Alphabet’s stock has had an impressive run over the past few months.

Earnings season is upon us, and it’s possible that some stocks could make some large movements following their quarterly announcements. One that I’ve got my eye on that has significant momentum is Alphabet(GOOG 0.86%)(GOOGL 0.82%). Since reporting Q2 earnings on July 23, Alphabet has received several positive developments, including a judge’s decision not to seek a breakup of Alphabet’s core business.

The good news sent shares soaring, with the stock up over 30% since reporting Q2 earnings. That’s a monstrous move for a large company like Alphabet (it’s currently the fourth-largest company in the world and recently crossed the $3 trillion valuation mark for the first time), but can it continue?

I think management’s Q3 outlook could be another catalyst for the stock to go higher, and buying it before it reports earnings on Oct. 29 is a smart move.

1. Persistent advertising growth

Throughout most of 2025, the consensus is that Alphabet’s primary property, the Google Search engine, was in trouble. Everyone was worried about how it would fare against generative AI competition, but it turns out it will be just fine. Google’s revenue growth has been resilient even in the face of rising competition from generative AI models, with its revenue growing at a 12% pace in Q2.

Part of the reason for this growth is that Google has incorporated AI search overviews into every Google search. This results in a hybrid search experience, combining traditional search with a generative AI-powered one. Management also commented that the AI search overview has about the same monetization as a standard search, so it’s not losing any money on this switch either.

If Alphabet reports growing Google Search revenue during this quarter, it will confirm that Google is continuing to excel even when everyone assumed that it couldn’t. With Alphabet’s core business doing well, I think it makes the stock a great buy.

2. Rising cloud computing demand

Another exciting area for Alphabet is its cloud computing division, Google Cloud. Cloud computing is one of the fastest-growing industries around, and is benefiting from a general migration to the cloud alongside rising AI demand. Google Cloud has become a great partner in this realm and has won business from OpenAI (the makers of ChatGPT) and Meta Platforms(META 0.82%).

While Google Cloud isn’t as large as some of its competitors, it’s growing at a healthy rate, with revenue rising 32% year over year in Q2. It’s also dramatically improving its operating margin, increasing from 11% last year to 21% this year. Investors are going to want to see this trend continue, and if it does, the stock could respond positively as a result.

3. Alphabet has a reasonable valuation

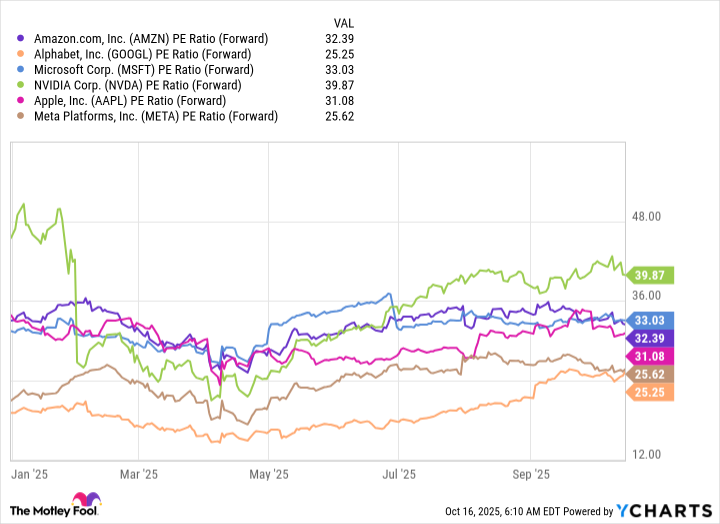

Lastly, Alphabet is still valued at a discount to its peers. Despite having an impressive run over the past few months, Alphabet still trades at a discount to all of its big tech peers from a forward price-to-earnings (P/E) standpoint.

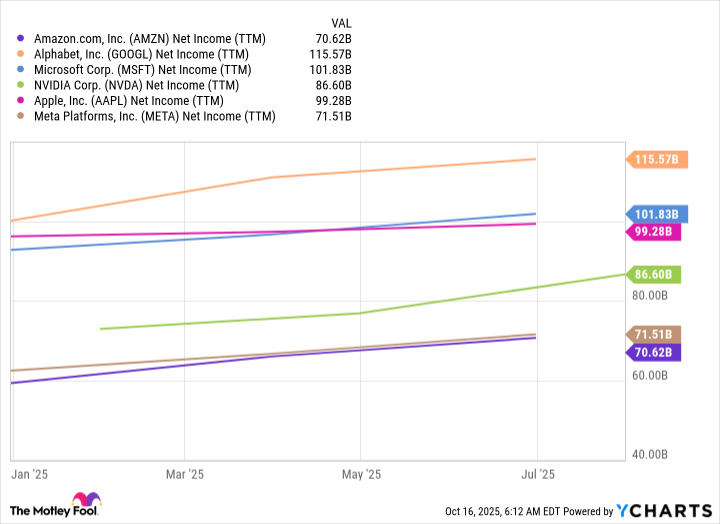

However, after its monstrous run, it’s extremely close to swapping places with Meta Platforms. Still, Alphabet is trading at a discount to others like Microsoft(MSFT 0.50%) and Apple(AAPL 2.04%). If all companies had an equal valuation, Alphabet would actually be the world’s largest because it generates the most net income out of all of them.

However, that’s not the way the stock market works, but it does give Alphabet an edge in future investments, as it has significant cash flows that it can buy back stock with, invest in AI, or potentially acquire a business.

Regardless, Alphabet is a highly profitable business with a reasonable valuation that’s growing at a healthy pace. I still think there’s plenty of room for the stock to run, and another catalyst could arrive when it reports earnings on Oct. 29. By buying now, investors can ensure that they get in on a potential pop following the earnings announcement.

Keithen Drury has positions in Alphabet and Meta Platforms. The Motley Fool has positions in and recommends Alphabet, Apple, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Rigetti Computing’s stock has been on an absolute tear over the past few weeks.

Quantum computing pure-play stocks have been on an unbelievable run over the past few weeks. One year ago, Rigetti Computing (RGTI -3.01%) was essentially a penny stock, trading for less than $1 per share. Now, it’s worth nearly $50 per share. A huge chunk of that growth has come recently, as Rigetti Computing traded for about $15 at the start of September.

There have been numerous headlines that have driven Rigetti Computing’s stock higher over the past few weeks, and after these unbelievable returns, some may be wondering if it’s time to take some profits and move on. However, should Rigetti Computing continue going higher, investors will miss out on some lucrative returns.

So, which course of action is the best?

Image source: Getty Images.

Rigetti Computing has soared on a few pieces of news recently

Rigetti Computing is a quantum computing pure play and has no backup business. For Rigetti, it’s quantum computing supremacy or bust. This is no easy feat, as the quantum computing space is filled with other strong competition like Alphabet and International Business Machines (IBM). Both have nearly unlimited resources compared to Rigetti, which makes this uphill climb even more challenging.

However, there are signs that Rigetti will be just fine. Just recently, it announced that it has sold quantum computing systems to two customers for about $5.7 million. One was to an Asian manufacturing company, while the other was a California physics and AI start-up. This shows Rigetti Computing already has a competitive offering for clients, as these two likely shopped around for other options before settling on Rigetti’s Novera quantum computer.

Another headline that caused Rigetti’s stock to pop was JPMorgan‘s announcement that it was investing up to $10 billion in four areas, one of which is quantum computing. This caused shares across the sector to pop, which has me worried that the quantum computing sector may be getting too hot.

In addition to quantum computing, JPMorgan was also planning on investing in supply chains and advanced manufacturing, defense and aerospace, and energy. There are a lot of mouths to feed in those investment sectors, and it’s not like JPMorgan is going to dump all $10 billion into quantum computing stocks. Furthermore, there was no specific announcement that JPMorgan would invest in Rigetti Computing; it was just that it was interested in investing in the sector.

After the pop, Rigetti is a $15 billion company, so even if it received a $1 billion investment from JPMorgan (which is extremely unlikely for JPMorgan to spend 10% of its funds on one company), it would only amount to a small stake in the business.

I think this displays how overheated the quantum computing investment market is getting, as we’re still a ways away from quantum computing being adopted at a widespread scale.

Rigetti Computing thinks we’re still years away from a large quantum computing market

Most quantum computing competitors point toward 2030 as the year when quantum computing will start to become a viable technology. Before 2030, Rigetti estimates that the annual value for quantum computing providers is about $1 billion to $2 billion, mostly fueled by government labs and other research institutions. From 2030 to 2040, the market heats up quite a bit, with Rigetti Computing estimating $15 billion to $30 billion.

If we estimate that the market will reach $30 billion in annual value by 2035, Rigetti captures a 90% market share (similar to what Nvidia has done in the AI world), and it can deliver a 50% profit margin (what Nvidia has accomplished), that would give Rigetti $6.75 billion in annual profits. If we apply a 40 times earnings multiple on that, it would indicate Rigetti would be valued as a $270 billion company. That’s more than a 10-bagger from today’s levels, so if Rigetti wins the quantum computing arms race and takes significant market share, there is still plenty of upside left in the stock.

However, there’s likely to be a large market drawdown sometime between now and 2035, and I’ll likely stay patient with investing in quantum computing stocks until then. I wouldn’t be surprised to see this upward trend continue for the stocks, but that means a bubble could be forming. I don’t think it’s a bad idea to trim some of your quantum computing stocks to take a quick win, as it is a good combination of letting your winners run while also being prudent about the rapid rise of these stocks that are still years away from profitability and viability.

JPMorgan Chase is an advertising partner of Motley Fool Money. Keithen Drury has positions in Alphabet and Nvidia. The Motley Fool has positions in and recommends Alphabet, International Business Machines, JPMorgan Chase, and Nvidia. The Motley Fool has a disclosure policy.

Macro conditions could improve thanks to central bank rate cuts.

Shares of SoFi Technologies(SOFI -0.24%) have been on an unbelievable run. During the past year, they have soared 166% (as of Oct. 17). The tech heavy Nasdaq Composite is up 24% during the same period.

SoFi has been putting up strong financial results. And the market has noticed, viewing the business in a much more optimistic light.

This fintech stock is now trading not far from record territory, so investors might think it’s too late to put some money to work. But that’s a flawed perspective. Here’s one reason now is a great time to buy SoFi.

SoFi should benefit as rates start to come down

Last month, the Federal Reserve lowered its benchmark fed funds rate. This was the first reduction since December 2024.

Market watchers have been waiting for such a move, as the central bank aims to boost the labor market. Investors expect the Fed will lower the rate two more times before the year is over.

Generally speaking, lower interest rates are good for the economy. They can drive consumer spending and business investment since it becomes cheaper to borrow capital. Consequently, a bank like SoFi can benefit greatly.

It is already growing rapidly. During the second quarter, its revenue surged 43%, with the business adding 846,000 net new customers. Despite a prolonged period of above-average interest rates, SoFi has still been expanding at a brisk pace. The potential for lower interest rates can supercharge that growth.

In the second quarter, the bank originated $8.8 billion worth of loans (combined among personal, student, and home). That figure was up 64% year over year. Besides interest income, the business collects fees for originations. And lower interest rates, unsurprisingly, can jump-start loan originations, which have already been growing at a fantastic clip.

This same situation can help the banking industry as a whole. On the flip side, though, investors need to pay attention to risks. Lower interest rates might spur demand from borrowers to take out loans. However, this can increase default risk on a lender’s balance sheet.

To its credit, SoFi has done a good job targeting a more affluent demographic. For instance, the company’s personal-loan borrowers have a weighted-average income of $161,000 and a weighted-average Fair Isaac FICO score of 743. They should be better able to make their loan payments.

“The health of our consumer remains strong, and we’re not seeing any signs of weakness,” Chief Financial Officer Chris Lapointe said during the second-quarter earnings call.

The business is poised to continue growing its profits

A reduction in interest rates can not only help SoFi generate more revenue, but it can also increase the company’s profits. It first became profitable on the basis of generally accepted accounting principles (GAAP) in the fourth quarter of 2023. Since then, the bottom line has expanded in an impressive fashion.

In 2024, SoFi reported $227 million in adjusted net income; management expects the company will post $370 million in 2025. And Wall Street analysts on average anticipate earnings per share will increase 77% in 2026 and 36% in 2027.

This is a very exciting outlook for shareholders. It highlights that SoFi operates with a very scalable business model, which is helped by the fact that it doesn’t carry the overhead of physical bank branches. It would make sense that SoFi’s earnings would grow at a faster clip than the top line.

And that can continue driving the stock higher. Value investors might hesitate, with the shares trading at a forward price-to-earnings (P/E) ratio of 47. However, don’t ignore the incredible trajectory that SoFi is on. It’s easy to be confident that the stock will do well over the long run given a more accommodative interest-rate environment that can push profits up.

Neil Patel has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The people who know Nvidia and Palantir best are sending a very clear and cautionary signal to investors.

With roughly 10 weeks to go before 2025 comes to a close, it looks as if it’ll be another banner year on Wall Street — and the evolution of artificial intelligence (AI) is a big reason why.

Empowering software and systems with AI capabilities affords them the opportunity to make split-second decisions and become more efficient at their assigned tasks without human intervention. It’s a game-changing technology that the analysts at PwC believe can add $15.7 trillion to the global economy by the turn of the decade.

Although dozens of public companies have benefited from the AI revolution, none have taken their spot on Wall Street’s mantle quite like Nvidia(NVDA 0.86%), the largest publicly traded company, and Palantir Technologies(PLTR 0.11%). Since 2022 came to a close, Nvidia stock has rocketed higher by more than 1,100% and added over $4 trillion in market value. Meanwhile, Palantir shares are approaching a nearly 2,700% cumulative gain, as of the closing bell on Oct. 16, 2025.

Image source: Getty Images.

While there’s a laundry list of reasons that can justify the breathtaking rallies we’ve witnessed in both companies, this dynamic AI duo has also issued a very clear warning to Wall Street that can’t be swept under the rug.

Nvidia’s and Palantir’s success derives from their sustainable moats

There are few business characteristics investors appreciate more than sustainable moats. Companies that possess superior technology, production methods, or platforms don’t have to worry about competitors siphoning away their customers.

Nvidia is best known for its world-leading graphics processing units (GPUs), which act as the brains of enterprise AI-accelerated data centers. Though estimates vary, Nvidia is believed to control 90% or more of the AI-GPUs currently deployed in corporate data centers.

No external GPU developers have come close to challenging Nvidia’s Hopper (H100), Blackwell, or Blackwell Ultra chips, in terms of compute abilities. With CEO Jensen Huang targeting the release of a new advanced AI chip in the latter half of 2026 and 2027, it seems highly unlikely that Nvidia will cede much of its AI-GPU data center share anytime soon.

To add fuel to the fire, Nvidia’s CUDA software platform has served as an unsung hero. This is the toolkit used by developers to build and train large language models, as well as maximize the compute abilities of their Nvidia hardware. The value of this software is exemplified by Nvidia’s ability to keep its clients within its ecosystem of products and services.

Meanwhile, the beauty of Palantir’s operating model is that no other company exists that can match its two core AI- and machine learning-inspired platforms at scale.

Gotham is Palantir’s true breadwinner. This software-as-a-service platform is used by the U.S. government and its primary allies to plan and oversee military missions, as well as gather and analyze data. The other core platform is Foundry, which is a subscription-based service for businesses looking to make sense of their data and automate some aspects of their operations to improve efficiency.

Palantir’s government contracts have supported a consistent annual sales growth rate of 25% or above, and played a key role in pushing the company to recurring profitability well ahead of Wall Street’s consensus forecast.

Yet in spite of these well-defined competitive edges, this AI-inspired dynamic duo has offered a stark warning to Wall Street and investors.

Image source: Getty Images.

Nvidia’s and Palantir’s insiders are sending a clear message to Wall Street

Though AI has been the hottest thing since sliced bread over the last three years, it’s not without headwinds.

For example, every next-big-thing technology and hyped innovation since (and including) the advent of the internet more than 30 years ago has endured an early innings bubble-bursting event. This is to say that all new technologies have needed time to mature, and evidence of that maturation isn’t wholly evident from the companies investing in AI solutions.

But perhaps the most damning message of all comes from the insiders at Nvidia and Palantir Technologies.

An “insider” refers to a high-ranking employee, member of the board, or beneficial owner holding at least 10% of a company’s outstanding shares. These are folks who may possess non-public information and know their company better than anyone on Wall Street or Main Street.

Insiders of publicly traded companies are required to be transparent with their trading activity. No later than two business days following a transaction — buying or selling shares of their company, or exercising options — insiders are required to file Form 4 with the Securities and Exchange Commission. These filings tell quite the tale with these two high-flying AI stocks.

Over the trailing five-year period, net-selling activity by insiders is as follows:

Nvidia: $5.342 billion in net selling of shares

Palantir: $7.178 billion in net selling of shares

In other words, insiders at the two hottest stocks in the AI arena have, collectively, sold $12.5 billion more of their own company’s stock than has been purchased since Oct. 16, 2020.

The stipulation to this publicly reported data is that most executive and board members at public companies receive their compensation in the form of common stock and/or options. To cover the federal and/or state tax liability tied to their compensation, company insiders often sell stock. In short, there are viable reasons for insiders to head for the exit that aren’t necessarily bad news.

What may be even more telling with Nvidia and Palantir Technologies is the complete lack of insider buying we’ve witnessed. The last time an Nvidia executive or board member purchased stock, based on Form 4 filings, was in early December 2020. Meanwhile, there’s been just one purchase by an executive or board member for Palantir since the company went public in late September 2020.

Neither Nvidia nor Palantir Technologies are inexpensive stocks, based on their price-to-sales (P/S) ratios. Over the trailing-12-month period, Nvidia and Palantir are valued at P/S ratios of 27 and 131, respectively. History tells us both figures aren’t sustainable over an extended period.

If no insiders from either company are willing to buy shares of their own stock, why should everyday investors?

Quantum computing is the latest technology hype cycle.

With shares up by a jaw-dropping 5,100% over the last 12 months, Rigetti Computing(RGTI -3.01%) exemplifies the life-changing potential of stock investing. If you bought $10,000 worth of shares of this speculative tech company last October, your position would now be worth over half a million dollars.

After a rise of that magnitude, potential new investors must be left wondering if they should jump on Rigetti’s hype train or wait for a dip. Let’s dig into the company’s fundamentals to decide what the near future might bring.

Is quantum computing ready for prime time?

Quantum computing promises to radically expand the reach of digital technology. When it works accurately, it can solve certain types of unusual, but extraordinarily difficult, problems that would take even a classical supercomputer an impossible amount of time. And while the technology has seemed “just around the corner” for decades, some recent breakthroughs have ignited optimism.

For example, one of the chief challenges in developing a useful quantum computer is that they are vastly more prone to errors than classical machines. But late last year, Alphabet subsidiary Google revealed its Willow chip, a state-of-the-art quantum computing chip that does a progressively better job of correcting its own mistakes the more computing power it uses. Perhaps more remarkably, on one of the benchmark computational problems that is used to test the abilities of quantum machines, Willow delivered the answer in about five minutes. For a traditional supercomputer to solve it would have taken 10 septillion years.

If they can be made reliable and cost effective enough to commercialize, such machines could drive revolutionary advances in areas ranging from drug discovery to material science. Quantum computers could also play a role in artificial intelligence by assisting with model training and optimization, which involves finding the most efficient use of resources to achieve a task.

Where does Rigetti fit in?

While Google looks like the leader in quantum computing technology, a rising tide lifts all boats, and investors are pouring capital into the entire industry. Rigetti’s compelling business model has also likely played a role in its explosive rally.

Rigetti takes a comprehensive picks-and-shovels approach to the quantum computing industry. It designs and builds its own chips, called quantum processing units (QPUs), at its California-based foundry. And it created its own programming language called Quil alongside a platform called Quantum Cloud Services (QCS), which is designed to allow clients to access its quantum processing power through the cloud.

The company is in the early stages of commercialization: It recently announced a $5.7 million purchase order for two of its Novera quantum computing systems, which it expects to deliver in 2026. But while these deals are a good sign, investors shouldn’t expect those purchases to necessarily mark the start of mass quantum computing adoption or sustainable growth.

While nonprofit research institutions and early adopters will continue to experiment with quantum computing, analysts at McKinsey and Company believe scalable quantum devices might not be commercially viable before 2040 at the earliest. In the meantime, Rigetti’s financial condition is alarming.

Massive cash burn

Image source: Getty Images.

For better or worse, public companies exist to generate profits for their shareholders. Technological prowess comes second, and arguably doesn’t matter at all if it doesn’t eventually benefit the bottom line. Rigetti’s shareholders may soon have to reckon with this fact.

In the second quarter, its operating losses grew 24% year over year to $19.8 million (compared to revenue of $1.8 million). Meanwhile, the number of shares outstanding jumped by 74% to almost 300 million. Rigetti is still sitting on a mountain of cash from a $350 million stock offering in June. But that money won’t last forever, and investors should expect the company to continue relying on equity financing to fund operations until it can achieve profitability.

With viable quantum computers potentially over a decade away, Rigetti’s management team will likely need to substantially dilute the positions of current shareholders in their efforts to get the company across the finish line. Yet even with this in mind, it’s not too late to buy the stock. If anything, it’s too early. But it may make sense to wait for a correction or another technological breakthrough before you consider opening a position in the stock.

Will Ebiefung has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet. The Motley Fool has a disclosure policy.

This dividend stock won’t excite you, but it will provide you and your descendants with a lofty 5.4% yield and reliable dividend growth over time.

The American dream is something like owning your own home, living comfortably, and seeing your children live happy and productive lives. That dream is even better if you can pass on your wealth to your children, which is basically what’s called generational wealth.

What if you don’t just pass on some money but instead pass on a reliable income stream? That’s what Realty Income(O 1.13%) could let you do. Here’s what you need to know about this unstoppable dividend stock.

The big number is, currently, 30

What does an unstoppable dividend stock look like? That’s pretty easy. It’s a company that manages to increase its dividend every year for decades on end. Real estate investment trust (REIT) Realty Income’s dividend streak is up to 30 years and counting at this point.

Image source: Getty Images.

What’s notable about that streak is that it includes some of the worst economic periods of recent history. And some of the worst bear markets. Realty Income’s dividend grew through the Dot.com crash, the Great Recession (and associated bear market) between 2007 and 2009, and the COVID-19 pandemic. What’s notable is that the Great Recession was particularly difficult for the real estate sector, and the pandemic was devastating to retailers, which make up over 70% of Realty Income’s tenants.

Basically, Realty Income has proven that it has what it takes to survive over the long term while continuing to reward investors with a progressive dividend. But that’s not all. It also happens to have an investment-grade-rated balance sheet, so it is financially strong. And it is geographically diversified, with properties in both the U.S. market and across Europe. While the portfolio is tilted toward retail properties, they tend to be easy to buy, sell, and release if needed. The rest of the portfolio, meanwhile, adds some diversification. All in all, it is a well structured REIT.

Plenty of generational opportunity ahead

The big draw for Realty Income is going to be the dividend yield, which sits at 5.4% or so. That’s well above the 1.2% the S&P 500 index is offering today and the 3.8% or so yield of the average REIT. But, as highlighted above, this isn’t exactly a high-risk investment. Why is the yield so high?

The answer is that Realty Income is a boring, slow-growth business. Over the three decades of dividend growth, the dividend has increased at a compound annual rate of 4.2%. That’s above the historical growth rate of inflation, so the buying power of the dividend has increased over time. But all in all, this is not an exciting stock to own and, frankly, isn’t meant to be. The company trademarked the nickname “The Monthly Dividend Company” for a reason: The REIT’s goal is specifically to be a reliable dividend stock.

There’s no reason to believe it will be anything but reliable in the future. Notably, it is the largest net-lease REIT, giving it an edge on its competitors when it comes to costs and deal making. Management has also been diversifying the business with the goal of increasing the number of levers it has to pull to support its slow and steady growth. None of its efforts involve undue risk, either. Slow and steady is the goal, but so far that’s worked out very well for dividend investors.

A simple and generational proposition

What you are getting when you buy Realty Income is a boring dividend stock that will pay you well to own it. And when the time comes, you can pass that income stream on to the next generation. Building generational wealth is a great thing, but just handing on a pile of money isn’t the only way to do it.

Imagine living a comfortable retirement with the monthly dividends you collect from Realty Income. And while you do that, you can think about how much easier the lives of your children will be when they collect that income instead of you.

IonQ has outperformed Nvidia since the start of the AI arms race.

Nvidia(NVDA 0.86%) has been one of the most successful stocks in the artificial intelligence (AI) arms race, rising 1,130% since it began at the start of 2023. This has delivered long-term investors phenomenal returns, but there’s a new, exciting investment trend in town that could disrupt how investors view Nvidia’s success.

Quantum computing is one of the most popular industries to invest in, and its stocks have surged over the past few months as investor sentiment surrounding the industry has improved. One of the most popular options is IonQ(IONQ -3.92%), which is no stranger to success. If you’d invested in IonQ instead of Nvidia at the start of 2023, you’d be up 2,150% (at the time of this writing)!

That may have some investors thinking they’ve backed the wrong horse in the computing race. So, is it time to move on from Nvidia and scoop up shares of IonQ? Let’s find out.

Image source: Getty Images.

Nvidia and IonQ are similar businesses

At their core, Nvidia and IonQ are quite close in terms of business pursuit. Nvidia makes graphics processing units (GPUs) alongside other equipment to optimize their performance. GPUs have become the gold standard in high-performance computing applications such as artificial intelligence, drug discovery, engineering simulations, and cryptocurrency mining. Their unique ability to process multiple calculations in parallel makes them a computing powerhouse, and AI hyperscalers have widely deployed them to train and run generative AI models.

IonQ appears to be a much earlier version of Nvidia, focusing on quantum computing rather than traditional computing methods. It’s developing a full-stack solution that provides clients with everything they need to run a quantum computer. Once quantum computing becomes mainstream, many believe it can have widespread use cases in applications like AI training and logistics network improvements. This could lead to a massive market opportunity, similar to what Nvidia experienced at the start of the AI arms race.

However, we’re still a ways away from quantum computing becoming relevant. IonQ and many other quantum computing companies point toward 2030 as the year when quantum computing will become a commercially viable technology. That’s five years out, and there’s still a lot of time for things to go wrong for IonQ (or go right).

IonQ competitor Rigetti Computing estimates that the annual value for quantum computing providers will reach $15 billion to $30 billion between 2030 and 2040. Should IonQ replicate Nvidia’s success by 2030, it could still have room to grow between now and then.

If we assume that the market reaches $15 billion annually in 2030 and IonQ replicates Nvidia’s dominant 90% market share and 50% profit margin, IonQ would be producing profits of $6.75 billion. At a 40 times earnings valuation, that would indicate IonQ could be a $270 billion company, more than a 10x from today’s $23 billion valuation.

But is that enough to warrant selling Nvidia shares to invest in IonQ?

Nvidia has a growth trend of its own

Over the next few years, capital expenditures relating to AI data centers are set to explode. Nvidia estimates that total capital expenditures in 2025 will total $600 billion, but reach $3 trillion to $4 trillion by 2030. If that plays out like Nvidia projects, the total amount of money spent on data center capital expenditures will rise at a compound annual growth rate of 42%. If Nvidia’s growth directly follows that trajectory, that means its stock could rise nearly 6 times in value.

So, which is more likely: Quantum computing becomes viable, IonQ establishes a dominant, Nvidia-like market share and achieves incredibly high margins, or Nvidia’s growth follows widely accepted AI spending trends? I think it’s more likely that the AI arms race continues in its current form, making holding on to Nvidia shares a smart decision. After all of the quantum computing investment hype, I think it’s time for investors to take a break from this sector and focus on some companies that have actual money flowing into them, rather than quantum computing-specific businesses like IonQ.

According to a filing with the Securities and Exchange Commission dated October 17, 2025, investment management company Capricorn Fund Managers Ltd established a new position in Waystar(WAY 0.46%), acquiring 505,122 shares. The estimated transaction value, based on the average closing price during the third quarter of 2025, was approximately $19.15 million. This addition brings the fund’s total reported positions to 59 at quarter-end.

What else to know

The new position in Waystar accounts for 6.4% of Capricorn Fund Managers’ 13F reportable assets under management. The stock is now the fund’s largest holding by reported market value.

The fund’s top holdings after the filing are:

WAY: $19.15 million (6.4% of AUM)

TARS: $14.26 million (4.8% of AUM)

MSFT: $14.15 million (4.8% of AUM)

VERA: $13.10 million (4.4% of AUM)

REAL: $12.64 million (4.2% of AUM)

As of October 16, 2025, shares of Waystar were priced at $36.81, up 34% over the one-year period, outperforming the S&P 500 by 20 percentage points during the same timeframe.

Company overview

Metric

Value

Price (as of market close October 16, 2025)

$36.81

Market capitalization

$7.06 billion

Revenue (TTM)

$1.01 billion

Net income (TTM)

$85.94 million

Company snapshot

Waystar provides a cloud-based software platform for healthcare payments, including solutions for financial clearance, patient financial care, claims and payment management, denial prevention and recovery, revenue capture, and analytics.

IMAGE SOURCE: GETTY IMAGES.

The company serves healthcare organizations as its primary customers, targeting providers seeking to optimize revenue cycle management and payment processes.

Waystar was founded in 2017 and is headquartered in Lehi, Utah, working in the technology sector with approximately 1,500 employees. The company operates at scale in the healthcare technology industry, focusing on streamlining payment processes for healthcare providers through its cloud-based platform.

Foolish take

Capricorn Fund Managers’ new position in Waystar stock merits attention for a few reasons. The investment management company not only deemed Waystar a valuable addition to its portfolio, but the purchase was so big, the stock catapulted to the top of its holdings.

Investing in Waystar makes sense. The business boasts some compelling qualities. It has grown revenue every quarter for the past two years, and the trend continues in 2025.

In Q2, Waystar’s sales rose 15% year over year to $270.7 million. The company expects to hit $1 billion in revenue this year, up from $944 million in 2024.

Waystar also had a solid balance sheet exiting Q2. Total assets were $4.7 billion compared to total liabilities of $1.5 billion. It does have over $1 billion in debt, but the company is slowly paying this down.

The consistent sales growth Waystar is experiencing, and its forward price-to-earnings ratio of about 25, which is reasonable for a fast-growing tech company, explains Capricorn Fund Managers’ big buy of Waystar stock. These factors make the stock a worthwhile investment for the long haul.

Glossary

13F reportable assets under management: The total value of securities a fund must disclose quarterly to the Securities and Exchange Commission (SEC) on Form 13F.

Stake: The ownership interest or investment a fund or individual holds in a company.

Initiated position: When an investor or fund purchases shares of a company for the first time.

Assets under management (AUM): The total market value of investments managed by a fund or investment firm.

Quarter-end: The last day of a fiscal quarter, used for financial reporting and portfolio snapshots.

Outperforming: Achieving a higher return or growth rate compared to a benchmark or index.

Cloud-based platform: Software and services delivered over the internet rather than installed locally on computers.

Revenue cycle management: The process healthcare providers use to track patient care revenue from appointment to final payment.

Denial prevention and recovery: Strategies to reduce and resolve rejected insurance claims in healthcare billing.

Market value: The current worth of an asset or holding based on the latest market price.

Healthcare payments: Financial transactions related to medical services, including billing, claims, and reimbursements.

TTM: The 12-month period ending with the most recent quarterly report.

Robert Izquierdo has positions in Microsoft. The Motley Fool has positions in and recommends Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Florida-based wealth advisory J. L. Bainbridge disclosed a purchase of Eli Lilly and Company valued at approximately $45.6 million for the quarter ended September 30, according to an SEC filing released on Friday.

What Happened

J. L. Bainbridge & Co. Inc. significantly increased its stake in Eli Lilly and Company(LLY -1.94%), acquiring 61,258 additional shares during the quarter. The estimated value of the purchase was $45.6 million based on the average closing price for the quarter. The position was reported in the firm’s quarterly Form 13-F filing with the Securities and Exchange Commission on Friday.

What Else to Know

This buy brings the position to 3.9% of J. L. Bainbridge & Co. Inc.’s 13F reportable assets.

Top holdings after the filing:

NASDAQ:MSFT: $164.85 million (13.9% of AUM)

NASDAQ:AAPL: $122.68 million (10.4% of AUM)

NASDAQ:GOOGL: $116.65 million (9.9% of AUM)

NYSE:GS: $71.43 million (6% of AUM)

NYSE:ETN: $59.86 million (5.1% of AUM)

As of Friday’s market close, shares of Eli Lilly and Company were priced at $802.83, down 11% over the past year and far underperforming the S&P 500’s nearly 14% gain over the same period.

Company Overview

Metric

Value

Price (as of market close Friday)

$802.83

Market Capitalization

$759.8 billion

Revenue (TTM)

$53.3 billion

Net Income (TTM)

$13.8 billion

Company Snapshot

Eli Lilly offers a broad portfolio of pharmaceuticals for diabetes, oncology, immunology, neuroscience, and other therapeutic areas, with leading products including Humalog, Trulicity, Jardiance, Verzenio, and Taltz.

The company generates revenue primarily through the discovery, development, manufacturing, and global sale of branded prescription drugs, leveraging both proprietary research and strategic collaborations.

It provides pharmaceuticals for chronic and complex diseases worldwide.

Eli Lilly and Company is a global pharmaceutical leader that maintains a diversified portfolio of innovative therapies for high-burden diseases. Its scale, established brands, and strategic partnerships provide competitive advantages in the rapidly evolving healthcare sector.

Foolish Take

Florida-based J.L. Bainbridge & Co. boosted its exposure to Eli Lilly last quarter, purchasing roughly $45.6 million worth of shares even as the stock has endured a difficult stretch. Shares are down 11% over the past year, pressured by valuation concerns and, most recently, political commentary on potential weight-loss drug price cuts. The decline followed remarks by President Donald Trump, who suggested GLP-1 treatments like Lilly’s Mounjaro and Zepbound could face price reductions—a move that briefly sent shares tumbling more than 4% on Friday.

Despite near-term volatility, Bainbridge’s purchase reflects long-term conviction in Lilly’s fundamentals. The pharmaceutical giant remains a dominant player in metabolic and diabetes care, with GLP-1 demand still far outpacing supply. Analysts at BMO Capital Markets called the recent selloff “overdone,” noting that most insured Americans already pay modest out-of-pocket costs for these drugs.

For Bainbridge, whose portfolio is anchored by Microsoft, Apple, and Alphabet, the addition of Lilly underscores a strategy centered on durable growth and innovation-led healthcare exposure. Long-term investors may see current weakness as a potential entry point into one of the most profitable franchises in global pharmaceuticals.

Glossary

Form 13-F: A quarterly SEC filing by institutional investment managers disclosing their equity holdings. AUM (Assets Under Management): The total market value of investments managed on behalf of clients by a fund or firm. Reportable AUM: Portion of a fund’s assets that must be disclosed in regulatory filings, such as the Form 13-F. Top holdings: The largest investments in a fund, ranked by their value as a percentage of total assets. Trailing twelve months (TTM): The 12-month period ending with the most recent quarterly report. Stake: The ownership interest or position an investor holds in a company, usually measured in shares or percentage. Strategic collaborations: Partnerships between companies to jointly develop, market, or distribute products or services. Pharmaceutical portfolio: The collection of drugs and therapies a company develops, manufactures, and sells. Underperforming: Delivering a lower return or performance compared to a benchmark or peer group.

Florida-based wealth advisory J. L. Bainbridge & Co. sold 119,376 shares of Biogen(BIIB 0.58%) during the third quarter for an estimated $16.1 million.

What Happened

In a quarterly disclosure filed with the Securities and Exchange Commission on Friday, J. L. Bainbridge & Co. Inc. reported selling 119,376 shares of Biogen (BIIB 0.58%) during the third quarter. The estimated value of the shares sold was $16.1 million, based on the average closing price for the period. The fund now holds just 2,969 shares of Biogen valued at $415,898 as of September 30.

What Else to Know

The sale reduced Biogen to 0.03% of reported U.S. equity assets under management as of September 30.

Top holdings after the filing:

NASDAQ:MSFT: $164.85 million (13.9% of AUM)

NASDAQ:AAPL: $122.68 million (10.4% of AUM)

NASDAQ:GOOGL: $116.65 million (9.9% of AUM)

NYSE:GS: $71.43 million (6% of AUM)

NYSE:ETN: $59.86 million (5.1% of AUM)

As of Friday’s market close, shares of Biogen were priced at $143, down 23% over the past year.

Company Overview

Metric

Value

Price (as of market close on Friday)

$143.00

Market Capitalization

$21 billion

Revenue (TTM)

$10 billion

Net Income (TTM)

$1.5 billion

Company Snapshot

Biogen’s portfolio includes therapies for neurological and neurodegenerative diseases, such as multiple sclerosis, spinal muscular atrophy, Alzheimer’s disease, and biosimilars targeting autoimmune disorders.

The company generates revenue through the discovery, development, manufacturing, and commercialization of branded pharmaceuticals and biosimilars, with a focus on specialty and rare disease markets.

Biogen serves a global customer base, including healthcare providers, hospitals, and specialty pharmacies treating patients with neurological and rare diseases.

Biogen specializes in therapies for complex neurological and neurodegenerative conditions. With a diversified product suite and a robust pipeline, Biogen leverages scientific innovation and strategic collaborations to maintain its position in high-need therapeutic areas.

Foolish Take

Florida-based J.L. Bainbridge & Co. dramatically scaled back its Biogen holdings last quarter, selling nearly its entire position for roughly $16 million. The firm, known for its long-term focus and balanced growth strategy, now holds only about $416,000 worth of Biogen stock—just 0.03% of its reportable U.S. equity assets.

The timing aligns with Biogen’s mixed performance over the past year. Shares are down 23%, despite a strong second-quarter report showing 7% year-over-year revenue growth to $2.6 billion and raised full-year guidance. The company highlighted sequential growth in Alzheimer’s therapy LEQEMBI, rare-disease drug SKYCLARYS, and postpartum-depression treatment ZURZUVAE, with CEO Christopher Viehbacher calling it “another quarter of strong execution” as Biogen reshapes its portfolio for sustainable growth. Still, the stock has struggled amid investor skepticism fueled by declining sales.

Bainbridge’s near-exit follows other portfolio adjustments—such as trims to Delta Air Lines—as the firm concentrates its holdings in proven large-cap growth names like Microsoft, Apple, and Alphabet. For long-term investors, Biogen’s upcoming October 30 earnings will be a key moment to gauge whether its new drug launches can meaningfully offset the erosion of its older franchises.

Glossary

AUM (Assets Under Management): The total market value of assets a fund or investment manager oversees on behalf of clients. Quarterly disclosure: A report filed every three months detailing a fund’s holdings, transactions, and other relevant financial information. Post-trade stake: The number of shares or percentage of ownership remaining after a buy or sell transaction. Top holdings: The largest investments in a fund’s portfolio, usually ranked by market value or portfolio percentage. Biosimilars: Biologic medical products highly similar to already approved reference drugs, used to treat various diseases. Specialty and rare disease markets: Healthcare sectors focused on developing treatments for uncommon or complex medical conditions. Pipeline: The portfolio of drugs or products a company is developing, from early research to late-stage clinical trials. Strategic collaborations: Partnerships between companies to jointly develop, market, or distribute products or technologies. TTM: The 12-month period ending with the most recent quarterly report.

Jonathan Ponciano has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Apple, Goldman Sachs Group, and Microsoft. The Motley Fool recommends Biogen and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

It has been an up and down year for Warren Buffett’s portfolio. Many of his biggest positions have been trimmed aggressively. But according to recent filings, his holding company, Berkshire Hathaway, is loading up on one of Buffett’s favorite stocks. Last quarter, it boosted its position by more than $500 million.

On paper, this stock has it all. It’s priced at a discount to the market, offers a compelling dividend yield, and could generate impressive growth over the next few years.

This has been one of Warren Buffett’s favorite stocks since 2020

Berkshire Hathaway first took a position in Chevron(CVX 0.94%) back in 2020, not long after the nadir of the COVID-19 flash crash. Buffett’s estimated purchase price was around $80. But over the years, he has managed the position aggressively. In early 2021, for instance, just one year after his initial purchase, Buffett slashed his Chevron stake by more than 50%. Towards the end of 2021, however, he began rebuilding his position. Several more purchases and sales occurred in 2022, including the massive acquisition of 121 million shares in the first quarter.

Notably, Berkshire has been a net seller in recent quarters. In six of the past seven quarters, for example, Berkshire has sold more Chevron stock than it purchased. But that all changed this quarter when Buffett purchased nearly 3.5 million shares worth roughly $520 million. It was one of the biggest stock purchases of the quarter for Buffett, giving Berkshire a 7% stake in the entire business.

Why did Buffett load up on this giant oil stock that he knows so well? The numbers below paint a compelling picture.

Chevron stock looks very attractive for certain investors

After several consecutive winning years, the stock market as a whole isn’t obviously a value right now. The S&P 500, for example, trades at 31 times earnings — well above its long-term average. Chevron stock, meanwhile, trades at just 19 times earnings. Revenue growth is stagnant right now, but free cash flow remains high, helping to support a 4.5% dividend yield.

Part of the challenge with Chevron stock right now isn’t under its direct control. Oil prices slid heavily this year, falling under $60 per barrel. Oil inventories continue to rise, with meaningful surpluses expected in 2026 due to rising production globally. In total, it’s a tough place to be for businesses that sell oil.

As an integrated producer, with interests in refining, chemical production, and even energy generation for artificial intelligence applications, Chevron has long been able to manage industry cyclicality with ease. Chevron’s CEO focuses on cost controls and capital efficiency to ensure profits remain stabilized even with low oil prices. But unless those oil prices move higher, expect so-so results from Chevron — a big reason why shares have traded sideways since 2022.

Here’s the thing: Chevron stock is still a very compelling purchase for certain investors. If you’re finding it difficult to find market values, are worried about a potential bear market, or believe geopolitical tensions are about to rise, allowing oil prices to recover quickly, Chevron shares could be a fit. While shares aren’t a steal, they are arguably fairly valued at 19 times earnings. The dividend yield and free cash flow consistency, meanwhile, can help offset losses during a market downturn. And given ongoing geopolitical disputes, it’s not unreasonable to expect sudden shifts in oil demand and supply.

All in all, this looks like a classic move for Buffett in this market environment. He understands Chevron’s business model well, and with a rising cash hoard, it’s clear that he’s finding it difficult to spot market bargains. Chevron is as close to a value stock in today’s environment as it gets.

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway and Chevron. The Motley Fool has a disclosure policy.

On October 17, 2025, Sapient Capital LLC disclosed a purchase of 259,392 Eli Lilly and Company(LLY -1.94%) shares, for a total transaction value of $193,028,908.

What Happened

Sapient Capital LLC increased its stake in Eli Lilly and Company by 259,392 shares during Q3 2025, according to a U.S. Securities and Exchange Commission (SEC) filing dated October 17, 2025 (SEC filing). The estimated transaction value was $193.03 million, based on the average closing price for Q3 2025. The fund now holds 1,477,879 shares worth $1.07 billion in Q3 2025.

What Else to Know

Buy activity increased the position to 16.53% of Sapient Capital’s 13F AUM in Q3 2025

Top holdings after the filing:

LLY: $1.07 billion (16.5% of AUM) as of September 30, 2025

APP: $906.45 million (14.0% of AUM) as of September 30, 2025

AAPL: $346.81 million (5.3% of AUM) as of September 30, 2025

MSFT: $313.49 million (4.8% of AUM) as of September 30, 2025

GOOGL: $238.99 million (3.7% of AUM) as of September 30, 2025

As of October 17, 2025, shares were priced at $802.83, down 12.46% over the past year; shares have underperformed the S&P 500 by 25.79 percentage points

Company Overview

Metric

Value

Price (as of market close 2025-10-17)

$802.83

Market Capitalization

$722.03 billion

Revenue (TTM)

$53.26 billion

Net Income (TTM)

$13.80 billion

Company Snapshot

Eli Lilly and Company is a global pharmaceutical leader with a market capitalization of $722.03 billion as of October 17, 2025 and a diversified portfolio of innovative therapies. The company’s strategy centers on advancing high-impact medicines and expanding its reach through scientific innovation and partnerships. Its scale and established presence in key therapeutic areas provide advantages in the healthcare sector.

The company offers a broad portfolio of pharmaceuticals for diabetes, oncology, immunology, neuroscience, and other therapeutic areas, with leading products such as Trulicity, Humalog, Jardiance, and Taltz. It generates revenue primarily through the discovery, development, and global commercialization of branded prescription medicines, leveraging internal R&D and strategic collaborations. It treats patients with chronic and complex health conditions.

Foolish Take

This recent transaction by Sapient Capital, a private wealth advisor, is a notable institutional purchase. Here’s why.

First off, Sapient acquired over 259,000 shares of Eli Lilly, worth around $193 million. That is, of course, a great deal of money. But beyond that, the transaction makes the stock Sapient’s largest overall holding, with about $1.07 billion worth of Eli Lilly stock. In other words, Sapient is significantly increasing its already enormous stake Eli Lilly stock. That demonstrates the fund managers have a great deal of conviction that Eli Lilly stock should perform well.

Average investors may want to take note of this, particularly given Eli Lilly’s recent underperformance against major market indexes like the S&P 500. For example, Eli Lilly stock has lagged the S&P 500 year-to-date. Indeed, it has generated a total return of around 5% in 2025, while the benchmark index has generated a total return of 14%.

One potential headwind for Eli Lilly may be political pressure from Washington. President Donald Trump recently said that his administration will work to cut the cost of brand-name GLP-1s, like Eli Lilly’s Zepbound, to $150 per month — a significant decrease from the rate Eli Lilly currently offers on their direct-to-consumer site. That could cut into the company’s profits which have skyrocketed from $5 billion to nearly $14 billion thanks in part to the introduction of Zepbound in 2023.

In summary, investment advisor Sapient has made a huge bet on Eli Lilly stock, boosting its stake by ~25% and making the stock its top holding. The company’s shares have underperformed this year, and pressure from Washington is increasing for the company to lower the price of its star drug, Zepbound, which could stifle its overall profitability. All in all, it’s a mixed picture for Eli Lilly with significant uncertainty surrounding at least one of its key products.

Glossary

13F assets under management (AUM): The value of securities a fund manager reports to the SEC on Form 13F, typically U.S.-listed equities. Position: The amount of a particular security or asset held by an investor or fund. Trailing twelve months (TTM): The 12-month period ending with the most recent quarterly report. Dividend yield: Annual dividends per share divided by the share price, shown as a percentage. Forward price-to-earnings ratio: A valuation metric comparing a company’s current share price to its expected future earnings per share. Enterprise value to EBITDA: A valuation ratio comparing a company’s total value (enterprise value) to its earnings before interest, taxes, depreciation, and amortization. Stake: The ownership interest or share held by an investor in a company. Holding: A security or asset owned by an investor or fund. Buy activity: The act of purchasing additional shares or assets, increasing an investor’s or fund’s position. Therapeutic areas: Specific categories of diseases or medical conditions targeted by pharmaceutical products. Strategic collaborations: Partnerships between companies to achieve shared business or research goals.

Jake Lerch has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

This Nvidia competitor has just won a big contract.

Nvidia has been the dominant force in the global semiconductor industry thanks to its graphics processing units (GPUs), which have played a critical role in enabling the proliferation of artificial intelligence (AI) applications. The demand for Nvidia’s GPUs has been so solid in the past three years that Nvidia has now become the world’s largest company.

Nvidia continues to rule the AI data center GPU market, facing very little threat from its peers so far. Analysts are expecting its top line to jump by an impressive 58% in the current fiscal year to more than $206 billion. That’s quite impressive for a company of Nvidia’s size. The stock registered respectable gains of 34% on the market this year based on the healthy growth that the company continues to deliver.

However, Nvidia’s stock market performance has been overshadowed by Broadcom(AVGO -1.24%). Broadcom has appreciated 48% this year and looks set to end 2025 on a high note following recent developments. In fact, it won’t be surprising to see Broadcom stock outperforming Nvidia next year as well. Let’s see why that may be the case.

Image source: Nvidia.

Custom AI chips are expected to witness stronger demand in 2026

So far, the majority of AI model training and inference has been carried out by Nvidia’s GPUs. GPUs are general-purpose computing chips with massive parallel computing power, making them ideal for quickly training AI models and moving them into production. OpenAI chose Nvidia’s A100 data center GPUs to train its popular chatbot ChatGPT three years ago.

Nvidia built upon its first-mover advantage and controlled an estimated 92% of the AI data center GPU market at the end of last year. However, the latest deal struck between OpenAI and Broadcom indicates that Nvidia’s influence over the AI chip market could wane. OpenAI will buy custom AI accelerators worth a whopping 10 gigawatts (GW) from Broadcom starting in the second half of 2026.

The deployment is expected to be completed by the end of 2029. This is a massive deal for Broadcom considering that it reportedly costs around $10 billion to build a 1 GW data center. Around 60% of the investment that goes into building a data center is allocated toward chips and other computing hardware, which would put Broadcom’s potential addressable market from each gigawatt of OpenAI’s deployment at $6 billion.

So, Broadcom could be sitting on a potential revenue opportunity worth $60 billion from this deal over the next three years. Broadcom’s custom AI processors have already been in terrific demand as hyperscalers and AI giants such as OpenAI are gravitating toward these chips because of the advantages they enjoy over GPUs.

Custom AI processors are designed for performing targeted tasks, such as AI inference. As a result, they are not only more power-efficient at running those workloads but also enjoy a performance advantage since they don’t need to perform any other tasks. Hence, deploying custom AI processors can help save costs for hyperscalers.

Shipments of application-specific integrated circuits (ASICs) meant for deployment in AI data centers are expected to increase by 45% in 2026, compared to the expected growth of 16% in GPUs. Broadcom is in the best position to make the most of this growth opportunity as it leads the ASIC market with an estimated share of 70%.

Moreover, the new deal with OpenAI along with another $10 billion contract with an unnamed customer that the company announced last month should ensure outstanding growth in Broadcom’s AI revenue next year.

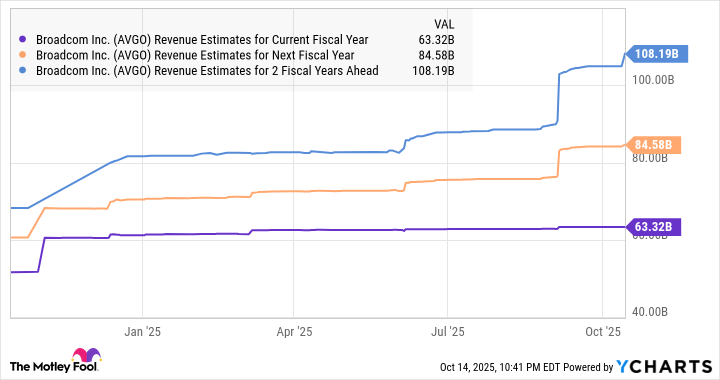

Broadcom’s AI revenue could now increase at a faster pace

Broadcom is on track to end the current fiscal year with almost $20 billion in AI revenue, an increase of 64% from the previous year. The company reported a record revenue backlog of $110 billion at the end of the fiscal third quarter (which ended on Aug. 3). That backlog is likely to have moved higher following the recent deals struck by the company.

Don’t be surprised to see Broadcom’s revenue jumping at a faster pace than the 33% growth that Wall Street is expecting next fiscal year, which would be a nice improvement over the 23% growth it is expected to deliver in the current one. There is a good chance that its revenue growth in the long run could be better than expectations as well.

Broadcom was already anticipating a serviceable addressable market worth $60 billion to $90 billion based on the three AI customers it was serving until earlier this year. That addressable market is now much bigger following the OpenAI contract, which opens up the possibility of stronger growth and more upside for Broadcom investors.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Retirees are getting a Social Security raise in 2026. How will it compare to the benefits bump they got in 2025?

In most years, Social Security retirees receive a cost-of-living adjustment (COLA), and that’s likely to happen in 2026. COLAs are critical because without them, benefits would remain unchanged while the price of goods and services increase over time. Retirees would be left with far less buying power, and many would struggle to make ends meet since Social Security is an important income source for seniors.

COLAs aren’t the same from one year to the next, though. While the 2026 COLA hasn’t been announced, there are good estimates of what it’s going to be. Based on the existing data, it looks like the amount of the benefits increase is going to be different from the raise retirees got in 2025.

Here’s what next year’s COLA is likely to be, compared with the benefits bump you got in 2025.

Image source: The Motley Fool.

How will next year’s Social Security COLA compare?

The 2026 COLA will officially be announced on Friday, Oct. 24, 2025. The Senior Citizens League estimates the cost-of-living adjustment will result in a 2.7% benefits increase.

A 2.7% increase would be a bit larger than the raise retirees got in 2025, when benefits rose 2.5%. However, it will be smaller than COLAs from recent memory, including the 3.2% benefit increase in 2024, the 8.7% raise in 2023, and the 5.9% COLA in 2022.

Unfortunately, while the COLA is on track to be larger in 2026 than in 2025, retirees may not see the full 2.7% increase in their payment because Medicare premiums are going to be rising as well — and by much more than they did in 2025.

In 2025, the standard premium for Medicare Part B rose $10.30, jumping from $174.70 in 2024 to $185.00 in 2025. In 2026, projections from the Medicare Board of Trustees suggest that Part B premiums will go up $21.50, from the current $185.00 all the way up to $206.50. This is one of the biggest year-over-year increases in the history of the program.

Unfortunately, since most people have Medicare premiums taken directly out of their Social Security checks, a good portion of the extra money that seniors get from the COLA will disappear.

For example, if someone had a $2,000 monthly benefit in 2024, this year’s 2.5% COLA would have given them around a $50 monthly raise, and they’d have lost $10.30 of it. Their check would have gone up by around $39.70.

Someone with a $2,000 check in 2025, on the other hand, could see their payments rise by 2.7% in 2026, or $54 per month. A $21.50 Medicare premium increase would leave them with only $32.50 extra each month.

This means the “bigger” benefits bump this year may be nothing but a mirage, and retirees could find themselves struggling to maintain buying power based on current levels of inflation.

Is a larger COLA good news or bad news?

The reality is, even aside from the Medicare issue, it isn’t good news that Social Security retirees are on track for a bigger COLA. That’s because cost-of-living adjustments are directly tied to a formula that measures how much the cost of goods and services is going up. A bigger raise means there are higher levels of inflation, and inflation generally isn’t good for older people on fixed incomes.

Many seniors also have money saved in retirement plans, and since people tend to be conservative with their investments during retirement, their returns may not outpace inflation by much when inflation is high.

For now, seniors will need to simply wait and see what the official COLA announcement brings on Oct. 24. The news will offer insight into what their finances will look like in the coming year, but retirees should prepare for potential disappointment, even if the COLA amount looks good on paper.

Quantum computing stocks have risen dramatically over the past few weeks.

Quantum computing stocks have been on an absolute tear recently as their companies announced major contract wins. But that was all topped off by JPMorgan Chase‘s announcement this week that it’s investing $10 billion into strategic tech companies. That includes quantum computing businesses. But for quantum computing stocks to rise around 20% (some more, some less) following that news is troublesome.

No specific investment was announced in any of these companies, and other massive industries were listed in the release — such as supply chain and advanced manufacturing, defense and aerospace, energy technology, and frontier and strategic technologies (where quantum computing was lumped in). This raises concerns about the short-term nature of the quantum computing market. The combined rise of all quantum computing stocks was more than the overall $10 billion investment announced by JPMorgan Chase, so there’s clearly not enough to go around.

Observers have begun to speculate that there may be a quantum computing bubble forming. So is now the time to sell? I think Warren Buffett has some great advice for investors on what they should do.

Image source: Getty Images.

Warren Buffett has seen a bubble or two in his career

Warren Buffett is the legendary CEO of Berkshire Hathaway, a position he has held since he took control of the company in 1965. Over the years, Buffett has given investors several great pieces of wisdom, and I think one quote is applicable right now. He wrote that his goal was to “attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

There are clearly many signs of greed in the quantum computing market. As mentioned above, many of the quantum computing stocks rose by a massive amount in response to a nonspecific announcement that JPMorgan Chase would invest in emerging technologies.

Furthermore, we’re still years away from quantum computing viability. Most competitors point toward 2030 as the likely turning point in quantum computing’s commercial relevance, and that’s still five years away. Five years ago, we were in the beginning stages of the COVID-19 pandemic, and nobody (outside of a handful of companies) had ever heard the term generative AI. It’s impossible to know what will happen in the field over the next five years, or which companies will be the winners.

Most of the investment dollars flowing into the quantum computing space have centered around the pure plays. Still, there are also legacy tech players, like Alphabet, Microsoft, and IBM, which have nearly unlimited resources compared to pure plays like IonQ(IONQ -3.92%) or Rigetti Computing(RGTI -3.01%). It’s still an uphill battle for IonQ and Rigetti, and just because the big tech players aren’t saying anything doesn’t mean they aren’t experiencing success.

Companies like IonQ and Rigetti Computing are still years away from profits, and have to rely on government contracts and stock issuance to continue to fund their operations. As a result, they must issue a news release on any piece of positive news they can to let investors know about their successes. The big tech companies like Alphabet, IBM, and Microsoft can afford to stay silent about any breakthroughs, as they’re internally funding their research.

The big tech players may be far more advanced than the pure plays, even if nobody outside of those companies knows it yet. I think this could be setting up some of the pure-play stocks for failure, and their shareholders should take action.

Taking some profits in an increasingly frothy industry is a smart move

Another Warren Buffett quote is applicable in this situation, too: “The first rule in investment is ‘Don’t lose.’ And the second rule in investment is ‘Don’t forget the first rule.'” Investors have already made a significant amount of money on the quantum computing trade, and while it’s possible these stocks could continue rising, a crash may be around the corner.

If you’ve invested in these stocks at any time this year, it may be time to at least trim some of them, as it’s unlikely that they’ll continue rising forever. By taking some profits now, you can be well positioned to deploy them back into the industry if it returns to earth.

Nobody ever lost money by selling a stock at a profit, although they have lost out on even larger returns. Still, I think the risk is greater than the reward, and it may be a wise time to take some profits off the table.

JPMorgan Chase is an advertising partner of Motley Fool Money. Keithen Drury has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Berkshire Hathaway, International Business Machines, JPMorgan Chase, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Investors looking for a low-risk stock with a great dividend have a good opportunity here.

Just across Long Island Sound from Long Island itself sits Purchase, NY, home of consumer-packaged goods giant PepsiCo(PEP 0.80%). The business began with a single beverage — Pepsi-Cola — in the small coastal town of New Bern, NC. But a bankruptcy saw the brand change hands, ultimately landing it with a business in New York, the state it’s still headquartered in today.

Since relocating to its current headquarters in Purchase, NY in 1970, PepsiCo has undergone a radical transformation. It’s an international powerhouse in the consumer-packaged goods space with dozens of beverage brands as well as food brands. And recent financial results underscore why this is still a solid stock to buy for the long term.

Image source: PepsiCo.

Pepsi’s rock-solid business

Pepsi stock is down about 23% from the all-time high it reached two years ago. Investors have soured on this stock because sales volume is under pressure. Investors consequently speculate that perhaps consumers are trading down to cheaper brands, that consumers are choosing healthier options, or that weight-loss drugs are suppressing appetites.

However, Pepsi is more resilient than investors give it credit for. On Oct. 9, the company reported financial results for its fiscal third quarter of 2025. Sales volume did decline by 1% for both beverages and convenient foods. And the decline was even more pronounced in North America. But the headline numbers didn’t tell the whole story.

Pepsi is actively reshaping its portfolio of beverage brands. One example is selling Rockstar Energy to Celsius. But another example is transitioning its case pack water business to a third-party partner. Changes such as these impact quarterly sales volume.

By simply adjusting results for the change to the water business, Pepsi’s beverage volumes in North America grew in Q3 — that’s a big deal. It suggest that the company is getting some positive traction in a core market with core products.

Sales in North America have been challenged for a while now. But Pepsi’s business was never in dire straights. This is because sales volume for food and beverages has continued rising in both Latin America and Asia.

This is the benefit of being a large, diversified business. Even if one part of Pepsi’s business is facing headwinds, chances are that other parts of the business are able to pick up the slack.

Is Pepsi stock a good long-term buy?

I believe that Pepsi stock is a good long-term buy, but I should clarify what I mean by that. I don’t believe that this will be among the top-10 stocks over the next decade or anywhere close to that. Those stocks will probably be up-and-coming businesses experiencing a lot of growth. And with over $90 billion in trailing-12-month revenue, it’s unrealistic to expect Pepsi’s business to be high growth.

But I believe Pepsi stock will make investors money over the long term with relatively little risk. Even if consumer tastes and preferences are shifting, the company operates a portfolio that it can adjust. As one example, Pepsi acquired prebiotic soda brand Poppi for nearly $2 billion, and it can use this new business to build more products that are aligned with trending preferences.

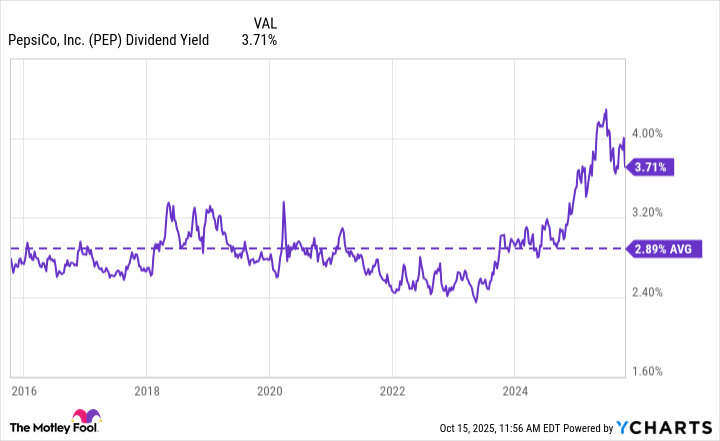

Moreover, Pepsi is a Dividend King, having paid and increased its dividend for 53 consecutive years now. This is a streak that it’s not going to give up on easily. And thanks to the pullback in the stock price, dividend investors can lock in at nearly an all-time high dividend yield, boosting returns from here.

Yes, Pepsi may be headquartered in New York. But this company is much more than the Pepsi brand, and it’s much bigger than the Empire State. It’s a profitable global business with a diversified portfolio that can adapt to changes in the consumer landscape.

Therefore, Pepsi stock is a solid long-term buy in my view and a good addition to a diversified portfolio of stocks.

Jon Quast has positions in Celsius. The Motley Fool has positions in and recommends Celsius. The Motley Fool has a disclosure policy.

Investors might have a hard time finding any negative qualities about this business.

Digital bank Nu Holdings(NU 2.00%) has a market capitalization of $72 billion — and that makes it a sizable business. However, many American investors might not know that much about the company because it operates in Latin America and has no U.S. presence.

Here’s a perfect example of why it’s important to understand that there are investment opportunities in international markets. This fintech stock might prove that point. Should you buy Nu Holdings while it’s trading below $16? Here’s why that might be a smart decision.

Image source: Getty Images.

Customer additions and revenue growth are through the roof

The market loves a good growth story — and Nu Holdings is exactly that. The company’s customer base went from 65 million at the end of Q2 2022 to 123 million as of June 30. In Nu’s home country of Brazil, the business counts 60% of the adult population as its customers. Newer markets of Mexico and Colombia are registering remarkable success, even though Nu’s penetration is still in the early stages in these countries.

Nu is benefiting from some notable tailwinds. It helps that internet and smartphone penetration in Latin America continue to grow. This provides a favorable backdrop for a digital-only bank like Nu to find broader adoption.

Essentially, Nu is riding the wave of the Latin American economy’s development. Given that a large portion of the population here is still unbanked or underbanked, Nu still has lots of potential for growth.

The company’s revenue increased 29% year over year in Q2. Wall Street consensus sell-side analyst estimates believe the top line will rise by 67% between 2025 and 2027. That outlook should make shareholders excited.

Nu’s focus on product innovation should help it reach more customers. Management has also hinted at entering new countries in the future, basically replicating strategies that have worked so well in its existing markets.

This is an extremely profitable enterprise

Companies that have access to cheap capital usually care about growth more than anything else when it comes to strategic priorities. That’s why over the past decade or so, some businesses have put up huge gains, adding customers and increasing sales rapidly. The issue, however, is that these companies don’t care about profits.

Nu bucks this trend and stands out. It’s an extremely profitable enterprise, which might be a surprise to many. Nu registered $1.2 billion in net income through the first six months of 2025. That translated to a phenomenal net profit margin of 17.4%. The margin has generally increased in recent years, which underscores the company’s ability to scale up in a lucrative manner.

Investors should pay attention to the unit economics. It cost the company $0.80 per month in Q2 to serve the average customer. But on the flip side, the average revenue per active customer came in at $12.20. After viewing these two figures, it makes sense why the leadership team is trying to grow so quickly.

Nu also has the advantage of not running any physical bank branches. A brick-and-mortar retail strategy like this would entail sizable operating expenses. Nu avoids this, which can help drive higher margins over time.

This fintech stock trades at a reasonable valuation

In the past three years, Nu’s shares have skyrocketed 262% (as of Oct. 16), thanks to incredible fundamental performs that has caught the market’s attention. After such a phenomenal gain, investors might be questioning the stock’s appeal. The last thing you’d want to do is overpay.

That’s certainly not the case here. The valuation still looks very compelling. Investors can buy the stock at a forward price-to-earnings ratio of 18.7. At under $16 per share, there is sizable upside over the next five years from the possibility of both higher earnings and valuation expansion.

Neil Patel has no position in any of the stocks mentioned. The Motley Fool recommends Nu Holdings. The Motley Fool has a disclosure policy.