Article content

Amazfit welcomes back Hunter McIntyre and expands its elite athlete team for the 2025/26 HYROX season with Rich Ryan, Joanna Wietrzyk, Emilie Dahmen, and Linda Meier

Following its cloud event last week, Wall Street analysts are raising their price targets on the stock.

Shares of Alibaba (BABA 4.26%) are rallying again today, up as much as 5.5% before settling into a 4.4% gain as of 12:34 p.m. ET.

Alibaba held a big cloud event last week, giving a bullish outlook and raising its cloud spending forecast above its prior target of $53 billion over three years. Apparently, the outlook was encouraging enough for several Wall Street analysts to significantly raise their price targets on shares to start the week.

On Monday, analysts at Wall Street banks Morgan Stanley and Jefferies raised their price targets on Alibaba. Morgan Stanley’s Alibaba analyst team raised its target from $165 to $200, largely on the back of increased cloud computing growth. The analysts now actually see cloud growth accelerating 32% in fiscal 2026 and 40% in 2027. For reference, last quarter Alibaba grew its cloud revenue 26%, which was already an accelerating figure.

Obviously, generative AI is sparking huge new demand for Alibaba’s cloud services and models, with the Morgan Stanley analysts projecting the number of tokens doubling every two to three months. An AI token is a word or part of a word in an AI prompt or response that acts as essentially a “unit” of AI processing.

Meanwhile, investment bank Jefferies raised its price target from $178 to $230. The analysts cited “remarkable” progress on Alibaba building out AI infrastructure, innovating with its Qwen series of models, and developing useful software agents.

Image source: Getty Images.

Alibaba’s stock has rallied 113% this year in a remarkable AI-fueled turnaround. However, shares only trade at 20.7 times earnings, which is still cheaper than the large U.S.-based tech giants.

There are certainly risks to investing in China; however, it appears the government is now more supportive of the tech sector than the hostile posture it took back in 2021-2022. As such, it’s no surprise to see the country’s tech leaders doing much better today.

Billy Duberstein and/or his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Jefferies Financial Group. The Motley Fool recommends Alibaba Group. The Motley Fool has a disclosure policy.

More than 30 of the largest banks worldwide join in the design, development, and testing of the new offering, SWIFT announced at the Sibos conference.

Big news at this year’s Sibos conference in Frankfurt came right at the opening on Monday. SWIFT announced it would add a shared blockchain-based ledger to its infrastructure, marking a groundbreaking move to accelerate and expand the advantages of digital finance across more than 200 countries and territories worldwide.

The initial focus will be on real-time, 24/7 cross-border payments, and the financial messaging cooperative creates a network connecting over 11,000 banks across more than 200 countries. The launch date hasn’t been announced, but once implemented, this ledger will make cross-border payments less expensive worldwide.

SWIFT and more than 30 leading financial institutions from 16 countries worldwide, including Bank of America, BBVA, BNP Paribas, Citi, DBS, Deutsche Bank, Emirates NBD, First Abu Dhabi Bank, HSBC, JPMorgan Chase, MUFG, OCBC, Royal Bank of Canada, Societe Generale – FORGE, Standard Chartered, and TD Bank, are collaborating on the project. Financial institutions will provide feedback on the ledger’s design, followed by further development and testing.

Initially, SWIFT will collaborate with blockchain software developer Consensys on a conceptual prototype of the ledger, which will support interoperability across current and emerging systems. The model employs the parallel tracks of “upgrading existing rails while creating future digital rails to maximize infrastructure choice for the industry.”

The announcement is significant for several reasons: it demonstrates that SWIFT is poised to leverage the unique strengths of its network for the launch of a global blockchain ledger, and it is backed by most major global banks worldwide. It is also a clear sign to all the various proprietary blockchain ledgers launched by other institutions that today’s plan is the result of a collective effort and will bridge and coordinate what each financial institution has done and is doing in this area.

“Our track record of developing instant cross-border payment capabilities and our early foray into blockchain-based payment solutions enable DBS to meaningfully support SWIFT’s digital shared ledger initiative,” said Lim Soon Chong, Group Head of Global Transaction Services at DBS Bank. “We believe blockchain technology can usher in the next generation of ‘always-on’ and ‘smarter’ financial services. SWIFT’s initiative goes a step further – it is interoperable with traditional correspondent banking rails, has a high transaction capacity within a secure environment, and is accessible by SWIFT’s global banking network. These characteristics are critical in supporting broad-based reach and adoption, and have the potential to form the backbone of a resilient and future-ready global financial infrastructure.”

Published on

29/09/2025 – 16:54 GMT+2

The sword of Damocles hanging for several months over the global film industry located outside the US appears to have fallen: US president Donald Trump announced on Monday that he wants to impose a 100% tax on films made abroad.

“Our movie making business has been stolen from the United States of America, by other Countries, just like stealing ‘candy from a baby.’ California, with its weak and incompetent Governor, has been particularly hard hit!” Trump wrote on his social media Truth Social, adding: “Therefore, in order to solve this long time, never ending problem, I will be imposing a 100% Tariff on any and all movies that are made outside of the United States. Thank you for your attention to this matter. MAKE AMERICA GREAT AGAIN! President DJT.”

In May 2024, Trump authorised the US Department of Commerce and the US Trade Representative to slap a 100% tariff on all movies not produced in the US.

Representatives of the EU film industry who spoke to Euronews feared at the time that they might be overlooked by the EU in its trade negotiations with the US.

Since then, a trade agreement concluded in July made no mention of the film industry – a service sector not covered by blanket tariffs of 15% that were slapped on all US-bound EU goods.

The EU film industry faces criticism from major American streaming platforms which claim EU rules are too protective of the interests of the European industry.

The Motion Picture Association (MPA), which represents US film, television, and streaming industries, has its sights set on the EU legislation imposing quotas requiring video on demand services operating in the EU to reserve 30% of their catalogue for European work and obligations to invest in European works made by EU member states. They had written to the Trump administration in March 2024 to defend their cause.

In 2023, 4.8 million European movies were screened in the US, according to the European Audiovisual Observatory.

The European Commission has been approached for comment.

Article content

Amazfit welcomes back Hunter McIntyre and expands its elite athlete team for the 2025/26 HYROX season with Rich Ryan, Joanna Wietrzyk, Emilie Dahmen, and Linda Meier

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

REGISTER / SIGN IN TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

THIS ARTICLE IS FREE TO READ REGISTER TO UNLOCK.

Create an account or sign in to continue with your reading experience.

or

Article content

MILPITAS, Calif. — Amazfit, a leading global smart wearables brand by Zepp Health (NYSE: ZEPP), and the Official Timing & Wearable Partner of HYROX, today announced the expansion of its HYROX athlete roster, with Hunter McIntyre (USA) returning for another season and four standout competitors joining the team: Rich Ryan (USA), Joanna Wietrzyk (Australia), Emilie Dahmen (Netherlands), and Linda Meier (Germany).

Article content

Article content

Article content

This roster reflects Amazfit’s commitment to supporting both proven champions and emerging talent in functional fitness racing, while integrating athlete feedback directly into product innovation.

Article content

This roster reflects Amazfit’s commitment to supporting both proven champions and emerging talent in functional fitness racing, while integrating athlete feedback directly into product innovation.

Article content

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Hunter McIntyre

Article content

– Widely regarded as the face of HYROX, McIntyre remains one of the sport’s most dominant and influential athletes. A multiple-time champion with a loyal fanbase, he continues to push boundaries in competition and beyond, leading training camps and outdoor adventure races. McIntyre has been instrumental in Amazfit product development, relying on the rugged

Article content

Amazfit T-Rex series

Article content

to fuel his relentless pursuit of podium finishes.

Article content

“I’m excited to be returning to Team Amazfit for another few years. The products are great, they listen to me when I have input, and I feel like I am getting actionable insights that are helping to drive my training. We almost got it done last year in Chicago — this year I’m here for the gold.”

Article content

Article content

Rich Ryan

Article content

– Known for his data-driven approach and coaching influence, Ryan brings dual impact as an elite competitor and educator. One of the fastest men on the HYROX course, he pairs his athlete achievements with seminars and coaching through his RMR training company. Ryan’s deep demand for precision aligns seamlessly with Amazfit’s

Article content

Balance 2

Article content

Article content

Helio series

Article content

, making him a trusted partner in advancing performance metrics for athletes everywhere.

Article content

“I joined Team Amazfit because of their commitment to HYROX and hybrid training. I believe hybrid training and competition can help athletes grow into healthier, more effective versions of themselves, and having partners who share those values is really important to me. I’m also excited to collaborate with the team at Amazfit, who continue to push innovation and show real ambition in this space.”

Article content

Article content

Joanna Wietrzyk

Article content

– A breakout star from Australia, Wietrzyk stunned the HYROX community with a second-place finish in Chicago. A former competitive tennis player, she is quickly emerging as a top contender across solo and doubles formats. Wietrzyk, who will be sporting the

Article content

Amazfit T-Rex 3

Article content

, values her close collaboration with Amazfit’s sports marketing team and is poised to elevate both her career and the brand’s visibility globally.

Article content

“After an incredible first season in HYROX, I’m focused on building momentum and pushing my performance even further this year. That means going beyond what I’ve done before and partnering with teams that truly support the way I train, recover, and compete. Amazfit does exactly that. Their technology helps me stay consistent and intentional, whether I’m tracking key metrics during intense sessions or monitoring recovery post-race. Amazfit gives me the right tools to train smarter, stay balanced and continue progressing – and that’s what makes this partnership so exciting.”

Article content

Article content

Article content

Emilie Dahmen

Article content

– One of the sport’s most exciting rising stars, Dahmen captured attention by winning two HYROX races in her debut season and finishing sixth at the World Championships. Still early in her career, she represents the next generation of HYROX talent. Dahmen’s embrace of Amazfit wearables, specifically the

Article content

Balance 2

Article content

Article content

Helio Strap

Article content

, makes her a natural fit for the team as she continues her rapid ascent.

Article content

“I hadn’t relied on a watch or performance data before, and reaching the HYROX Elite 15 without it was already a huge achievement. Partnering with Amazfit now gives me the tools to train smarter, recover better, and truly compete at the highest level. Their technology helps me unlock even more potential, and I hope to inspire others to see how powerful smart training can be.”

Article content

Article content

Linda Meier

Article content

– The reigning HYROX World Champion, Meier delivered a career-defining performance in Chicago to secure her title. Already a respected competitor, her consistency and professionalism make her an invaluable ambassador. Meier relies on the

Article content

Amazfit Helio Strap

Article content

Article content

Amazfit T-Rex 3

Article content

for advanced data insights, helping her balance performance and recovery at the highest level.

Article content

“With Amazfit by my side, I can combine my World Champion spirit with smart technology – showing that anyone can push beyond their limits with the right tools.”

Article content

Article content

“Our partnership with HYROX is about helping athletes maximize every moment of training, performance, and recovery,” said Scott Shepley, Head of Global Marketing of Amazfit. “By signing a roster that blends world champions with promising new talent, we’re reinforcing Amazfit’s role as the performance partner of choice for athletes who trust data to fuel their goals.”

Article content

As part of Team Amazfit, these athletes will contribute to product testing, content storytelling, and community engagement, ensuring Amazfit continues to deliver cutting-edge tools that meet the evolving demands of functional fitness athletes.

Article content

Athletes and fans can explore Amazfit’s full range of smart wearables — including the T-Rex series, Balance 2, Active 2, and Helio Strap — at www.amazfit.com, and follow the brand’s HYROX journey throughout the 2025/26 season.

Article content

About Amazfit

Article content

Amazfit, a leading global smart wearable brand focused on health and fitness, is part of Zepp Health (NYSE: ZEPP), a health technology company with its principal office based in Gorinchem, the Netherlands. Zepp Health operates as a distributed organization, with team members and offices across the Americas, Europe, Asia, and other global markets.

For 90 years, Social Security has provided Americans with a financial safety net. Today, Americans are concerned about potential cuts to the program.

Surveys may be little more than a snapshot in time, but they can provide an interesting peek into the minds of fellow Americans. This year, as Social Security turns 90, the Bipartisan Policy Center’s (BPC) American Savings Education Council polled Americans on how they feel about the current state of the program. Here’s what they learned.

Image source: Getty Images.

Whether they’re just beginning to plan for retirement or have been chipping away at it for years, Americans value Social Security. The following represents their concerns, anxieties, and hopes.

According to Jonathan Burks, Executive Vice President of Economic and Health Policy for the BPC: “Americans across the political spectrum agree strongly that Social Security matters, and they want to see bipartisan work to strengthen the program for the future. Now it is up to lawmakers to build on this consensus and do the hard work of forging a path forward.”

If Congress doesn’t take steps to shore up the Social Security program, it’s expected that the Social Security trust fund will run dry in 2033. At that time, the Social Security Administration would begin across-the-board cuts of 23%. For example, a Social Security recipient with a monthly benefit of $2,000 would see their checks reduced to $1,540.

While it’s impossible to see the future, here are some of the expected consequences of cuts to Social Security:

“The only way we get a fix is if the two parties hold hands and jump together,” Shai Akabas, Vice President of Economic Policy at BPC, said in the report. “These results show that the American people understand and support that outcome. It’s time for our elected leaders to follow suit.”

Home ![]() Transaction Banking

Transaction Banking ![]() Finastra Unveils Intelligent Routing Module To Revolutionize Payments Processing

Finastra Unveils Intelligent Routing Module To Revolutionize Payments Processing

The new module is designed to help banks route payments faster, cheaper, and smarter across multiple rails.

Finastra, a global leader in financial services software, announced its new Intelligent Routing Module at Sibos 2025 on Monday, a solution aimed at greatly improving efficiency and customer experience in payments processing for banks and financial institutions.

The Intelligent Routing Module brings a data-driven approach to payment routing, enabling banks to process transactions faster and at a lower cost. Finastra reports that the new solution can achieve an impressive straight-through processing rate of upwards of 95%, leading to better outcomes for both financial institutions and their customers.

The module operates as a standalone capability for broader payment orchestration or as an integrated component within Finastra’s Global PAYPlus payment-hub offering. It utilizes advanced algorithms to identify the most efficient payment rails in real-time. This includes factoring in critical elements such as costs, speed, available payment scheme options, and regulatory requirements. The system is designed to ensure each transaction takes the optimal path across various payment types, including mass payments, instant payments, high-value transactions, and even optimizing correspondent banking chains for high-value cross-border payments.

“Payments are the lifeblood of banking, and speed, cost, and transparency matter more than ever,” states Radha Suvarna, chief product officer, Payments at Finastra, highlighting the importance of the new module. “Our Intelligent Routing Module delivers on all three – giving banks the intelligence to route payments for maximum efficiency while meeting customers’ expectations for fast, seamless service.”

Leveraging decades of expertise in processing trillions of dollars in daily transactions for major global banks, the Intelligent Routing Module is available both within Finastra Global PAYplus and as a standalone, system-agnostic modular package. Built on microservices and open APIs, the solution empowers banks to more efficiently validate clearing memberships, determine optimal payment routes, and establish efficient cross-border correspondent chains.

The module’s open architecture enables seamless integration with various payment initiation channels, order management systems, orchestration systems, or existing payment engines. This flexibility promises a rapid return on investment and mitigates the risks often associated with large-scale transformations or system replacements.

Finastra’s Global Payments Framework, which combines an API-first approach with configurable business rules and AI-driven intelligence, aims to empower financial institutions to deliver differentiated customer experiences with greater flexibility, speed, and minimal customization.

Published on

29/09/2025 – 14:05 GMT+2

The price of gold climbed to a new record on Monday, rising above $3,850 an ounce in the afternoon in Europe, up more than 1% on the day.

Precious metals across the board surged, fuelled by a weak dollar and high uncertainty around funding for the US federal government.

On Monday, US President Donald Trump and the Republican Party are meeting with Democrats to discuss a short-term spending bill to avoid a government shutdown on Tuesday. Republicans need at least seven votes from Democrats to pass the legislation.

Uncertainty is high, which historically sees investors flocking into so-called safe-haven assets such as gold. The precious metal is a more stable option in turbulent times when other asset classes are far more volatile.

So far this year, gold has shown itself to be an investor favourite amid increased geopolitical tensions and trade uncertainties. Since January, the precious metal has gained over 45%, rising from $2,669 an ounce.

Other factors are also supporting gold prices, including expectations of further rate cuts from the Federal Reserve. On 17 September, the Fed lowered its target range for its main lending rate to 4% – 4.25%, and officials indicated that there could be two more rate cuts this year.

Lower rates tend to weaken the US dollar, in which gold is denominated, increasing the metal’s appeal. This is particularly the case when other interest-bearing assets like bonds and savings accounts offer lower yields, following rate cuts.

“Gold prices continue to mark new records, with expectations for further rate cuts from the Fed supportive, given the precious metal does not offer income,” said Russ Mould, investment director at AJ Bell.

“Now above $3,800, gold has also been boosted by central bank buying over several years, weaker demand for traditional safe havens like US government bonds driven by concerns over US deficits and trade policy, dollar weakness and geopolitical tensions, including conflicts in the Middle East and Ukraine,” Mould added.

“The threat of a shutdown in Washington, as policymakers engage in tense negotiations ahead of a deadline at midnight on Tuesday, is yet another factor driving support for gold.”

Disclaimer: This information does not constitute financial advice; always do your own research on top to ensure it’s right for your specific circumstances. Also remember, we are a journalistic website and aim to provide the best guides, tips and advice from experts. If you rely on the information on this page, then you do so entirely at your own risk.

These stocks are down, but certainly not out. Take a closer look before they bounce back.

The market’s moving higher, and there’s a good chance that many of the stocks in your portfolio are having a good year. That doesn’t mean that you have a portfolio loaded with winners. Every investor has laggards, and for me, one of them is Target (TGT 1.02%). I’ve owned the discount retailer through some good years, and lately some bad ones.

Target shares have been cut nearly in half over the past year. Investors tend to shy away from falling stocks, but this out-of-favor stock is high on my list of potential purchases in November. And it’s not the only name I’m looking at. I believe that Duolingo (DUOL 4.29%) and Crocs (CROX 6.63%) — two other stocks I own that have fallen by at least 40% from their 52-week highs — are also ready to bounce back; I think they’re out-of-favor stocks to buy right now.

Let me dive into what I hope will be a timely contrarian take on Target, Duolingo, and Crocs.

Before I go into what’s holding Target back these days, I want to talk about its juicy dividend. The cheap-chic chain is currently yielding 5.2%, a historic high. With money-market and fixed-income yields heading lower, Target’s quarterly distributions are worth celebrating.

Target is good for the money; it has found a way to boost its dividend for 54 consecutive years. You know how they say that e-commerce will be the end of brick-and-mortar chains? Well, Target has found a way to deliver hikes every year since the commercialization of the internet. This Dividend King‘s latest guidance calls for a profit of between $7 and $9 per share this year, meaning a healthy payout ratio of 51% to 65%.

Image source: Getty Images.

The dividend is sustainable, despite Target’s recent misfires. The retailer is struggling to connect with shoppers. In-store comparable sales slipped 5.7% in its most recent quarter, with overall comps down 3.8% for the period. It’s losing market share — a sobering reality for a company that used to feast at the expense of its retail stock rivals with its now-fading aspirational brand.

But patient investors are getting more than a bountiful 5.2% yield right now; they’re getting a bargain. Target is trading for just 11 times the midpoint of its earnings guidance this year.

Analysts see a return to revenue and net income growth next year. Wall Street profit targets have been inching higher over the past three months, and the mass-market retailer has exceeded bottom-line expectations in two of the last three quarters. Last month’s quarterly report wasn’t popular with most investors, but at least three major analysts boosted their price targets on the company. While the turnaround will take time and a potential uptick in reinvestment obligations, there are worse places to be than riding it out with big dividend checks coming every quarter.

Unlike Target, Duolingo isn’t going through growing pains. Revenue growth has topped 40% in each of the last five years. The language-learning company’s top line accelerated in its latest quarter, with a 42% year-over-year surge as its healthiest jump in more than a year.

Duolingo’s shares have still fallen 40% since scoring an all-time high in the spring, which doesn’t seem fair. It wasn’t just revenue picking up the pace since the shares peaked — in the most recent earnings report, profit landed 32% ahead of what Wall Street was modeling. There are concerns about artificial intelligence (AI) leveling the playing field for language learning, but that dismisses Duolingo’s own AI enhancements. Its platform and the gamification of learning have made the company a winner.

Unlike the other two names on this list, Duolingo isn’t cheap; it’s trading for nearly 40 times forward earnings. However, it was trading a lot higher when it lacked today’s momentum. The Duolingo owl is wise. This feels like a buying opportunity in any language.

Like another discarded cheap-chic stock, Crocs is a bargain. The maker of distinctive footwear is trading for just 6 times this year’s projected adjusted earnings. As with Target, revenue and profitability are going the wrong way this year.

Crocs has a history of riding the ups and downs of demand for its comfy hole-laden resin clogs. The same can be said of most shoe stocks. It always finds a way to get back in style, doing so consistently for a couple of decades. Its streak of seven consecutive years of top-line gains may come to an end this year, but it’s not likely to stay down for long.

It doesn’t offer the same chunky yield as Target — there’s no payout at all — but bargains come with different perks. Crocs is cheap, and history is on the side of those who believe when the masses do not.

Rick Munarriz has positions in Crocs, Duolingo, and Target. The Motley Fool has positions in and recommends Target. The Motley Fool recommends Crocs and Duolingo. The Motley Fool has a disclosure policy.

Published on

29/09/2025 – 11:58 GMT+2

In order to attract global investors, AstraZeneca said it will directly list its ordinary shares on the New York Stock Exchange, in addition to its shares trading in the UK and Sweden.

To do so, the Anglo-Swedish pharmaceutical giant needs to replace its existing US listing of AstraZeneca American Depositary Receipts (ADRs) on the Nasdaq.

The company said that the move aims to harmonise its listing structure “while remaining headquartered in the UK”.

“The Board of AstraZeneca is recommending to shareholders a Harmonised Listing Structure for the Company’s ordinary shares across the London Stock Exchange (LSE), Nasdaq Stockholm (STO) and the New York Stock Exchange (NYSE),” the company said in a statement.

The announcement follows increased speculation that the pharma company may move its shares entirely from the London Stock Exchange, where it is one of the largest companies traded. And according to analysts, the current announcement doesn’t exclude this possibility in the future.

“While there is logic to shifting to a direct listing in the US rather than American Depositary Receipts beyond setting up for any longer-term moves, it does at least hint at the possibility of a more dramatic shift at some point in the future,” said AJ Bell investment director Russ Mould.

The US has the world’s largest and most liquid public markets by capitalisation. A direct listing makes it easier for US investors to buy AstraZeneca shares directly without going through ADRs.

Compared to ordinary shares, American Depositary Receipts come with additional costs and extra steps. ADR investors may be subject to fees and double taxation, and ADRs come through a custodian bank.

“Enabling a global listing structure will allow us to reach a broader mix of global investors and will make it even more attractive for all our shareholders to have the opportunity to participate in AstraZeneca’s exciting future,” said Michel Demaré, Chair of AstraZeneca.

In response to the announcement, AstraZeneca’s shares listed on the FTSE 100 rose 0.71% at around 11.30 CEST.

If you have a buy-and-hold mindset, here are two dividend stocks that you can easily hang on to for a decade or longer.

“If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.” — Sir John Templeton

Dividend stocks have a few things going for them. Companies with growing dividends tend to be soundly profitable and financially healthy, which are two advantageous qualities to have during periods of economic downturn. Companies with a long dividend history are also more likely to have economic moats and advantages that enable them to pass along price increases and better maintain margins long-term.

Here are two solid companies that boast dividends and could trade higher as they improve their businesses from recent struggles.

It’s certainly been an interesting ride over the past few years for Campbell’s (CPB -0.34%). Its business mix shifted substantially, with its core soup lineup accounting for roughly 25% of total sales, down from about 40% in fiscal 2017. Snacks are up to 50%, up from less than 30% over the same timeframe.

Image source: Campbell’s.

Beyond its changing sales mix, management has worked to improve operating efficiencies across its supply chain and manufacturing network, while also backing up its brands with more marketing spend. These changes have driven an increase in annual organic sales.

Campbell’s still isn’t done, however. It recently laid out plans to unlock $250 million in savings through fiscal 2028, on top of the $950 million it realized over the past few years. Campbell’s is also driving growth through acquisitions and recently scooped up Sovos Brands, which generates more than $1 billion in annual sales.

Despite moving in the right direction and offering a dividend yield of 4.6%, the stock price has slid 20% year to date. This gives investors a chance to buy low on a consumer defensive dividend stock that is improving its business.

It’s been a bumpy ride over the past three years or so for the athletic apparel leader Nike (NKE 0.09%). But after the stock price spiraled 25% lower over that timeframe, it gives investors an opportunity to not only buy into its potential turnaround, but to enjoy receiving its 2.25% dividend yield while waiting.

Nike has faced recent problems that include a lack of product innovation, softer demand for sportswear, and strained relationships with wholesale customers. The company has proven that, over a long period of time, it can maintain its market share and pricing. But there are a couple of things that could drive this turnaround in the medium term.

First, although Nike’s recovery in China has been slower than desired, there’s still a massive opportunity as the market expands and more developing regions, such as China and Latin America, among others, have swaths of people moving into the middle class.

Second, during fiscal 2025, Nike brought back longtime executive Elliott Hill to serve as its CEO. Given his company knowledge and relationships with crucial partners, investors should be optimistic that he can improve results more quickly.

Both of these companies possess incredibly recognizable global brands, have real potential for stock price upside, and offer investors dividends while they wait for the business to turn around. If Campbell’s executes its savings initiative and Nike can capture growth in developing regions, both could become long-term cornerstones of just about any portfolio and provide some income from healthy dividends. These are definitely two stocks you can hold without worry for a decade.

Daniel Miller has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Nike. The Motley Fool recommends Campbell’s. The Motley Fool has a disclosure policy.

Small modular reactors are a perfect match for power-hungry artificial intelligence technologies.

So far this year, NuScale Power (SMR 0.66%) stock has more than tripled in value. The reason: rapidly rising interest in small-scale nuclear power. NuScale is arguably the leading developer of small modular reactors, with a quantifiable first-mover advantage. This lead could provide it with a decades-long runway of growth, fueled by another rapidly growing industry: artificial intelligence.

Proponents of nuclear power as a scalable, renewable, low-carbon source of power have been repeatedly stymied by global events that have hindered nuclear power expansion. From reactor meltdowns to sudden tsunamis, public opinion has shifted heavily due to numerous public failures of nuclear technology. Public outcry and safety concerns caused regulatory scrutiny to soar across many parts of the world, leading to huge cost overruns and engineering delays for many major nuclear projects.

The tides have turned yet again in recent years due to soaring energy demand from sectors like artificial intelligence — a sector that is requiring ever higher amounts of energy to thrive and survive. Big tech, for example, is deploying billions of dollars into restarting old nuclear facilities, as well as building several new facilities across the U.S. According to the Harvard Business Review, big tech has gone “all in” on nuclear.

These projects could take many years to come to fruition, and only deep-pocketed entities like Big Tech can afford to see them through. That’s partially why there’s so much hype around small modular reactors: a newer generation of nuclear reactors that can be built in a factory off-site and delivered anywhere in the world. That’s a huge advantage for power-hungry data centers located in cold, remote areas of the world — an advantage for reducing cooling costs, but a problem when it comes to sourcing large amounts of reliable local energy.

Small-scale nuclear has been a dream for decades. But the reality of small-scale nuclear may finally be upon us. NuScale has the first and only SMR certified by the Nuclear Regulatory Commission for commercial production. Management believes the company’s first order is just months away.

Image source: Getty Images.

In 2023, the NRC certified the first-ever SMR for commercial production: NuScale’s 50 MW model. Earlier this year, however, the company was able to gain certification for a larger 77 MW model. NuScale management thinks that its first order could be made official by this December — less than 90 days from now. The company already has a dozen reactors under construction. This would allow it to fulfill one or two initial orders, given that the company expects customers to combine six to 12 modules into each operating facility.

To be sure, competition exists. But none have gained certifications from the NRC. Some companies, like Oklo, have begun the application process, but NuScale is safely one to three years ahead of the competition in this regard. That lead is especially true when considering that NuScale has already lined up nearly all of the necessary materials and outsourcing partners to begin fulfilling orders. NuScale management believes they could handle up to 20 orders per year as demand materializes.

Investors should be cautious regarding the timelines here. Even if NuScale receives an order in 2025, construction of the project wouldn’t be completed until 2030 at the earliest. NuScale would, of course, receive revenue before that date. But there may not be a fully functioning, real-world use case of SMRs for another five years, a reality that may keep demand low in the meantime.

Still, NuScale is an exciting growth company that has a healthy lead on the competition. With a market cap of just $10 billion, the stock looks like a reasonable bet for patient investors, even after the strong run-up.

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool recommends NuScale Power. The Motley Fool has a disclosure policy.

This innovation-first stock is priced for good long-term growth.

Over the past couple of years, there’s a strong case that no companies have gotten as much attention as those dealing with artificial intelligence (AI). In some cases, these are relatively new companies, while in other cases, they are established big tech stocks.

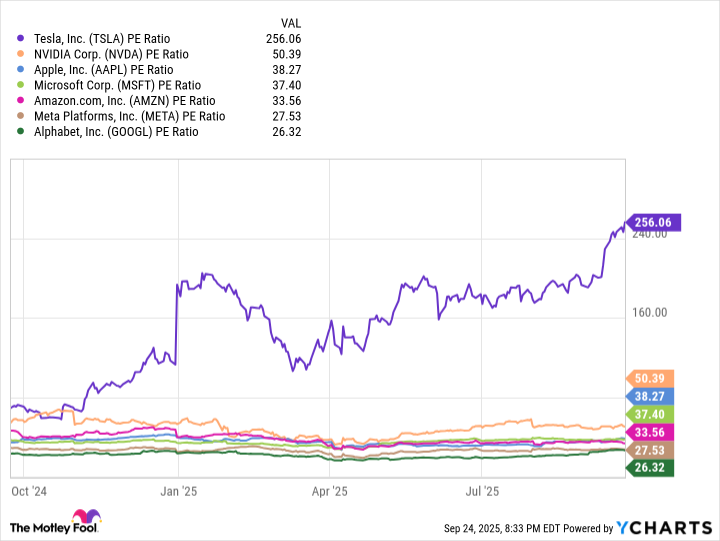

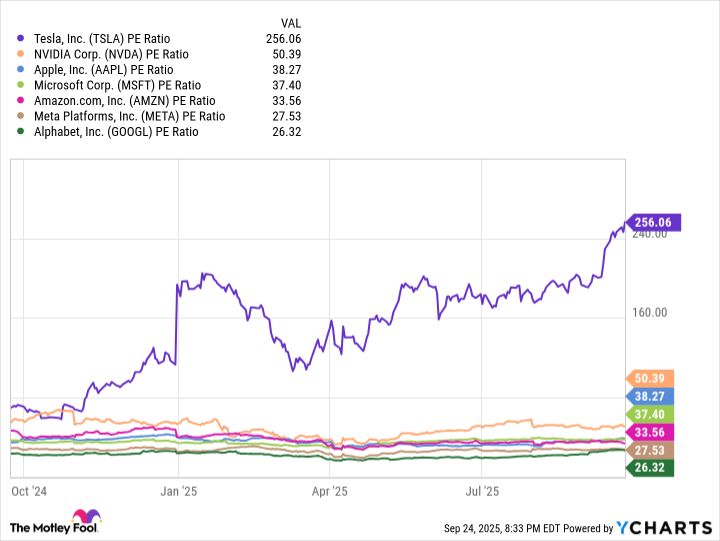

Focusing on the big tech stocks (because they’re better positioned for longevity in most cases), there’s one stock that sticks out as one of the best AI bargains on the market: Alphabet (GOOG 0.21%) (GOOGL 0.28%). At the time of writing, Alphabet is trading at 26.3 times its projected earnings over the next 12 months — which is the cheapest of all the “Magnificent Seven” stocks.

TSLA PE Ratio data by YCharts. PE = price-to-earnings.

Valuation alone doesn’t make a stock a buy, but it does give it more upside than downside. There isn’t as much growth and expectation priced into the stock, which could help guard against sharp pullbacks if those expectations aren’t met.

Image source: Getty Images.

Aside from just its valuation, Alphabet sticks out because it operates in many critical parts of the AI pipeline. Its subsidiary, DeepMind, handles AI research. It owns and operates dozens of data centers (which are needed to train and scale AI), and it has consumer AI applications, such as its generative AI tool, Gemini, and Flow, its filmmaking tool.

Being involved in the various parts of the AI pipeline is beneficial for Alphabet, because it has more control over innovation and integration and is less reliant on others.

Stefon Walters has positions in Apple and Microsoft. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

You can count on these ultra-reliable dividend stocks to boost your passive income no matter what the stock market is doing.

As companies mature, they often choose to implement a dividend as a way to directly reward shareholders. On the other hand, smaller up-and-coming companies will want to put all the dry powder possible into their ideas to make them succeed.

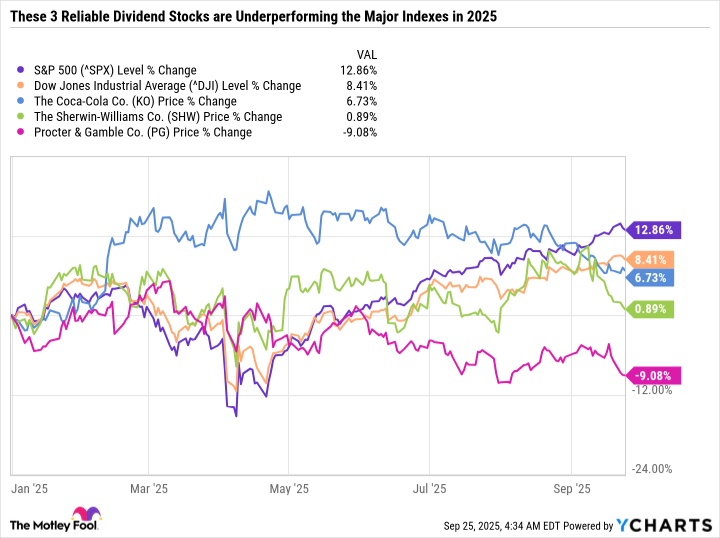

Coca-Cola (KO -0.52%), Procter & Gamble (PG 0.23%), and Sherwin-Williams (SHW 0.58%) are three industry-leading companies that have been around for over 100 years. Their track records have earned them spots among the 30 components in the Dow Jones Industrial Average (^DJI 0.65%).

Dividends have been an integral part of their capital allocation plans for decades. And because all three companies have steadily grown their earnings over time, they have also been able to increase their quarterly dividends.

Investing $15,000 into each stock could help you generate over $1,000 in passive dividend income per year. Here’s why all three dividend stocks are great buys in October.

Image source: Getty Images.

Coca-Cola was one of the few stocks that held up when the market was tanking in response to tariff woes and geopolitical uncertainty in April. That same month, it hit an all-time high. But since then, Coke has been steadily falling while the S&P 500 (^GSPC 0.59%) has been gaining. And after a hot start to the year, Coke is now underperforming the Dow and the S&P 500.

Coke’s fundamentals remain intact. The company is generating solid organic growth and diversifying its beverage lineup by leaning into healthier options. Coca-Cola Zero Sugar and Diet Coke are performing well, and Coke is shifting from high-fructose corn syrup to cane sugar in the U.S.

Coke has the beverage lineup, supply chain (through its bottling partnerships), and brand power to adapt to changing consumer preferences. In the meantime, the stock has gotten much cheaper, sporting a 23.6 price-to-earnings (P/E) ratio compared to a 10-year median P/E of 27.7.

Coke yields 3.1%, making it a solid source of passive income. And it has raised its dividend for 63 consecutive years, earning it a coveted spot on the list of Dividend Kings.

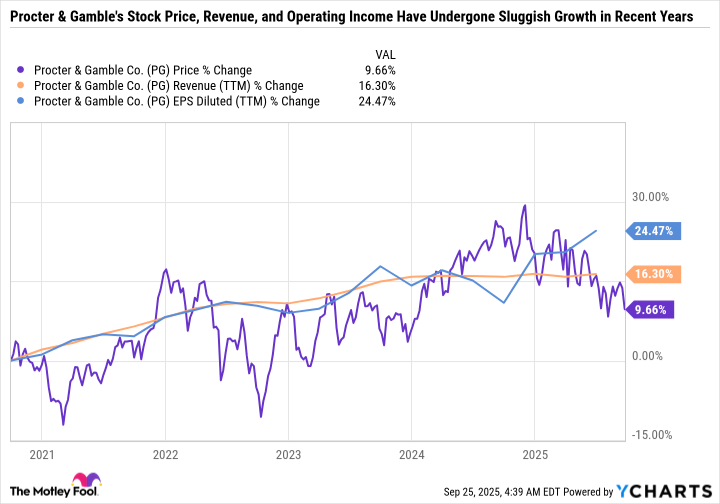

P&G is in a similar boat to Coke. It has great brands, but consumers are getting hit hard by inflation and cost-of-living pressures.

In June, P&G announced plans to cut 7,000 jobs and exit certain brands and markets as part of a restructuring effort. In July, it announced that its chief operating officer, Shailesh Jejurikar, would take over as CEO on Jan. 1, 2026. These major shakeups, paired with relatively weak results and guidance, may be why P&G is hovering around a 52-week low at the time of this writing.

P&G has essentially three levers it can pull to grow its earnings. It can sell higher volumes of products, it can raise prices, and it can repurchase stock, which increases earnings per share. Volume growth is the most sustainable option because it has fewer limits compared to price increases, which are subject to consumer constraints. And there’s only so much free cash flow P&G generates to buy back its stock (it usually reduces its share count by 1% to 2% per year).

Unfortunately, P&G has been relying heavily on price increases in recent years. And consumers are pushing back, as P&G’s organic growth has drastically slowed.

P&G now sports a P/E ratio of 23.4 and a forward P/E of 21.8 compared to a 10-year median P/E of 25.5. Like Coke, P&G is a Dividend King with a high yield at 2.8%. It’s a great buy for risk-averse investors looking for a reliable source of passive income who don’t mind giving the company time to restructure.

The paint and coatings giant had been a steady market outperformer to the point where it earned its spot in the Dow last year, replacing commodity chemical giant Dow Inc. But Sherwin-Williams’ stock has underperformed the major indexes this year largely due to high interest rates, which are impacting many of its end markets.

Sherwin-Williams benefits from increases in consumer spending and economic growth. Higher borrowing costs have been a drag on the housing market and home improvement projects, as evidenced by Home Depot‘s lackluster earnings growth over the last couple of years.

Still, Sherwin-Williams has the makings of an excellent dividend stock for long-term investors. It has 46 consecutive years of dividend raises, but its yield is just 0.9% because the stock price has outpaced its dividend growth rate — gaining 352% over the last decade, which is even better than the S&P 500’s 244% increase.

Sherwin-Williams has an excellent business model. It sells its products through its own retail stores, online, and partnerships with retailers like Lowe’s Companies. It also has a sizable coatings business and industrial and commercial paints business. Coatings are used to protect surfaces across various industries, including automotive, aerospace, and marine.

Add it all up, and Sherwin-Williams is a great buy in October.

Coke, P&G, and Sherwin-Williams may not light up a growth investor’s radar screen. But all three companies pay growing, ultra-reliable dividends.

Coke and P&G have discounted valuations compared to their historical averages, whereas Sherwin-Williams is roughly in line with its 10-year median valuation.

Add it all up and these are three picks ideally suited for investors looking to round out their portfolios with non-tech-focused ideas.

Sofi Technologies is a fast-growing digital bank that is turning profitable while pursuing significant opportunities in investing and crypto.

SoFi Technologies (SOFI -0.45%) has faced plenty of sceptics since going public in 2021. Many investors viewed it as a niche player in student loan refinancing, doubting it could ever achieve profitability.

Fast-forward to today, and SoFi not only generates consistent profits, it’s expanding into new areas that have the market buzzing. Shares recently surged to fresh highs, putting the company squarely in the fintech spotlight.

Here are three reasons why everyone is talking about SoFi right now — and what investors should keep in mind before following the crowd into buying the stock.

Image source: Getty Images.

SoFi isn’t your typical bank. While most financial institutions make money through a patchwork of branches, tellers, and specialized divisions, SoFi operates as a digital-first platform. Its pitch is simple: Manage your entire financial life in one app.

That means you can open a checking account, refinance a loan, trade stocks or crypto, and even buy into new exchange-traded funds (ETFs) — all in one account. The company’s strategy is to cross-sell as many products as possible to each customer, increasing engagement and lowering churn.

This integrated approach matters. Traditional banks often specialize in one area — say, deposits and mortgages — while a brokerage focuses on investing. By integrating everything into a single ecosystem, SoFi increases switching costs and fosters long-term customer loyalty.

For years, critics argued that SoFi could attract users but not profits. And they were right, at least until 2023.

But that narrative is shifting as Sofi has delivered two consecutive years of positive adjusted net income and continues to do so in 2025. In the second quarter of 2025, adjusted net revenue rose 44% year over year to $858 million. Adjusted net income surged 459% to $97 million. The solid performance is a result of a record high in new members, new products, and an increase in fee-based revenue.

Membership growth was equally impressive. SoFi added 846,000 new members in Q2 2025, pushing its base to 11.7 million — more than double what it had three years ago. Crucially, the mix of revenue is changing. Fee-based revenue contributed 44% of total revenue, indicating the company has expanded beyond its student loan financing roots.

Even its lending portfolio has performed well of late as the company originated a record $8.8 billion in loans in the quarter, while bad debt charge-off has largely been declining over the last few quarters. Expectations for lower interest rates could also further boost lending volumes and profitability in the coming quarters.

SoFi could easily stop at being a profitable digital bank. Instead, management is pushing into new frontiers. The company will restart its crypto service this year, enabling members to trade Bitcoin and Ethereum. While volatile, crypto broadens SoFi’s appeal among younger and more tech-savvy users.

It also launched new investment products, like the SoFi Agentic AI ETF, designed to capture investor interest in artificial intelligence. Beyond ETFs, SoFi is expanding into private market funds, giving retail investors access to opportunities once reserved for institutions.

These moves highlight SoFi’s ambition to build a full-spectrum financial platform. But they also come with risk. Each market brings established competitors — from Robinhood Markets in trading, to BlackRock in asset management, to Coinbase Global in crypto. Execution and regulatory oversight will be ongoing challenges that investors should track.

SoFi is no longer just a one-dimensional fintech tied to student loans. It’s becoming a diversified platform with real profitability and a broad set of growth levers. That’s why the stock is getting so much attention right now.

Still, investors should recognize the risks. Valuations already incorporate optimism — as of this writing, the stock trades at a price-to-earnings (P/E) ratio of 62 times — and SoFi must prove it can balance banking, investing, and emerging areas like crypto without losing focus.

For growth investors, the pitch is straightforward. If SoFi can scale its ecosystem while executing on new growth bets, it has the potential to be a defining financial company of this generation.

Either way, it’s worth keeping the stock on watch.

Lawrence Nga has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin and Ethereum. The Motley Fool recommends BlackRock and Coinbase Global. The Motley Fool has a disclosure policy.

Fresh Europe data on August Tesla registrations wasn’t pretty.

Tesla (TSLA 3.94%) shares fell more than 4% last Thursday as investors digested disappointing Tesla vehicle registration data in Europe ahead of the company’s third-quarter deliveries update expected in early October. The electric vehicle maker sells premium battery-electric cars and energy storage products globally, with meaningful exposure to the European market.

The market’s question now is simple: Does the regional weakness point to a poor quarter, or is it mostly noise inside a broader and still-uncertain recovery?

Image source: Getty Images.

News out Thursday showed Tesla’s European Union registrations fell about 37% year over year in August to roughly 8,200 vehicles, marking a second straight month in which the China-based BYD outsold Tesla in the bloc. Including the broader European region (the U.K., Norway, and other EFTA countries), Tesla still led in absolute units for August, but registrations were down about 22% year over year, underscoring persistent pressure in the region.

This softness in Europe follows a tough second quarter for the electric car maker. In Q2, Tesla delivered just over 384,000 vehicles — down 13% from about 444,000 in the year-ago period.

It is also worth recalling the company’s tone on the latest earnings call. CEO Elon Musk acknowledged that the near term may not be smooth, noting that things could get “rough” before they get better over the next few quarters. While that comment doesn’t guarantee weak third-quarter deliveries, it frames Tesla’s headlines about European deliveries within management’s own caution about the path back to growth.

With only days left in the period when the August Europe data hit the tape, the right way to think about Q3 is probably through a conservative range, not a single-point guess. Start with what we know: Tesla delivered about 384,000 vehicles in the second quarter, it delivered roughly 463,000 in last year’s third quarter, and outside Europe there are mixed but not universally negative signals. Some trackers have flagged improving weekly registrations in parts of Europe late in September, and several outlooks have pointed to steadier demand in China and the U.S., even as Europe stays choppy. Still, Europe’s August decline argues for caution.

A reasonable, conservative estimate for Q3 deliveries is 430,000 to 455,000. The low end assumes Europe remains a drag through quarter-end and that China/U.S. improvement only partly offsets it. The high end assumes late-September sequential gains in key markets and typical quarter-end logistics help. That range sits close to widely cited expectations near the mid-440,000s and acknowledges both the seasonal lift from Q2 and the regional weakness that surfaced this week. For reference, landing near 445,000 would be down modestly year over year versus the roughly 463,000 delivered in last year’s third quarter.

Of course, in the end, no one knows where deliveries will come from. Further, note that this is a conservative estimate. There’s always a chance that deliveries could come in above this range (or even below).

Meanwhile, the stock’s valuation doesn’t help the bull case. At a market value well above $1 trillion and with a price-to-earnings ratio of 252 as of this writing, the stock embeds high expectations well beyond one quarter’s deliveries. Such a high valuation leaves less cushion if third-quarter deliveries disappoint, or if commentary points to rough demand trends going into year-end.

Of course, there are some significant positives for investors to consider, too. Energy storage deployments remain a bright spot. Furthermore, a recent Model Y refresh, advancements in self-driving technology, and a planned upcoming vehicle launch could all contribute to increased demand in the second half of the year. But given this fresh data on Tesla registrations in the E.U., it’s fair to say that risk sits a bit higher heading into next week’s update.

The bigger story, anyway, will be a forward-looking one. Investors should look for any insight management provides on how quickly it thinks deliveries can reaccelerate. Because sales are going to need to pick up sharply at some point in order for Tesla’s fundamentals to live up to its stock price.

Daniel Sparks and/or his clients have positions in Tesla. The Motley Fool has positions in and recommends Tesla. The Motley Fool recommends BYD Company. The Motley Fool has a disclosure policy.

The stock has rocketed 361% over the last 12 months.

BigBear.ai (BBAI -5.74%) is a leader in providing artificial intelligence (AI) technology for national security. Investor optimism about increasing government investment in AI, and the potential impact on BigBear, has sent the stock up 361% over the last year.

President Donald Trump’s “big, beautiful bill” could be a catalyst, as it provides substantial funding for spending on defense technology. BigBear.ai believes it is well positioned to benefit, but does this make the stock a buy?

Image source: Getty Images.

Revenue has been flat over the last three years. The company reported an 18% year-over-year decrease in revenue in the second quarter, driven by lower volume from certain Army programs.

While the loss of revenue from these Army programs was a setback, legislative tailwinds are in BigBear’s favor. The bill provides billions of dollars in funding for border security, which is one of BigBear’s specialties, where it supplies biometric solutions for traveler processing.

BigBear ended last quarter in a solid financial position. It has a net cash position of $248 million on its balance sheet — the strongest financial position in the company’s history. Management intends to invest aggressively in hiring top-tier AI talent and innovation to win a share of the funding going to national security programs.

The stock offers significant upside potential from a market cap of just $2.6 billion. But the company will have to prove it is up to the job and win more contracts, which is no guarantee. I would look at the stock like a call option on whether the company can land a big contract. This is a stock for those who are willing to accept high volatility for the potential of explosive returns if BigBear.ai can secure large government deals.

John Ballard has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

Big news for retirees is on the way in just 17 days.

Seventeen days. That’s how much longer Social Security beneficiaries must wait to find out how big their “raise” will be in 2026.

The Social Security cost-of-living adjustment (COLA) countdown is about to kick into overdrive. But you don’t have to sit on pins and needles in anticipation of the official COLA announcement on Oct. 15, 2025, to have a pretty good feel for what the increase will be.

Image source: Getty Images.

If you want to know how big of a Social Security benefit increase to expect, probably the best place to turn is The Senior Citizens League (TSCL). This nonprofit organization has advocated for seniors since 1992, initially as part of The Retired Enlisted Association and then as an independent entity beginning in 1994.

TSCL developed a sophisticated statistical model that projects the next Social Security COLA. This model is updated monthly. It incorporates inflation and unemployment data, as well as the interest rates set by the Federal Reserve.

Earlier this month, TSCL announced its final prediction for the 2026 Social Security COLA. The organization projects an increase of 2.7%, a little higher than the 2.5% COLA given in 2025. It’s also slightly above the average benefit adjustment over the last 20 years of 2.6%.

How much additional money will this COLA give retirees? It depends on your current benefit amount, of course. However, the average increase will be $54 per month if TSCL’s model is right.

The Social Security Administration (SSA) already has most of the data it needs to calculate next year’s COLA. It will receive the last piece on Oct. 15 when the U.S. Bureau of Labor Statistics (BLS) releases its inflation numbers for September.

SSA doesn’t use the most widely followed inflation metric in the BLS report, the Consumer Price Index. Instead, the agency bases the annual Social Security COLA on a different statistic — the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). As its name indicates, this index measures how much prices have increased for blue-collar workers in urban areas.

The COLA is calculated by determining the percentage increase (if any) between the CPI-W for the third quarter of the current year and the CPI-W in the third quarter of the previous year. SSA only needs to plug in the CPI-W for September to crunch the numbers.

Could the actual 2026 COLA that will be announced on Oct. 15 differ from the 2.7% predicted by TSCL? Absolutely. Inflation could be higher in September than anticipated, perhaps due to the impact of tariffs making their way through the U.S. economy. On the other hand, the effects of tariffs could be more muted than TSCL’s model projects, resulting in a lower COLA. Either way, TSCL’s projected number will probably be close to the actual 2026 COLA.

Retirees shouldn’t count on having an additional 2.7%, give or take a couple of percentage points, reach their bank accounts, though. There’s one “gotcha” that will likely reduce how much extra money you’ll receive.

Most retirees ages 65 and older have their Medicare premiums automatically deducted from their monthly Social Security benefit payments. Unfortunately, your Medicare Part B premiums will almost certainly be much higher than the expected 2.7% Social Security increase.

The Medicare Trustees project that Part B premiums will rise by 11.6%. This translates to an extra expense of $21.50, enough to wipe out much of the average retiree COLA of $54. The annual Medicare Part B deductible will also likely jump by $31 to $288 next year.

The countdown is on for finding out the exact amounts for the 2026 Medicare Part B premiums and deductibles, too. While the numbers will probably be announced in October, retirees might not learn how their pocketbooks will be impacted as soon as they learn what their Social Security COLA will be.

Renewed interest in nuclear energy has Centrus stock has soaring.

Centrus Energy (LEU -2.19%) has been one of several nuclear energy stocks that have crushed the market in 2025. Compared to the S&P 500‘s impressive 13% gain so far this year, Centrus’ stock is up about 295% in 2025 at the time of writing — and over 450% year over year.

At that yearly gain, you’d be forgiven if you thought Centrus was training large language models (LLMs) instead of enriching uranium. And yet its growth potential does have an indirect connection with artificial intelligence (AI) in that its fuel could help power the data centers behind the boom.

With the first American-owned enrichment plant to start production in decades, Centrus finds itself at the center of an industry that hasn’t seen this much interest since the 1970s. But does that make this growth stock a no-brainer buy today?

Ground floor side view of the HALEU cascade. Image source: Centrus Energy.

Centrus operates two main businesses. The first is supplying low-enriched uranium (LEU) for today’s reactors. And the second is providing technical services, including a Department of Defense (DOE) contract, to produce high-assay low-enriched uranium (HALEU) for advanced reactors.

Of the two, the HALEU production likely offers more growth opportunity long-term. That’s because many next-generation reactors — like small modular reactors (SMR) — are increasingly being designed to run on this fuel.

In Piketon, Ohio, it runs the only U.S.-owned enrichment facility licensed to make HALEU. Emphasis there on only: Centrus currently holds the only license from the Nuclear Regulatory Commission to enrich uranium above 5%. If HALEU does end up becoming the preferred fuel for future reactors, Centrus could have a first-mover advantage in the U.S. for producing it.

But don’t overlook the last part of that sentence. Although no other U.S. company is licensed to produce HALEU, there are several companies producing it worldwide, some at a much larger scale than Centrus.

One is a Russian company, Tenex, a subsidiary of the state-owned Rosatom. The funny thing about Tenex: It has a supply contract with Centrus, meaning that some of Centrus’ LEU — which it sells to reactors in the U.S. — comes from Russian supplies. Any geopolitical risk — or a refusal on the part of Tenex to continue supplying Centrus — could hurt the company’s ability to meet obligations.

That hasn’t happened yet, however, and Centrus is likely aware of this dependence. But until it can achieve self-sufficiency in production, the Russian link to LEU remains an uncomfortable fact, especially since Tenex is also the world’s go-to for HALEU.

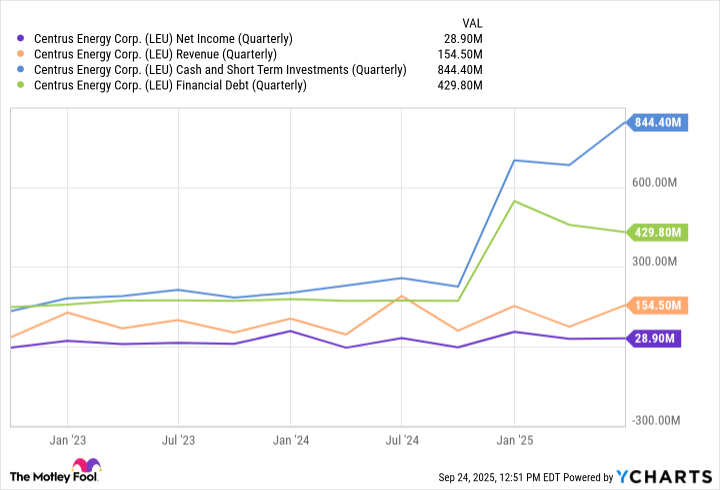

Usually, when I write about advanced nuclear stocks, the phrase “pre-revenue” always finds a place near “balance sheet.” In this way, Centrus is ahead of the pack in that it’s not only selling something (fuel) but it’s actually profitable.

In the second quarter of 2025, it reported net income of $28.9 million, a slight decrease from $30.6 million a year ago. What stood out, however, was its gross profit of about $54 million — an increase of 48% from last year — which shows a stronger margin even as revenue declined.

LEU Net Income (Quarterly) data by YCharts

The company also ended the quarter with a hefty consolidated cash balance of $833 million and a backlog of $3.6 billion that extends to 2040.

Centrus offers a rare, U.S.-based play on nuclear fuel independence at a time when governments are rethinking energy. And yet it’s not an obvious buy, at least for those who want to stay away from volatility.

Bulls will point to a few major tailwinds at Centrus’ back.

The first is policy. In May 2025, President Donald Trump signed a flurry of executive orders aimed at boosting the country’s nuclear energy capacity, including calls for a stronger domestic supply chain of nuclear fuel. That puts Centrus in a strong position to benefit from government funding.

Meanwhile, international interest, like Centrus’ recent memorandum of understanding with Korea Hydro & Nuclear Power, could be stirring, especially as concerns rise over Russia’s dominance of the global nuclear fuel market.

But even the bulls have to acknowledge that Centrus, though it has support, doesn’t have the industrial capacity to produce enriched uranium at scale. Until expansion efforts at its Piketon plant are complete, or new capacity is turned online, Centrus will remain pretty supply-constrained for now.

Investors interested in Centrus’ stock should also take note of its rich valuation. At today’s price, the stock trades at 76 times forward earnings, which is several times higher than the energy sector writ large (about 16).

Clearly, investors are expecting growth. Whether or not they get it will depend on Centrus’ ability to scale enrichment capacity.

It may go down as one of the best investments Buffett and Munger ever made.

Over 35 years ago, Warren Buffett told investors, “When we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever.” Since then, he’s bought and sold dozens of stocks for Berkshire Hathaway (BRK.A 0.55%) (BRK.B 1.06%), proving that even the Oracle of Omaha doesn’t have a perfectly clear crystal ball.

Even when Buffett has made extremely successful equity investments, he’s often had reason to sell at least some of Berkshire’s stake — either to maintain a more balanced portfolio, or sell a stock that’s become overvalued, or for any number of other reasons. Those are factors that have come to the fore recently for Buffett and his team of investment managers. Berkshire Hathaway has sold more marketable equities than it bought in each of the last 11 quarters.

Those sales include one stock that Berkshire first bought in 2008 and will go down as one of Buffett’s (and Munger’s) most successful investments of all time.

Image source: The Motley Fool.

In late September 2008, as the global stock market was reeling amid the Great Recession, Buffett and Munger took the opportunity to buy a 10% stake in a Chinese auto company called BYD (BYDDY -0.94%) (BYDD.F -1.20%). They gradually increased Berkshire’s stake in the business, reaching about 20% at one point. Today, the company is the largest EV manufacturer in the world, surpassing Tesla.

It was Vice Chairman Charlie Munger who brought the company to Buffett’s attention. He found CEO Wang Chuanfu’s engineering and managerial skills extremely impressive. He had developed one of the largest battery manufacturers in the world before transitioning to the automotive business in the early 2000s. With its battery expertise and other vertically integrated components made through acquisitions, BYD looked poised to do well in the nascent electric vehicle market.

Sure enough, BYD has developed a broad lineup of vehicles sold around the world. Its global sales of fully electric vehicles surpassed Tesla’s in the fourth quarter of 2023 and for the full year of 2024. It’s not just success in its home country, either. BYD’s European sales surpassed Tesla’s in April this year. Management aims to sell half of its cars outside of China by 2030. It’s worth noting BYD has yet to enter the U.S. market due to tariffs and the political environment.

It’s no surprise, then, that BYD’s stock price has soared amid its success. With the acceleration in sales over the last few years, BYD’s stock is up more than eightfold since the start of 2020.

Buffett started decreasing Berkshire’s stake in BYD starting in August 2022, after Berkshire’s initial investment had already climbed about 20-fold. At one point, Berkshire’s shares were worth $9 billion. Based on financial reports from Berkshire Hathaway subsidiary, Berkshire Hathaway Energy, the company gradually sold off shares until completely divesting its stake in the first quarter of this year.

Buffett may have missed the absolute peak of BYD’s stock price, but shares have certainly struggled in the latter half of the year, as Chinese competitors take market share from its domestic business. BYD’s August deliveries were flat year over year, as were July’s. Not only has the intense domestic competition hurt unit sales, but it’s also hurt BYD’s margins.

But the company stands at a distinct advantage over the competition thanks to its significant vertical integration. As mentioned, BYD is one of the leading battery manufacturers in the world. That, in and of itself, is a significant advantage over other EV makers who need to source batteries from third parties. But BYD also makes many other components in its vehicles, including the motors, semiconductors, and practically everything else except the tires and glass.

That allows the business to adapt quickly and maintain better margins than its competitors. With plans for an aggressive international expansion, it’ll have to replicate its manufacturing capabilities all around the world. But management has proven quite adept at building systems and scaling them.

After the pullback in price, investors can buy shares for just 1 times sales and less than 16 times forward earnings expectations. That’s an attractive price for the leader in a growing industry, even if it’s seeing some pressure from the competition weighing on revenue growth and margins. It’s certainly a better valuation than investors could get with Tesla. While Buffett may have sold out of the stock, it might still deserve a spot in your portfolio.

Adam Levy has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway and Tesla. The Motley Fool recommends BYD Company. The Motley Fool has a disclosure policy.