In this video, Motley Fool contributors Jason Hall and Jeff Santoro discuss what Berkshire Hathaway (NYSE: BRK.A)(NYSE: BRK.B) could look like once Warren Buffett is no longer CEO, and potentially once he’s no longer the chairman.

*Stock prices used were from the afternoon of Oct. 2, 2025. The video was published on Oct. 6, 2025.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Should you invest $1,000 in Berkshire Hathaway right now?

Before you buy stock in Berkshire Hathaway, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Berkshire Hathaway wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004… if you invested $1,000 at the time of our recommendation, you’d have $621,976!* Or when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $1,150,085!*

Now, it’s worth noting Stock Advisor’s total average return is 1,058% — a market-crushing outperformance compared to 191% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

Jason Hall has positions in Berkshire Hathaway. Jeff Santoro has positions in Berkshire Hathaway. The Motley Fool has positions in and recommends Berkshire Hathaway. The Motley Fool has a disclosure policy. Jason Hall is an affiliate of The Motley Fool and may be compensated for promoting its services. If you choose to subscribe through their link they will earn some extra money that supports their channel. Their opinions remain their own and are unaffected by The Motley Fool.

This niche chipmaker just emerged from bankruptcy protection — but can it grow again?

Wolfspeed(WOLF -1.30%), a leading maker of silicon carbide (SiC) and gallium nitride (GaN) chips, filed for bankruptcy protection on June 30 as its sales stalled out, its losses widened, and its debt levels spiraled. On that dark day, its stock closed at a record low of $0.39.

But on Sept. 29, Wolfspeed emerged from Chapter 11 bankruptcy after reducing its total debt by approximately 70%, extending its maturities to 2030, and reducing its annual cash interest expenses by roughly 60%. Today, it trades at about $23 — so a $1,000 investment at its all-time low would have grown to nearly $59,000 in just three months.

Image source: Getty Images.

Wolfspeed pulled itself back from the brink, but will it stabilize its business and generate even bigger gains for its investors over the next 12 months? Let’s review this niche chipmaker’s business model, growth rates, and valuations to decide.

What does Wolfspeed do?

Wolfspeed’s SiC and GaN chips can operate at higher voltages, temperatures, and frequencies than traditional silicon chips. That resilience makes them well-suited for short-length LEDs, lasers, 5G base stations, military radars, solar panels, wind turbine systems, and electric vehicles (EVs).

Unlike other “fabless” SiC and GaN chipmakers which outsource their production to third-party foundries, Wolfspeed is an integrated device manufacturer (IDM) which manufactures its chips and power devices at its own foundries. It mainly produces SiC wafers, SiC power devices, and GaN radio frequency (RF) and power devices.

To ramp up the production of its newest SiC and GaN chips, Wolfspeed opened a new 200mm plant at Mohawk Valley, New York in 2022. It also started building an even larger 200mm plant in Siler City, North Carolina in 2023, and it’s gradually winding down the production of its older 150mm chips at its older plants in Texas and North Carolina.

How fast is Wolfspeed growing?

Wolfspeed was known as Cree until late 2021, when it spun off its LED and lighting segments to focus on selling its Wolfspeed-branded SiC and GaN products. From fiscal 2021 to 2025 (which ended in June), its revenue expanded at a compound annual growth rate (CAGR) of 9.6%, from $526 million to $758 million.

However, most of that growth occurred immediately after its restructuring and rebranding, and it initially benefited from a shift toward wide-bandgap (WBG) SiC and GaN chips across the EV, industrial, and renewable energy markets. But over the following three years, its revenue growth decelerated and its adjusted gross margins crumbled.

Period

FY 2022

FY 2023

FY 2024

FY 2025

Revenue Growth

42%

24%

(12%)

(6%)

Adjusted Gross Margin

36%

33%

13%

2%

Data source: Wolfspeed.

Inflation, rising interest rates, supply chain disruptions, and other macro headwinds all reduced its shipments to its EV and industrial customers. It also faced fresh competition from Chinese SiC and GaN chipmakers, which flooded the market with an excess inventory of cheaper chips.

Instead of cutting costs to cope with that slowdown, Wolfspeed continued to ramp up the production of its 200mm chips at its Mohawk Valley plant, while pouring more cash (and securing more CHIPS Act funds) for the construction of its Siler City plant. That’s why its total year-end liabilities rose nearly fivefold from $1.5 billion in fiscal 2022 to $7.3 billion in fiscal 2025.

That mix of slowing growth, declining margins, and soaring debt spooked Wolfspeed’s investors, and its board ousted its CEO, Gregg Lowe, in late 2024.

Where will Wolfspeed be in a year?

Prior to filing for bankruptcy protection, Wolfspeed appointed Robert Feurle — an industry veteran who previously worked at Micron Technology and ams-OSRAM AG — as its new CEO. In a recent press release, Feurle said Wolfspeed was still “well positioned to capture rising demand” for SiC chips and devices across the “AI, EVs, industrial, and energy” markets. He noted its “improved financial stability” and “vertically integrated 200mm facility footprint” would put it in a better position to profit from the nascent market’s expansion.

From fiscal 2025 to 2027, analysts expect Wolfspeed’s revenue to grow at a CAGR of 15% from $758 million to $998 million as the macro environment stabilizes. But it will remain unprofitable for the foreseeable future as it continues to expand its first-party foundries.

Yet with a market cap of about $640 million (which was reduced by the cancellation of its old shares in exchange for new common shares), its stock looks dirt cheap at less than 1 times this year’s sales. Assuming Wolfspeed gets its act together, matches analysts’ estimates, and trades at a more reasonable 1 times its forward sales, its stock could rise 55% over the next 12 months.

I wouldn’t go all-in on Wolfspeed’s stock right now, since fabless SiC and GaN chipmakers like Navitas(NVTS -4.76%) are safer and less capital-intensive plays on the same trend. But it might be worth nibbling on if you expect its new CEO to successfully stabilize its business.

Welcome back to the Times of Troy newsletter, where we’re back from the bye, recharged and ready for the gauntlet ahead on USC’s schedule. Here’s hoping you had a nice relaxing weekend away that didn’t involve yelling at the television about your team’s struggling secondary.

Following that lead, we’re going to step away from the football field for this week to talk about something that every college football program could use more of these days, but never seems to get enough of:

Money.

Fight on! Are you a true Trojans fan?

First, let me take you back four years before the Pac-12 imploded, to when then-Pac-12 commissioner Larry Scott had a big idea to save his flailing conference.

His plan? Sell off a 15% stake of the Pac-12 to a private equity firm for a reported infusion of $1 billion, which Scott hoped would be enough to help stabilize the conference. At the time, the Pac-12’s media rights deal was only providing about $30 million per school annually. A private equity investment, Scott figured, would add tens of millions to that total, helping to hopefully keep the Pac-12 afloat until the conference’s next media rights negotiation.

But the plan never came to fruition, and the Pac-12 unraveled. The reason it didn’t work then was the presidents and chancellors of the Pac-12’s member schools had no stomach for selling off a stake in their conference to a private equity firm, no matter how desperate the conference was. USC, in particular, was one of the most vocal detractors. Viewing itself as the crown jewel of the conference, it already wasn’t happy with the equal distribution of media revenue. It saw no reason, at the time, to give away more valuable equity in its brand while locking into that arrangement for a longer period.

Had Scott managed to make that deal, who knows what might have happened with the Pac-12.

But almost seven years later, private equity firms are once again swirling like vultures overhead. As first reported last week by ESPN, USC’s new conference, the Big Ten, is now seriously considering a $2-billion private equity infusion. That deal would also reportedly lock in the conference’s members through 2046, injecting at least a little stability into an especially unstable landscape.

A decision is expected in the coming weeks, and the conference is looking for consensus among schools to move forward. But USC had no interest in such a deal before. Why would that be different now?

Well, for one, college sports have gotten a lot more expensive in the wake of the House settlement. Even before adding a $20.5 million line item to its budget, USC’s athletic expenses were among the highest in the nation at $242 million, according to the most recent Department of Education data. And that figure doesn’t consider the $200-million football facility currently being built or the millions of scholarship money that needs to be raised or the $200-million budget deficit the larger university finds itself in.

A nine-figure private equity check would go a long way in soothing those financial concerns. Especially at the Big Ten’s smaller schools. But it wouldn’t solve every revenue problem in USC’s future. And it would be foolish to think that money doesn’t come with strings attached, even if the discussed deal does at least attempt to mitigate that influence.

The deal would create a separate corporate structure that would handle all things related to revenue generation within the Big Ten. That revenue would then be distributed between 20 equity stakeholders — the 18 conference schools, the league office and this private equity firm.

So the private equity firm wouldn’t own a piece of USC athletics, so much as it would own a share of the Big Ten’s business interests. That setup would then theoretically limit the investor’s control and keep private equity out of other decisions pertaining to Big Ten athletics, which had been the fear of Pac-12 presidents when the conference previously turned up its nose to such an investment.

There are still many unknowns here, most notably how the revenue would be distributed. But there’s no reason to think the conference’s biggest brands, such as USC or Michigan or Ohio State, would sign on to any deal that didn’t include distribution of that revenue that significantly favored those schools.

That appears to be the plan. But as of now, neither Michigan nor Ohio State is on board yet.

“I believe selling off Michigan’s precious public university assets would betray our responsibility to students and taxpayers,” Jordan Acker, a member of Michigan’s Board of Regents, wrote on social media.

And in this case, the buyer has an entirely different mission than the other stakeholders involved. Private equity firms exist solely to provide up-front capital in order to eliminate risk, turn a profit and then exit the marketplace. There’s no reason to think it would be different in this case. Which doesn’t exactly jibe in the marketplace that is college athletics.

So is a $100-million check worth giving away that control? For Purdue or Rutgers, probably. For USC? I’m not so sure.

USC, like Michigan and Ohio State, has yet to sign off on plans for conference-wide private equity investment and still has questions about the potential deal, a person familiar with the decision not authorized to discuss it publicly told The Times. But the school wants to be good partners in the conference, and of course, it could always use an infusion of cash.

But does USC really need money that badly? The athletic department has already taken significant steps to raise revenue in light of the House settlement, including striking a massive, new 15-year multimedia rights deal with Learfield. USC doesn’t necessarily need the Big Ten or its new private equity partner to create conference-wide revenue streams where it could just strike deals on its own. Nor does it need assurances of the Big Ten’s long-term stability enough to sacrifice equity.

USC once made a mistake by accepting an equal share as its peers in the Pac-12. But it can’t make that mistake again. By virtue of its brand, USC is always going to have a seat at the table.

And if the Big Ten is getting into bed with private equity, it should be using every bit of that leverage to get the best possible deal. There’s no world in which USC should accept a smaller slice of that pie than Michigan or Ohio State, no matter the history of the other two.

Calling all questions!

Have any questions, comments or concerns about USC coming out of the bye week?

Send them along to [email protected] or shoot me a DM @RyanKartje on X or @rkartje on Instagram by Monday night, and I’ll include the best ones in a video mailbag I’m planning to put out early next week.

—Kilian O’Connor is out for at least two games with a knee injury, and maybe more. J’Onre Reed will start at center in his place. Most assumed that Reed would be the starter when he joined USC in the offseason. But O’Connor, a former walk-on, won the job in camp. Which, depending on your perspective, is either troubling for Reed or encouraging for O’Connor. Nonetheless, this is a guy who started 25 games at Syracuse. I’d hope, if USC made a point to pursue him in the portal, that Reed should be at least a passable replacement for a former walk-on. That said, the next two games — against Michigan and Notre Dame — wouldn’t have been a cake walk for USC’s offensive front even at full strength.

—Freshman All-American Caden Chittenden is getting healthier, but don’t expect him to be handed kicking duties when he returns. USC brought in Chittenden after a tremendous freshman season at Nevada Las Vegas to solve its field goal woes. But he’s been dealing with a hamstring injury since the preseason, and in his place, Ryon Sayeri has been as good as anyone could have hoped. Sayeri has hit eight of nine field goals, third-best in the Big Ten, and all 28 extra point attempts. On kickoffs, he’s been “a machine.” “If a guy is playing at a high level, no matter who it is, we wouldn’t make a change just because of that,” Riley said last week. Don’t be surprised if he keeps the job the rest of the way, regardless of Chittenden’s status.

—USC’s top guard, Rodney Rice, will miss the next few weeks with a shoulder injury. Not ideal, obviously. But Rice should be ready to go for the basketball season opener on Nov. 3, when the Trojans take on Cal Poly. Assuming he returns to full health, he’s primed for a big season as the engine of USC’s offense.

—Former Trojan quarterback Mark Sanchez was stabbed and later arrested after allegedly drunkenly assaulting a 69-year old man in Indianapolis on Friday night. When the story was first reported, it seemed like Sanchez was the victim of a violent attack. Turns out, the police believe it was the other way around. The other man involved, a 69-year-old grease disposal truck driver, told police that Sanchez tried to break into his truck and assaulted him when he refused to move his truck from an alleyway, according to police records. The man first pepper sprayed Sanchez, then, allegedly fearing for his life, stabbed Sanchez multiple times in the chest. Sanchez was eventually taken to the hospital in critical condition, and he later told police that he didn’t know who stabbed him. He’s now in stable condition.

—The NCAA tournament is “inching closer” to expanding to 76 teams. That’s according to Yahoo’s Ross Dellenger, who reported that the expansion would likely feature a 12-game opening round in multiple cities, as opposed to the four-team “First Four” matchups which traditionally took place in Dayton, Ohio. I suppose this was inevitable, with so much TV money to be made with the tournament. But I’m not sure if anyone outside of TV execs are really clamoring for this expansion.

Olympic sports spotlight

Many of you have asked and I have heard your pleas for more Olympics sports coverage in the newsletter! So from here on out, most Mondays, we’re going to zoom in on a standout team or athlete from one of USC’s non-revenue programs.

Maribel Flores was named Pac-12 freshman of the year two years ago, but she missed part of the next women’s soccer season to play for Mexico at the U20 World Cup and tallied just a single point as a sophomore.

Now, as a junior, Flores is back in peak form. She has 15 points across 11 games for USC, which ranks third in the Big Ten.

USC struggled without a win through the first three weeks of September, but has since gotten back on track with a three-game win streak. After a road swing through Minnesota and Iowa next week, the Trojans won’t have to leave L.A. for the rest of the regular season. For now, they’re just one game behind UCLA, in second place in the Big Ten.

Phil Parma (Philip Seymour Hoffman), in ‘Magnolia.’

(Peter Sorel/New Line Cinema)

Inspired by last week’s pick in this space, “One Battle After Another,” which exceeded my sky-high expectations, I’ve decided to dive back into the Paul Thomas Anderson filmography and check off the boxes I’ve missed.

First up in that quest was “Magnolia,” a sprawling, three-hour epic that I’ve been meaning to watch for many years. Set in the San Fernando Valley, where many of Anderson’s films take place, it follows an ensemble of interconnected narratives that Anderson somehow manages to weave into one story. Incredible writing. Amazing acting. As if I needed any more evidence of Anderson’s genius, “Magnolia” only solidified my adoration of his work.

Until next time …

That concludes today’s newsletter. If you have any feedback, ideas for improvement or things you’d like to see, email me at [email protected], and follow me on X at @Ryan_Kartje. To get this newsletter in your inbox, click here.

You’re reading a free article with opinions that may differ

from The Motley Fool’s Premium Investing Services. Become a Motley Fool member today to get instant access to our top analyst recommendations, in-depth research, investing resources,

and more. Learn More

The federal $7,500 EV tax credit expired on Sept. 30.

For years, federal subsidies have played a critical role in accelerating the adoption of electric vehicles (EV). Most notably, President Joe Biden’s Inflation Reduction Act included a $7,500 tax credit designed to make EV purchases more affordable and spur demand. Under President Donald Trump, however, policy priorities have shifted. As part of the newly enacted “big, beautiful bill,” the EV tax credit was eliminated as of Sept. 30.

Let’s examine how this policy change could affect Tesla(TSLA -1.41%) and what it could mean for the company’s trajectory going forward.

Image source: Tesla.

Spoiler alert: Tesla crushed Q3 deliveries

Shortly after the legislation was signed into law, I predicted that eliminating the EV tax credit would actually provide Tesla with a short-term boost. The logic was straightforward: Consumers who had been undecided about purchasing an EV would likely accelerate their decisions in order to take advantage of the $7,500 credit before it expired.

According to consensus estimates from FactSet and Bloomberg, Wall Street expected Tesla’s third quarter vehicle deliveries to fall in the range of 439,800 to 447,600 units. In reality, Tesla delivered 497,099 cars during the quarter — absolutely shattering analyst expectations.

In short, the removal of the EV tax credit was far from a death knell for Tesla. Relying solely on subsidies to determine the health of Tesla’s business and its future roadmap is a narrow view of the company’s potential. As the discussion below will show, Tesla’s long-term investment case extends well beyond government incentives.

Tesla’s expanding vision: More than just cars

Investing in Tesla requires shareholders to be fully aligned with Elon Musk’s broader technological ambitions. At its core, Musk’s vision for Tesla is centered on artificial intelligence (AI), robotics, and autonomous systems.

Consider Optimus, Tesla’s humanoid robot project. While still in early development, Optimus is designed as a scalable, general-purpose robot with the potential to augment human labor within factories — boosting productivity and delivering exponential cost savings over time. In fact, Musk himself has touted that Optimus could represent 80% of Tesla’s future value once scaled.

Equally transformative is Tesla’s vision to create a robotaxi network. The company aims to deploy a fleet of fully autonomous vehicles capable of generating recurring revenue streams that far exceed the economics of one-time vehicle sales. If successful, robotaxi could not only disrupt incumbents in the mobility market — such as Lyft, Uber Technologies, DoorDash, or Hertz — but it could also unlock a new business model for Tesla: A software-driven, high-margin service powered by its Full Self-Driving (FSD) platform.

On a deeper level, Tesla’s potential extends beyond physical products and into the intangible realm of machine intelligence. Musk has repeatedly hinted at closer integration between Tesla and his separate venture, xAI — which is developing a large language model (LLM) known as Grok to compete with OpenAI. Such a partnership could meaningfully enhance Tesla’s software stack, enabling a more intelligent and connected ecosystem that spans vehicles, robots, and AI-powered services.

Is Tesla stock a buy now?

The loss of the $7,500 EV subsidy may affect short-term affordability for certain buyer segments, but ultimately it does not fundamentally change Tesla’s long-term investment thesis.

That said, valuation deserves careful attention. As of Oct. 2, Tesla shares were trading near all-time highs. Recent momentum has been fueled in part by Musk’s $1 billion open-market purchase of Tesla stock, as well as traders positioning ahead of the Q3 delivery beat — which indeed materialized.

For these reasons, I would be cautious about chasing Tesla at current levels. While projects like Optimus, the robotaxi network, and potential xAI synergies are exciting, none have yet generated material revenue or profit. Each remains highly speculative at this stage.

For now, investors may be better served monitoring Tesla’s execution on the AI front and considering entry points on pullbacks rather than buying into the stock at peak optimism.

Adam Spatacco has positions in Tesla. The Motley Fool has positions in and recommends DoorDash, FactSet Research Systems, Tesla, and Uber Technologies. The Motley Fool recommends Lyft. The Motley Fool has a disclosure policy.

The first half of 2025 marked a decisive shift from balance-sheet defence to strategic deployment, with issuance patterns reflecting not just a recovery in confidence but a deliberate repositioning of funding models.

European investment-grade corporate bond issuance exceeded €100 billion in May 2025, up 22% year on year and the highest first-half total since 2021 and a new monthly record12. Even more striking is the nature of the deals: larger ticket sizes, cross-border placements, and a clear shift toward capital market funding as an alternative to traditional bank lending.

As monetary conditions stabilise and macroeconomic risks recede, this resurgence is less about cyclical rebound and more about long-term recalibration of how corporates source, structure, and signal their capital raising.

From pause to strategic re-entry

Throughout 2023 and early 2024, corporate treasurers largely adopted a defensive stance. Uncertainty over the European Central Bank’s rate trajectory, persistent inflation, and geopolitical instability curbed euro-denominated issuance. Spreads widened, investor appetite cooled, and expansion plans were deferred.

By 2025, however, the backdrop had shifted. The ECB’s decision to hold rates steady for a third consecutive quarter gave markets breathing room. Inflation in the euro area fell to 2.3% in June, close to the central bank’s target. And corporate balance sheets have remained robust, having built up liquidity during the period of uncertainty.

With the macro picture stabilising, corporate issuers are seizing the opportunity. CaixaBank’s corporate and investment banking division has seen pent-up demand converting into deal flow. This does not just apply to the domestic market in Spain – corporates around the world with near-term refinancing needs as well as longer-term strategic investments are springing back into action. One example: almost half of all the financing mobilised by the bank’s CIB division in 2024 originated in international branches.

A Convergence of catalysts

This rebound is the product of multiple reinforcing factors. This is not a flood of opportunistic refinancing – it is a more selective, higher-quality wave of issuance, tailored to a new set of investor demands.

In Q2 2025, there was a noticeable uptick in multi-tranche and hybrid structures, as corporates leveraged strong investor appetite for yield with longer-dated or subordinated instruments. ESG-linked issuance has also begun to recover, albeit with more rigorous scrutiny. Investors are asking harder questions—and issuers are responding with better transparency and clearer KPIs.

For example, CaixaBank recently acted as joint bookrunner, heading the syndicated financing for Scottish Power, for a total amount of more than €1.6 billion (a €900 million tranche and a £600 million tranche granted by the National Wealth Fund). The green financing for the development and construction of smart electricity grids owned or managed by Scottish Power in the UK had to comply with the taxonomy criteria set out in the UK’s Green Financing Framework.

Globalisation of European corporate funding

While euro-denominated issuance remains dominant, there has also been a rebound in non-euro placements by European corporates, particularly in USD. US non-financial corporates borrowed €40 billion as of 9 May, according to Bank of America data3. This trend is driven by favourable currency hedging conditions, as well as broad global investor interest in high-quality European names.

This global diversification signals a deliberate strategy: corporates are building resilience by broadening their investor base and optimising access across currencies.

Time for banks to re-calibrate?

What differentiates the 2025 rebound from previous waves of issuance is its quality. Companies are not flooding the market with opportunistic refinancing. Instead, they are tailoring structures to align with evolving investor demands. This creates a moment of recalibration for corporate and investment banks. Clients now expect more than just distribution – they want advice on everything from interest rate overlays to ESG structuring to regulatory disclosures. The ability to help clients re-enter the market smoothly, credibly, and strategically is where banks must differentiate.

The new issuance landscape is not about volume alone, it is about value. The days of commoditised bond issuance are gone. In their place is a smarter, more intentional market, where capital is raised not just to refinance but to reposition.

Banks are evolving to meet this need. So CaixaBank’s CIB business has grown from 760 employees at the end of 2024 to 850, with plans to expand to 920 by 2027. The division will explore opportunities across multiple geographies, especially in sectors with a global footprint, particularly renewable energy, civil and digital infrastructure, technology, and financial services.

The next phase of market leadership

This is not a return to business as usual. It is the opening phase of a smarter cycle where the measure of success is value created, not just volume raised. Those corporates and banks that can combine strategic foresight with disciplined market execution will define the next chapter of European capital markets leadership.

It’s hard to narrow down the best of any category to only one favorite. That’s true whether we’re talking about the greatest football player of all time, the best actor, or the top musical artist.

Choosing the most outstanding artificial intelligence (AI) stock is difficult, too. What is the single best stock to buy for the AI revolution?

Image source: Getty Images.

Multiple worthy contenders

Answering that question isn’t easy because there are multiple worthy contenders. Nvidia(NVDA -0.77%) absolutely makes the list. It’s the largest company in the world based on market cap. Nvidia’s GPUs remain the gold standard for training and deploying AI systems. The company’s technology is also used in AI-powered robots and self-driving vehicles.

I like Microsoft(MSFT 0.26%), too. Its Azure is the second-largest cloud platform. The company has embedded generative AI into its software products that are used by millions of people across the world. Microsoft also arguably represents the best way to invest in ChatGPT developer and AI pioneer OpenAI, which doesn’t trade publicly at this point. The two companies are close partners, and Microsoft has invested in OpenAI.

If you’re thinking about the next frontiers for AI, Meta Platforms(META -2.29%) especially stands out. The Facebook and Instagram parent is going all-in on developing artificial superintelligence (ASI). Meta also leads the fast-growing AI glasses market.

Ark Invest’s Cathy Wood and Wedbush analyst Dan Ives think that Tesla(TSLA -1.41%) is the best AI stock. Tesla ranks as the largest holding in Wood’s Ark Invest portfolio. Ives views Tesla as the most undervalued AI stock on the market. Tesla is best known for its electric vehicles (which feature AI self-driving technology), but CEO Elon Musk predicts that its Optimus humanoid robots will be the company’s greatest growth driver in the future.

Checking off all the AI boxes

I think solid cases can be made for Nvidia, Microsoft, Meta, and Tesla as the single best AI stock to buy. However, my vote goes to another AI leader — Google parent Alphabet(GOOG -0.04%)(GOOGL -0.14%). This company checks off all the AI boxes, in my view.

Alphabet’s Google Cloud is the fastest-growing major cloud provider. The unit uses Nvidia’s GPUs, but has also developed Tensor Processing Units (TPUs) that can be more cost-effective in specific machine learning operations.

Like Microsoft, Alphabet has integrated generative AI into many of its products, including Google Search and Google Workspace productivity software. Its Google Gemini large language model (LLM) competes against OpenAI’s GPT-5. Google’s research into transformers (the “T” in GPT) paved the way for today’s LLMs, by the way.

Google DeepMind is actively working on artificial general intelligence (AGI), a critical stepping stone to ASI. Google Glasses were a predecessor to Meta’s AI glasses. Google teamed up with Warby Parker to develop smart glasses using the extended-reality operating system Android XR that will compete against Meta’s devices.

Alphabet’s Waymo unit has a solid head start on Tesla in the autonomous ride-hailing market. Google DeepMind is developing humanoid robots that use the Gemini 2.0 AI model. And, with apologies to Wedbush’s Ives, Alphabet’s stock appears to be more attractively valued than Tesla on every commonly used metric.

Is Alphabet the single best stock to buy for the AI revolution?

Are there risks for Alphabet? Absolutely. Rivals are hoping to chip away at Google Search’s market share. Some industry observers have even predicted that generative AI presents an existential threat to Google Search. Alphabet’s dominance in multiple arenas makes it a big target for regulatory agencies in the U.S. and Europe.

However, Google’s integration of generative AI into its search engine appears to be paying off so far. The regulatory threat against Alphabet also doesn’t seem nearly as concerning after a federal judge didn’t impose the worst-case penalties against the company in a recent decision in an antitrust case.

Multiple stocks will be big winners in the AI revolution, probably including all of the ones discussed earlier. However, if I had to pick the single best AI stock to buy, it would be Alphabet.

Keith Speights has positions in Alphabet, Meta Platforms, and Microsoft. The Motley Fool has positions in and recommends Alphabet, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Deals with Apple and the U.S. Government are steps in the right direction.

It’s been an outstanding year to own MP Materials(MP 0.56%) stock. From the end of 2024 through Oct. 3, 2025, Shares of the rare earth metals and magnets producer rose 358%.

The U.S. Government’s push to reshore manufacturing is the tailwind pushing this stock forward. Magnets made from rare earth elements, especially neodymium, are essential components in electronic vehicles, military drones, and everyday consumer electronics.

The first thing to know about rare earth magnets is that China is the world’s leading supplier of refined rare earth metals. This April, China halted exports of rare earth metals to the U.S. to strengthen its position when negotiating new tariffs. That decision has plenty of American businesses eager to build a more secure supply chain.

Image source: Getty Images.

In the right place at the right time

As the only operational rare earth mine operator in the U.S., MP Materials is an obvious beneficiary of a reshoring push. Recently, USA Rare Earth has collected a great deal of capital with the intention of creating an end-to-end magnet production chain. The potential competitor acquired some mining rights in Texas, but it hasn’t begun extracting any minerals yet.

As the only magnet manufacturer with an operational mine, MP Materials is in a good position to receive government assistance. In July, the company entered a partnership with the U.S. Department of Defense (DoD) to build up the country’s rare earth magnet supply chain.

MP Materials intends to use government funds to construct a second domestic magnet manufacturing facility to be called the 10x Facility. Once complete, DoD has agreed to ensure the sale of every magnet the new facility produces for 10 years. The company thinks it can produce 10,000 kilograms annually with help from the new facility, once it’s built.

Also in July, MP Materials announced an agreement to sell magnets to Apple for use in its popular devices. Magnet shipments to the iPhone manufacturer are expected to begin in 2027.

Missing the most important part of the supply chain

Before getting too excited about MP Materials, it’s important to understand that its facilities for refining ore into metal that can be used to manufacture magnets are small. This is why the deal with Apple involves recycling old magnets, not producing new ones from ore the company dug up in its Californian mining operation.

The 10x Facility to be built in partnership with DoD is for manufacturing magnets. It isn’t the big refinery that the company needs to actually remove China from its supply chain. The company only expects to improve the minor refining operation at its Mountain Pass, California facility.

It’s unlikely that MP Materials’ planned improvements will allow for much independence from Chinese imports. Rare earth metal refining is a chemically intensive process that produces heaps of health-threatening pollution. It’s hard to imagine environmental regulators in California letting such a refinery operate at scale.

Why MP Materials’ stock is risky

Investors who buy MP Materials at recent prices need the company to overcome some extremely high expectations, or they could suffer heavy losses. Most basic materials companies trade at price-to-sales multiples in the low single digits. With a market cap north of $12.6 billion, this stock is trading at 48 times trailing 12-month sales.

The DoD established a guaranteed minimum price of $110 per kilogram of neodymium and praseodymium (NdPr) to be processed at the 10x Facility. The company hasn’t broken ground yet. Even if we can assume it will rapidly complete construction and begin selling 10,000 kg annually to DoD at that price, we can only expect about $1.1 billion annually.

A bet on MP Materials now is a bet that its new battery recycling program with Apple succeeds. New investors are also betting on perfect execution regarding its partnership with DoD. Those bets entail more risk than most investors should feel comfortable with. It’s probably best to keep this company on a watchlist for now and revisit it after its 10x Facility is up and running.

Cory Renauer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Apple. The Motley Fool recommends MP Materials. The Motley Fool has a disclosure policy.

Warren Buffett’s company owns these stocks, and they could be great additions to your portfolio.

Berkshire Hathaway CEO Warren Buffett helped turn the investment conglomerate into one of the world’s most valuable companies. With a market capitalization of approximately $1.08 trillion as of this writing, Berkshire ranks as the world’s 11th-biggest business (at the time of this writing).

Given Berkshire’s incredible success, it’s little wonder that many investors pay close attention to the company’s stock holdings and strategies. Read on to see why two Motley Fool contributors think that these Berkshire Hathaway portfolio components stand out as great buys right now.

Image source: Getty Images.

One of Buffett’s favorites

Jennifer Saibil (Apple): Warren Buffett has been selling Apple(AAPL 0.28%) stock left and right, so I might be going against the grain to say that Apple is one of his best stocks to buy today. But Buffett himself is a contrarian investor, so I’m only following in his footsteps.

In any case, Apple is still the largest stock in the portfolio, accounting for more than a fifth of the total, so Buffett hasn’t lost confidence in it at all. He has said he would never sell as long as he’s controlling Berkshire Hathaway, but that time is coming to an end, and investors are already speculating as to whether Greg Abel will keep it in the portfolio.

But many of the same reasons Buffett originally bought it still hold today. Apple has a large and differentiated consumer products business with a sticky ecosystem, and loyal fans purchase an assortment of its devices, which easily connect to each other. Although it’s often labeled as a tech business, which isn’t in Buffett’s wheelhouse, it’s at least as much the kind of consumer products business that he loves. The tech part also gives him exposure to artificial intelligence (AI), which may not be the reason he bought it, but is a reason many other investors might find it exciting.

So far, Apple Intelligence has disappointed investors. Apple hasn’t released AI services that stand out, and it doesn’t have a strong timeline for when it will.

Still, the recent debut of its newest iPhone, the iPhone Air, demonstrates why fans love Apple and rush to buy its latest launches. It’s the thinnest smartphone on the market, and the design appeals to style-conscious users who often wear their devices as statement pieces. Apple just debuted several new launches that will go on sale later this month, including the new iPhone17 that ramps up the quality and capabilities users love and pay up for, and new AirPods that use Apple Intelligence to translate language in real time.

In other words, Apple is still on top of its game, and it isn’t likely that its customers are going anywhere else anytime soon. However, Apple stock fell after the new products were announced, and it’s down 10% this year. The market didn’t seem to think its launches had enough innovation, especially with AI. That makes this a great opportunity to buy on the dip for the long-term investor.

Amazon stock still looks like a great long-term play

Keith Noonan (Amazon): Like Apple, Amazon(AMZN -1.34%) stock has been a high-profile tech-sector underperformer in 2025. The e-commerce and cloud computing giant’s share price is up just 2% across this year’s trading. Meanwhile, the S&P 500 index’s level has risen roughly 15%, and the Nasdaq Composite‘s level has surged approximately 18%.

Also like Apple, Amazon is also part of Berkshire Hathaway’s stock portfolio. Coming in at just 0.7% of Berkshire’s public stock holdings, Amazon occupies a relatively small position in the investment conglomerate’s portfolio — but I think the tech leader stands out as a strong long-term investment at today’s prices.

Trading at roughly 33.5 times this year’s expected earnings, Amazon admittedly still has a growth-dependent valuation. On the other hand, the extent to which the stock has underperformed the broader market in recent years points to an opportunity. For reference, the company’s share price has risen just 43% over the last five years. Meanwhile, the S&P 500 and Nasdaq Composite have both more than doubled across that stretch.

There are some good reasons behind the underperformance. For starters, the company’s e-commerce business faced some substantial headwinds from supply chain disruptions and inflationary trends connected to the pandemic. With the majority of the company’s sales still coming from its e-commerce business, Amazon is also facing some pressures from tariffs.

On the other hand, Amazon remains one of the world’s strongest businesses — and it’s likely in the early stages of capitalizing on AI-related tailwinds that power incredible new growth phases. The growth catalysts that AI can present for the company’s cloud-infrastructure services business seem to be acknowledged but still broadly underappreciated. Meanwhile, the market seems to be largely overlooking the transformative impact that AI and robotics will have on margins for its e-commerce business. With Amazon positioned to benefit from powerful tech trends, the stock looks like a smart buy while it’s still a market laggard.

Jennifer Saibil has positions in Apple. Keith Noonan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Apple, and Berkshire Hathaway. The Motley Fool has a disclosure policy.

IonQ’s share price is rocketing higher, but the company’s long-term success is anything but guaranteed.

Quantum computing holds a lot of promise to impact fields such as climate science, pharmaceuticals, artificial intelligence (AI) modeling, and much more. Many investors are keen on getting in on the ground floor of new tech trends because, as artificial intelligence stocks have proven, buying early can pay off in spades.

That optimism may be fueling the staggering gains of more than 600% that IonQ(IONQ 5.29%) has returned over the past year. Some investors, no doubt, are wondering if they’re missing out by not owning IonQ. But there are a few reasons why investors may want to pause before buying IonQ stock. Here are a few.

Image source: Getty Images.

Expenses are rising, and losses are widening

IonQ is in growth mode right now, which means that the company is investing heavily into building its technology so that it can, ideally, outpace its competitors and generate significant revenue and earnings down the road.

There’s nothing wrong with that, and many growth companies, especially in the tech sector, do this. But it’s important to highlight how much money IonQ is losing in relation to its revenue. The company’s research and development spending spiked more than 230% in Q2 as the company invested in new tech and acquisitions. For reference, IonQ spent more on R&D in Q2 of 2025 than it did in the first nine months of last year.

That spending contributed to significant losses for the company of $177.5 million, up from a loss of just $37.5 million in the year-ago quarter. If we look at IonQ’s loss on an earnings before interest, taxes, depreciation, and amortization basis (EBITDA), things look a little better, but not great. The company’s EBITDA loss was $36.5 million in the quarter, an increase from $23.7 million in the year-ago quarter.

Revenue is growing quickly, with sales jumping 81% in the quarter, but it’s still a modest amount of about $21 million. With losses expanding and IonQ likely to continue spending on R&D and potential acquisitions, revenue will have to accelerate dramatically for the company to eventually offset its losses.

The stock is pricey, and quantum computing is speculative

Even if you’re comfortable with the company’s losses, I think IonQ’s valuation and the speculative nature of the quantum computing market are two more reasons to hold off on buying IonQ. The company’s shares have a price-to-sales ratio of 303, which is very expensive even by tech stock standards — with software application and infrastructure stocks having an average P/S ratio of just 4.

That means IonQ’s sales have to grow at a tremendous rate in order to justify its stock’s current premium price tag, making its most recent revenue increase of 83% in Q2 appear relatively modest.

What’s more, quantum computing is still in its early stages, and even some technology heavy hitters, including Alphabet and Microsoft, believe its practical use cases are still years away. This means IonQ could continue investing in quantum computing technologies, widening its losses, with revenue increases that don’t keep pace with spending, all while betting that quantum computing demand will be there years from now.

IonQ is not a buy

When you add up all of the above, I think IonQ is too risky to buy right now. Its share price has surged at a time when it seems like nothing could dent the stock market’s returns, and I think a little too much optimism has crept into the market, pushing valuations very high.

I think investors would be better off monitoring how well the company’s revenue grows over the coming quarters, see if it can narrow its losses, and find out whether the quantum computing market delivers on its high hopes. But for now, IonQ looks too speculative for my liking.

Chris Neiger has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

The Oracle of Omaha probably won’t ask for stock advice. But he’d probably like this stock.

Does Warren Buffett need help selecting stocks? Of course not. He’s done a really good job of doing it all on his own for decades.

Sure, the legendary investor would likely insist that he’s a “business picker” rather than a stock picker. Buffett would also probably point out that he has farmed out some of the decision-making to his two investment managers, Todd Combs and Ted Weschler, for quite a while.

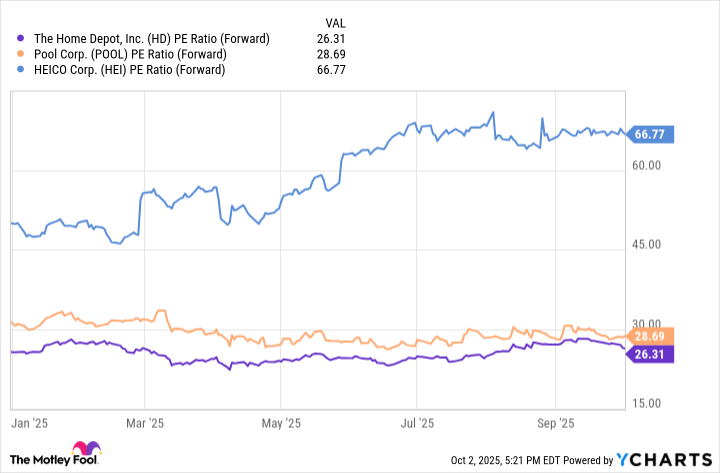

But let’s suppose that Buffett asked me to give him a hand choosing one stock to buy for Berkshire Hathaway‘s (NYSE: BRK.A)(NYSE: BRK.B) portfolio. If that wild scenario happened today, which stock would I recommend? I think I’d go with The Home Depot(HD -0.04%).

Image source: The Home Depot.

Why Home Depot would make a great Buffett stock

I view Home Depot as a great Buffett stock in part because it once was a Buffett stock. He initiated a position in the home improvement giant 20 years ago but eventually sold all of Berkshire’s stake in the second quarter of 2009.

Buffett might wish he had held onto those shares in retrospect. Over the 14 years since he exited Berkshire’s position in Home Depot, the stock has skyrocketed roughly 1,570%. That’s more than double the gain delivered by Berkshire Hathaway itself. The Home Depot’s total return, including reinvesting dividends, since Buffett bailed on the stock in 2009 is around 2,370%.

We don’t have to worry about Buffett not liking Home Depot’s business. It’s certainly one that he understands. Buffett has even recently bought stocks that benefit from some of the same trends as Home Depot — homebuilders D.R. Horton(NYSE: DHI) and both share classes of Lennar (NYSE: LEN)(NYSE: LEN.B).

The median age of U.S. homes has increased quite a bit since Buffett last owned Home Depot. It stood at 41 years in 2023, according to the American Community Survey. Aging homes bode well for demand for home improvement products and supplies over the coming years.

The fly in the ointment

Is Home Depot the perfect Buffett stock? I wouldn’t go that far. There is one fly in the ointment.

Like many stocks these days, Home Depot has a relatively high valuation. Its trailing 12-month price-to-earnings (P/E) ratio and its forward P/E are close to 26. Buffett learned from the father of value investing, Benjamin Graham. Would he balk at paying such a premium for Home Depot? Maybe, but maybe not.

Berkshire bought 12 stocks in Q2. Several of them were bargains that you’d expect Buffett to like. However, two had forward earnings multiples that have been consistently higher than Home Depot’s all year: Heico(NYSE: HEI), which currently trades at a sky-high 66.8 times forward earnings estimates, and Pool Corp.(NASDAQ: POOL), which has a forward P/E of 28.7.

Perhaps Heico and Pool are part of the portfolio managed by Combs and Wexler. However, Buffett hasn’t been afraid of paying more for quality in the past when he’s been confident about a company’s long-term earnings growth prospects.

Is Home Depot a good pick for every investor?

I selected Home Depot because it was a stock I thought would fit well with Buffett’s investing style. Is this stock a good pick for every investor? Probably not.

I suspect that a purist value investor (which I don’t think describes Buffett, by the way) would prefer to quickly move past Home Depot for the reasons already discussed. The home improvement retailer’s dividend yield of 2.3% might not be juicy enough for some income investors. And growth-oriented investors can certainly find stocks that are more likely to deliver stronger earnings growth than Home Depot.

And even though Home Depot is the stock I’d pick for Buffett, I don’t personally own it. I like the stock, but I like others more. And, unlike Buffett, I’m not sitting atop a cash stockpile of $344 billion.

Keith Speights has positions in Berkshire Hathaway. The Motley Fool has positions in and recommends Berkshire Hathaway, D.R. Horton, Home Depot, and Lennar. The Motley Fool recommends Heico. The Motley Fool has a disclosure policy.

Despite a long history of returning value to shareholders, these two industry giants have traded lower over the past year — but it’s an opportunity for investors.

“Do you know the only thing that gives me pleasure? It’s to see my dividends coming in.”

– John D. Rockefeller

Rockefeller was onto something there: Receiving quarterly dividend payments is one of the most satisfying things for anyone looking to reinvest for the power of compounding.

These two dividend stocks offer investors not only a long history of consistent dividends (and increases), they also both have strong economic moats to help ensure financial growth over the long haul. Here’s why these two deserve income investors’ consideration.

Getting back to its higher-margin roots

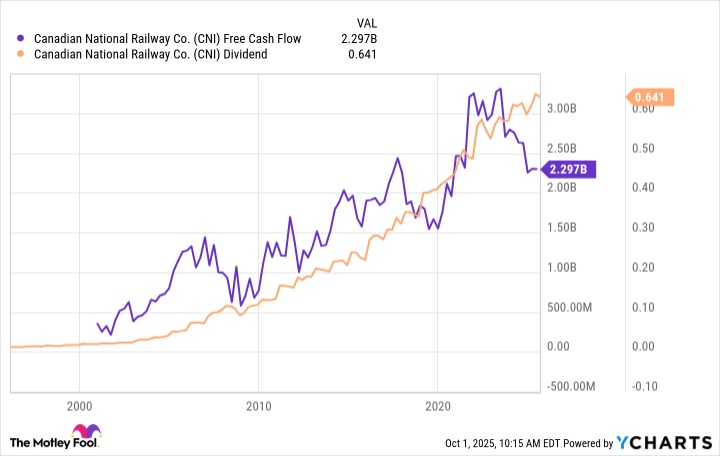

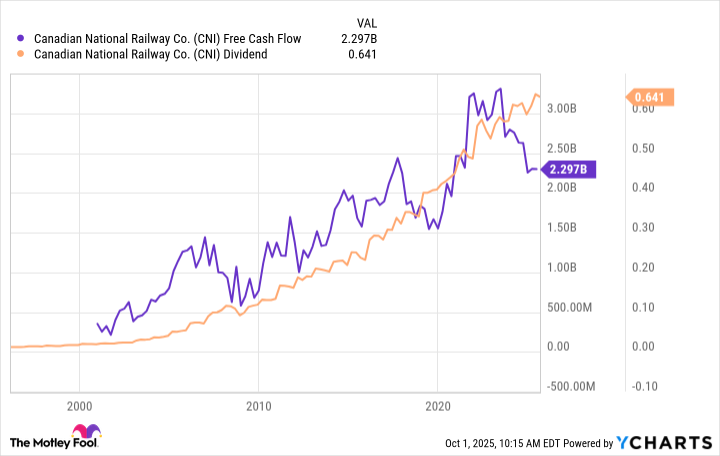

The Canadian National Railway (CNI 1.99%) is a powerful company, driving the economy by transporting more than 300 million tons of natural resources, manufactured products, and finished goods throughout North America annually. It has nearly 20,000 miles of rail lines and related transportation services, connecting Canada’s East and West Coasts, and the Midwest, including a valuable route through Chicago and all the way to New Orleans.

What makes CN (as it’s known for short) a great dividend stock is an economic moat that’s based not only on its geographic reach but also on its extensive railroad infrastructure that’s nearly impossible to replicate. And it’s the primary and most significant rail operator for the Port of Prince Rupert in British Columbia, which contributes to its intermodal growth potential.

Those competitive advantages and its moat help the company continue to print cash, and in turn increase its dividend. The growth of both is obvious in the graph below.

CN has closed the margin gap with competitors in recent years, after having led the industry in the early 2000s thanks to pioneering the practice of precision scheduled railroading (PSR). However, the father of PSR, Hunter Harrison, took his talents to competitors in 2009, and while his innovations still have their imprint on the business, the company needs to refocus on margins.

While that process develops, investors have a respectable dividend yield of 2.7% and a history of consistent increases.

A snack and beverage juggernaut

PepsiCo(PEP -0.24%) is a household name and global leader in snacks and beverages with brands including its namesake Pepsi, as well as Gatorade, Lay’s, Cheetos, and Doritos, among many others. The company dominates the global market for savory snacks and is the second-largest beverage provider, behind only Coca-Cola.

One factor in investors’ favor is the company’s diversification with exposure to carbonated soft drinks, water, sports and energy drinks, and convenience foods that generate roughly 55% of revenue. PepsiCo is truly global: International markets made up roughly 40% of both total sales and operating profits in 2024.

Image source: Getty Images.

This could prove to be a good time to pour a small investment into the company. The past few years of less than desirable growth — due to self-inflicted wounds and underinvesting in its marketing and brands — has left the stock trading lower over the past year. Management is working to reverse that and has steadied the top and bottom lines, so there should be room for improvement and a return to growth.

Not only does the demand for PepsiCo’s snacks and beverages remain resilient through economic cycles, but it also attracts investors with a healthy 4% dividend yield.

Are the stocks buys?

Over the past year, PepsiCo and CN have traded 17% and 19% lower, respectively. But a couple of missteps and headwinds won’t stop these two juggernauts for long because their competitive advantages are durable. PepsiCo is benefiting from the growth in its snack business and international expansion, while the Canadian National Railway is getting back to its roots and closing the margin gap with competitors, fueling its dividend in the future. Both warrant consideration for a small position for long-term investors looking for dividend income.

Daniel Miller has no position in any of the stocks mentioned. The Motley Fool recommends Canadian National Railway. The Motley Fool has a disclosure policy.

The AI market is booming. Bain projects the total addressable market for AI hardware and software will grow 40%-55% annually, reaching $780 billion to $990 billion by 2027.

This growth is enabling companies that provide AI tools, such as chips for data centers, to benefit as demand surges for infrastructure supporting AI applications. Nvidia(NVDA -0.77%) and Broadcom(AVGO -0.00%) stand out as early leaders of the AI megatrend. They’re turning into cash-flow machines. Both are producing such an abundance of cash that they’re returning most of their growing windfalls to shareholders.

Image source: Nvidia.

1. An AI-powered cash-flow machine

Nvidia pioneered GPU-accelerated computing, a technology that leverages specialized semiconductors and algorithms to enhance the speed of compute-intensive operations within applications. This advanced technology is crucial for supporting innovations like AI and robotics. Unsurprisingly, AI-focused tech companies have been snapping up Nvidia’s AI semiconductors to turn data centers into supercomputers.

The semiconductor company generated $46.7 billion of revenue in its recently completed fiscal 2026 second quarter. That was up 6% from the first quarter and 56% from the year-ago period. The bulk of those sales were to data center customers ($41.1 billion).

Nvidia’s AI semiconductor platform has become a cash-printing machine. During the first half of its 2026 fiscal year, the company generated nearly $43 billion in cash from operations — up from almost $30 billion during the year-ago period. Of that cash, Nvidia returned $24.3 billion to investors via dividends and share repurchases. Despite this massive cash return, the company still had nearly $57 billion in cash on its balance sheet at the end of the period.

Nvidia plans to keep returning cash to investors. With only $14.7 billion remaining on its buyback authorization at the end of the second quarter, Nvidia’s board in late August added another $60 billion for share repurchases.

Meanwhile, there’s more AI-powered growth ahead for Nvidia. The company’s Blackwell platform is becoming the gold standard in AI. Blackwell data center sales surged 17% sequentially in the second quarter and should continue growing briskly in the future as more companies adopt this technology.

2. The AI-powered accelerator

Broadcom has also been cashing in on the AI race. The infrastructure software and semiconductor company reported a 22% year-over-year increase in its revenue in its fiscal third quarter of 2025, pushing it to a record $16 billion. AI revenue growth accelerated in the period, surging 63% to $5.2 billion.

The company generated nearly $7.2 billion in cash from operations during the period. The capital-light business spent only $142 million on capital expenses, enabling it to produce over $7 billion in free cash flow, representing an impressive 44% of its revenue. Free cash flow has surged 47% over the past year.

Broadcom returned $2.8 billion of that cash to investors via dividends. The company previously increased its dividend by 11% for this fiscal year, marking its 14th consecutive year of dividend increases since initiating the payout in fiscal 2011. The semiconductor company also authorized a $10 billion share repurchase program earlier this year, $4.2 billion of which it bought back in its fiscal second quarter. Even with those robust cash returns, Broadcom ended its fiscal third quarter with nearly $11 billion of cash on its balance sheet.

The company’s robust cash flow should continue growing. Broadcom expects its AI semiconductor revenue to accelerate to $6.2 billion in its fiscal fourth quarter, pushing its total revenue up to $17.4 billion in the period. That should further boost its free cash flow, providing Broadcom with more funds to return to shareholders. The semiconductor giant will likely give its investors another sizable raise later this year when it announces its annual dividend increase, and extend its growth streak to 15 years in a row.

Cashing in on the AI megatrend

Surging global investment in AI semiconductors is transforming Nvidia and Broadcom into cash-flow machines. Their ability to convert massive AI-driven revenue into cash is allowing them to return more money to investors through dividends and buybacks. With their cash printing presses unlikely to slow down anytime soon, they’re potentially compelling investment opportunities for those seeking companies cashing in on the AI megatrend.

Matt DiLallo has positions in Broadcom. The Motley Fool has positions in and recommends Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Artificial intelligence (AI) continues to advance at an astonishing rate.

The frenzy over artificial intelligence (AI) stocks kicked off in late 2022 with the arrival of OpenAI’s ChatGPT. While this watershed moment occurred years ago, the AI market shows no sign of slowing down.

In fact, Google parent Alphabet(GOOGL -0.16%) (GOOG -0.04%) achieved a recent breakthrough with Gemini, a large language model (LLM) comparable to ChatGPT in many ways. The innovation suggests the AI industry could enjoy prosperity for decades.

If so, now may be the time to invest in AI giants like Alphabet. Here’s a dive into the company’s artificial intelligence accomplishment, as well as the implications for Alphabet’s stock and the broader AI market.

Alphabet’s AI achievement

In September, Alphabet’s Gemini achieved a groundbreaking outcome, becoming the first AI model to win a gold medal in an international computer programming competition. It successfully solved complex, real-world calculations that stymied human participants.

Google DeepMind, Alphabet’s AI research division, was responsible for Gemini. The DeepMind team highlighted the significance of the landmark achievement by stating, “Solving complex tasks at these competitions requires deep abstract reasoning, creativity, the ability to synthesize novel solutions to problems never seen before, and a genuine spark of ingenuity.”

Gemini demonstrated these traits in the competition, including successfully coming up with a creative solution to one challenge that no human participant was able to solve. This result marked a crucial step on the path toward artificial general intelligence (AGI). AGI is a theoretical level of AI proficiency considered equivalent to human thinking.

Gemini’s milestone is a memorable bellwether, akin to the moment when the world was stunned by IBM’s Deep Blue computer beating the reigning human chess champion in 1997.

How Alphabet’s milestone impacts the AI industry

A quarter-century after Deep Blue’s achievement, OpenAI’s introduction of ChatGPT opened the floodgates for the current AI boom. Now, Gemini’s breakthrough signals the start of a new era in the evolution of artificial intelligence, as the tech edges closer to the capacity for original thought.

AI is evolving from simply completing specific tasks toward solving more complex problems that require leaps in thinking — for example, designing innovative microchips or coming up with new medicines. The possibilities to upend markets in the years to come could be akin to how today’s AI is delivering unprecedented transformation across industries.

One example is Nvidia, the semiconductor chip leader. AI systems require increasingly potent computing capabilities. This need led to the company’s impressive 56% year-over-year sales growth to $46.7 billion in its fiscal second quarter, ended July 27, and drove its stock to a $4 trillion market cap.

Alphabet was among the first to power its AI with Nvidia’s new Blackwell chips. When the chip debuted in 2024, Nvidia stated, “Blackwell has powerful implications for AI workloads” and that the tech would help “drive the world’s next big breakthroughs.” Following Gemini’s AI milestone, it appears that Nvidia’s words were something more than empty marketing boasts.

The computing power needed to produce the Gemini breakthrough must have been substantial. Alphabet declined to specify how much, but admitted it was more than what’s available to customers subscribing to its top-tier Google AI Ultra service for $250 per month. With that kind of computing capability required for AI to perform advanced reasoning, Nvidia and other hardware providers can continue to benefit from AI advances.

What the Gemini breakthrough means for Alphabet stock

While building toward artificial general intelligence will increase computing costs for Alphabet, the company can afford it. Thanks to its search engine dominance, Alphabet generates substantial free cash flow (FCF) to invest in its AI systems. The company produced $66.7 billion in FCF over the trailing 12 months through Q2.

In addition, AI is already delivering business growth for the company. Its second-quarter sales were up 14% year over year to $96.4 billion as customers adopted AI features Alphabet released onto its search engine, cloud computing services, and advertising platforms.

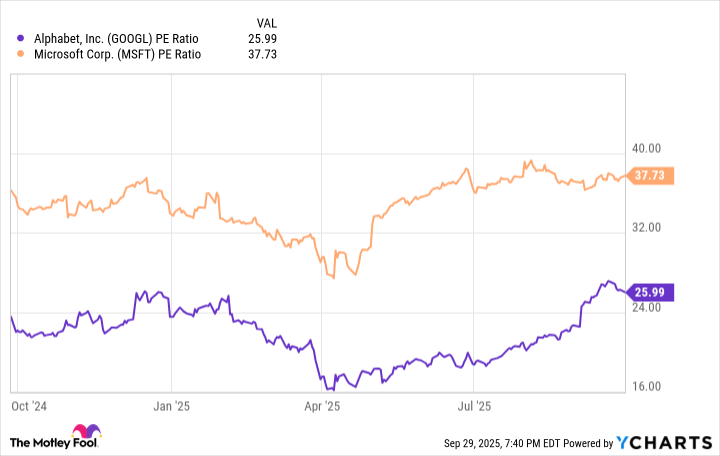

Despite these strengths and Gemini notching a significant AI victory, Alphabet shares remain reasonably valued compared to rivals such as Microsoft. This can be seen in the stock’s price-to-earnings (P/E) ratio, which reflects how much investors are willing to pay for each dollar of a company’s earnings, based on the trailing 12 months.

The chart shows Alphabet’s P/E ratio is lower than Microsoft’s, suggesting it’s a better value. In other words, now could be a good time to pick up Alphabet shares at a reasonable price.

Since the Google parent isn’t the only beneficiary of ongoing AI progress, it’s worth considering the growth potential in other AI players, such as Nvidia, IBM, and Microsoft. As the tech industry moves closer to achieving AGI, the AI space is poised for innovations that are likely to fuel the sector’s growth for decades to come.

Robert Izquierdo has positions in Alphabet, International Business Machines, Microsoft, and Nvidia. The Motley Fool has positions in and recommends Alphabet, International Business Machines, Microsoft, and Nvidia. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

On Nov. 26, 1983, six men robbed a warehouse serving London’s Heathrow Airport. Hoping to find £1 million worth of foreign currency, they found instead 6,800 gold bars, worth £26 million in 1983 money — a record-setting robbery at the time — under the temporary supervision of Brink’s-Mat. (A union of the American security firm and a British transport outfit.) This event has been transmuted into “The Gold,” an involving British drama premiering here Sunday on PBS.

The robbery itself takes up little screen time; the question on the criminal side becomes how to turn three tons of gold into cash, and for the police, one of recovering the loot and bringing the villains to justice. The cops and the criminals overlap here and there, a point screenwriter Neil Forsyth does not want you to miss, and is a particular bee in the bonnet of upright Detective Chief Superintendent Brian Boyce (Hugh Bonneville), self-contained but always ready to speak his mind. (He is also “infuriated” by what people get wrong about jazz, which he likens to police work.)

Recruited by Boyce to a special task force are detectives Tony Brightwell (Emun Elliott), historical, and Nicki Jennings (a charismatic Charlotte Spencer), invented, who are good company for the viewer and generally for each other, though as people who spend long hours sitting together in cars waiting for something to happen, they have their moments of friction, played for humor. As a created character, Jennings — who, as a woman, has to outline the many steps and hard work it took to achieve her position — offers an opportunity for emotional elaboration, notably in scenes (affectionate, prickly) with her father, Billy (Danny Webb), “by a country mile the worst villain in England,” his criminal career sidelined by ill health.

Though one of the actual robbers, Micky McAvoy (Adam Nagaitis), gets a good deal of attention, the bulk of the series involves three criminals subsequently processing the gold and laundering the money. Kenneth Noye (Jack Lowden) is “a fence with protection,” owing to his friendship with police officers through membership in the Masons. (When Boyce brings Jennings and Brightwell onto his team, he sets the rules as “no overtime, no drinking at lunchtime, no freemasonry.”) John Palmer (Tom Cullen), a dyslexic dealer in gold and jewelry, has a handy portable smelter in his yard. And the invented Edwyn Cooper (Dominic Cooper), an up-from-the-streets solicitor with posh airs and a rich wife whose snooty parents treat him with barely disguised disdain, finds himself working for “a group of businessmen who have a lot of money that needs to be made respectable,” in the words of liaison Gordon Parry (Sean Harris, sinister).

Stretched over six episodes, it’s not a speedy telling, and, in fact, a second series covering a long tail of aftermath has already aired in the U.K. Apart from some surveillance, tailing suspects, one fatal encounter and an occasional chase, there’s little in the way of capital-A Action, mostly just a lot of talk — inquisitive, instructive, threatening, discursive, domestic or speechifying. Though the production is naturalistic — in a way that ties it to an earlier, golden era of British productions — the dialogue can sound highly composed. Characters are given little monologues, often to explain how they became the person they are, that play as the sort of thing that might occur late in the last act of a stage drama: Jennings found the sirens outside her window comforting, which led her to police work, “so that kids like me will be safe”; Boyce had a life-changing moment involving a pair of red leather shoes while fighting in the so-called Cypriot Emergency. Some dialogue might have been lifted whole from a 1930s gangster film. Critiques of British class structure and bad actors within the police department are raised high enough to be impossible to miss.

There are a lot of moving parts in “The Gold,” represented in sometimes brief alternating scenes, and it may take a while, among the crooks, at least, to get a handle on things, to sort out where you are, who’s who, who’s married to whom, and what part each plays in the caper. Though Noye is arrogant enough to root against, Forsyth wants to show, as much as each character allows, the just-folks elements of his bad guys, psychologically relatable sorts who have, from early experience, a lack of opportunity, or a certain kind of genius, decided that the path to freedom is best paved with other people’s money. (“If it wasn’t for people trying trying to break out of the lives they’ve been given,” observes Boyce of his country’s social stratification, the police would be out of a job.) This may be soft-pedaling matters somewhat — to read the historical accounts might give you a different picture — but as drama it pays dividends.

As a period piece, it doesn’t oversell the era. There are old cars, of course, and more mustaches than we are currently accustomed to. But apart from the pop songs that run over the end credits, nothing screams These Are the ’80s. (Compare, for example, the “Life on Mars” sequel, “Ashes to Ashes.”) It’s more a question of what isn’t there. The detectives have a computer, but only Brightwell has an idea of what it’s for or how to use it. No cellphones, but there are walkie-talkies. A tracking device, apparently the only one in all of British law enforcement, has to be imported from Belfast (and sneakily at that). There is a refreshing absence of guns — none of those Kevlar-clad teams going in with pistols raised. (Just truncheons.) And the remodeling of East London into a gentrified glass forest, a minor plot point, has only just begun.

It’s like a vacation from now, and who can’t use one of those?

Knowing what to look for allows you to avoid joining a pyramid scheme.

Pyramid schemes are nothing new. For example, in the 1920s, Charles Ponzi promised investors high returns on postal reply coupons, using the money from new investors to pay returns to earlier investors. Like all pyramid schemes, Ponzi’s collapsed in a heap.

Because scam artists will do anything they can to separate their victims from their savings, it’s vital that seniors understand that they’re prime targets. More importantly, seniors must know how to spot and avoid pyramid schemes.

Image source: Getty Images.

Prime targets

If you’ve spent years strategizing how you’ll retire, scammers consider you a prime target. While they might not be able to con a 21-year-old out of much, they suspect you have plenty of money put away. It may be someone you meet in the park, bowling, or even at church. The scammer may be someone you’ve never heard of, someone who contacts you out of the blue, or someone who’s introduced to you by a friend.

The point is that pyramid schemes and the scammers who operate them see you as a rich source of cash.

Packaged to look like something else

Trying to sell you on a pyramid scheme involves making you believe you’re getting involved in a legitimate pursuit, like a business venture. One only needs to look at Charles Ponzi’s 1920s scam to understand how pyramid schemes work.

Ponzi, once known as a financial wizard, convinced well-meaning investors that he’d found a way to make huge profits by buying international postal reply coupons in countries with weakened currencies and selling them at a higher price in the U.S. Ponzi said he was so confident that he promised a 50% return in 90 days.

This was the “Roaring Twenties,” a decade of economic prosperity in the U.S., and many wanted in on the action. The problem with Ponzi’s plan was this: The only people who experienced a payday were those who got in early. The money from those who bought into Ponzi’s scheme later was used to pay the people on board early.

It’s the same with today’s pyramid schemes. No matter what’s promised, only a few will profit and the scheme will eventually collapse, leaving most participants holding the bag. As simple as a pyramid scheme seems, it can suck anyone in, from a new investor to someone who’s been investing for decades.

Red flags

If someone invites you to invest in a new business or one-of-a-kind product, or become part of a multi-level marketing (MLM) enterprise, here’s how you can determine if it’s actually a pyramid scheme:

More money paid for recruiting others than for product sales. If the program requires you to recruit others to join for a fee, it’s likely a pyramid scheme.

No genuine products or services sold. According to Investor.gov, fraudsters claim you’ll sell “products,” like online advertising, websites, tech services, or mass-licensed e-books. They’re creating “businesses” that are hard to value to hide the fact that they’re pyramids.

Promise of high returns. A scammer will promise you fast cash to get their hands on your Social Security, pension, annuity, and other assets. If you see a return, it’s typically paid out of money from new recruits rather than actual sales.

Promise of passive income. If you’re offered payment in exchange for doing very little, like placing online advertisements on obscure websites or recruiting others, it’s probably a pyramid scheme.

There is little or no revenue from retail sales. If you look at documents, such as financial statements audited by a certified public accountant (CPA), and those documents show income primarily from recruiting new members, it’s a serious red flag.

Complex commission structure. Legitimate companies pay commission based on products or services you sell to people outside the program. Be careful if the commission structure is too complex to be easily understood.

Protect yourself

Fortunately, once you know the signs, you’re in an excellent position to protect your interests. Here’s how:

Be skeptical. If an investment or work-from-home offer sounds too good to be true, it probably is.

Ensure sales generate income. Verify that you’ll earn money from legitimate retail sales, not just recruitment fees.

Investigate the company. Go online to read about others’ experiences.

Finally, check with the Better Business Bureau (BBB) and your state’s Attorney General to learn if the company is legitimate and whether there have been complaints. Don’t allow anyone to steal the retirement you’ve planned for so long.

It’s not too late for investors to gain exposure to the powerful AI tailwind.

Artificial intelligence (AI) isn’t just a buzzword. It’s a top priority for companies of all sizes and in all industries. The most successful businesses in the future will be those that can harness the power of this technology.

Investors must pay close attention, and the good news is that it’s not too late to join the party. Here’s one leading AI stock that I think investors should buy before the end of 2025.

AI from A to Z

You don’t have to search far and wide to find a smart AI bet. Look no further than Alphabet(GOOGL -0.16%)(GOOG -0.04%). About a decade ago, the company began shifting its strategy to focus more on AI. These days, it’s a leader in the space.

Alphabet’s family of large language models, called Gemini, are integrated with its various user-facing products and services. The company’s ad customers also benefit from AI tools that drive creativity and boost targeting capabilities that can increase return on money spent.

Google DeepMind is a leader when it comes to AI research, and Alphabet is developing its own chips, called Tensor Processing Units. And with Google Cloud, the business owns a powerful platform that enables other companies to build their own AI applications.

Time to buy

Despite being one of best ways to put money to work behind the AI trend, shares aren’t expensive. They trade at a forward price-to-earnings ratio of 23.4. I think investors would be smart to buy the stock now.

Neil Patel has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet. The Motley Fool has a disclosure policy.

Shares of the electric carmaker sold off sharply Thursday and Friday despite record deliveries and powerful catalysts on the horizon.

After sliding sharply on Thursday and Friday, Tesla(TSLA -1.41%) is back in focus ahead of its next earnings report, scheduled for Oct. 22. With a combination of record quarterly deliveries, a sharp sell-off, and an earnings report on the horizon, it’s a good time to look closely at the growth stock. Is the pullback a buying opportunity?