Don’t underestimate what could be one of your largest retirement expenses.

The scary thing about retirement is that it’s hard to know exactly how much money you’ll need to cover your costs until that period of life begins. Sure, you can estimate a budget based on certain assumptions, like where you’ll live and how you’ll spend your days. But nailing down an exact budget is pretty difficult.

Meanwhile, one of the most tricky retirement expenses to estimate is none other than healthcare. That’s because the cost there will hinge on factors like:

Still, it’s important to have a basic handle on what healthcare might cost you down the line. And recent data reveals that a good chunk of Americans are clueless in that regard.

Do you know what you might spend on healthcare in retirement?

In a recent report, Fidelity found that the typical 65-year-old today can expect to spend $172,500 on healthcare costs during retirement. But it also found that 20% of Americans have never thought about what healthcare might cost them down the line.

There are two reasons it’s important to plan for healthcare costs in retirement. First, it’s one expense that’s non-negotiable.

You can downsize your home if the costs of maintaining it are too high. And you can move to a state that’s cheaper if it helps you stretch your income and Social Security benefits. But you can’t not pay for healthcare. If you need a certain medication to function, you may not have a choice about taking it.

Secondly, healthcare has, for many years, outpaced broad inflation. When Fidelity first started estimating healthcare costs for retirement back in 2002, it found that the typical senior would spend $80,000 throughout their senior years. In the past two decades and change, that projection has more than doubled. And chances are, it’ll continue to climb.

Have a plan for tackling healthcare expenses

There are steps you can take to make healthcare in retirement more affordable, like going to your scheduled physicals and screening appointments to get ahead of potential issues and choosing the right Medicare plan. But there may be only so much you can do to keep your costs down.

That’s why it’s so important to save well for healthcare specifically. And while you could always boost your IRA or 401(k) plan contributions, you may want to allocate funds in a separate account specifically for healthcare.

In that regard, a health savings account, or HSA, is a great option to look at. The nice thing about HSAs is that they’re triple tax-advantaged, which means:

Contributions go in tax-free

Investment gains are tax-free

Withdrawals are tax-free when used to cover qualifying healthcare expenses

Plus, HSAs are extremely flexible. You can withdraw your money at any time, and your money will never expire.

Also, if you end up in the enviable position of having lower healthcare costs in retirement than expected, your HSA won’t go to waste. When you’re under age 65, HSA withdrawals for non-medical expenses incur a steep penalty. But that penalty is waived once you turn 65, at which point an HSA can function like a traditional IRA or 401(k) plan.

Between Medicare premiums, deductibles, copays, and other expenses, you may find that healthcare in retirement costs more than expected. Read up on healthcare costs so you’re not caught off guard once your career comes to an end. Better yet, make sure you’re saving for your future healthcare needs so you never have to be in a position where you have to skimp on care because of the price tag attached to it.

Shares may look pricey, but Broadcom is still one of the top AI investments.

As one of the leading semiconductor companies, Broadcom (AVGO -1.24%) has handily outperformed the market recently. It’s up 51% year to date (as of Oct. 17), while the S&P 500 index has risen 13%.

Following such a rally, this might not seem like the ideal time to invest in Broadcom — the stock is trading near its all-time high. Given the tech giant’s growth, however, its stock can continue to climb. Here’s one reason why.

Image source: Getty Images.

A growing list of high-value partnerships

On Oct. 13, Broadcom and OpenAI, the developer of ChatGPT, announced a partnership on 10 gigawatts of custom artificial intelligence (AI) accelerators. Broadcom will be helping OpenAI design its own custom chips, and this is just the latest of several AI companies that are working with Broadcom for that purpose.

Broadcom makes custom AI chips for three major hyperscalers, believed to be Alphabet, Meta Platforms, and ByteDance, the parent company of TikTok. It’s seeing increasing chip demand from these companies, and CEO Hock Tan has also mentioned a fourth major customer that has placed $10 billion worth of orders. While there was speculation this mystery customer was OpenAI, Broadcom has now said that’s not the case.

Broadcom’s share price has been soaring, but it’s not fueled by hype. Revenue is on the rise, particularly its AI revenue, which increased 63% year over year to $5.2 billion in Q3 2025. Tech companies are increasingly turning to Broadcom for custom chips that better fit their needs and to avoid being overly reliant on graphics processing units (GPUs) from Nvidia.

During Broadcom’s last earning call, Tan mentioned that the company has an order backlog of over $110 billion, an indicator that its excellent revenue growth should continue. Don’t let the valuation deter you — Broadcom’s crucial role in AI development makes it one of the stronger tech companies to invest in.

Lyle Daly has positions in Broadcom and Nvidia. The Motley Fool has positions in and recommends Alphabet, Meta Platforms, and Nvidia. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

Nvidia stock has skyrocketed over the past few years amid excitement about the company’s AI dominance.

About a year ago, Nvidia(NVDA 0.86%) was facing one of its biggest moments ever. The artificial intelligence (AI) chip giant was launching its new Blackwell architecture, a system that was being met with “insane” demand as CEO Jensen Huang told CNBC at the time. The company announced Blackwell in March 2024 and the fourth quarter of the year was the first to include Blackwell revenue.

Blackwell was to be the first release of a new routine for Nvidia: launching chip or entire platform updates on an annual basis. Since that time, this new architecture has helped Nvidia’s earnings roar higher, with Blackwell data center revenue climbing 17% in the most recent quarter from the previous one. In the report, Huang said, “The AI race is on, and Blackwell is the platform at its center.” Meanwhile, Nvidia stock has reflected all of this, advancing 40% so far this year.

Now, it’s logical to wonder where Nvidia will be as this story progresses, for example, 24 months after the Blackwell launch. Here’s what history says.

Image source: Nvidia.

Nvidia’s path in AI

First, though, let’s consider Nvidia’s path in the AI market so far. The company has always been a graphics processing unit (GPU) powerhouse, but in its earlier days, it mainly sold these high-performance chips to the gaming market. As it became clear that their uses could be much broader, Nvidia developed the CUDA parallel computing platform to make that happen — and then, as the potential of AI emerged, Nvidia didn’t hesitate to put its focus on this exciting market.

That proved to be a fantastic move as it helped Nvidia secure the top spot in the AI chip market — and the quality and speed of its GPUs has kept it there. All of this has resulted in several quarters of double- and triple-digit revenue growth as well as high profitability on sales — gross margin has generally surpassed 70% in recent times.

To keep this leadership going, Nvidia committed to ongoing innovation, with the promise of updating its chips once a year. The company kicked this off with the launch of Blackwell about a year ago, then released update Blackwell Ultra a few months ago. Next up on the agenda is the Vera Rubin system, set for release late next year.

From platform to platform

All of these platforms operate together seamlessly, so customers don’t have to wait for a specific one and instead can get in on Nvidia’s current system and easily move forward with the latest innovations when needed. Still, as mentioned earlier, demand from big tech customers for the latest systems has been great — they want to win in the AI race and to do so aim to get their hands on the best tools as soon as possible.

So, where will Nvidia be 24 months after the Blackwell launch? The clues so far suggest revenue will continue to climb in the double-digits — and Wall Street’s average estimates call for a 33% increase in revenue next year from this year’s levels. And as Rubin is released, demand is likely to increase for that system as customers’ interest in gaining access to the latest AI technology continues.

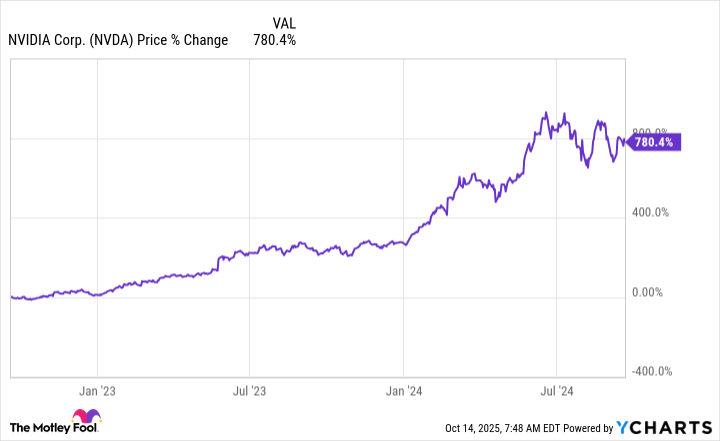

But what about Nvidia’s stock price? History offers some clues. Prior to this time, Nvidia’s major recent releases happened every two years. We can look back to the launch of the Ampere platform on May 14, 2020, and the release of Hopper on Sept. 20, 2022. And each time, over the next 24 months, Nvidia stock soared in the triple digits. It climbed 120% in the two years following the Ampere release and more than 700% following the release of Hopper.

History shows Nvidia stock is on track for a triple-digit gain two years after the Blackwell launch. If we use the starting point as the first quarter of Blackwell revenue — this quarter ended on Jan. 26, 2025 — we can see the stock has climbed about 30% so far. But Nvidia still has plenty of time to post more Blackwell sales and potentially see its shares advance in the triple-digits from their level earlier this year through the first month of the 2027 calendar year.

To illustrate, a 100% gain from early 2025 levels would bring the stock price to $284, and that would result in $6.9 trillion in market cap by the start of 2027. This fits into a scenario I wrote about recently, predicting Nvidia will reach $10 trillion in market value by the end of the decade.

Of course, it’s impossible to guarantee this outcome — any negative geopolitical or economic news, or even an unexpected problem like a decline in tech spending could hurt Nvidia’s revenue and stock performance. But, if these potential risks don’t materialize, history could be right — and Nvidia stock may find itself significantly higher 24 months after the Blackwell launch.

We paid half of what we were going to – and it was a nice way to end the holiday

This article contains affiliate links, we will receive a commission on any sales we generate from it. Learn more

We sat outside and watch planes land and take-off(Image: Sophie Buchan)

Screaming kids and a four-hour delay. That’s what my boyfriend and I were faced with when we set foot in the airport last week – and after we decided to escape to the airport lounge no matter the cost, we were shocked that we were entitled to a discount, cutting the price in half.

Flying from Tenerife, we were due to land back home in Scotland at 11pm and instead arrived home at 4am – so it’s safe to say it was a heck of a delay. Thankfully, though, as my partner is a member of Monzo Premium, he got us a discount, and we had no idea it was a perk he was entitled to.

On top of that, airport chairs are not comfy enough for a three-hour wait – and that doesn’t even include waiting to board once we’re called to our gate. So how do you get the discount and how much did we end up paying?

How to get an airport lounge discount worldwide

We ended up paying a total of around £48, which brought it down to £24 each. Saving us half the price, we were delighted. We were given free WI-FI, access to showers (towels provided) as well as all-you-can-eat food and drink – including alcohol.

Explained on the Monzo Help page, the online-based bank revealed they have teamed up with LoungeKey to give anyone with Monzo Premium or Monzo Max discounted access to airport lounges worldwide.

It explained: “You and guests can access 1,100 airport lounges around the world for a flat fee of £24 per person, per visit. This rate includes Max Family, and you will need to pay per person, per visit.

“You are required to complete strong customer authentication (SCA) before visiting a lounge for the first time. You will only need to go through this process once, as subsequent transactions will be processed from your stored card on file.

“If you replace your card you will need to re-register the payment method and complete SCA again, this includes physically presenting your new card at the lounge the first time you intend to use it.”

Do you have to pre-book?

We didn’t book and instead just turned up, as it was never our plan to go to the lounge until we were faced with loud kids and a massive wait. Monzo explained that some lounges will allow you to pre-book before your visit.

Howeve,r if you go for this option, you will be charged at least £6 on top of your discounted price. It states this price is determined by the airport lounge and has nothing to do with Monzo.

It added: “If you visit on the day without pre-booking, you will just pay the discounted price of £24 per person, but this is dependent on whether the lounge has space.”

It is worth noting that Monzo says that customers will need to have their physical Monzo card with them for their first visit. We had ours with us, but were also able to give the staff the number on our card to get the benefit too.

So where are you planning on holidaying next – and will you be getting comfy in an airport lounge? Let us know in the comments.

A lot of people start collecting Social Security specifically because they’ve stopped working, or when they’re ready to stop. But you should know that if you wish to work while collecting Social Security, that option exists.

However, there are rules you should know in the context of working while on Social Security. Here’s a rundown.

Image source: Getty Images.

Working while on Social Security has its advantages

You may find that your Social Security benefits aren’t enough to cover your retirement expenses in full. If you don’t have an IRA or 401(k) to supplement with, then you may be inclined to work in some capacity to make up the difference.

Once you reach full retirement age, which is 67 for people born in 1960 or later, you don’t have to worry about having Social Security benefits withheld for working, regardless of what you earn. But if you’re collecting Social Security before having reached full retirement age, you’ll be subject to an earnings test whose limits change annually.

This year, for example, you can earn up to $23,400 without having any Social Security withheld if you’re under full retirement age. Beyond that point, you’ll have $1 in Social Security withheld per $2 of income.

The earnings-test limit is much higher if you’re reaching full retirement age at some point in 2025. In that case, it’s $62,160. And beyond that point, you’ll have $1 in Social Security withheld per $3 of income.

If you’re under full retirement age but also earn less than the earnings-test limit, you can enjoy a nice supplement to your income without any negative impact. And even if you have benefits withheld for exceeding the earnings-test limit, you’ll get that money back eventually.

Once you reach full retirement age, your monthly benefits will be recalculated and boosted to make up for withheld Social Security earlier on. That could be a good thing, because if you get used to living on less and your monthly benefits go up substantially, it could feel like a bonus of sorts.

You may get larger monthly benefits for another reason

In addition to putting more money in your pocket, working while on Social Security could set you up for larger benefits down the line. The formula used to calculate your benefits accounts for your 35 highest-paid years of earnings while adjusting earlier wages for inflation.

If you earn a lot while collecting Social Security, you might replace a year of lower income with a higher income. That could, in turn, lead to larger benefit payments.

Let’s say you worked for 35 years, but for three of those years, you only worked part-time and earned very little. If you work part-time while on Social Security and bring in $22,000 over the course of the year, you’ll be below the earnings-test limit.

But $22,000 may also be a lot more than what you earned during one of your years of part-time work, even with those earlier wages adjusted for inflation. So you may find that working leads to a more generous monthly payday for life once the Social Security Administration is able to factor your most recent wages into your benefit formula.

Know the rules

You may have heard that working while on Social Security is not a good idea because of the earnings-test limit. Or, you may be under the impression that if you’re getting monthly benefits, you’re barred from working, period.

It’s important to understand the rules of working while collecting Social Security so you’re able to supplement your income as you please. And you may find that holding down a job while receiving benefits gives you more money not just from those wages, but in the form of larger monthly Social Security checks later on.

RMDs can seem confusing at first, but the calculation is pretty simple.

You probably think of the money in your retirement accounts as yours, but if you have traditional IRAs or 401(k)s, it’s not that straightforward. You owe the IRS a cut of your savings, and at a certain point, it forces you to start taking required minimum distributions (RMDs). These are mandatory annual withdrawals that you must pay taxes on.

If you’re new to RMDs, they can seem a little intimidating. Failing to withdraw the required amount results in a steep 25% tax penalty on the amount you should’ve withdrawn, so it’s important to know how to calculate yours correctly. Let’s look at the example of a retirement account with a $500,000 balance.

Image source: Getty Images.

Three situations where you don’t have to take an RMD

You won’t have to take an RMD from your retirement account if any of the following are true:

You’re under age 73: RMDs begin in the year you turn 73. If you turn 73 in 2025, you technically have until April 1, 2026 to take your first RMD. In all subsequent years, you must take RMDs no later than Dec. 31 of that year.

It’s a Roth account: You fund Roth accounts with after-tax dollars, so you can enjoy tax-free withdrawals in retirement. Because of this, the government has no incentive to force you to take money out each year.

The account is associated with your current employer: If you’re still working, you can delay RMDs from your current employer’s retirement plan until the year after the year you retire. However, you still have to take RMDs from old 401(k)s and traditional IRAs,if you have any.

If none of these things apply to you, then you will need to take an RMD. Fortunately, they’re not too difficult to calculate.

How to calculate your RMD on a $500,000 account

You calculate your RMD using the balance as of Dec. 31 of the previous year — Dec. 31, 2024 for your 2025 RMD. If you don’t know what your balance was at that time, you may need to look it up or speak to your plan administrator.

Once you know the amount, all you need to do is divide that by the distribution period next to your age in the IRS’ Uniform Lifetime Table. The result is your RMD.

So, for example, if you had $500,000 in your 401(k) as of Dec. 31, 2024 and you turned 73 in 2025, your RMD would be $500,000 divided by 27.4 — the distribution period for 73-year-olds. That comes out to about $18,248.

You’re free to take out more than this if you’d like. But this is the minimum amount you must withdraw in order to avoid the 25% penalty.

What if you don’t want to take your RMD?

Avoiding mandatory withdrawals generally isn’t worth it. The 25% penalty will likely cost you more than what you would’ve paid in income taxes if you’d just taken the RMD as scheduled.

That said, sometimes you may not want to deal with the extra taxes an RMD can bring. In that case, consider making a qualifying charitable distribution (QCD). This is where you ask your plan administrator to send an amount equal to your RMD or a portion of it to a qualifying tax-exempt organization.

The money must go directly to the charity. If the plan administrator distributes it to you first, it does not count, even if you give it all away to charitable causes. Done properly, the IRS won’t tax you on this retirement account withdrawal, and it’ll consider your RMD satisfied for the year.

The maximum QCD you can make in 2025 is $108,000. This should be more than enough for most people.

You may have already spent an amount equal to your RMD on living expenses this year. In that case, you’re in the clear until next year. Check with your plan administrator if you’re unsure how much you’ve already withdrawn from your accounts in 2025. If you come up a little short, be sure to make some more withdrawals in the next few weeks.

According to Experian data, the average American driver pays roughly $2,328 per year for full coverage auto insurance in 2025. If you carry only the minimum coverage required by your state, that drops to about $1,546 annually.

Of course, those are just averages. Your actual rate might be far higher or much lower. It all depends on personal factors, like where you live, what kind of car you drive, and your claims history.

So how do you stack up?

My personal rate

For example, my current full-coverage policy runs about $1,047 a year here in California. I’ve got a clean driving record, great credit, a family minivan (yep, full dad mode), and I only rack up around 6,000 miles a year.

I pay less than half the national average — but it didn’t happen by luck. I make it a habit to compare quotes every so often and keep my profile in top shape.

Insurance companies use dozens of factors to gauge your risk and determine your policy rate.

Some of these factors you can control, others not so much.

Here are the biggest ones that matter:

Location: Rates differ wildly by state and even ZIP code. Drivers in Maryland, for instance, might pay more than double what drivers in Vermont do.

Driving record: Tickets, accidents, and DUIs can raise your rate for years.

Vehicle type: Minivans and sedans generally cost less to insure than luxury or sports cars.

Credit score: In most states, a higher credit score can help lower your premium.

Annual mileage: Driving less typically means less risk — and lower rates.

Coverage level: Full coverage offers stronger protection but costs more.

Deductible: Choosing a higher deductible can reduce your monthly premium.

Knowing which levers you can pull gives you real control over your rate.

Why it pays to compare

Every year, your car gets a little older, your driving record gets a little longer, and your situation changes. Maybe you’re driving less, moved somewhere safer, or finished paying off your car.

Meanwhile, most insurance companies raise your rate each renewal — even if nothing about your risk has changed. It’s just how the system works.

That’s why checking rates once a year can pay off big.

In fact, Consumer Reports found that nearly 1 in 3 drivers switched auto insurers in the past five years. And those who did saved an average of $461 a year.

Since it only takes a few minutes to shop around, it’s always worth checking if better rates are available out there.

Personally, I like to check insurance prices once a year. Most of the time, I find I’m already getting the best deal. But every so often, I stumble across a lower rate for the exact same coverage!

No lease, no financing, no $749 a month disappearing into a lender’s account. Just my old 2007 Honda Element, still rumbling down the road. She’s not the prettiest girl at the bar anymore, but she’s all I need.

At some point, I realized every “small” car payment my friends were making could have been a serious savings engine.

The power of redirecting that $749 a month

The average new car payment today is a jaw-dropping $749 a month. Skip that for 10 years, and you’ve kept nearly $90,000 in your pocket before even earning a cent in interest.

But that money doesn’t have to sit idle. Over the past few years, the first place I’ve been putting what would’ve been my “car payment” is straight into a high-yield savings account. At around 4.50% APY, that’s earned me thousands in interest while staying completely risk-free.

While I don’t want to keep all of my money in an HYSA, I keep my emergency fund with a few months of living expenses there and just make sure it’s always topped off. Beyond that, everything flows into my favorite tax-advantaged retirement accounts.

Why I park my money in a high-yield savings account

I treat my HYSA like a first stop for the money I used to waste on car payments. It’s my emergency and peace-of-mind fund, and here’s what makes high-yield savings accounts so easy to love:

Safe and FDIC-insured up to $250,000

Instant access when you need your cash

Rates still around 4.00%, even as the Fed starts cutting

What you could do instead of sending money to a bank

Once I saw how quickly my savings grew, I realized it was really about peace of mind. I never worry about an unexpected bill or repair anymore. My high-yield savings account is my safety net, and every month I go without a car payment, that net gets stronger.

If you want that same feeling, start by opening a high-yield savings account that actually rewards you for saving. Rates around 4.00% APY won’t last forever, but getting started now could give you years of financial breathing room.

For years, I parked my savings at Wells Fargo because it felt safe and familiar. The problem is it was earning almost nothing.

Wells Fargo’s standard savings account still pays just 0.01% APY, which means every $10,000 earns $1 a year in interest. One dollar.

Then I finally moved my money into a high-yield savings account (HYSA) paying around 4.00% APY, and it completely changed the math. Even if rates dip as the Fed starts cutting, I’ll still earn over $1,000 in interest over the next two years.

Here’s how that adds up, and why I keep telling everyone I know to switch.

Earning hundreds more, even if rates fall

Right now, the best HYSAs are still offering between 4.00% and 4.50% APY.

To stay realistic, let’s assume rates drop gradually:

Year 1: 3.60% APY

Year 2: 3.20% APY

I keep about $20,000 in savings. Here’s what that earns me:

Year

APY

Interest

1

3.60%

$720

2

3.20%

$640

Total (2 years)

—

$1,360

Data source: Author’s calculations.

Now compare that with Wells Fargo:

Year

APY

Interest

1

0.01%

$2

2

0.01%

$2

Total (2 years)

—

$4

Data source: Author’s calculations.

That’s a $1,356 difference, just for moving my money to a better bank.

Lower balances still earn serious money

You don’t need a big balance to make this work. Even smaller amounts can grow fast in a high-yield account.

Switching accounts used to sound intimidating, but now it’s incredibly simple. Once you open a new HYSA, you can link it to your checking account, transfer funds, and start earning immediately.

Your money stays FDIC-insured up to $250,000, just like it was at Wells Fargo — only now it’s actually working for you.

If I’d switched years ago, I’d probably have several thousand dollars more by now. Don’t make the same mistake I did.

Don’t let your bank keep your interest

It takes less than 15 minutes to move your savings to a high-yield account that pays you what your money deserves.

Can you put a price on the experience of enjoying a World Series game at Dodger Stadium?

Yes, and it’s a very high one.

The Dodgers put tickets for potential World Series games on sale Tuesday, with the cheapest seat available for $881.95, according to an afternoon review of the team website. That seat — $800 for the ticket and $81.95 for fees — is located at the end of the reserve level, high above the field and next to the foul pole.

World Series prices posted on the website Tuesday ranged as high as $1,510.05. The best seats are sold as part of season packages, so that $1,510.05 seat ($1,371 ticket plus $139.05 fees) is located on the field level, near the foul pole and bullpen.

If the Dodgers advance to the World Series and play the Seattle Mariners, the Dodgers would play as many as four home games, starting Friday, Oct. 24. If the Dodgers advance and play the Toronto Blue Jays, the Dodgers would play as many as three home games, starting Monday, Oct. 27.

On Oct. 24, a family of four could get into Disneyland for a total of $796. On Oct. 27, a family of four could get into Disneyland for a total of $676.

Ticket prices are subject to change based on demand.

When the Dodgers put National League Championship Series tickets on sale, the cheapest price was $155. On Tuesday, the cheapest ticket on the team website for Game 3 on Thursday was $168.

However, since the game time has been set at 3 p.m. and weekday afternoon games are not popular, tickets on the resale market could be bought for about $100 Tuesday.

The danger is past, and there are lessons to learn.

Markets occasionally dump a bucket of icy water on everyone at once, and on Oct. 10, it was the cryptocurrency sector’s turn. In the late afternoon, President Donald Trump threatened to hike tariffs on China, and then a total panic exploded in crypto. For a few terrifying minutes, prices looked like trapdoors into oblivion, wiping hundreds of billions of dollars off the sector’s market cap.

Flash crashes like these are obviously extremely uncomfortable for investors, but they’re clarifying because they expose weak financial plumbing, miscalibrated risk-taking habits, and shaky narratives. They also give long-term investors a checklist for what to do next. Here’s what you need to know, and what you need to do.

Image source: Getty Images.

What just happened

The catalyst for the flash crash had little to do with crypto itself, as the sector is largely unrelated to the flow of trade with China, which the newly threatened tariffs would affect. As the weekend unfolded, Trump and his advisors subsequently softened their tone, which helped markets to stabilize. But the damage was already done.

Prices fell shockingly fast. Bitcoin(BTC -3.26%) dropped by more than 12% from the prior week’s peak before rebounding somewhat. Ethereum(ETH -4.06%) slid by even more at the worst point.

Meme coins and altcoins were utterly shellacked. Dogecoin(DOGE -4.80%) briefly cratered by about 50% before stabilizing. Tokens outside the very largest cohort fell even harder. The crypto publication CoinDesk cited a 33% drop across the board for non-BTC, non-ETH assets, with many losing 80% or more, and a small handful losing close to 99.9% of their value in the same very short period.

The scale of this crash was historic. But why did it cascade so badly? Start with leverage.

The market was primed for a massive unwinding by a recent boom in the leveraged trading of perpetual futures in a handful of new decentralized exchanges (DEXes), and highly leveraged activity across the existing set of centralized exchanges (CEXes). Roughly $19 billion of forced liquidations of leveraged positions across DEX and CEX venues have been reported so far, which is the largest on record by a very large margin. The mechanism here was that the initial price shock caused by the tariff announcement caused a huge number of leveraged positions to blow up and get roughly simultaneously liquidated by the exchanges.

Then came problems with liquidity. Reports indicate that as exchanges were in the process of liquidating those leveraged positions, their own collateral used for borrowing was becoming worthless quite rapidly. This in turn caused some market makers to step back from providing their services to altcoins as volatility exploded amid the liquidations, leaving thin order books and allowing absurd air-pockets in pricing.

That’s likely why the downward price action became so intense so quickly. Without any liquidity available on tap for exchanges or market makers, and without any buyers at most of the prevailing prices, even a small amount of selling activity can create large price moves — and there was a lot of selling. There’s also some evidence that some of the crypto exchanges’ data oracles responsible for being authoritative sources of pricing information seized up or failed in the midst of this process. This heightened fear across both centralized and decentralized venues.

Separately, there is a significant amount of chatter alleging that an insider had advance knowledge of Trump’s new tariff policy announcement and took out a very large short position on Bitcoin in advance, pocketing around $200 million in the resulting crash. These allegations are not proven, though they rhyme with previous instances suspiciously perfectly timed trading in advance of tariff-related crypto market dumps.

However, it’s important to recognize that Bitcoin was actually the least affected asset during this event, and that its price activity was not really a major contributor to the cascade downward in and of itself.

What long-term investors should do next

The big lessons from the flash crash are simple, and they will age well.

First, do not use leverage to own crypto. Leverage turns both routine and exceptional volatility events into portfolio-destroying liquidations. Blue-chip cryptos like Solana, XRP, Chainlink, and Dogecoin can gap down hard in minutes when liquidity thins. Many traders (or short-term investors) using conservative amounts of leverage — less than 2X — were liquidated right alongside the gamblers levered to 100X.

Second, keep the bulk of your exposure restricted to crypto majors like Bitcoin, Ethereum, Solana, XRP, and Chainlink. Bitcoin held up well, and large chains reported a swift rebound as the tariff rhetoric cooled. The fact that they have a real investment thesis that exists independent of market phenomena helps significantly, too.

Finally, stick to the long game. The flash crash revealed what was fragile. What it did not change is the multi-year thesis for the majors, which depends on adoption, infrastructure, and policy clarity. If you build your allocations around that reality, you will be positioned to survive and benefit.

Alex Carchidi has positions in Bitcoin, Ethereum, and Solana. The Motley Fool has positions in and recommends Bitcoin, Chainlink, Ethereum, Solana, and XRP. The Motley Fool has a disclosure policy.

Investors should look beyond Nvidia and consider semiconductor stocks that combine strong AI fundamentals and reasonable valuation.

The artificial intelligence (AI) revolution is transforming every corner of the global economy. Nvidia, the company at the center of this revolution, continues to be a Wall Street favorite for all the right reasons. As an undisputed leader in accelerated computing, the company’s hardware and software power much of the world’s AI infrastructure buildout.

Shares of Nvidia have already surged over 43% so far in 2025. However, despite the massive demand for its Blackwell architecture systems, software stack, and networking solutions, the stock may grow quite modestly in future months. With its market capitalization now exceeding $4.6 trillion and shares trading at a premium valuation of nearly 30 times forward earnings, much of the optimism is already priced in.

Memory giantMicron(MU 6.12%), on the other hand, is still in the early stages of its AI-powered growth story. Shares of the company have surged nearly 128% in 2025, which highlights the increasing investor confidence in its high-bandwidth memory and data center portfolio. Yet, Micron could still offer investors higher returns in 2026, while riding the same AI wave. Here’s why.

Image source: Getty Images.

Lower customer concentration risk

Wall Street has been highlighting one significant underappreciated risk for Nvidia. Nvidia’s revenues depend heavily on a few hyperscaler customers, with two accounting for 39% and four accounting for 46% of its revenues in the second quarter of fiscal 2026 (ending July 27, 2026). Many of these hyperscaler clients are developing proprietary chips, which may offer a price-performance optimization in their specific workloads. This may reduce their dependence on Nvidia’s chips in future years.

Micron’s revenue base is significantly more diversified than Nvidia’s. The company’s largest customer accounted for 17% of total revenue, while the next largest contributed 10% in fiscal 2025 (ending Aug. 28, 2025). The company has earned over half of its total revenues from the top 10 customers for the past three years. The company has a reasonably broad customer base, including data center, mobile, PC, automotive, and industrial markets.

Hence, compared with Nvidia, Micron’s lower concentration risk makes it more resilient in the current economy.

HBM demand and AI memory leadership

Micron’s high-bandwidth memory (HBM) products, known for their superior data transfer speeds and energy efficiency, are being increasingly used in data centers. HBM revenues reached nearly $2 billion in the fourth quarter of fiscal 2025, translating into $8 billion annualized run rate.

Management expects Micron’s HBM market share to match its overall DRAM share by the third quarter of fiscal 2025. The company now caters to six HBM customers and has entered into pricing agreements covering most of the 2026 supply of HBM third-generation extended (HBM3E) products.

Micron has also started sampling HBM fourth-generation (HBM4) products to customers. The company expects the first production shipment of HBM4 in the second quarter of calendar year 2026 and a broader ramp later that year.

Beyond HBM, Micron’s Low-Power Double Data Rate (LPDDR) memory products are also seeing strong demand in data centers. The data center business has emerged as a key growth engine, accounting for 56% of Micron’s total sales in fiscal 2025.

Hence, Micron seems well-positioned to capture a significant share of the AI-powered memory demand in the coming years.

Valuation

Micron appears to offer a stronger risk-reward proposition than Nvidia, even in the backdrop of accelerated AI infrastructure spending. The company currently trades at 12.3 times forward earnings, significantly lower than Nvidia’s valuation. Hence, while Nvidia’s premium valuation already assumes near-perfect execution and continued dominance, Micron still trades like a cyclical memory stock. This disconnect leaves room for modest valuation expansion to account for Micron’s improving revenue mix toward high-margin AI memory products.

Wall Street sentiment is also increasingly positive for Micron. Morgan Stanley’s Joseph Moore recently upgraded the stock from equal-weight or neutral to overweight and raised the target price from $160 to $220. UBS has reiterated its “Buy” rating and increased the target price from $195 to $225. Itau Unibanco analyst has initiated coverage for Micron with a “Buy” rating and target price of $249.

Analysts expect Micron’s earnings per share to grow year over year by nearly 100% to $16.6 in fiscal 2026. If the current valuation multiple holds, Micron’s share price could be around $204 (up 6% from the last closing price as of Oct. 9), with limited downside potential. But if the multiple expands modestly in the range of 14 to 16 times forward earnings, shares could fall in the range of $232 to $265, offering upside of 20% to 37.8%.

On the other hand, there remains a higher probability of valuation compression for Nvidia, leaving less room for growth. With diversified customers, increasing AI exposure, and reasonable valuation, Micron may prove to be the better semiconductor pick in 2026.

The government shutdown has complicated things, but the COLA is still coming soon.

Every October, the Social Security Administration (SSA) announces the cost-of-living adjustment (COLA) for the upcoming year.

Up until recently, that announcement was supposed to be around Oct. 15 — right after the Bureau of Labor Statistics (BLS) releases September’s inflation report. But with the federal government closed until further notice, it seemed as if that report wouldn’t be released anytime soon.

New information from the BLS, however, suggests we could be getting the COLA announcement sooner than expected. Here’s when it might be coming, what it might be, and how that might affect your retirement.

Image source: The Motley Fool.

When will the new COLA be released?

The SSA calculates the COLA by averaging Consumer Price Index data from July, August, and September. That average is compared to the figure from the same period the year prior, and if it’s higher, the percentage difference will be next year’s COLA.

Before the government shut down, the BLS was expected to release September’s Consumer Price Index data on Oct. 15. But with that office almost entirely furloughed, it was unlikely the report would be published before the government reopened.

However, on Oct. 10, the BLS published an update noting that September’s inflation report would be released on Oct. 24. Generally, the SSA announces the new COLA almost immediately after the BLS inflation report is published.

What might next year’s adjustment be?

We won’t know the official 2026 COLA until the SSA makes the announcement later this month, but nonpartisan advocacy group The Senior Citizens League has estimated that it will land at 2.7%.

That figure is based on already available inflation data, as well as the projected data from September. If September’s numbers are significantly different from the estimates, the COLA may be higher or lower than predicted.

The average retired worker collects just over $2,000 per month in benefits, according to August 2025 data from the SSA. A 2.7% COLA, then, would amount to a raise of around $56 per month.

While any boost in benefits is helpful to a degree, for many retirees, next year’s COLA may be underwhelming. Inflation has stayed stubbornly high throughout the year, and tariffs have also taken a bite out of many retirees’ budgets.

Medicare Part B premiums are also expected to increase from $185 per month this year to a projected $206.50 per month in 2026, according to this year’s Medicare Trustees Report. Because Medicare premiums are typically deducted from Social Security checks, that $21.50 monthly increase will eat up a significant chunk of the COLA raise for the average retiree.

What does this mean for retirees?

It doesn’t hurt to keep an eye out for the COLA announcement to help budget for 2026, but for the most part, retirees may want to avoid relying too heavily on this adjustment to make ends meet.

Again, any extra cash can help pay the bills, especially with many older adults stretched thin financially right now. But with Social Security not going as far as it used to, it may be wise to start finding ways to reduce your dependence on your benefits.

According to a report from The Senior Citizens League, Social Security benefits lost around 20% of their buying power between 2010 and 2024. If you can swing it, finding a source of passive income or going back to work temporarily could have a bigger impact on your budget than any COLA.

This won’t be possible for everyone, but if you can beef up your savings even slightly, you won’t need to worry quite as much about future COLAs falling short. No matter where the 2026 adjustment lands, it’s wise to keep realistic expectations about how far that money will go.

Labour’s China spy trial explanation is total rubbish slams former security minister Tom Tugendhat

It didn’t bother explaining why — one minute the trial was on, the next it was dead meat.

Industrial secrets

It now transpires that the CPS took advice from British government officials.

It is entirely possible that the UK’s National Security Adviser, Jonathan Powell, a good mate of Keir, was one of the officials involved.

Shortly after their meeting with the CPS, the decision was taken to drop the case.

Why? They apparently told the CPS China couldn’t be called a “threat” to the UK.

Instead, it was just a “geo-political challenge”.

And so the charges against Cash and Berry wouldn’t stick.

In a previous spying case it was decided that charges were relevant only if it involved “a country which represents, at the time of the offence, a threat to the national security of the UK”.

Have you ever heard anything more ridiculous?

If China isn’t a threat to the UK, then who is?

The head of MI5, Sir Ken McCallum, has reported that the Chinese have tried to entice 20,000 Brits to act as spies for them, against our interests.

Did nobody think to ask Sir Ken if he thought China was a threat? I suspect I know the answer that would have been forthcoming

He also claimed that 10,000 UK businesses were at threat from the Chinese trying to nick industrial secrets.

In addition, he said that MI5 had 2,000 current investigations into Chinese spying activity — and that a new case was opened on the Chinese — behaving very deviously indeed — every 12 hours.

Did nobody think to ask Sir Ken if he thought China was a threat?

I suspect I know the answer that would have been forthcoming.

Of course the country is a threat.

It is menacing other nations down in South East Asia.

It has a whole bunch of nukes pointed directly at the West.

It arrests dissidents who want western-style freedoms.

And it does everything it can to undermine the UK’s politics and industry.

Truth be told, anybody who is working secretly for a foreign country in the UK is a threat to this country.

This seems to me so obvious that it should not need stating.

If their secret outside income involves a vast load of Yuan, some fortune cookies and cans of bubble tea, then we should investigate very seriously.

The truth in this particular case, though, is particularly damning.

It seems almost certain that Whitehall officials intervened at the behest of the Government.

And that they did this so as not to p**s off the Chinese — because aside from being a threat to the UK, which China certainly is, we are going cap in hand begging for investment from them.

Other nations don’t have a problem with employing a dual approach.

Make no mistake, we may need to do business with the likes of China, much as we did once with Russia — but they ARE the enemy

They understand that while they all need to do trade with horrible totalitarian countries such as China, they also need to count their spoons, if you get my meaning — and at the slightest sign of devious behaviour, call them out.

The Chinese understand this too.

Yes, being caught with a bunch of spies in our Parliament may be embarrassing for a short while.

But it won’t be allowed to get in the way of China making more money.

It seems that our government was too frit to risk it.

Too scared that the Chinese might react nastily and pull investment.

Or decide not to invest in the future. We mustn’t offend the Chinese.

Strategies like this simply do not work — and the Chinese, just like their big mates the Russians, will continue to spy on our institutions and do everything they can to harm our state.

Enemy is laughing

Make no mistake, we may need to do business with the likes of China, much as we did once with Russia — but they ARE the enemy.

And currently an enemy that is laughing its head off.

The government officials involved will be coming before the House of Commons Joint Committee on National Security Strategy.

If it is discovered that Jonathan Powell did warn off the CPS from pursuing the cases against Cash and Berry, then Powell should resign or be sacked.

Unless, of course, Powell was simply doing the bidding of the Prime Minister or the then Foreign Secretary, the intellectual colossus who is David Lammy.

If that’s the case then THEY should resign.

One way or another, we cannot allow Chinese spies to run amok in this country of ours just because we want to trouser some more wonga down the line, through Chinese investment.

This is a truly important week for Starmer.

The Chinese spygate scandal is the most serious he has faced since taking office last July.

It could yet be the finish of the man.

Which won’t make me lose a terrific amount of sleep, I have to tell you.

THE Man Who Never Sweats is probably feeling a bit moist under the armpits right now.

It has been discovered that Prince Andrew was still sending chummy texts to disgraced paedo Jeffrey Epstein long after the royal said he was.

Andrew is alleged to have messaged him to say: “We are in this together.”

This happened 12 weeks after the point at which Andrew claimed, in that BBC interview, to have cut off all contact with the odious slimeball.

It’s high time King Charles took action and kicked Andrew out of his Royal Lodge home in Windsor Great Park.

If you want to be among the top 10% of American households, you’ll need a seven-figure net worth.

Net worth is one of the most important financial numbers to know.

You should monitor your net worth because it changes over time, and it gives you a good idea of how close you are to being financially independent and shows whether you are making progress on your financial goals.

It can also be fun to see how your net worth stacks up to your peers. In particular, you may be curious about what net worth you would need to be among the top 10% of American households. The number is, unsurprisingly, pretty big.

Here’s the amount you would need, along with some details on calculating your net worth — and increasing it.

Image source: Getty Images.

How do you calculate your net worth?

Before diving into the net worth you need to be among the top 10%, it’s helpful to consider how to calculate net worth in the first place.

Net worth is essentially how much wealth you have to your name. To calculate your net worth:

Start by adding up the value of all your assets. Money in your bank account and savings account counts. So does money in your money market account. If you have CDs, these count as well. Same with investment dollars in a brokerage account. If you own real estate, a car, jewelry, personal items, or anything else of value, it counts toward your net worth.

Add up all your debt. You’ll also need to add up what you owe. Credit card debts, student loans, payday loans, a mortgage, and any other financial obligations you have will all become part of your debt calculation. You can check your credit report to confirm balances on all your debts if you aren’t sure of the amounts.

Subtract the amount of your debt from the value of your assets. If your assets are worth $500,000, for example, but you have $350,000 in debt, then you subtract $350,000 from $500,000 to discover that your net worth is $150,000.

If your net worth is negative, that’s pretty common if you’re young. Many people don’t own much, and they borrow for school, so they graduate with a lot of debt.

As you get older, though, your net worth should be growing as you build up money in brokerage accounts and retirement plans.

Are you in the top 10% of American households?

Now that you know how net worth is calculated, you may want to see where you stand.

The best information on this comes from the Federal Reserve’s Survey of Consumer Finances, which comes out once every three years. Unfortunately, the most recent data is from 2022. Still, we can take a look at that information to get an idea of what the top 10% of earners have in terms of wealth.

Based on this data from the Federal Reserve, the top 10% of American households had a net worth of at least $1,936,900, although the threshold varies by age. For example:

Among 18 to 29-year-olds, you’d need $281,550 or higher to be in the top 10%

Between 30 to 39, you’d need $711,400

Between 40 to 49, you’d need $1,313,700

Between 50 to 59, you’d need $2,629,060

Between 60 to 69, you’d need $3,007,400

At age 70 and over, you’d need $2,862,000

While these are high numbers, the amount is most likely even higher today due to the stellar performance of the stock market and the increase in real estate values in recent years.

While the Federal Reserve should have new data soon, these numbers show that it takes millions to be among the wealthiest Americans in terms of net worth.

Still, regardless of how you compare to your peers, what’s important is that you work on growing your own net worth by paying down debt, investing in your 401(k), IRA, and other accounts, and making smart financial choices that make you more financially secure over time.

In just a few days, the Social Security Administration (SSA) will be making a huge announcement about changes to the program in 2026. A new earnings-test limit will be shared, as well as the maximum monthly benefit.

Perhaps the most anticipated update the SSA will share, however, is an official cost-of-living adjustment, or COLA, for 2026.

Image source: Getty Images.

Each year, Social Security benefits are eligible for a raise, based on inflation. Without COLAs, beneficiaries would be pretty much guaranteed to lose buying power over time.

Initial projections are calling for a 2.7% COLA for 2026, but that number doesn’t take inflation data from September into account. If inflation rose substantially last month, seniors could be looking at an even larger boost to their Social Security checks in 2026.

While a 2.7% or higher COLA might seem like something to celebrate, you may want to temper your excitement if you count on Social Security for income. That’s because that COLA may not be yours to keep in full.

Will a Medicare increase eat into your COLA?

Seniors who are enrolled in Medicare and Social Security at the same time pay their premiums for Part B, which covers outpatient care, directly out of their monthly benefits. This means that if the cost of Medicare increases in 2026, it will eat into whatever COLA retirees receive.

In 2025, the standard monthly Part B premium rose from $174.70 to $185. But based on projections from the Medicare Trustees released earlier this year, the standard Part B premium for 2026 could be a whopping $206.50 — an increase of $21.50. It also could cause many seniors to lose out on a good chunk of their Social Security raises.

As of August, the average monthly Social Security benefit for retired workers was about $2,008. A 2.7% COLA would result in a boost of about $54 per month. However, if Medicare Part B goes up by $21.50 per month, the typical Social Security benefit might only rise by around $32.50, in practice.

It’s best to have income outside of Social Security

Until the SSA makes an official COLA announcement on Oct. 15, we won’t know for sure what next year’s COLA will amount to. However, even if it’s fairly generous, a large uptick in Part B costs could wipe out much of it.

That’s why it’s important not to be too reliant on Social Security COLAs to keep up with inflation. A better bet? Save well for retirement, and set yourself up with a portfolio of assets that continues to generate income for you.

Those assets could include a mix of stocks and bonds. The stocks should ideally provide growth and income in the form of dividend payments. The bond portion, meanwhile, may be more stable, providing you with steady income you can use to supplement your monthly Social Security checks.

There are other options for generating retirement income, too, like working part-time. And that part-time work doesn’t have to come in the form of a boring job with a strict, preset schedule.

Thanks to the gig economy, you can explore different options for earning some money. You may find that, on top of the extra income being helpful, it’s nice to have a reason to get out of the house on a regular basis and socialize with other people.

No matter what strategy you choose, the key is to have some income outside of Social Security — because while the program’s COLAs do help seniors keep up with inflation to some degree, they also have their fair share of shortcomings.

A LUCKY viewer of a brand new ITV game show has walked away with an eye-watering £1million.

Sienna McSwiggan, 20, secured the top prize last night on Win Win with People’s Postcode Lottery on Saturday night.

3

Sienna McSwiggan, 20, broke down in tears after winning the huge jackpot

3

After trading in a trip to the Maldives, she took home £1millionCredit: ITV

The hotel manager from The Black Country took home the £1million cash prize, as well as two cars, two luxuryholidays, a trip to Australia to see The Ashes and Take That tickets.

After answering the winning question correctly, Sienna questioned if it was real and said the money would be life-changing for herself and family.

She said: “I don’t even know what to say. I am in shock.

“I’ve literally got a penny in my account.

“I’m over the moon. It feel like a dream and someone’s gonna wake me up any minute.”

Hosted by Mel Giedroyc and Sue Perkins, the quiz show sees contestants battling it out in the studio.

At home viewers can also get involved and play for prizes.

However, the show’s format also allows these viewers to become contestants in the studio.

Once they have bagged a prize, players have to face the ultimate decision.

They must choose between keeping their original prize or risk it all and trade it in to join Millionaire’s row.

Watch as one young woman shares how her family won the lottery

Sienna took the gamble and traded a trip to the Maldives for a chance to win big.

The risk saw her take home one of the UK’s biggest telly prizes.

Last month, The Sun reported that another contestant took home a huge £20,000 jackpot.

After answering the final question correctly, Shayanne took home the winning prize.

Previously discussing the format, Mel Giedroyc said: “This quiz is so extra!

“Imagine winning something like a car just by playing along with a gameshow you’re watching on a Saturday night in your pyjamas?

“I can’t wait!”

Sue Perkins added: “If I wasn’t hosting this, I’d be playing it at home; sat in my leopard print onesie, cuddling the dog whilst trying to figure out The Nation’s favourite chocolate bar. Bring it on!”

Speaking to The Mirror ahead of yesterday’s finale, Sue added: “Saturday’s show really is going to be a night like no other.

“The thrilling thing, of course, is that all of this is going to be won by one person, and that person might even be a viewer turned contestant, who simply signed up, joined in from their sofa and got the surprise of their life.”

Hardest Quiz Show Questions

Would you know the answers to some of quizzing TV’s hardest questions

Who Wants To Be A Millionaire – Earlier this year, fans were left outraged after what they described as the “worst” question in the show’s history. Host Jeremy Clarkson asked: “From the 2000 awards ceremony onwards, the Best Actress Oscar has never been won by a woman whose surname begins with which one of these letters?” The multiple choice answers were between G, K, M and W. In the end, and with the £32,000 safe, player Glen had to make a guess and went for G. It turned out to be correct as Nicole Kidman, Frances McDormand and Kate Winslet are among the stars who have won the Best Actress gong since 2000.

The 1% Club – Viewers of Lee Mack’s popular ITV show were left dumbfounded by a question that also left the players perplexed. The query went as follows: “Edna’s birthday is on the 6th of April and Jen’s birthday falls on the 15th of October, therefore Amir’s birthday must be the ‘X’ of January.” It turns out the conundrum links the numbers with its position in the sentence, so 6th is the sixth word and 15th is the fifteenth word. Therefore, Amir’s birthday is January 24th, corresponding to the 24th word in the sentence.

The Chase – The ITV daytime favourite left fans scratching their heads when it threw up one of the most bizarre questions to ever grace the programme. One of the questions asked the player: “Someone with a nightshade intolerance should avoid eating what?” The options were – sweetcorn, potatoes, carrots – with Steve selecting sweetcorn but the correct answer was potatoes.

3

Last night, a contestant took home a £1million cash prizeCredit: Shutterstock Editorial

IT is set to be one of the most momentous occasions in soap history.

For the first time ever, ITV‘s landmark shows will be combining for an epic hour of soap drama that is being teased as changing the course of both programmes forever.

6

A soap crossover is coming with multiple deaths expected to hitCredit: Not known, clear with picture desk

6

This is who I think should be killed off in CorriedaleCredit: ITV

This January, Coronation Street and Emmerdale will join forces for the aptly titled Corriedale to herald the stars of the new ‘soap power hour’.

It’s a clever, bold and HUGE move by ITV with both programmes having faced mass cast axings, job cuts, dwindling ratings and general backlash from fans over the past few years.

It is hoped by executives that the special show will help to revitalise both shows and kickstart a new era for the programmes – as well as being a clever way to conceal the fact they’ve both lost 30 minutes of screen-time a week.

From next year, both shows will air for just 30 minutes per night – the equivalent of five episodes per week unlike the current six.

But with the epic stunt set to take place, which is currently being filmed on long night shoots and being kept tightly under wraps, there promises to be the deaths of fan-favourite characters from both programmes.

Being such a historic moment in TV means that it should come with an utterly unforgettable death that will go down in the soap historybooks.

With only one chance to get it right, here is who I think ITV should kill off now.

Eric Pollard

6

Time is up for Eric in the DalesCredit: ITV

Yes, you read that right.

Emmerdale bosses need to make an impact and as such, they should volunteer their longest-serving character ever as a sacrifice.

Not only would killing Eric off be the biggest unexpected twist that would have people gasping up and down the country, it would lay the foundations for the village to truly be changed forever.

Having been portrayed by Chris Chittell since 1986, he has become part of the foundation in the Dales.

But as an avid viewer, it hasn’t gone unnoticed that he has fallen into a rather bumbling repeated pattern of storyline in recent years.

Fans often see Eric disappear from screens for a number of weeks before popping back up to have a new brief crisis.

It quickly results in him snapping at anyone in sight and becoming public enemy number one with his grumpy old man act.

But just as quickly as the crisis arises, he soon realises the error of his ways and makes peace with his family and friends in true story-telling fashion.

Frankly, we’ve seen it multiple times and we really don’t need to see it again.

If bosses aren’t planning on placing Eric in a new mass murder plot or turn him into the Dales’ next gangster, I fear his potential plots have naturally come to an end.

Be brave Emmerdale and let go of your longest player if you truly want a memorable moment.

April Windsor

6

Axing April Windsor might be the best decision all roundCredit: ITV

The other character I think Dales bosses should be offering up to meet their maker in the crossover could not be more opposite to Eric.

If they don’t make their big death the village OAP then yes, a wayward teen schoolgirl is the next best way to go.

Played by Amelia Flanagan, April has been one of Emmerdale’s biggest success stories in terms of transition from very young child performer to a teen actress who is able to hold her own when it comes to lengthy and gritty storylines.

However, her transition from wise-beyond-her-years 10-year-old to a reckless and easily-influenced 15-year-old has never sat right.

Over the past 12 months, goody-two-shoes April has become soap’s most troubled teen ever out of nowhere.

She went missing for months, became homeless, began underage drinking, went through a heartbreaking teen stillbirth whilst living on the streets and has now found herself a drug mule in a shocking county lines storyline.

I can’t help but think this unexpected character development could be for one bigger reason.

Having faced many brushes with death over her chaotic year, the soap stunt could be the perfect time to portray a real story of a teen tragedy.

Seeing a teenager killed off would have the shock factor to last years if done correctly.

April meeting a tragic end also allows for the soap to delve into family heartache and tragedy following her potential passing.

MY EMMERDALE VERDICT: Emmerdale needs to go to the extremes and for me, it’s either the show’s oldest character or on the flip-side, one of their youngest.

Sean Tully

6

Sean Tully has certainly overstayed his welcomeCredit: ITV

When it comes to who Corrie could offer up for their soap death, the first person that comes to mind (and, let’s be honest, most fans’) would be Sean Tully.

How Sean has scraped through 22 years on the Street boggles the mind.

As both a TV journalist and viewer of the programme, I am yet to encounter anyone, either personally or professionally, who would make a campaign to save Antony Cotton’s character from getting the axe.

Of course, Sean does have many ties to the faces of Weatherfield and would likely see some moving performances from them in the aftermath of his passing.

But with the character having truly lacked a notable storyline for close to 10 years, his spot on the soap is purely taking away space from another character who could help provide a much-needed boost to the already fledgling soap.

And let’s be real, Corrie needs to be saving all the money it can amid the ongoing cash crisis.

Whilst killing Sean off would realistically go rather unnoticed in the long-run of the soap, marking the end of such a universally disliked character will have soap fans rejoicing in their droves and for that alone, Coronation Street will have achieved a milestone.

Dee-Dee Bailey

6

Fans are set to lose the budding Street icon so let’s give her a proper send-offCredit: ITV

It is safe to say, amid a crowd of unnecessary and irritating new characters since the pandemic, Dee-Dee has been a true breathe of fresh air.

She exudes classic Corrie and Channique is a formidable actress.

But with her choosing to walk away after just four years, I worry that she’s about to fall into a bad trap.

We have seen it time and time again with incredible actresses leaving soap after just a few short years at the promise of breaking out into even bigger roles.

But despite their talent, they fade into the abyss and the characters are too forgettable to encourage bosses to ever bring them back.

Case and point Amy James Kelly, who played Maddie Heath on Corrie between 2013 and 2015.

She rocked Weatherfield to its core but with Amy quickly being predicted for bigger and better things on Corrie, she quit before she became too tied down to the role.

But her star power soon faded and she failed to be the big star everyone had hoped and Maddie became forgotten about much quicker than expected.

I’d hate this to happen to Channique but I fear it may be written in the stars.

But if bosses decide to place Dee-Dee at the forefront of their most anticipated episode since 2010’s Tram Crash (which did wonders for the legacy of Molly Dobbs played by the iconic Vicky Binns) then they will cement her in the history books for YEARS to come.

Whilst I don’t want to see Dee-Dee die, it could be her only hope of remaining a Corrie icon.

MY CORONATION STREET VERDICT: When it comes to the Corrie death, bosses either need to take one for the team and free audiences from an abysmal character or preserve the legacies of who could have been a Street Queen.

Destiny Wealth Partners reported in an SEC filing on Monday that it sold 59,354 shares of the iShares Biotechnology ETF (IBB) in the third quarter—an estimated $8.1 million transaction based on average pricing for the quarter.

What happened

According to a filing with the Securities and Exchange Commission on Monday, Destiny Wealth Partners reduced its holding in the iShares Biotechnology ETF (IBB) by 59,354 shares during the quarter. The estimated value of the shares sold was $8.1 million. The fund now holds 16,430 IBB shares valued at $2.4 million as of September 30.

What else to know

This sale left IBB representing 0.3% of Destiny Wealth Partners’ 13F reportable assets.

Top holdings after the filing:

JAAA: $46.41 million (5.7% of AUM)

VUG: $40.11 million (4.9% of AUM)

DFLV: $32.03 million (3.9% of AUM)

JCPB: $28.13 million (3.45% of AUM)

AMZN: $27.70 million (3.4% of AUM)

As of Tuesday afternoon, IBB shares were priced at $149.73. The fund is up about 5% over the year.

Company overview

Metric

Value

AUM

$6.2B

Dividend yield

0.18%

Price as of Tuesday afternoon

$149.73

1-year total return (as of Sept. 30)

–0.65%

Company snapshot

IBB seeks to track the investment results of a biotechnology-focused equity index, investing at least 80% of assets in component securities and economically similar investments.

It operates as a non-diversified ETF, with periodic rebalancing to maintain index alignment.

The iShares Biotechnology ETF (IBB) offers investors access to the U.S. biotechnology sector through a passively managed fund. With over $6 billion in market capitalization, the ETF provides exposure to biotechnology companies.

Foolish take

Destiny Wealth Partners’ decision to unload roughly $8.1 million in iShares Biotechnology ETF (IBB) shares adds to a broader theme in markets this year: Institutional investors have been cooling on biotech. The sector has struggled to regain its pandemic-era momentum as investors favor AI, energy, and industrial plays. IBB is up about 5% over the past year, trailing the S&P 500’s 18% gain.

IBB’s two largest holdings—Vertex Pharmaceuticals and Amgen—have each slumped, down about 8% and 7%, respectively, over the past year. That drag has offset strength from smaller, high-growth biotech names focused on oncology and gene therapy. Meanwhile, the fund’s expense ratio of 0.44% sits slightly above broad-market ETF averages, reflecting the niche exposure investors are paying for.

For long-term investors, IBB still offers diversified exposure to the innovation pipeline driving future drug breakthroughs—but near-term returns will depend on FDA approvals, pricing clarity, and investor appetite for higher-risk growth sectors.

Glossary

ETF (Exchange-Traded Fund): An investment fund traded on stock exchanges, holding a basket of assets like stocks or bonds.

Biotechnology ETF: An ETF focused on companies in the biotechnology industry, such as drug development and medical research.

AUM (Assets Under Management): The total market value of assets that an investment manager or fund controls on behalf of clients.

13F reportable AUM: The portion of a fund’s assets that must be disclosed in quarterly SEC Form 13F filings, typically U.S. equity holdings.

Non-diversified ETF: A fund that invests in fewer securities or sectors, increasing exposure to specific industries or companies.

Index-based selection: An investment strategy where holdings are chosen to match a specific market index, rather than by active management.

Component securities: The individual stocks or assets that make up an index or ETF portfolio.

Dividend yield: The annual dividend income expressed as a percentage of the investment’s current price.

Total return: The investment’s price change plus all dividends and distributions, assuming those payouts are reinvested.

Rebalancing: Adjusting a fund’s holdings periodically to maintain alignment with its target index or asset allocation.

Knowing what to look for allows you to avoid joining a pyramid scheme.

Pyramid schemes are nothing new. For example, in the 1920s, Charles Ponzi promised investors high returns on postal reply coupons, using the money from new investors to pay returns to earlier investors. Like all pyramid schemes, Ponzi’s collapsed in a heap.

Because scam artists will do anything they can to separate their victims from their savings, it’s vital that seniors understand that they’re prime targets. More importantly, seniors must know how to spot and avoid pyramid schemes.

Image source: Getty Images.

Prime targets

If you’ve spent years strategizing how you’ll retire, scammers consider you a prime target. While they might not be able to con a 21-year-old out of much, they suspect you have plenty of money put away. It may be someone you meet in the park, bowling, or even at church. The scammer may be someone you’ve never heard of, someone who contacts you out of the blue, or someone who’s introduced to you by a friend.

The point is that pyramid schemes and the scammers who operate them see you as a rich source of cash.

Packaged to look like something else

Trying to sell you on a pyramid scheme involves making you believe you’re getting involved in a legitimate pursuit, like a business venture. One only needs to look at Charles Ponzi’s 1920s scam to understand how pyramid schemes work.

Ponzi, once known as a financial wizard, convinced well-meaning investors that he’d found a way to make huge profits by buying international postal reply coupons in countries with weakened currencies and selling them at a higher price in the U.S. Ponzi said he was so confident that he promised a 50% return in 90 days.

This was the “Roaring Twenties,” a decade of economic prosperity in the U.S., and many wanted in on the action. The problem with Ponzi’s plan was this: The only people who experienced a payday were those who got in early. The money from those who bought into Ponzi’s scheme later was used to pay the people on board early.

It’s the same with today’s pyramid schemes. No matter what’s promised, only a few will profit and the scheme will eventually collapse, leaving most participants holding the bag. As simple as a pyramid scheme seems, it can suck anyone in, from a new investor to someone who’s been investing for decades.

Red flags

If someone invites you to invest in a new business or one-of-a-kind product, or become part of a multi-level marketing (MLM) enterprise, here’s how you can determine if it’s actually a pyramid scheme:

More money paid for recruiting others than for product sales. If the program requires you to recruit others to join for a fee, it’s likely a pyramid scheme.

No genuine products or services sold. According to Investor.gov, fraudsters claim you’ll sell “products,” like online advertising, websites, tech services, or mass-licensed e-books. They’re creating “businesses” that are hard to value to hide the fact that they’re pyramids.

Promise of high returns. A scammer will promise you fast cash to get their hands on your Social Security, pension, annuity, and other assets. If you see a return, it’s typically paid out of money from new recruits rather than actual sales.

Promise of passive income. If you’re offered payment in exchange for doing very little, like placing online advertisements on obscure websites or recruiting others, it’s probably a pyramid scheme.

There is little or no revenue from retail sales. If you look at documents, such as financial statements audited by a certified public accountant (CPA), and those documents show income primarily from recruiting new members, it’s a serious red flag.

Complex commission structure. Legitimate companies pay commission based on products or services you sell to people outside the program. Be careful if the commission structure is too complex to be easily understood.

Protect yourself

Fortunately, once you know the signs, you’re in an excellent position to protect your interests. Here’s how:

Be skeptical. If an investment or work-from-home offer sounds too good to be true, it probably is.

Ensure sales generate income. Verify that you’ll earn money from legitimate retail sales, not just recruitment fees.

Investigate the company. Go online to read about others’ experiences.

Finally, check with the Better Business Bureau (BBB) and your state’s Attorney General to learn if the company is legitimate and whether there have been complaints. Don’t allow anyone to steal the retirement you’ve planned for so long.