks are successful or even attempted is unclear since companies typically keep that information under wraps. A significant attack reported last year by CNN and others involved a Hong Kong-based corporate finance executive of UK-based engineering firm Arup, who warily eyed an email requesting a secret, $25 million payment. He sent the money anyway, after a video call with several persons who looked and sounded like colleagues—but were, in fact, deepfakes.

In another incident reported by The Guardian last year, scammers used a publicly available photo of Mark Read, CEO of advertising giant WPP, to establish a fake WhatsApp account. That account in turn was used to set up a Microsoft Teams meeting that used a voice clone of one executive and impersonated Read via a chat window to target a third executive, in an attempt to solicit money and personal details.

A WPP spokesperson confirmed the accuracy of The Guardian’s account but declined to explain how the scam was foiled, noting only, “This isn’t something we are eager to relitigate.”

Unlike deepfake video clips, which are extremely difficult to detect, real-time voice and video via social messaging platforms are still prone to errors, says Carpenter. Whereas earlier deepfakes had obvious tells, like facial warping, unnatural blinking, or inconsistent lighting, newer models are starting to self-correct those irregularities in real time.

Consequently, Carpenter doesn’t train clients on the oftenfleeting technical flaws, because that can lead to a false sense of security. “Instead, we need to focus on behavioral cues, context inconsistencies, and other tells such as the use of heightened emotion to try to get a response or reaction,” he says.

Rapid deepfake evolution poses an especially significant risk for corporate finance departments, given their control over the object of the fraudsters’ desire. Distributing a new code word to verify identities, perhaps daily or even per transaction, is one approach, says Stuart Madnick, professor of information technology at MIT Sloan School of Management. There are various ways to do so safely.

When executives in corporate finance who deal with large fund transfers are well acquainted, they can test their voice or video counterparts by asking semi-personal questions. Madnick has asked alleged colleagues what their “brother Ben” thinks about an issue, when no such brother exists.

A clever, but not a permanent solution, Madnick cautions: “The trouble is that the AI will learn about all of your siblings.” Ultimately, all companies should use multifactor authentication (MFA), which bolsters security by requiring verification from multiple sources; most large companies have broadly implemented it. But even then, some critical departments may not consistently use MFA for certain tasks, notes Katie Boswell, US Securing AI leader at KPMG, leaving them susceptible.

“It’s important for corporate leadership to collaborate with their IT and technology teams to make sure that effective cybersecurity solutions, like MFA, are in the hands of those most likely be exposed to deepfake attacks,” she urges.

Even with MFA, devious fraudsters can mine social media and online resources and use AI to conjure authentic looking invoices and other documents, and along with deepfake video and/or audio, create backstories persuasive enough to convince executives to make decisions they later regret. That makes training critical, conditioning executives handling large sums of money to automatically pause when they receive unusual requests and demand additional verification.

“There should almost never be an immediate need to wire a large amount of money without first verifying through a known internal channel,” says Carpenter. An interlocutor who communicates over a private phone or email account is also problematic, especially if they resist moving the conversation to the company’s secure systems. Ploys like adopting a tone of urgency, authority, or high emotion are also red flags, “so it’s critical that people give themselves permission to pause and verify,” he said.

While two or more verifications help, companies must still ensure their verification sources are secure. Madnick recalls a client company losing money when a fraudster passed a phony check. Suspicious, the bank called the company’s corporate finance department to verify the transaction, but the fraudster had already instructed the phone company to reroute calls to a number where it validated the check.

“Companies can set up procedures with their phone company that require them never to reroute calls without further verification with the company,” Madnick says. “Otherwise, it’s at the discretion of the phone company.”

Given corporate finance’s allure for fraudsters, KPMG’s Boswell stresses the importance of keeping abreast of emerging threats. Since CFOs and other top finance leaders must focus on their immediate duties, they can’t be expected to read the latest research on deepfake attacks. But companies can establish policies and procedures that ensure IT, or other experts regularly update them, raising finance’s awareness of the latest types of attacks, both internally and at other companies.

Madnick regularly asks corporate finance executives to raise their hands if they know their departments have faced cyberattacks. Many do not.

“The trouble is that cyberattacks on average continue over 200 days before they’re discovered,” he says. “So, they may think they haven’t experienced an attack, but they’re just not aware of it yet.”

Corporate finance can also include deepfake scenarios in its risk assessments, including tabletop exercises incorporated in the company’s security initiatives. And employees should be encouraged to report even unsuccessful attacks, or what they believe may have been attacks, that they might otherwise dismiss, Boswell advises.

“That way, others in the organization are aware that it has potentially been targeted, and what to look out for,” she says.

In addition, while c-suite executives at large companies may have significant public profiles, information available externally about lower-level executives and departments such as accounts payable and accounts receivable should be limited. “Threat actors use that type of information more frequently using AI, to help manipulate targets through social engineering,” Boswell notes. “If they don’t have access to that data, they can’t incorporate it in attacks.”

Such precautions are only becoming more important, as deepfake fraudsters broaden and deepen their reach. While they have been spreading fastest in major economies such as the US and Europe, even countries whose populations use fewer common languages are increasingly exposed.

“Most criminals may not know Turkish, but what’s great about AI systems is that they can speak just about any language,” Madnick cautions. “If I were a criminal, I would target companies in countries that have been targeted less in the past, because they are probably less prepared.”

MercadoLibre exhibits attributes that Buffett may appreciate, but other aspects of the business may be concerning to him.

Latin American consumer conglomerate MercadoLibre (MELI 0.10%) has drawn considerable interest from investors. The company spearheaded Latin American e-commerce and pioneered the fintech industry in the region through its business segment, Mercado Pago.

Moreover, investors may be curious to know how it fits with Warren Buffett‘s investment philosophy, even though Berkshire Hathaway does not hold any MercadoLibre shares. Still, comparing MercadoLibre to Buffett’s philosophy could help investors better understand this investment and determine whether it is suitable for them.

Image source: Getty Images.

On the surface, it is not immediately apparent how well MercadoLibre’s stock and business align with Buffett’s philosophy. Buffett has tended to avoid companies in countries with unstable political environments. Berkshire sold Taiwan Semiconductor Manufacturing (TSMC) due to Taiwan’s precarious political position, so the same sentiment could discourage him from investing in MercadoLibre.

That does not always mean Berkshire avoids companies operating in the developing world. Buffett has invested in several Chinese companies and also showed interest in Latin American fintech a few years ago. For a time, it owned shares in Brazilian fintech stocks StoneCo and Nu Holdings, parent of the world’s largest digital bank outside of Asia.

However, it has since sold both companies without an explanation. That could mean Buffett feels increasingly uncomfortable with these markets.

That discomfort is likely to discourage Buffett and his team from paying a premium for such stocks. Unfortunately for Berkshire, MercadoLibre trades at a 58 P/E ratio, meaning it may have to pay more than a fair price to take advantage of this opportunity.

However, most of the inconsistencies are countered by Berkshire’s ownership of one company: Amazon. Amazon is MercadoLibre’s counterpart in the developed world. It is also a company that Buffett said he was “an idiot” for not seeing its potential earlier. Until recently, Amazon had an elevated P/E ratio, so it is possible he set his valuation concerns aside when his company purchased shares in 2019.

That is critical, since MercadoLibre seems to see some of the same valuation trends as Amazon when it was a smaller company. Additionally, Buffett likes industry leaders. That fits the description of Berkshire’s three largest positions, Apple, Bank of America, and American Express, all of which are among the top companies in their respective fields.

More importantly, Buffett likes to see long-term competitive advantages in stable industries, and MercadoLibre mostly fits that description. As mentioned, the company pioneered e-commerce in Latin America. Furthermore, it leads its region in fintech and has developed a shipping and fulfillment network that gives it a competitive edge.

Indeed, investors tend not to associate Latin America with stability. Nonetheless, from building a logistics operation to developing Mercado Pago to sell online in a cash-based society, MercadoLibre has successfully turned regional challenges into advantages.

MercadoLibre stock is a worthy investment, but Warren Buffett more than likely does not see it that way. Indeed, MercadoLibre’s leadership in e-commerce and fintech in Latin America is likely to bolster the stock, even at a 58 P/E ratio. Since it possesses the unique talent of turning regional adversity into a revenue source within fast-growing industries, the stock is likely to continue its upward trend in the longer term.

Still, Buffett ultimately has shown little tolerance for political instability. His past positions in StoneCo and Nu Holdings showed some open-mindedness, but the fact that Berkshire sold these positions without any apparent justification is telling. His sale of TSMC seems to confirm these feelings.

Ultimately, given its history and resilience, long-term investors are likely to outperform the market with MercadoLibre stock. Just don’t expect Buffett to follow that lead.

American Express is an advertising partner of Motley Fool Money. Bank of America is an advertising partner of Motley Fool Money. Will Healy has positions in Berkshire Hathaway, MercadoLibre, and Nu Holdings. The Motley Fool has positions in and recommends Amazon, Apple, Berkshire Hathaway, MercadoLibre, StoneCo, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Nu Holdings. The Motley Fool has a disclosure policy.

Aldo Perracini was appointed CFO of Meren Energy, formerly Africa Oil Corp., in March, following its acquisition of Prime Oil & Gas Coöperatief. Listed in Toronto and Stockholm, Meren focuses on production, development, and exploration, with assets across Africa. Its largest shareholder is BTG Pactual, where Perracini began his career in 2008.

Global Finance: Since you took the CFO role at Meren, what has been your main challenge?

Aldo Perracini: I’d highlight two main challenges. First, stepping into my first CFO role at a listed company brought a significant shift, particularly around regulatory demands and managing relationships with equity investors. It’s been a steep but rewarding learning curve. Second, integrating Prime and Africa Oil wasn’t just operational, it was cultural. Both had strong, independent teams, and we worked hard to bring them together. Today, we’ve built a streamlined, unified team that’s aligned in purpose and values.

GF: What’s distinctive about the CFO role in the oil and gas industry?

Perracini: Like any commodity business, oil and gas is highly volatile. What makes it especially complex—particularly in deep offshore—is it’s capital intensity. You’re constantly balancing sharp price fluctuations with the need to commit significant investment to long-term projects. Navigating that tension is a core challenge for CFOs in this space.

GF: How do you manage the business in an exceptionally uncertain period?

Perracini: You could say we’re in exceptional times, but truthfully, we’ve been in them for a while now. Since Covid-19 and the years that followed, volatility has become the norm. In our sector, the best way to manage that is through hedging; we hedge an adequate portion of our production to reduce exposure to price swings. We also maintain strong financial buffers: a solid cash position and a low gearing ratio compared to peers. That gives us resilience in a very unpredictable global environment.

GF: How much has AI changed the way you work?

Perracini: We’re still in the early stages, but AI is already proving valuable. We are structuring the company to use it to automate repetitive tasks like reconciliations, invoice processing, and data aggregation, which frees up time for deeper analysis. The real potential lies in using AI for real-time modeling of commodity prices, working capital, and credit exposure. It will make our decision-making faster and allow us to focus more on strategy than on data processing. I am a big supporter of extending AI use.

GF: Looking ahead two to three years, how do you define success in your role?

Perracini: Success for me is delivering on what the business plan communicates to the market. It’s about building credibility by executing our strategy, particularly through shareholders’ return and disciplined M&A growth. We’re not chasing specific production or reserve targets. Our focus is on creating shareholder value, growing the business carefully while maintaining financial discipline and resilience in a volatile industry.

GF: What areas absorb most of your time and energy?

Perracini: I split my time across three main areas. First, financial strategy: hedging, financing, and liquidity planning to ensure strong credit metrics. Second, team leadership: building a cohesive team. And third, managing external relationships with auditors, regulators, banks, investors, and lenders.

GF: How do you ensure you have the right team in place?

Perracini: It starts with technical competence across finance, accounting, and technology. But just as important is culture: discipline, resilience, and above all, integrity. Transparency is key; people should feel safe to admit mistakes or challenge ideas. The best argument should always win, no matter who it comes from. That’s how you build trust and make better decisions.

GF: What keeps you up at night?

Perracini: Honestly, I sleep well! But volatility is always on my mind. The first thing I do each morning is check the news for any geopolitical shocks, from missiles to tariffs. These events can impact our industry instantly. Being alert to that risk helps us stay ahead and mitigate it wherever possible.

Article content

TORONTO — dynaCERT Inc. (TSX: DYA) (OTCQB: DYFSF) (FRA: DMJ) (“dynaCERT” or the “Company”) is pleased to announce the appointment of John Amodeo effective immediately.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

or

Article content

John Amodeo has recently joined the Board of Directors of dynaCERT (See Press Release dated July 30, 2025) and continues to serve as a Member of the Board of Directors and has served as Chair of dynaCERT’s Audit Committee since his appointment. John has resigned from his position as Audit Committee Chair to take on the new role as Chief Financial Officer.

Article content

Article content

Article content

As a new Director of dynaCERT, Mr. Amodeo’s vast capabilities in global business development and market strategies will provide added direction to the Board of Directors to boost dynaCERT’s international and domestic expansion. His industry and network knowledge aligns with dynaCERT’s expansion plans aimed at growing the sales volume of the Company’s climate change mitigation products.

Article content

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Mr. Amodeo brings to dynaCERT over 40 years of experience in business including in the North American metals and steel industry. Mr. Amodeo had a career as Executive Vice President and Chief Financial Officer of Samuel, Son & Co., Limited; Vice President and Chief Financial Officer of Samuel Manu-Tech, Inc.; Executive Vice President and Chief Financial Officer of Bracknell Corporation; Senior Vice President, Finance and Chief Financial Officer of Molson Breweries and as a member of the Auditing Practice at Coopers & Lybrand, Chartered Accountants. He is a Member of the Chartered Professional Accountants Canada and CPA Ontario. He attended Harvard Business School (Program for Management Development) and holds a Bachelor of Commerce Degree from the University of Toronto.

Article content

Jean-Pierre Colin, who took on the role of interim CFO of dynaCERT on March 31, 2023, continues in his senior role with dynaCERT as Executive Vice President and continues to serve as a Member of the Board of Directors, and Corporate Secretary of the Company.

Article content

Jim Payne, Chairman and CEO of dynaCERT, stated, “Along with our Board of Directors and the entire team at dynaCERT, I welcome John Amodeo as CFO of our Company. John will not only actively work as a CFO and Director but also will lend his financial expertise at the board level as we continue to build and strengthen our team for continued growth and global expansion in many vertical markets. I also personally take this moment to thank my colleague, Jean-Pierre Colin, who served as interim CFO of dynaCERT for over two years and remains committed as a continuing senior officer and Director of the Company.”

Article content

About dynaCERT Inc.

Article content

dynaCERT

Article content

Inc. manufactures and distributes Carbon Emission Reduction Technology along with its proprietary HydraLytica™ Telematics, a means of monitoring fuel consumption and calculating GHG emissions savings designed for the tracking of possible future Carbon Credits for use with internal combustion engines. As part of the growing global hydrogen economy, our patented technology creates hydrogen and oxygen on-demand through a unique electrolysis system and supplies these gases through the air intake to enhance combustion, which has shown to lower carbon emissions and improve fuel efficiency. Our technology is designed for use with many types and sizes of diesel engines used in on-road vehicles, reefer trailers, off-road construction, power generation, mining and forestry equipment. Website:

Article content

Article content

Article content

Article content

READER ADVISORY

Article content

This press release of dynaCERT Inc. contains statements that constitute “forward-looking statements”. Such forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause dynaCERT’s actual results, performance or achievements, or developments in the industry to differ materially from the anticipated results, performance or achievements expressed or implied by such forward-looking statements. There can be no assurance that such statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements. Actual results may vary from the forward-looking information in this news release due to certain material risk factors.

Article content

Except for statements of historical fact, this news release contains certain “forward-looking information” within the meaning of applicable securities law. Forward-looking information is frequently characterized by words such as “plan”, “expect”, “project”, “intend”, “believe”, “anticipate”, “estimate” and other similar words, or statements that certain events or conditions “may” or “will” occur. Although we believe that the expectations reflected in the forward-looking information are reasonable, there can be no assurance that such expectations will prove to be correct. We cannot guarantee future results, performance of achievements. Consequently, there is no representation that the actual results achieved will be the same, in whole or in part, as those set out in the forward-looking information.

Article content

Forward-looking information is based on the opinions and estimates of management at the date the statements are made and are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those anticipated in the forward-looking information. Some of the risks and other factors that could cause the results to differ materially from those expressed in the forward-looking information include, but are not limited to: uncertainty as to whether our strategies and business plans will yield the expected benefits; availability and cost of capital; the ability to identify and develop and achieve commercial success for new products and technologies; the level of expenditures necessary to maintain and improve the quality of products and services; changes in technology and changes in laws and regulations; the uncertainty of the emerging hydrogen economy; including the hydrogen economy moving at a pace not anticipated; our ability to secure and maintain strategic relationships and distribution agreements; and the other risk factors disclosed under our profile on SEDAR at

Two AI beneficiaries just posted eye-catching updates. But which is the more attractive stock?

Shares of Broadcom (AVGO 0.19%) and Oracle (ORCL -5.05%) both ripped higher around earnings, with Oracle’s one-day surge among the biggest in decades. Broadcom, a chip and infrastructure-software company, continues to ride custom artificial intelligence (AI) accelerators and high-end networking. Oracle, the database and cloud provider, stunned investors with a massive jump in contracted work tied to AI demand.

The question for investors is which AI stock looks more attractive after these moves. Looking through the numbers and today’s prices, the edge goes to the company with faster AI growth in hand and a clearer path from bookings to revenue.

Image source: Getty Images.

Broadcom’s most recent quarter underscored how central AI has become to results. In the third quarter of fiscal 2025 (the quarter ended Aug. 3), revenue rose 22% year over year to about $16 billion, adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) margin was 67%, and non-GAAP earnings per share was $1.69. Management also guided for fourth-quarter revenue of about $17.4 billion and said AI semiconductor revenue should climb to roughly $6.2 billion in the fourth quarter after growing 63% to $5.2 billion in the third. Free cash flow hit $7.0 billion, or 44% of revenue.

Summing the last four reported quarters puts Broadcom’s trailing-twelve-month non-GAAP earnings per share at about $6.29. At the stock’s price at the time of this writing, near $365, the stock trades around 58 times that trailing-12-months (TTM) figure — rich even after factoring in Broadcom’s breadth across AI accelerators, ethernet switching, and VMware-driven infrastructure software.

One key risk for Broadcom is that a large slice of near-term growth depends on just a handful of hyperscale customers, and cyclical pockets in legacy networking or storage can offset AI strength. Still, Broadcom‘s cash generation, dividend capacity, and guidance argue for durable fundamentals as AI builds out. The question is whether that durability is already priced in.

Oracle’s fiscal first quarter of 2026 (the quarter ended Aug. 31) changed the story. Revenue rose 12% to $14.9 billion, non-GAAP EPS increased 6% to $1.47, and — most importantly — remaining performance obligations (RPO) soared 359% to $455 billion on the back of four multi-billion-dollar AI agreements. Yes, you heard that right. Cloud revenue grew 28%, including 55% growth in infrastructure-as-a-service. Investors reacted in dramatic fashion, sending the stock up roughly 36% in a day.

In the company’s earnings release, CEO Safra Catz called it “an astonishing quarter,” adding that demand for Oracle Cloud Infrastructure is building and that more large contracts could follow. Management also previewed a multi-year framework for accelerating Oracle Cloud Infrastructure revenue growth tied to these wins. Momentum in the business is visible in the reported numbers and management’s commentary, but RPO is a commitment that must convert to usage; investors will need to see that flow through revenue and margins over time.

Trading at about $315 as of this writing, Oracle trades roughly 52 times TTM non-GAAP earnings — also expensive, but a discount to Broadcom on this basis. The stock’s violent move higher means execution against that towering backlog is now the key driver of returns from here.

Both companies are clear AI winners. Broadcom has revenue and cash flow already showing up from AI hardware and networking, plus a software portfolio that throws off steady cash. Oracle just unlocked a wave of contracted demand that, if it converts as management expects, could drive years of cloud infrastructure growth.

Choosing between them comes down to what is embedded in the share prices. Broadcom offers observable AI revenue today, but the stock carries a higher non-GAAP TTM price-to-earnings multiple. Oracle’s valuation is lower (though still elevated) and is now backed by a backlog that, if it turns into actual consumption, could reset the company’s growth profile. Given the trade-off — realized AI revenue at a steeper multiple versus massive contracted AI demand at a somewhat lower one — Oracle looks slightly more compelling for investors willing to accept the execution risk of turning record bookings into billable usage at healthy margins. Broadcom remains a high-quality AI play, but its premium leaves less room for error after the recent rally.

Daniel Sparks and his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Oracle. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Cathie Wood’s Ark Investment Management is forecasting a major shift in Tesla’s business.

Tesla (TSLA 7.21%) is one of the world’s largest manufacturers of electric vehicles (EVs), but rising competition is slowly chipping away at its market share. EV sales are still the main driver of Tesla’s financial results, but CEO Elon Musk is trying to future-proof the company by steering its resources into new products like autonomous vehicles and robotics.

Ark Investment Management, which was founded by seasoned tech investor Cathie Wood, predicts autonomous vehicles will transform Tesla’s economics. In fact, Ark thinks a whopping 86% of the company’s earnings will come from self-driving robotaxis by 2029, paving the way for a stock price of $2,600. That would be a 615% increase from where Tesla stock trades today.

How realistic is Ark’s forecast? Let’s dive in.

Image source: Tesla.

To meet Ark’s bullish 2029 forecast, Tesla will have to transition from selling passenger EVs to selling self-driving robotaxis, and it will also have to build new services like an autonomous ride-hailing network.

Unfortunately, Tesla is currently operating from a position of weakness, which is forcing this shift earlier than the company perhaps would have liked. After all, government regulators haven’t approved Tesla’s full self-driving (FSD) software for unsupervised use anywhere in the U.S. yet, which is a huge barrier to the success of its upcoming Cybercab robotaxi.

Tesla delivered 1.79 million passenger EVs during 2024, which was down 1% from the prior year, marking the first annual decline since the company launched its flagship Model S in 2011. The situation is much worse in 2025, with deliveries shrinking by a whopping 13% in the first half of the year. This led to a 14% decline in Tesla’s revenue and a 31% collapse in its earnings per share (EPS) during the same period, which is alarming to say the least.

A rapid increase in competition is a key reason for Tesla’s woes. Low-cost EV producers like China-based BYD are making serious inroads into some of Tesla’s biggest markets. Tesla’s sales sank by 40% across Europe in July, despite EV registrations climbing by 33% overall. BYD, on the other hand, saw a whopping 225% increase in sales in the region.

Simply put, Tesla is quickly losing market share in the passenger EV space. The company is launching a low-cost EV of its own in order to compete, but production just started so it probably won’t be a factor until next year at the earliest.

Elon Musk is making a big bet on autonomous ride-hailing. The Cybercab, which will enter mass production in 2026, will run entirely on Tesla’s FSD software, so it’s designed to operate without any human intervention. In theory, that means it can haul passengers and even small commercial loads at all hours of the day, creating a lucrative new revenue stream for the company.

Scaling this business will come with challenges. I mentioned FSD isn’t approved for unsupervised use in the U.S. just yet, but Tesla will also have to compete with established ride-hailing giants like Uber Technologies, which has already partnered with 20 other companies in the autonomous driving space. Around 180 million people already use Uber every single month, so it’s in a much better position to dominate the autonomous ride-hailing industry compared to Tesla, which has to build an entire network from scratch.

However, Ark thinks Tesla will eventually make it work. Its forecasts suggest the company will generate $1.2 trillion in annual revenue by 2029, with 63% ($756 billion) coming from its robotaxi platform alone. Ark says that could translate to $440 million in earnings before interest, tax, depreciation, and amortization (EBITDA), with 86% attributable to the robotaxi because of its high profit margins — human drivers are the largest cost in existing ride-hailing networks, but the robotaxi won’t need them.

In my opinion, Ark’s predictions are too ambitious. Wall Street thinks Tesla will generate around $93 billion in revenue during 2025 (according to Yahoo! Finance), so that figure will have to grow by almost 1,200% over the next four years to meet Ark’s forecast of $1.2 trillion — driven by a brand-new robotaxi product that hasn’t even hit the road yet.

Tesla’s valuation is another issue. Its stock is trading at an eye-popping price-to-earnings (P/E) ratio of 209, making it almost seven times as expensive than the Nasdaq-100 technology index — which trades at a P/E ratio of 31.6. Remember, Tesla’s earnings are currently shrinking, which makes its premium valuation even harder to justify.

Therefore, I’m hesitant to buy into the idea that Tesla stock could surge by another 615% over the next four years to reach Ark’s price target of $2,600. It might be possible if the company’s robotaxi platform becomes as successful as Ark predicts, but I think that’s unlikely in such a short period of time. After all, Elon Musk has promised unsupervised self-driving cars for the last 10 years, and Tesla still hasn’t delivered.

Polkadot’s next phase: faster, better, and easier to use. Is the Web3 token ready to take off?

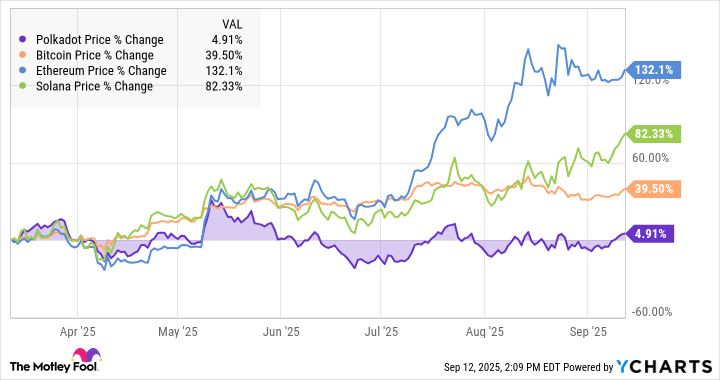

Investors in the Polkadot (DOT -3.88%) cryptocurrency have been craving game-changing news for a while now. The crypto market is having a great summer overall with fantastic returns on leading names like Bitcoin (BTC -0.57%), Ethereum (ETH -1.18%), and Solana (SOL -0.89%). But nobody told Bitcoin where the party was happening. As of Sept. 12, it gained less than 5% over the last 6 months:

Polkadot Price data by YCharts

Forget the chart for a moment, though. App builders, not price charts, ultimately drive durable value in most cryptocurrencies, and especially the developer-friendly Polkadot. And I have good news: Polkadot is readying two builder-centric platform upgrades that could change the trajectory of this lagging cryptocurrency. Say hello to the JAM scaling upgrade and a ready-to-code DevContainer.

Here’s what changed — and why it could matter for DOT investors.

The chain-spanning connector package known as Polkadot is about to get a massive makeover. The incoming technical changes are so powerful, Polkadot’s backers in the Web3 Foundation call it “Polkadot 3.0.”

I could get all up in the nerdy weeds with the changes, built around the Join Accumulate Machine (JAM) upgrade. Trust me, I’m tempted to go there. But you’re not here for that geekery, so let’s keep it simple: Polkadot is about to get much faster, more flexible, and easier to use.

The global network of computing nodes that validate Polkadot transactions and execute code in its smart contracts is already one of the fastest blockchains on the market. JAM will multiply the computing power of this platform by 10, by some estimates. Polkadot co-founder Gavin Wood calls it “a supercomputer on the blockchain,” with easy and instant access to exactly the number-crunching resources your app needs.

Gone are the unpredictable auctions for computing time, in comes a new project funding system. Parachains are still a thing, and existing Polkadot projects will be fully compatible with the new JAM core. It’s just going to be much easier to get your hands on the right resources at the right time. There’s a price list now; just pay for your computing power and you’re good to go. Easy as Polkadot pie.

Image source: Polkadot.

The new DevContainer feature may not feel as important, but anything that attracts more developers to the Polkadot platform should also be good for the tightly integrated cryptocurrency in the long run.

The Polkadot Smart Contracts DevContainer does exactly that, at least in theory. Getting started as a Polkadot developer has never been easier. Traditional setups of a new development system can be a slow and frustrating process. Now, the manual setup and configuration is replaced by one command and lots of automation.

I can’t promise that this system will be popular with new or existing Polkadot app builders, but it sounds pretty good to my (non-developer) ears. Instant setup and then you’re dealing with the power-packed JAM system — where do I sign up?

The DevContainer package is already available and JAM should take over as the main Polkadot engine before the end of 2025. These helpful upgrades coincide with rising interest in Web3 apps, giving more control to app users and less of it to massive social network corporations.

Polkadot’s chart has actually been lagging behind other cryptocurrencies for years:

Polkadot Price data by YCharts

And it’s kind of funny. Using Polkadot in an app project, you can connect to many other cryptocurrencies and move data, monetary assets, or code from one blockchain to another. If Web3 is the blockchain-based foundation of the next internet epoch, then Polkadot is the digital glue that holds it together.

JAM replaces clunky auctions with pay-as-you-go capacity, and the DevContainer gets builders going in minutes. If people show up, it could turn into a real block party for DOT holders as usage drives demand.

I think it’s time to connect the DOTs between better tech and investor value. Polkadot has been struggling in the shadows for too long, letting the likes of Ethereum and Solana have all the headline-inspiring fun. That could change when JAM rolls out.

I don’t expect a sudden spike in DOT prices, but a lucrative rise over time as developers and app users (i.e., pretty much everybody) adopt this technology in real-world smartphone apps and cloud platforms.

Anders Bylund has positions in Bitcoin, Ethereum, Polkadot, and Solana. The Motley Fool has positions in and recommends Bitcoin, Ethereum, and Solana. The Motley Fool has a disclosure policy.

Delta just posted solid results and reiterated its outlook. Now the question is whether the stock’s valuation leaves enough upside for investors.

Last Wednesday, Delta Air Lines (DAL -0.83%) delivered a strong June-quarter update and reiterated its 2025 outlook, helping steady sentiment after a choppy year for airlines. The Atlanta-based carrier, one of the largest global network airlines, highlighted resilient premium demand, steady co-brand card economics, and progress on costs — all while acknowledging ongoing softness in economy seats.

The mix between main cabin and premium cabins has become a key storyline for Delta. Premium revenue and loyalty economics are doing more heavy lifting, while management trims weaker main cabin flying and leans into higher-margin products. With this backdrop, are shares a buy? More specifically, with guidance intact and premium resilience evident, do shares offer an attractive risk-reward today?

Image source: Getty Images.

If there’s a meaningful slowdown in travel, Delta isn’t seeing it. The company’s second quarter produced record revenue and double-digit margins, giving management enough confidence to reiterate its full-year guidance. In the quarter, operating revenue was roughly $16.6 billion, operating margin was 13%, and earnings per share landed at $2.10 on the company’s non-GAAP basis. Management guided the September quarter to flat to up low-single-digit revenue growth year over year and a 9% to 11% operating margin, and reaffirmed full-year targets for earnings per share of $5.25 to $6.25 and free cash flow of $3 billion to $4 billion.

Beyond the headline numbers, the mix story stood out. Management said in the company’s second-quarter earnings call that “main cabin margins remain soft,” while reiterating that diversified revenue streams — credit card remuneration, loyalty, and premium cabins — now represent a large slice of the business. That matches comments on the call that softness is “largely contained to main cabin,” with premium products and the Delta-American Express partnership offsetting the pressure.