Dogecoin Is Falling Today. Should You Buy the Dip?

Key Points

-

The U.S. government could soon shut down if legislators fail to reach a deal.

-

The market is slightly down as investors anticipate a shutdown, with riskier assets like Dogecoin being hit harder.

Dogecoin (CRYPTO: DOGE) fell on Tuesday, down 4.2% as of 1:12 p.m. ET, as measured from 4 p.m. on Monday. The move comes as the S&P 500 (SNPINDEX: ^GSPC) and the Nasdaq Composite (NASDAQINDEX: ^IXIC) lost 0.2% and 0.3%, respectively.

The meme coin is falling with much of the market as investors anticipate a government shutdown. More speculative assets like Dogecoin tend to see outsized drops when the market is uneasy.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Crypto investors brace for a shutdown

While a U.S. government shutdown could be avoided, the clock is ticking. Legislators need to pass a funding bill by the end of the day, but both sides of the aisle are playing hardball and refusing to budge. The market seems to be anticipating a shutdown.

Image source: Getty Images.

It wouldn’t be the first time — there have been 14 shutdowns since 1980 — but a shutdown introduces uncertainty, which often leads to a dip in the market. Investors like stability.

Dogecoin is a very risky asset

Dogecoin’s drop today outpaced most of the crypto market because it’s a meme coin with no real value. It is highly speculative and built on hype. It really shouldn’t be viewed as a serious investment; it is more of a bet.

While today’s dip could look like an opportunity to buy, I wouldn’t. Dogecoin can fall a lot further. A more serious market event could cause Dogecoin to plummet.

Investors should instead look to cryptos with a proven track record of value and projects with innovative technology. Bitcoin and Ethereum are much smarter plays.

Should you invest $1,000 in Dogecoin right now?

Before you buy stock in Dogecoin, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Dogecoin wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $650,607!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,114,716!*

Now, it’s worth noting Stock Advisor’s total average return is 1,068% — a market-crushing outperformance compared to 190% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 29, 2025

Johnny Rice has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Bitcoin and Ethereum. The Motley Fool has a disclosure policy.

Financial Institutions’ Top Concern Is Compliance

Maintaining older systems slows advancements towards real-time payment and regulatory compliance.

A Bottomline report released at Sibos on Monday shows that 91% of banks and other financial institutions expect compliance challenges in the coming year, as they manage regulations, customer expectations, and fraud prevention.

The global report, “The Future of Competitive Advantage in Banking & Payments,” highlights legacy systems as a significant obstacle and is based on interviews with 220 financial institutions. Slightly more than four in ten respondents cited these systems as the biggest barrier to real-time payments, and 31% mentioned that they hinder regulatory compliance.

Operational resilience remains a key concern, with 37% of those surveyed highlighting the importance of using alternative payment methods to prevent primary system failures. Modernization is a key focus, with 32% concentrating on new payment channels and another 32% on enhancing cross-border strategies.

A significant “cash visibility gap” persists: 50% lack an end-to-end view due to disparate systems, and 45% report incomplete cash positioning despite partial automation, underscoring the need for comprehensive cash visibility and real-time balance tracking.

Prioritization of Swift Global Payments Innovation (GPI) surged from 35% in 2024 to 56% in 2025. This addresses slow or unclear payment speeds, identified by 61% as a top pain point, through real-time tracking and enhanced visibility.

Accuracy in sanctions screening is paramount, with 57% highlighting it as the most important factor when selecting a solution. This relates to the 37% who cite high volumes of false positives as their biggest challenge, hindering operational efficiency.

Vitus Rotzer, Bottomline’s Chief Product Officer for Financial Messaging, warns that companies not yet implementing ISO 20022 messaging are significantly behind schedule.

“It is crucial for companies to understand that ISO implementation goes beyond a mere technical upgrade. Most have already handled the technical aspects, but truly leveraging the data offers far greater advantages,” he says. “The more detailed and enhanced data available, the greater the potential for identifying fraud patterns and other critical insights. Companies not utilizing this rich data are at a distinct disadvantage, effectively starting behind their competitors. The value lies in fully exploiting the enhanced information that ISO provides.”

CoreWeave Is Soaring Again. Time to Buy?

Meta’s latest artificial intelligence (AI) capacity commitment lights a fire under CoreWeave shares, but expectations are sky-high.

Shares of CoreWeave (CRWV 12.34%) jumped after the company filed an 8-K detailing a fresh order with Meta Platforms.

The agreement initially commits up to $14.2 billion of spend through Dec. 14, 2031, “with the option to materially expand its commitment through 2032 for additional cloud computing capacity”– sending the GPU-cloud provider’s stock higher as investors digested the scale and duration of the commitment. Shares climbed as much as 16.4%, but were up about 13% as of noon ET.

Image source: Getty Images.

Massive dealmaking

The new order sits under an existing master services agreement and provides Meta access to CoreWeave’s reserved artificial intelligence (AI) compute capacity. In plain English, Meta is locking in a lot of high-end GPU cloud for years, with room to grow. That should help CoreWeave diversify beyond its biggest ecosystem relationships and improve revenue visibility through 2031, with a possible step-up in 2032. It also signals that hyperscale AI buyers continue to secure multiyear capacity, a trend that can move shares quickly when deals are disclosed.

Importantly, this Meta news comes just days after CoreWeave and OpenAI expanded their own agreement by up to $6.5 billion. That Sep. 25 update increased OpenAI’s long-term commitments with CoreWeave and extended the relationship through 2031. Taken together, the two back-to-back announcements highlight how CoreWeave is steadily locking in multibillion-dollar, multiyear partnerships with the most important AI developers.

Valuation and the long view

The business clearly has momentum — and today’s Meta order strengthens the backlog and diversifies demand. That said, after a string of headline contracts and a sharp rebound in the share price, the stock appears priced for perfection. We’re talking about a cyclical company with a market capitalization of $68 billion that is still reporting losses.

Of course, we can’t rule out a scenario in which fundamentals do exceed expectations. But this will depend on the speed of future capacity ramps and market demand over the next five years — two very unpredictable factors.

Overall, in a capital-intensive, fast-moving market where supply chains, customer concentration, and hardware cycles can shift quickly, patience is probably a good idea. At a lower price, the stock might make sense. But after its recent run-up, it’s probably worth staying on the sidelines.

Daniel Sparks and his clients have no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms. The Motley Fool has a disclosure policy.

Micron Gives Investors More Evidence That The Artificial Intelligence (AI) Boom Is Here to Stay

You’re reading a free article with opinions that may differ

from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to

get instant access to our top analyst recommendations, in-depth research, investing resources,

and more. Learn More

Why Shares of CoreWeave Are Soaring Today

CoreWeave just struck a new multibillion-dollar, multiyear deal.

Shares of cloud infrastructure player CoreWeave (CRWV 12.90%) were trading 15% higher as of 10:50 a.m. ET Tuesday. The stock price jump came after the company announced a new $14.2 billion deal with Meta Platforms.

Continuing to strike deals

In a regulatory filing Tuesday morning, CoreWeave announced that it had expanded its deal with Meta Platforms: It will provide cloud computing capacity to the social media giant through 2031 for $14.2 billion. Meta also has “the option to materially expand its commitment through 2032 for additional cloud computing capacity under the Order Form.”

Image source: Getty Images.

CoreWeave builds and operates data centers equipped with the latest graphics processing units (GPUs) from Nvidia, and rents out capacity on its machines largely to companies that use it to power and train artificial intelligence (AI) applications. Many of the hyperscalers in the “Magnificent Seven” have high demand for this type of processing capacity. “The agreement underscores that behind every AI breakthrough are the partnerships that make it possible,” a CoreWeave spokesperson told CNBC.

CoreWeave has had a good couple of weeks. It recently expanded its deal with OpenAI, the company behind ChatGPT, for an additional $6.5 billion. Meta CEO Mark Zuckerberg has previously vowed to spend hundreds of billions of dollars on new data centers to help power his company’s AI ambitions.

Good as long as the party continues

As long as companies keep spending on AI infrastructure, CoreWeave is going to benefit. How long the party will continue is another question. CoreWeave is fast approaching a $70 billion market cap, but it is not yet profitable and trades at about 13 times forward expected sales. It also has a debt-to-equity ratio of more than 8.3, which is high.

All of this makes me a bit cautious on CoreWeave, despite the high-profile agreements it has signed recently. Due to the state of its balance sheet, its valuation, and the possibility of a slowdown in AI capital expenditures, I wouldn’t recommend investing too much of your portfolio in the stock.

Bram Berkowitz has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms and Nvidia. The Motley Fool has a disclosure policy.

Could This Beaten-Down Stock Help You Become a Millionaire?

The company would need to maintain the strong momentum it’s had this year for a long time.

Becoming a millionaire through stock investing is possible, but it requires patience, discipline, and the acumen to make informed investment choices. Not every company can generate the kind of returns over the long run that will help you achieve that goal — in fact, most probably won’t.

Buying ETFs that track the performance of major indexes is a low-risk strategy, but perhaps you can do better by picking out stocks that can post superior gains. It’s even better to invest in companies that have been beaten down, but still boast significant upside potential and attractive long-term prospects.

That brings us to CRISPR Therapeutics (CRSP 1.15%), a mid-cap biotech. The company’s shares have slumped more than 60% from all-time highs achieved in early 2021. Does it have what it takes to deliver competitive-enough returns to help you become a millionaire?

Image source: Getty Images.

Banking on pipeline progress

Smaller, unprofitable biotech companies, such as CRISPR Therapeutics, thrive on strong clinical and regulatory progress. The company’s shares could soar over the next five years if it impresses the market in those areas.

CRISPR’s current leading pipeline candidates include CTX310, a gene-editing therapy being developed to lower LDL (“bad”) cholesterol and triglycerides (TGs, a type of fat). Its goal is to inactivate the ANGPTL3 gene, which plays a role in regulating both. While they’re significant risk factors for various types of common heart diseases, there are few treatment options aimed at reducing LDL and TGs.

CTX310 is progressing well in clinical trials so far. In an ongoing phase 1 study, the medicine led to significant reductions in both LDL and TG levels. There are 40 million patients in the U.S. alone who have high levels of either or both. Although CRISPR Therapeutics will focus on high-risk patients, the commercial opportunity is vast. That’s why consistent positive data should jolt the stock, as it already has this year; shares are up by 48% this year thanks to progress with CTX310.

Elsewhere, CRISPR’s CTX320 is being developed to help decrease levels of liporotein(a), which is a risk factor for heart attack and strokes. Therapy options here are also limited. In other words, CRISPR Therapeutics is developing potentially breakthrough medicines for conditions with high unmet needs and large patient populations.

Its gene-editing platform already has an approved product on the market: Casgevy, which it created and developed in collaboration with Vertex Pharmaceuticals. Although CRISPR Therapeutics doesn’t generate much revenue from it yet, Casgevy was a significant milestone, as no such therapy had received approval before; the approval demonstrated that the biotech’s CRISPR-based gene-editing medicines can clear regulatory hurdles.

What’s more, CTX310 and CTX320 look even more commercially viable than Casgevy. Here’s why. Casgevy is an ex vivo gene-editing therapy, which means the process to administer it involves collecting a patient’s cells, manipulating and editing them, then reinserting them back into the patient. The process is highly complex and can only be done in authorized treatment centers.

CTX310 and CTX320, in contrast, are both in vivo medicines that bypass the cell collection process and are administered via intravenous infusions. This is another important reason that their progress could lead to massive gains for CRISPR Therapeutics in the next five years or so.

A millionaire-maker stock?

What about beyond the end of the decade? Becoming a millionaire through stock investing typically requires at least a couple of decades, and often more. Can CRISPR Therapeutics perform well for that long? It’s hard to say. The company has even more investigational therapies in its pipeline that could make progress in the long term. And its highly innovative gene-editing platform could produce even more gems.

That said, there’s a significant risk involved. CRISPR Therapeutics could face clinical and regulatory setbacks. If these issues arise with its leading candidates in the next few years, they’re likely to affect its stock price, especially considering it currently operates at a loss. Competing medicines are also being developed by other companies, which could reduce its commercial opportunity later.

CRISPR Therapeutics has significant upside potential, but investors should note that the stock carries a higher level of risk. If you’re comfortable with volatility, you might consider initiating a small position in the company. However, it shouldn’t be one of the largest holdings in a well-diversified portfolio that’s designed to help average investors become millionaires.

Is Growth Stalling for MP Materials Investors?

MP Materials was in the right place at the right time, but there is a lot of hard work to be done from here.

In the second quarter of 2025, MP Materials‘ (MP -0.76%) revenue declined sequentially from the first quarter. Its adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) and earnings both fell deeper into the red. That’s not a change that most investors will find pleasing to read, but the company’s future remains very bright.

Here’s why MP Materials’ growth isn’t stalling, even though there’s a lot of heavy lifting for the company to do from here.

What does MP Materials do?

MP Materials mines for and processes rare earth metals. These metals are vital to the technology sector and get used in everything from cellphones to missiles. That said, MP Materials is really best viewed as a mining company.

Image source: Getty Images.

That’s important because mining is a very capital-intensive business. A company has to find a place to mine, get approval for it, build the mine, operate it (in this case also process the output into usable rare earth metals products), and then return the mine back to its pre-mine state once it is depleted. MP Materials is really just at the very beginning of this process, which is the most expensive from a capital investment point of view.

That said, MP Materials finds itself in a very enviable position thanks to geopolitical issues. The new U.S. tariff regime has led to friction with China, which is the world’s largest producer of rare earth metals. China has been very willing to limit access to these vital metals as it vies for the best tariff deal. That, essentially, has put the world on notice that China can’t be counted on as a supplier of rare earth metals.

MP Materials has a huge opportunity to exploit

MP Materials didn’t just magically find itself here. The company’s specific goal was to create a rare earth metals supplier that is located in an economically and politically stable region. The company is exactly where it wanted to be and that is leading to a huge influx of cash.

The U.S. government has invested in MP Materials. Apple has inked a sizable deal with the company. And, after the stock advance following these two events, the company was able to sell shares into the market at attractive prices. Demand was so strong for MP Materials’ stock that it was able to sell more shares than it had originally planned.

This is all very good news from a growth perspective. It means that MP Materials has the cash it needs to keep building out its business. And that, in turn, means that it still has a huge growth opportunity ahead that will be easier to achieve since access to capital is less of a constraint. If anything, the growth opportunity isn’t stalling out, it is getting more attractive.

Don’t expect instant results at MP Materials

Despite the positives here, there’s still one small problem. MP Materials is a young miner that is building out its business. That takes time and will likely mean red ink for at least a while longer.

MP Materials stock is up over 350% over the past year, with most of that gain coming after the U.S. government’s investment in the company. So while the business has huge growth potential, a lot of that appears to have been priced into the stock in a very short period of time. Investors should probably tread cautiously with MP Materials, which looks like it has become a story stock at this point.

If the story doesn’t happen as expected (including as quickly as expected), the shares could quickly turn lower again even if the long-term opportunity for the business remains robust.

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple. The Motley Fool recommends MP Materials. The Motley Fool has a disclosure policy.

Here’s What $25K Earns in a Big Bank vs. a High-Yield Account

A standout option right now is the LendingClub LevelUp Savings account. It currently pays 4.20% APY with $250+ in monthly deposits and even comes with a debit card linked to your savings. You can read our full LendingClub LevelUp Savings review here for all the details.

LendingClub LevelUp Savings

Member FDIC.

APY

4.20% APY with $250+ in monthly deposits

Rate info

Circle with letter I in it.

LevelUp Rate of 4.20% APY applied to full balance with $250+ in deposits in Evaluation Period. Otherwise, accounts earn Standard Rate of 3.20% APY. LevelUp Rate applies for first two statement cycles. Rates variable & subject to change at any time. See terms: https://www.lendingclub.com/legal/deposits/levelup-savings-t-and-cs

Min. To Earn APY

$0 to open, $250 cumulative monthly deposits for max APY

- Competitive APY

- No fees

- Easy ATM access

- Unlimited number of external transfers (up to daily transaction limits)

- Requires you to make monthly deposits to earn the best APY

- ACH outbound transfers limited to $10,000 per day for some accounts

- No branch access; online only

The LendingClub LevelUp Savings account has a lot to offer. At the top of the list is its high APY, though you must deposit monthly to earn the best rate. Next is zero account fees, a strong and straightforward perk. Finally, you get a free ATM card, which you can use to withdraw from thousands of ATMs nationwide. Interested? You can open an account with $0.

Why I park my $25K in an HYSA

I keep about $25,000 in emergency funds and short-term savings. This is the cash I’d tap if my car breaks down, a medical bill pops up, or I want to book a family trip. I need it safe, liquid, and ready to go.

That’s exactly what an HYSA is built for. It’s federally insured (FDIC insurance up to $250,000), so my money is protected even if the bank itself fails. At the same time, it’s still earning me hundreds each year in interest.

Another thing I love: my HYSA doesn’t nickel-and-dime me. I pay no monthly fees, there’s no minimum balance requirements, and no hidden charges. It’s the opposite of my old big-bank account, where I felt like I was paying them just for the privilege of parking my cash there.

And the tech is better, too. The app is clean, transfers are quick, and my cash is back in my checking account within a day or two if I need it.

Bottom line

When you see the numbers side by side, it’s hard to justify leaving big chunks of money in a traditional savings or checking account.

Whether you’ve got $25,000 or even just $1,000, high-yield savings accounts are one of the easiest wins in personal finance.

Stop earning pennies and start earning hundreds. Check out the best high-yield savings accounts today and see how much your cash could earn.

How Much Is the Required Minimum Distribution (RMD) if You Have $500,000 in Your Retirement Accounts?

Key Points

-

You must begin taking required minimum distributions the year you turn 73.

-

The amount of your RMD will depend on your age and account value at the end of the previous year.

-

You could face a penalty of up to 25% of the RMD if you don’t take them.

Aside from allowing you to proactively save and invest for retirement, the major benefit of using retirement accounts like a 401(k) or traditional IRA is the up-front tax break you get by reducing your taxable income with contributions. The downside is that you must pay taxes on withdrawals in retirement.

To avoid situations where someone doesn’t make any withdrawals so they don’t ever have to pay taxes, the IRS enacts required minimum distributions (RMDs), which begin the year you turn 73. The exact amount of these RMDs will depend on your current age and account balance at the end of the previous year.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Image source: Getty Images.

How to calculate your required minimum distribution

You can calculate your RMD in three steps:

- Find your account balance at the end of the previous year.

- Look for the life expectancy factor (LEF) corresponding to your age and marital status. Most people will use the uniform lifetime table, except those whose sole beneficiary is their spouse who is more than 10 years younger than them.

- Divide your account value by your LEF.

For those using the uniform lifetime table, below are the RMDs for people with $500,000 in a retirement account as of the end of 2024:

| Age | Life Expectancy Factor | Required Minimum Distribution |

|---|---|---|

| 73 | 26.5 | $18,868 |

| 74 | 25.5 | $19,608 |

| 75 | 24.6 | $20,325 |

| 76 | 23.7 | $21,097 |

| 77 | 22.9 | $21,834 |

| 78 | 22.0 | $22,727 |

| 79 | 21.1 | $23,697 |

| 80 | 20.2 | $24,752 |

Data source: IRS. RMDs rounded to the nearest dollar.

It’s important to be aware of your RMDs because not taking them (whether accidentally or intentionally) will result in a 25% penalty of the amount you failed to withdraw. If you correct your mistake within two years, this penalty will be reduced to 10%.

The $23,760 Social Security bonus most retirees completely overlook

If you’re like most Americans, you’re a few years (or more) behind on your retirement savings. But a handful of little-known “Social Security secrets” could help ensure a boost in your retirement income.

One easy trick could pay you as much as $23,760 more… each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we’re all after. Join Stock Advisor to learn more about these strategies.

View the “Social Security secrets” »

The Motley Fool has a disclosure policy.

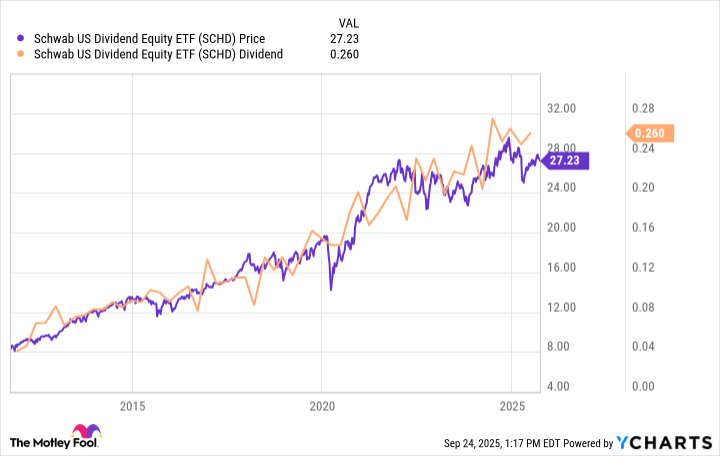

Don’t Miss Out on This $30-Trillion Dollar Sector: The Top ETF to Buy

Roughly half of all U.S. stocks pay dividends, making it a huge investable universe, with this one ETF letting you buy the best of the best.

The U.S. market is huge, with a combined market cap of around $63 trillion. There are all sorts of different ways you can slice and dice the U.S. stock market, with the top ETFs offering plenty of variety. But if you are a dividend lover, you are only interested in about half of the total universe, which cuts your investable universe down to “just” $30 trillion or so.

If that’s still a little daunting (it should be), then you need to get to know Schwab US Dividend Equity ETF (SCHD -0.39%). Here’s why it could be the top dividend exchange-traded fund (ETF) for you to buy.

Image source: Getty Images.

What does Schwab US Dividend Equity ETF do?

Schwab US Dividend Equity ETF tracks the Dow Jones U.S. Dividend 100 Index. Although the exchange-traded fund technically doesn’t do anything other than mimic the index, the index and the ETF are, in practice, doing the same things and can be discussed interchangeably. From here on out, the ETF will be discussed and not the index.

The first step in creating Schwab US Dividend Equity ETF’s portfolio is to winnow down the $30 trillion worth of dividend stocks to a more manageable number. To do this, only stocks that have increased their dividends for at least 10 years are examined for further consideration. Also eliminated are real estate investment trusts (REITs), because of their unique corporate structure that emphasizes dividends and avoids corporate-level taxation.

Once a core investable universe is created, Schwab US Dividend Equity ETF builds a composite score for each of the remaining companies. The score includes cash flow to total debt, return on equity, dividend yield, and a company’s five-year dividend growth rate. Essentially, the ETF is trying to find financially strong companies that are well run and that return material value to shareholders via regular, and growing, dividend payments. The 100 companies with the best composite scores are included in the ETF.

The ETF uses a market cap weighting approach, so the largest companies have the biggest impact on performance. And the list of holdings is updated annually. That’s a lot of work, but the expense ratio is a very modest 0.06%. At the end of the day, Schwab US Dividend Equity ETF is doing what most dividend investors would do if they bought stocks on their own at a cost that is very close to free by Wall Street standards.

Why you should buy Schwab US Dividend Equity ETF

Some caveats are important here. You can easily find higher-yielding ETFs. You can easily find ETFs that have had better price appreciation. Simply put, Schwab US Dividend Equity ETF isn’t a perfect investment choice for every investor. But it provides a very good balance between yield, price appreciation, and dividend growth over time.

As the chart above highlights, the dividend and the ETF’s market price have both trended generally higher since its inception in October 2011. Now add in the well-above-market dividend yield of around 3.7% today, and the story gets even better. For reference, that’s just over three times greater than what you’d collect from an S&P 500 index (^GSPC 0.26%) tracking ETF like Vanguard S&P 500 ETF (NYSEMKT: VOO).

And since Schwab US Dividend Equity ETF’s portfolio is regularly updated, you don’t need to think about what’s in the portfolio. How it invests is more important than what it owns at any given moment. Its holdings will naturally shift along with the market over time. In other words, you just have to make one buy decision and let the ETF do the rest of the work for you.

A simple “one and done” ETF for dividend investors

There are a lot of public companies in the United States. And around half of those public companies pay dividends. Schwab US Dividend Equity ETF lets you cut through the $30 trillion worth of dividend noise to focus on just 100 of the best dividend stocks. And it basically picks dividend stocks the way a dividend investor would do it, looking for quality companies with growing businesses, attractive yields, and growing dividends. If you love dividends, Schwab US Dividend Equity ETF could easily be the top ETF for you.

What Is One of the Best Cloud AI Stocks to Buy Right Now?

This cloud company just signed massive deals with several leading AI companies.

Investment in computing infrastructure to support artificial intelligence (AI) is reshaping the cloud computing market, and Oracle (ORCL -0.32%) might be the best cloud stock to bet on. Its focus on offering the greatest customer flexibility and processing speeds for AI applications is driving accelerating growth that could send the stock higher.

Image source: Getty Images.

World-class AI companies are choosing Oracle

Oracle’s cloud infrastructure (OCI) segment posted a revenue increase of 55% year over year last quarter, up from 52% in the previous quarter. Oracle signed deals with multiple tech giants, including ChatGPT’s OpenAI, sending its remaining performance obligations up 359% year over year to $455 billion.

These results show demand for AI training, inference, and data analytics is accelerating, and Oracle is in pole position. It has become the go-to cloud provider for AI workloads. Oracle’s customers can run its cloud services on other platforms from Amazon, Google, and Microsoft, providing the utmost flexibility.

The spike in remaining performance obligations shows Oracle’s ability to scale rapidly. Leading AI companies are choosing Oracle to train their AI models due to its ability to build large data centers that are faster and more cost-efficient than any of its competitors.

Analysts expect Oracle’s earnings to grow 15% annually in the coming years, but these estimates have been trending up. Management expects its cloud infrastructure business to reach $144 billion in revenue in four years, up from $18 billion this year. This should support more gains for Oracle investors.

John Ballard has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Microsoft, and Oracle. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Tesla, Rivian, and Lucid Will Have Their Fortunes Changed Forever Today, Sept. 30, Courtesy of President Donald Trump

President Trump’s “Big, Beautiful Bill” is reshaping the electric-vehicle (EV) landscape.

When a new president enters office, it’s not uncommon for changes to take place, either through the signing of bills into law or via executive orders. Since President Donald Trump was inaugurated a little over eight months ago, we’ve witnessed a slew of adjustments made to Social Security, as well as the passage of his flagship tax and spending law, the “Big, Beautiful Bill.”

While Trump’s big, beautiful bill introduced a number of tax breaks for select groups, including a higher standard tax deduction for eligible seniors from 2025 through 2028, and partial deductions for tips and overtime pay for eligible workers during the same four-year timeline, it also removed some important benefits.

President Trump delivering his State of the Union address. Image source: Official White House Photo.

Specifically, Donald Trump’s law changes the fortunes of the electric-vehicle (EV) industry and its leading pure-play manufacturers, which includes Tesla (TSLA 0.61%), Rivian Automotive (RIVN -2.15%), and Lucid Group (LCID 0.56%), as of today, Sept. 30.

EV makers bid adieu to an important dangling carrot

Among the laundry list of tax and credit adjustments in the president’s big, beautiful bill is a newly shortened timeline that ends the $7,500 tax credit consumers received when purchasing a qualifying new EV or plug-in hybrid, as well as the $4,000 credit when buying a used EV. This EV credit was available to new vans, SUVs, and trucks priced below a manufacturer’s suggested retail price (MSRP) of $80,000, as well as new sedans with an MSRP of no more than $55,000.

Though this credit (officially known as the Clean Vehicle Credit) was initially slated to end in 2032, based on the Inflation Reduction Act, Donald Trump’s big, beautiful bill brings this new EV purchase credit to an end today, Sept. 30. Qualifying new vehicles purchased after today will no longer be eligible for the $7,500 credit.

This EV credit applied to a significant percentage of the vehicles Tesla sells, including its Model 3 Sedan, all-wheel drive Model X SUV, single and dual motor Cybertruck, and multiple variants of the Model Y SUV. While Rivian’s and Lucid’s EVs are generally priced above the MSRP range where tax credits end, both companies had been angling leases of upcoming models as a way to take advantage of the $7,500 EV credit.

This EV credit was akin to a dangling carrot that allowed pure-play electric-vehicle manufacturers to be more price-competitive with internal combustion engine (ICE) vehicles. Undercutting traditional ICE vehicles on price is viewed as a borderline necessity with EV charging infrastructure still somewhat lacking on a nationwide basis.

Without this upfront cost advantage, it’s likely that future buyers will opt for traditional gas- and diesel-powered vehicles due to the availability of ICE fueling infrastructure and opportunity cost. Whereas it takes just a few minutes to refuel an ICE vehicle, it can take an hour to a full day, depending on the type of charger used, to juice up an EV.

Image source: Tesla.

But wait — there’s more bad news

However, ending this lucrative tax credit that incentivized the purchase of EVs isn’t the only way Donald Trump’s big, beautiful bill is disrupting pure-play EV manufacturers.

When the president signed his flagship tax and spending bill into law on July 4, 2025, it put an end to corporate average fuel economy (CAFE) fines, as well as retroactively eliminated fines for 2022 model years and all subsequent years.

CAFE regulations represent the standard of how far vehicles must travel on a gallon of fuel. These figures, which are set by the National Highway Traffic and Safety Administration, are designed to promote more fuel-efficient vehicles over time and lessen the reliance on fossil fuels. Automakers that failed to meet these standards were subject to fines. With CAFE civil penalties removed, courtesy of Trump’s law, there’s no longer any financial incentive for automakers to meet sky-high mile-per-gallon targets.

This is almost certain to have an adverse impact on the ability of Tesla, Rivian Automotive, and Lucid Group to generate profits.

Government agencies provide automotive regulatory credits to these pure-play EV manufacturers, which sell these tax credits to legacy automakers that are short of compliance targets. For Tesla especially, selling these tax credits plays a key role in its profitability. Without regulatory credits, Elon Musk’s company would have reported a pre-tax loss during the first quarter of 2025.

With the teeth behind CAFE regulations removed by the big, beautiful bill, the market for automotive regulatory credits in the U.S. is going to be severely depressed. It has the potential to expose the fact that Wall Street’s EV darling, Tesla, has been consistently generating more than half of its pre-tax income from unsustainable and/or non-innovative sources, such as selling automotive regulatory credits and earning interest income on its cash.

It’ll also minimize regulatory tax credit revenue for Rivian and Lucid. Whereas Tesla has at least been profitable on a recurring basis for five consecutive years (with the help of automotive regulatory credits), Rivian and Lucid continue to lose money hand over fist as they ramp up operations and attempt to carve out their own unique niches in the automotive marketplace. Despite substantial cash piles for both companies and brand-name financial backing, long-term success is far from a guarantee.

Though I wouldn’t go so far as to say Donald Trump drove a dagger through the heart of the EV industry, his actions are almost certain to thin the herd and make it considerably more difficult for pure-play electric-vehicle makers to compete with traditional ICE vehicles.

Is ConocoPhillips Stock an Obvious Buy Right Now?

ConocoPhillips is integrating new assets as it focuses on its best properties, setting up for stronger returns when oil prices rise again.

If there is one thing that investors need to understand about the energy sector, it is that oil and natural gas prices are inherently volatile. But there’s a somewhat counterintuitive takeaway here. Sometimes the best investment opportunities arise when business in the oil space isn’t going so well.

Which is why investors might want to buy ConocoPhillips (COP -2.80%) today. Indeed, the company’s successful business overhaul is so obvious that it is hard not to notice (at least partly because the company is so happy to point it out).

Image source: Getty Images.

Not such a great quarter for sales and earnings

ConcoPhillips’ earnings in the second quarter of 2025 weren’t great when you compare it to the same quarter in 2024, with a drop from $1.98 per share last year down to just $1.56 this year. But that doesn’t even do justice to the energy company’s earnings decline, since pulling out a one-time gain in the second quarter of 2025 drops the total down to $1.42 per share. That’s the worst quarterly earnings outcome in over a year and down sequentially from even the first quarter.

But that’s kind of how things go in the energy sector, where oil and natural gas prices drive the top and bottom lines of the income statement. In fact, it isn’t even remotely unusual for ConocoPhillips’ earnings to be volatile from quarter to quarter. That said, the energy sector is, generally, not in the best place today relative to the highs achieved in the price rebound coming out of the coronavirus pandemic.

For example, ConocoPhillips’ share price has fallen around 25% from its late 2022 highs. For comparison, Brent Crude, a key international oil benchmark, and West Texas Intermediate Crude, a key U.S. oil benchmark, have both lost about a third of their value over the same span. This could actually be a good time for more aggressive investors to consider buying ConocoPhillips.

An obvious reason to like ConocoPhillips

Assuming you can stomach the uncertainty of a commodity-based business like ConocoPhillips, there are good things happening at the company. Notably, it has been integrating the acquisition of Marathon Oil and executing above expectations. For example, it added 25% more resources than projected when the deal was inked. Despite that, it also managed to reduce the number of rigs it was operating on the added properties by 30%. All in, it was able to double the business synergies it projected, saving $1 billion in costs annually. And management managed to set up $2.5 billion in dispositions in nine months, when it had previously been looking to shed $2 billion in assets over a two-year period.

The dispositions are a special consideration. ConocoPhillips isn’t looking to get big for the sake of getting big. It is attempting to optimize its portfolio of assets so it can focus on only its best properties. That, in turn, should help to improve profitability over the long term. To be fair, even the best properties won’t change the variability in energy prices. But wider profit margins means the company will make more money when times are good and have more downside leeway when times are bad. ConocoPhillips isn’t hiding its success, it is proudly telling investors all about what it has achieved. In other words, there are obvious improvements taking shape at the business.

This is the setup for better performance in the future

To state the obvious again, as an energy company, energy prices are going to dictate ConocoPhillips’ financial results. Conservative investors looking for consistent earnings or reliable dividends (the company pays a dividend regularly, but the amount of the dividend is highly variable) probably shouldn’t buy the stock.

But if you are looking for direct exposure to energy prices, ConocoPhillips could be a solid choice given management’s efforts to overhaul the business. When commodity prices take off again, the upgrades made to the portfolio will help supercharge ConocoPhillips’ financial results. And Wall Street will almost certainly reward the stock for that.

Why Investors Were Barking for Datadog Stock Today

It was hardly a dog of an investment for the stock market that day.

Highly specialized tech stock Datadog (DDOG 4.49%) received quite a treat from stock market investors on Monday, as they collectively sent the company’s shares up by well over 4%. It was clear they took an analyst’s bullish update on the stock to heart, since that increase trounced the S&P 500 index’s 0.3% rise.

A generous price target lift

That prognosticator was BMO Capital’s Keith Bachman, who published a new take on Datadog before market open. In that note, he raised his price target on the stock to $154 per share, which was quite the boost from his previous $130 assessment. In doing so, Bachman kept his outperform (i.e., buy) recommendation on the shares intact.

Image source: Getty Images.

Bachman’s revision was based on a new calculation of his revenue estimate in the coming quarter for the company, according to reports. With that, he changed the price target to reflect what he believes is a fair multiple of 14 to 15 times Datadog’s expected fiscal 2026 top line.

Formerly, he had pegged this at 13 to 14 times the forecast revenue.

Second-quarter success

For the most part, there hasn’t been much proprietary news coming from Datadog recently. In early August, it published quite an encouraging quarterly earnings report, in which it not only scored a double beat on the consensus analyst estimates for the period, but also comfortably beat projections for the entirety of this year.

This was on the back of some rather encouraging growth numbers for the company. Revenue rose by 28% year over year to hit $827 million, while non-GAAP (adjusted) net income advanced 7% to almost $164 million.

Eric Volkman has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Datadog. The Motley Fool has a disclosure policy.

Vail Resorts MTN Q4 2025 Earnings Call Transcript

Image source: The Motley Fool.

DATE

Monday, September 29, 2025 at 5 p.m. ET

CALL PARTICIPANTS

Chief Executive Officer — Rob Katz

Chief Financial Officer — Angela Korch

Need a quote from a Motley Fool analyst? Email [email protected]

TAKEAWAYS

Resort reported EBITDA— $844 million for fiscal 2025, representing 2% growth compared to the prior year.

Fiscal 2026 net income guidance— $221 million to $276 million projected for the upcoming year.

Fiscal 2026 resort reported EBITDA guidance— $842 million to $898 million, including $14 million in one-time resource efficiency costs.

Season pass sales trend— As of September 19, 2025, season pass units decreased approximately 3%, while sales dollars increased approximately 1% compared to September 20, 2024.

Resource Efficiency Transformation Plan— Expected to deliver $38 million in incremental efficiencies for fiscal 2026, targeting over $100 million in annualized efficiencies by year-end.

Cash tax payments guidance— Anticipated at $125 million to $135 million for fiscal 2026.

Capital expenditures for calendar 2025— Planned at $198 million to $203 million in core capital, plus $46 million in growth capital for European resorts and $5 million in real estate projects.

Share repurchases— 1,290,000 shares repurchased (3% of outstanding) at an average price of $156 per share, totaling $200 million.

Quarterly dividend declaration— $2.22 per share dividend payable October 27, 2025, to holders as of October 9, 2025.

Net leverage— Net debt was 3.2x trailing twelve-month total reported EBITDA as of July 31, 2025.

Epic Friend Tickets initiative— New benefit for 2025-2026 Epic Pass holders offers lift tickets at a 50% discount to walk-up prices for the 2025-2026 season; full ticket value can be applied toward a future pass purchase.

Lift ticket revenue outlook— CFO Korch said, “still expect to be slightly positive on lift ticket revenue” despite lower pass visitation.

Liquidity position— Company reported approximately $1.4 billion in total liquidity (cash, revolver, and delayed draw term loan availability) as of July 31, 2025.

Transformative marketing focus— Management stated a shift is underway from email-based to broader digital, social, and influencer engagement aimed at brand building and guest acquisition.

Australia operations— Improved visitation and normalization of weather in Australia are expected to contribute $9 million to resort reported EBITDA growth.

SUMMARY

Vail Resorts(MTN 0.41%) management acknowledged financial underperformance versus expectations, attributing this to changing consumer behaviors and lagging adaptation in guest engagement approaches. The company expects overall skier visitation to be slightly down, driven primarily by an anticipated decline in pass sale units, with incremental lift ticket sales expected to offset only a portion of the decrease. Fiscal 2026 growth initiatives focus on targeted lift ticket strategies, enhanced digital marketing, and increased mobile conversion, with a multi-year timeline projected for material revenue acceleration. Net debt levels and liquidity are described as sufficient to sustain current capital priorities.

CEO Katz explicitly confirmed that visitation is expected “to be down slightly” due to lower pass sales, with a partial offset from new lift ticket initiatives.

Passholder renewals are up among multi-year loyal customers, while first-year and new buyer retention remains a challenge.

CFO Korch indicated that visitation is really the key on both ends when assessing the guidance range, highlighting the outsized impact of traffic on results.

Ancillary revenue capture and improved technology deployment (notably, launches for My Epic app integrations) are planned to boost per-guest monetization and operational efficiency.

Management reported no material geographic or demographic concentration in the weak pass trends, describing softness as broad-based rather than isolated to any segment.

Dividend maintenance is prioritized even at the lower end of guidance, with willingness to allow leverage to go up a little bit if necessary, per CEO Katz.

INDUSTRY GLOSSARY

Epic Friend Tickets: Discounted lift tickets made available to Epic Pass holders for their friends and family, priced at 50% off standard walk-up lift ticket rates, and applicable for future pass conversion.

Resource Efficiency Transformation Plan: Vail Resorts’ cost optimization initiative aimed at achieving over $100 million in annualized cost savings, centering on operational and marketing efficiency.

Full Conference Call Transcript

Angela Korch: Thank you, operator. Good afternoon, and welcome to our fiscal 2025 fourth quarter earnings conference call. Joining me on the call today is Rob Katz, our Chief Executive Officer. Before we begin, let me remind you that some information provided during this call includes forward-looking statements that are based on certain assumptions and are subject to a number of risks and uncertainties as described in our SEC filings. Actual future results may vary materially. Forward-looking statements in our press release issued this afternoon along with our remarks on this call, are made as of today, 09/29/2025. And we undertake no duty to update them as actual events unfold. Today’s remarks also include certain non-GAAP financial measures.

Reconciliations of these measures are provided in the tables included with our press release, which along with our annual report on Form 10-Ks, filed this afternoon with the SEC, are also available on the Investor Relations section of our website www.vailresorts.com. I would now like to turn the call over to Rob for some opening remarks.

Rob Katz: Thank you, Angela. Good afternoon, everyone. Thanks for joining us. Before we discuss our results and fiscal 2026 guidance, I want to share my perspective on where the business stands today and where I see opportunities for future growth after being back in the CEO role for the past four months. I want to start by acknowledging that results from the past season were below expectations, and our season-to-date pass sales growth has been limited. We recognize that we are not yet delivering on the full growth potential that we expect from this business, in particular on revenue growth, in both this past season and in our projected guidance for next year.

That said, I’m confident that we are well-positioned to return to higher growth in fiscal year 2027 and beyond. At the heart of our underperformance is that the way we are connecting with guests has not kept pace with the rapidly evolving consumer landscape. We have not fully capitalized on our competitive advantages nor have we adapted our execution to meet shifting dynamics. For years, email was our most effective channel for reaching and converting guests, leveraging data to deliver efficient and targeted communications. However, as consumer preferences have changed, particularly over the last few years, email effectiveness has significantly declined but we did not make enough progress in shifting to new and emerging marketing channels.

Compounding this, we historically have prioritized transactional call-to-action messaging with our guests and missed the opportunity to tap into the strong emotional connection our guests have with the Epic brand and our individual resorts. This approach was successful during a time period where we were rapidly adding resorts and innovating our pass product portfolio. But over the last few years, we have not benefited from those types of positive news events, and instead have dealt with actually some moments we did not deliver on the operational front. Our approach has not been reaching a broader array of guests in order to amplify brand awareness, attract new guests, and increase guest loyalty.

We’ve also not had enough focus on our lift ticket business. Again, this made sense as we were rapidly growing our pass business, but as we dramatically increased pass penetration, we have not pivoted to bring the same level of focus, creativity, and resources to engaging with guests who, for whatever reason, were not yet ready to purchase a pass before the season. Finally, while we have made great strides in developing and improving our My Epic app, the app does not have native commerce, and we have not been set up to accept either Google Pay or Apple Pay.

However, we are seeing guest engagement dramatically increase in the app and on mobile, yet purchase conversion within both are significantly lower than what we would see on our website and below its potential. I’m fully committed to course-correcting and executing a multiyear strategy that unlocks the full potential of our business. The strategy is rooted in leveraging our strong competitive advantages to drive sustained and profitable growth. We own and operate 42 resorts across almost all regions in North America and Australia, and we have the strongest brands and most popular resorts.

By owning and operating our resorts, we are able to collect extensive data from our guests across all our lines of business throughout the entire network, giving us tools we can leverage in every marketing channel, and use to inform mountain and technology investments in the highest return areas across all our resorts. We can also leverage our integrated model and data to optimize every aspect of our product and pricing approach across all lift access products, passes, and lift tickets, at each resort as well as ancillary revenue, which will continue to be a larger focus for the company going forward. Finally, we are well-positioned to leverage the new technologies that are defining the current market environment.

However, our immediate priority is increasing visitation to our resorts, an essential driver of revenue and ultimately free cash flow. We will continue to invest in our resorts and our employees, consistent with our long-standing focus on delivering exceptional guest experiences. At the same time, we are taking decisive steps that we believe rebuild lift ticket visitation, evolve our guest engagement approach, to better reach and convert guests, and reaccelerate growth of our pass program. All of which are critical to strengthening our long-term financial performance. On the first item, we are focused on rebuilding lift ticket visitation, an essential driver of revenue and long-term growth.

We are strategically enhancing lift ticket offerings, pricing strategies, and our marketing approach aimed at bringing in new guests to our resorts in ways that complement our pass program. In August, we introduced Epic Friend Tickets, a new benefit for the 2025-2026 Epic Pass holders giving them the ability to share discounted lift tickets with family and friends. This not only celebrates the social side of skiing and riding, but it also drives lift ticket sales for new guests that would be attracted to visiting our resorts with their friends and family. Importantly, the full value of the ticket can be applied towards a future pass purchase, making it a powerful tool for future pass conversion.

At the same time, we’re evolving our lift ticket pricing strategy with more targeted adjustments by resort and by time period. This allows us to balance guest access and value while optimizing demand, particularly in off-peak periods, without compromising the strength of our pass program. We are also increasing our media investment with a focus on top-of-funnel awareness of our resorts, to help us reach new audiences and drive incremental visitation throughout the winter. And intend to continue to innovate our lift ticket product offering as we get into the upcoming ski season.

Beyond the expected immediate impact on visitation, lift ticket guests represent a high conversion population for future pass sales, which supports our pass growth in FY ’27 and beyond. Second, we’re evolving our guest engagement strategy to better connect with skiers and riders and drive stronger performance. Our focus is on broadening our reach and modernizing how we engage across channels. We plan to increase our exposure within digital and social platforms and expand our influencer partnerships. We believe this shift will allow us to reach guests where they are, and to fully utilize our guest data to create content that resonates with our guests and drives action.

We’re also aiming to elevate the individual brands of our resorts, by tapping into the emotional connection guests have with each destination. We believe this is an important differentiator in a competitive landscape. Third, we continue to see meaningful opportunities to expand advanced commitment and grow our pass business. Pass price reset ahead of the 2021-2022 season exceeded our expectations in the initial years. And despite some modest declines recently, pass units are expected to be up over 50% fiscal 2026 compared to fiscal 2021. And the same is true for our Epic and Epic Local pass products, which despite recent modest declines, we expect to be up approximately 20% in units, since the 2021 season.

And importantly, we have delivered this strong growth in those products despite significantly expanding other pass options for guests, including our Epic Day Pass products. This growth in our pass program has significantly strengthened our financial resilience and stability. We’re focused on driving long-term guest loyalty, which means ensuring we’re optimizing the pass offering and continue to drive retention and conversion of new guests to the program. Toward that end, while driving lift ticket sales, Epic Friend Tickets is also a new benefit for unlimited pass. We’re also investing in personalized media and influencer channels better target and convert prospective pass buyers.

Because passes were already on sale during the CEO transition, our ability to influence fiscal 2026 pass results was limited. Looking ahead to fiscal 2027, we will be evaluating all aspects of our pass portfolio, including the product offering, pricing, and benefits, in conjunction with our lift ticket products and pricing, with a focus on driving conversion to our highest value highest frequency products, and optimizing our overall lift access revenue growth.

We are also actively searching for a new leader of our marketing organization, and have retitled the role as a Chief Revenue Officer reflecting the clear focus for this leader on driving all aspects of revenue for the company, and are looking for an executive with strong P&L ownership and overall leadership experience. Finally, we will continue to invest in our people and our resorts to ensure we are delivering an experience of a lifetime.

We are uniquely positioned to capitalize on investments in new technologies and processes that make it easier for our guests to engage with each aspect of the physical and digital experience we provide, driving both more value for our guests and revenue opportunities for the company. Vail Resorts, Inc. has delivered incredible stability and has an extraordinary foundation to execute on these opportunities, and generate stronger long-term sustainable growth. We have irreplaceable resorts, an owned and operated business model and robust data infrastructure that enables a sophisticated approach to product and pricing decisions across our resorts.

We continue to execute against our growth strategies of growing the subscription model, unlocking ancillary, transforming resource efficiency, differentiating the guest experience, and expanding the resort network. In addition, we have a resilient business model with demonstrated financial stability and strong free cash flow generation. And a track record of disciplined capital allocation and consistent innovation. Coupled with our passionate and talented teams, we believe we are well-positioned to succeed in the future. These actions taken together with the continued success of our Resource Efficiency Transformation Plan gives me confidence in our ability to deliver long-term sustainable growth and long-term value for our shareholders, our guests, our communities, and our employees in the years ahead.

With that, I will turn it over to Angela to further discuss our financial results and fiscal 2026 outlook.

Angela Korch: Thank you. As Rob mentioned, while our financial results in fiscal 2025 do not reflect the full potential of the company, the results do highlight the stability of the business model and early success of the resource efficiency transformation plan. The company generated $844 million of resort reported EBITDA in fiscal 2025, which represents 2% growth compared to the prior year, despite total 3% across our North American resorts. The results were within the original guidance range for fiscal 2025 per resort reported EBITDA, provided in September 2024, and excluding the CEO transition costs and changes in foreign exchange rates, the result was within 1% of the midpoint of the original resort reported EBITDA guidance range.

Results for our fourth quarter fiscal quarter 2025 were slightly ahead of our expectations with strong cost management, solid demand for our North American summer operations, and improved visitation in Australia relative to the prior year. Now turning to our outlook for fiscal 2026. In fiscal year 2026, we expect net income attributable to Vail Resorts, Inc. to be between $221 million and $276 million and resort reported EBITDA to be between $842 million and $898 million. The guidance includes an estimated $14 million in one-time costs related to the Resource Efficiency Transformation Plan.

We anticipate growth in fiscal 2026 to be driven by price increases, ancillary capture, incremental efficiencies related to the resource efficiency transformation plan, and normalized weather conditions in Australia in 2026, partially offset by lower pass unit sales which are expected to have a negative impact on skier visits relative to the prior year, and cost inflation. Season pass sales through 09/19/2025 for the upcoming North American ski season decreased approximately 3% in units, and increased approximately 1% in sales dollars, as compared to the prior year period 09/20/2024.

The season-to-date trends through 09/19/2025 were generally consistent with the spring selling period, a decline in units driven by less tenured renewing guests, those that had a pass for just one year, and fewer new pass holders. Renewals are up for our more loyal pass holders, those that have had a pass for more than one year. As we enter the final period for season pass sales, we expect our December 2025 season-to-date growth rates to be relatively consistent with our September 2025 season-to-date growth rates. The Resource Efficiency Transformation Plan continues to generate strong results for the company, and we expect to exceed the $100 million in annualized cost efficiencies by the end of fiscal year 2026.

Our fiscal 2026 guidance assumes we will deliver $38 million incremental efficiencies before one-time costs, contributing to the achievement of an expected $75 million of cumulative efficiencies since we announced the plan in September 2024. Finally, in fiscal 2026, we anticipate cash tax payments to be between $125 million to $135 million. As Rob noted, while our guidance for fiscal 2026 reflects growth over the prior year, it does not reflect the full potential of the company. We are committed to positioning the company to unlock stronger and sustainable long-term growth moving forward. Turning to our capital allocation priorities.

Operator: We remain committed to a disciplined and balanced approach

Angela Korch: as stewards of our shareholders’ capital. Our capital allocation priorities remain consistent. First, prioritize investments and enhance our guest and employee experience. Generate strong returns. And second, maintain flexibility to pursue strategic acquisition opportunities. After those top priorities, we return excess capital to shareholders. In support of reinvestment in our resorts, in calendar year 2025, we expect to spend approximately $198 million to $203 million in core capital, before $46 million of growth capital investments at our European resorts, and $5 million of real estate-related capital projects. In addition to this year’s significant investments, we are pleased to announce some select projects from our calendar year 2026 capital plan.

A full capital investment announced planned for December 2025, including a core capital plan consistent with the company’s long-term capital guidance. At Park City, we are continuing the multiyear transformation of the Canyon Village to support a world-class luxury-based village experience. Vail Resorts, Inc. in partnership with the Canyons Village Management Association is replacing the open-air cabriolet transport lift with a modern 10-passenger gondola which will improve the guest experience, reduce weather-related disruptions, and complement the Canyons Village parking garage, a new covered parking structure with over 1,800 spaces being developed by the developer of the Canyons Village. In addition, we plan to resubmit for permits to replace the Eagle and Silverload lifts at Park City Mountain.

To continue our investment in the on-mountain experience, which if approved, would be upgraded for the 2027-2028 North ski season. Planning of additional investments at Park City Mountain across the mountain is underway and additional projects will be announced in the future. The company also remains committed to the multiyear transformation of Vail Mountain. And in calendar year 2026, we will continue to invest in real estate planning to develop the West Lions Head area into the fourth base village in partnership with the town of Vail and developer, East West Partners.

In addition, the company plans to build on the success of its calendar year 2025 lodging investment at the Arabelle at Vail Square with plans to renovate guest rooms at the Lodge at Vail in calendar year 2026. In addition, to further enhance the guest experience across our resorts, the company will be investing in technology enhancements and new functionality for the My Epic app including new in-app commerce functionality, payment platform integrations, to improve mobile conversion, enhanced My Epic assistant functionality, and expansion of the new ski and ride school technology experience. In addition, the company will make technology investments to enhance the integration of My Epic Gear guest experience. Turning to the second priority.

Our balance sheet remains strong and is positioned to enable future strategic acquisition opportunities. As of 07/31/2025, the company’s total liquidity, as measured by total cash plus revolver availability and delayed draw term loan availability was approximately $1.4 billion. The company’s net debt was 3.2 times its trailing twelve-month total reported EBITDA. On 07/02/2025, the company completed its offering of $500 million aggregate principal amount of five and five-eighths percent notes, due in 2030. We used a portion of the proceeds from the offering to repay seasonal borrowings under our revolving credit facility, in addition to the $200 million of share repurchases completed during the quarter.

We intend to use the excess proceeds from the bond issuance together with the $275 million delayed draw term loan for the repurchase or repayment of our outstanding 0% convertible senior notes due 2026 at or prior to their maturity on 01/01/2026. After these priorities, we focus on returning excess capital to shareholders. In the current environment, we look to balance our approach between share repurchases and dividends. The company declared a quarterly cash dividend on Vail Resorts, Inc. common stock, a $2.22 per share dividend will be payable on 10/27/2025 to shareholders of record as of 10/09/2025.

The current dividend level reflects the strong cash flow generation of the business, with any future growth in the dividend dependent on material increases in future cash flow. We also maintain an opportunistic approach to share repurchases based on the value of the shares. As mentioned in the quarter, we repurchased approximately 1,290,000 shares or 3% of outstanding shares at an average price of approximately $156 per share for a total of $200 million. We continue to evaluate the highest return opportunities for capital allocation. Now I’d like to turn the call over to Rob.

Rob Katz: Thanks, Angela. In closing, we greatly appreciate the loyalty of our guests this past season and the continued loyalty of our pass holders who have already committed to next season. With our Australia winter season coming to a close, I would like to thank our frontline team members for their passion and dedication to delivering an incredible experience to our guests. I would also like to thank all of our team members who are working to welcome skiers and riders back to the mountain this coming winter season. We are looking forward to a great upcoming winter season in the US, Canada, and Switzerland. At this time, Angela and I would be happy to answer your questions.

Operator, we are now ready for questions.

Operator: At this time, if you wish to ask a question, please press 1 on your telephone keypad. You may remove yourself from the queue by pressing 2. Again, please limit yourself to one question and one follow-up. We’ll take our first question from Shaun Kelley with Bank of America. Your line is open.

Shaun Kelley: Good afternoon, everyone. Thanks for taking my questions. Rob or Angela, maybe I just wanted to start with kind of the broad backdrop for visitation for this upcoming season. So Rob, in the prepared remarks, you talked a lot about some very, I think, interesting initiatives to start to address the visitation challenges and some you see there. Obviously, the Epic Friend Tickets being a piece there, and I imagine you expect utilization on those to be pretty good.

So can you help us just kind of think about that underlying backdrop and what you’re doing on marketing and, you know, with Epic Friends and contrast that with kind of in the, you know, in the bridge for the year on the financial side, it seemed like the implication was that the expectation given the pass units are down a little bit was that maybe visits are down, but I might be misreading that. So just wondering kind of how you expect really this season to play out from a visitation standpoint given some of the initiatives in play? Thanks.

Rob Katz: Yeah. Thanks, Shaun. Yes. That’s true. We do expect visitation in total for this year to be down slightly. I think that is primarily driven by the decline in pass sales to this point. And while we do think that we’re gonna make a portion of that up with lift ticket sales, you know, it’s not gonna be enough to overcome, in our view, the decline in pass sales to this point. What I would say is that a lot of the things that I mentioned about what we need to do to correct how we engage with guests are things that are multiyear efforts. None of those things are things that happen right away.

Even the Epic Friend piece will take time for our guests to understand what they have for us to communicate with our guests, for them to then increase their utilization to understand the change in terms for that and how they can use it and how they could turn it into a ticket the following year. So we expect to see some benefit from it this year, but, obviously, additional benefit from it in future years. The same is true with our paid media investments. Again, I think, you know, if you’re looking for top-of-funnel brand building efforts, that’s not something that’s gonna happen in a month or two. That’s something that takes more time.

The same is true for getting deeper and more skilled and more sophisticated in all the other marketing channels that we have. So what I would say is I think, you know, in the end of the day, we are starting to prepare for the fiscal 2027 season now. So we have work going on. We’re obviously working on pass sales, but also working on other initiatives. If you kind of back that up, you realize, like, yeah, from the time that some of this started, right, not possible to have a full impact on fiscal 2026.

Shaun Kelley: Got it. Makes complete sense. And then just as my follow-up, and you kind of already touched on a little bit of it. Just for the 2027 and beyond plan, some of the outline for maybe the Chief Revenue Officer and some of the opportunity. But just how big of a change is on the table here, Rob, just in terms of like look, the big initiative done was, you know, to push for volume, to push pass utilization up at the expense a little bit of price. Right? That was sort of the compromise made back during the pandemic.

Is something as fundamental as that shift on the table here as we think about moving forward, whether it be raising the pass price in its entirety to balance out that ecosystem differently or maybe thinking about it differently, just the, you know, possibly charging an add-on, which has been proposed at, you know, a major, you know, kind of high-value resort like, like, Vail, like, just to change the composition of, you know, price versus volume. Just how are you thinking about sort of that very fundamental idea as we turn the page to next year?

Rob Katz: Yeah. I think the way to think about it is I think what we did with the price reset was really kind of a right across the board approach because what we saw was that we felt like all of our pricing was too high in terms of getting the penetration that we wanted in pass. And I think that was the right move at the time, and I think it’s driven actually good success. And, obviously, as we highlighted, you know, we’re still well above where we were before then. But what I would say though is I think what we have not done is we have a lot of different pass products. Right?

So it’s not just the Epic and Epic Local. Right? We have a lot of different pass products for that. We then have child pricing and college pricing and team pricing and regional passes. And then all of those products really sit on top of all of our lift ticket products. And I think what you’re hearing from us is I think what we can do is now, right? Not take a kind of across the board approach to any of this, but actually, resort by resort or pass product by pass product approach.

And there’s technology now that’s available that given our data and what we can put into it, right, where all of a sudden we have a much higher level of confidence in terms of what we can drive with some of these individual moves. It’s, you know, I we have, I don’t know, 200 plus pass products or something like that. We have thousands of lift ticket products. And those have largely been marching in lockstep. We think, actually, there’s an opportunity for us to think much more strategically about it. Again, using, you know, some of the tools that are out there that we all know about.

And so what I’d say is, you know, in a way, the big if we’re cracking something open, it’s not necessarily that we’re looking to take price up or price down per se. It’s that we’re actually cracking this kind of connection that every single product has had to each other over the last fifteen years.

Shaun Kelley: Perfect. Thank you very much.

Operator: We’ll move next to David Katz with Jefferies. Your line is open.

David Katz: With respect to the sort of single-day visitation or the walk-up,

Rob Katz: know, window, one of the debates you know, I’m I’m guess you’re you’re having is on sort of that price. Right? And know, whether any of the strategies around improving walk-up visitation you know, includes adjusting some of the price schedules that are out there or some of the pricing strategies.

Rob Katz: Yeah. What I would say is that I think we look at it, I mean, maybe a little bit more broadly. So right at a at a top-line level, we’re looking at pass. Right? So that’s all the products that are sold before the season begins that are nonrefundable. And then there’s lift tickets, and within lift tickets, we have a lot of different lift tickets, some of which most of which, candidly, are advanced lift tickets. So there’s something that you buy three days in advance, seven days in advance. And so we do put a lot of business through that. And then, yes, we do have people who walk up to buy tickets just that day.

And so we are looking at all of those prices. But, of course, I would say, yeah, we’re we’re still gonna be putting, you know, the Epic Friend Ticket is a 50% discount on the walk-up price. That would, you know, perfectly fit for somebody who wants to make a decision that day. But we think there could be opportunities for us to be more creative about some of the other prices that we have and the kind of advanced windows that we have for them because of when people if you haven’t made your decision by the pass deadline, then it’s a question of when do people start making decisions, you know, for their future trips.

So in the end, some of this is like, we’re trying to kind of tailor this to how people make a decision. You know, it’s not that many people are deciding to go to Vail that day and then, you know, come flying out. So the question is, like, when can we shift price that makes the biggest impact on driving more visitation? I understood. And, you know, interesting about

David Katz: the discussion around you know, media channels, And Yep. Historically, the company has always been particularly advanced at you know, data gathering. How much of this strategy about sort of reaching customers through the right channels

Rob Katz: is also about data gathering that builds intelligence know, for the future? Or is it just the right connection channel?