The Corporation for Public Broadcasting (CPB), a nonprofit that distributes federal funds to public radio and television stations in the United States, has announced it would be shutting down as the result of funding cuts under President Donald Trump.

On Friday, the group issued a statement saying it had launched an “orderly wind-down of its operations” in response to recent legislation that would cut nearly $1.1bn of its funding.

“Despite the extraordinary efforts of millions of Americans who called, wrote, and petitioned Congress to preserve federal funding for CPB, we now face the difficult reality of closing our operations,” its president, Patricia Harrison, wrote.

According to the statement, the Corporation for Public Broadcasting would remain in operation for the next six months, albeit with a reduced staff.

The majority of its employees will be let go on September 30. Then, a “small transition team” will remain through January 2026 to “ensure a responsible and orderly closeout”.

The death knell for the nonprofit came last month in the form of two legislative actions.

The first was the passage of the Rescission Act of 2025, which was designed to revoke funding that Congress approved in the past. The Rescission Act targeted federal programmes that Trump sought to put on the chopping block, including foreign aid and federal funding for public broadcasters.

The Senate voted to pass the act by a margin of 51 to 48, and the House then approved it by a vote of 216 to 213.

The second legislative wallop came on July 31, as the Senate Appropriations Committee unveiled its 2026 funding bill for labour, health and human services, education and related agencies.

That bill earmarked $197bn in discretionary funding, but none of it went to the Corporation for Public Broadcasting.

Never in five decades had the corporation been excluded from the appropriations bill, according to the nonprofit.

Both houses of Congress are controlled by Republicans, and party members have largely fallen in line with Trump’s legislative priorities.

Defunding public media has long been a priority of Republicans, stretching back to President Richard Nixon’s feud in the 1970s with public broadcasting personalities like Sander Vanocur.

Nixon, like Trump, had an adversarial relationship with the media, and in 1972, he vetoed a public broadcasting funding bill, forcing Congress to return with a slimmed-down version of its funding. That move helped establish a trend of Republicans seeking to whittle down federal support for public, non-commercial TV and radio.

Trump, during his second term, has made it a priority to slash at what he considers government “bloat”, and that includes reducing federal spending.

He and his allies have accused news outlets like National Public Radio (NPR) and the Public Broadcasting Service (PBS) of being left-wing soapboxes.

The Corporation for Public Broadcasting distributes its funds to NPR and PBS member stations. NPR boasts a weekly audience of 43 million. PBS, meanwhile, reaches 130 million people each year through its television offerings alone, not counting its online presence.

Still, in the lead-up to the passage of the Rescissions Act, Trump threatened to yank his support from any Republican who opposed his efforts to defund the corporation.

Trump also said public broadcasting was worse than its commercial counterparts, including MSNBC, which he frequently misspells as “MSDNC” to imply alleged bias towards the Democratic National Committee (DNC).

“It is very important that all Republicans adhere to my Recissions Bill and, in particular, DEFUND THE CORPORATION FOR PUBLIC BROADCASTING (PBS and NPR), which is worse than CNN & MSDNC put together,” Trump wrote on social media on July 10.

“Any Republican that votes to allow this monstrosity to continue broadcasting will not have my support or Endorsement. Thank you for your attention to this matter!”

But Harrison, the president of the Corporation for Public Broadcasting, framed the organisation’s closure as a loss for education and civic engagement.

“Public media has been one of the most trusted institutions in American life, providing educational opportunity, emergency alerts, civil discourse, and cultural connection to every corner of the country,” Harrison said.

“We are deeply grateful to our partners across the system for their resilience, leadership, and unwavering dedication to serving the American people.”

US President Trump alleged that the data had been manipulated to make him look bad.

United States President Donald Trump has removed the head of the agency that produces the monthly jobs figures after a report showed hiring slowed in July and was much weaker in May and June than previously reported.

Trump, in a post on his social media platform on Friday, alleged that the figures were manipulated for political reasons and said that Erika McEntarfer, the director of the Bureau of Labor Statistics (BLS), who was appointed by former President Joe Biden, should be fired. He provided no evidence for the charge.

“I have directed my Team to fire this Biden Political Appointee, IMMEDIATELY,” Trump said on Truth Social. “She will be replaced with someone much more competent and qualified.”

Trump later posted: “In my opinion, today’s Jobs Numbers were RIGGED in order to make the Republicans, and ME, look bad.”

After his initial post, Labor Secretary Lori Chavez-DeRemer said on X that McEntarfer was no longer leading the bureau and that William Wiatrowski, the deputy commissioner, would serve as the acting director.

“I support the President’s decision to replace Biden’s Commissioner and ensure the American People can trust the important and influential data coming from BLS,” Chavez-DeRemer said.

Friday’s jobs report showed that just 73,000 jobs were added last month and that 258,000 fewer jobs were created in May and June than previously estimated. The report suggested that the economy has sharply weakened during Trump’s tenure, a pattern consistent with a slowdown in economic growth during the first half of the year and an increase in inflation during June that appeared to reflect the price pressures created by the president’s tariffs.

“What does a bad leader do when they get bad news? Shoot the messenger,” Democratic Senate Leader Chuck Schumer of New York said in a Friday speech.

Revisions to hiring data

Trump has sought to attack institutions that rely on objective data for assessing the economy, including the Federal Reserve and, now, the BLS. The actions are part of a broader mission to bring the totality of the executive branch – including independent agencies designed to objectively measure the nation’s wellbeing – under the White House’s control.

McEntarfer was nominated by Biden in 2023 and became the commissioner of the BLS in January 2024. Commissioners typically serve four-year terms, but since they are political appointees, they can be fired. The commissioner is the only political appointee of the agency, which has hundreds of career civil servants.

The Senate confirmed McEntarfer to her post 86-8, with now Vice President JD Vance among the yea votes.

Trump focused much of his ire on the revisions the agency made to previous hiring data. Job gains in May were revised down to just 19,000 from 125,000, and for June they were cut to 14,000 from 147,000. In July, only 73,000 positions were added. The unemployment rate ticked up to a still-low 4.2 percent from 4.1 percent.

“No one can be that wrong? We need accurate Jobs Numbers,” Trump wrote. “She will be replaced with someone much more competent and qualified. Important numbers like this must be fair and accurate, they can’t be manipulated for political purposes.”

The monthly employment report is one of the most closely-watched pieces of government economic data and can cause sharp swings in financial markets. The disappointing figure sent US market indexes about 1.5 percent lower on Friday.

While the jobs numbers are often the subject of political spin, economists and Wall Street investors – with millions of dollars at stake – have always accepted US government economic data as free from political manipulation.

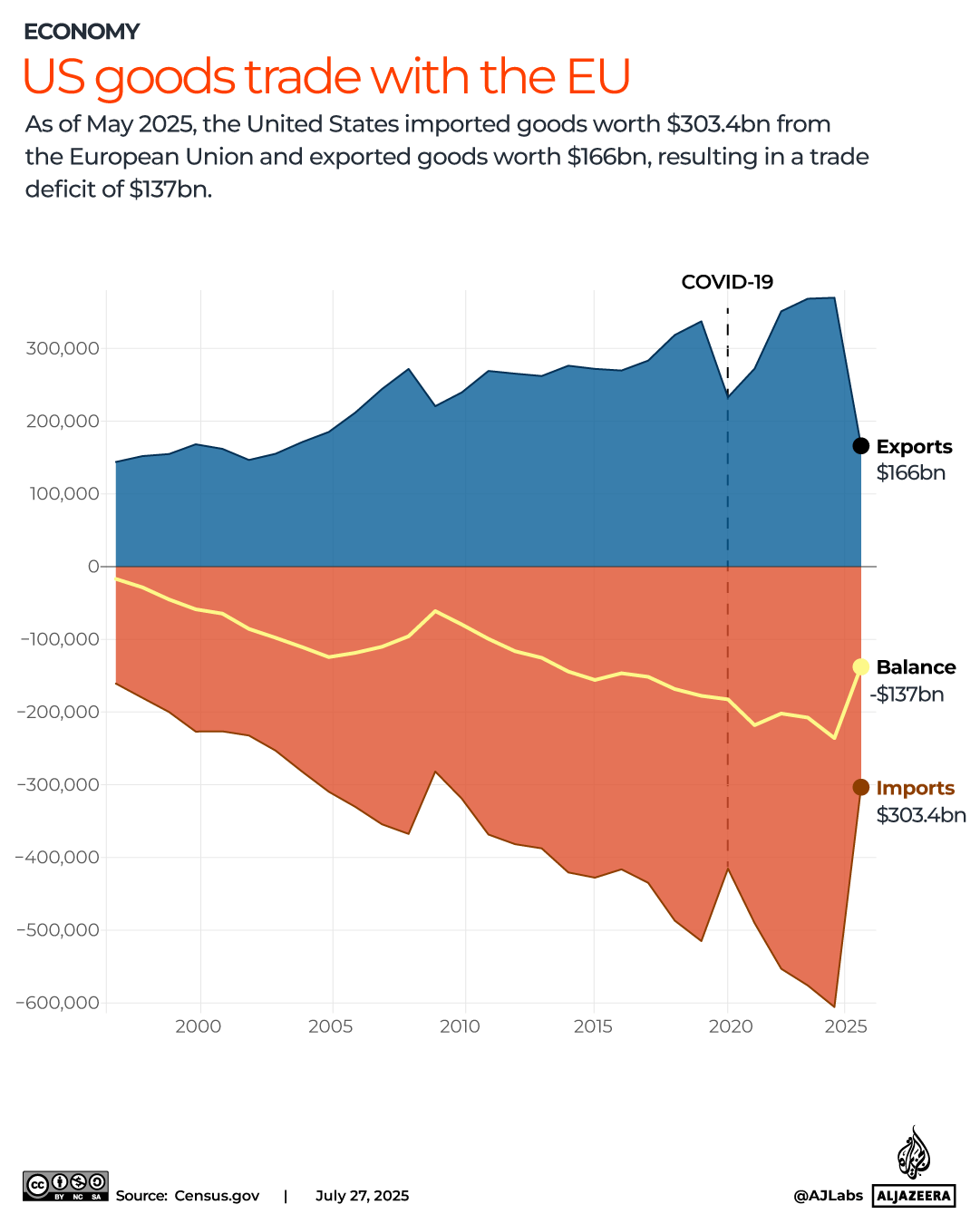

Switzerland says it will try to negotiate its way out of stiff United States tariffs, hours after US President Donald Trump’s administration shocked the European country by announcing plans to impose a 39-percent tariff rate on Swiss goods.

The Swiss government said on Friday that it was “disappointed” and would decide how to proceed after Trump unveiled the 39-percent rate, more than double the 15 percent being applied for most European Union imports into the US.

The new tariffs, which are set to go into effect on August 7, would prove painful for several key Swiss industries, including manufacturing and watchmaking.

The Swiss government said in a statement on social media that it remains in contact with US authorities and “still hopes to find a negotiated solution”.

“The Federal Council notes with great regret the intention of the US to unilaterally burden Swiss imports with considerable import duties despite the progress made in bilateral talks and Switzerland’s very constructive position,” it added.

The Trump administration unveiled a range of new tariffs on many US trading partners on Thursday, saying the move aimed to address a “continued lack of reciprocity in our bilateral trade relationships”.

Nearly 70 countries now face import duties that were due to come into force on Friday. But most will now begin on August 7, giving countries a few days to try to reach an agreement with Washington to stave off or reduce their respective tariff rate.

“Everyone had been focused on August 1 … and now there is a new deadline,” Al Jazeera’s Kimberly Halkett reported from the White House on Friday morning.

“The reason is so that there can be a little bit more time and breathing space to get some more deals done. There were a few that were very close but didn’t quite make the deadline, and so the White House [said] this will allow … for these final agreements to be worked out.”

Trump negotiated trade frameworks over the past few weeks with the EU, Japan, South Korea, Indonesia and the Philippines — allowing the US president to claim victories as other nations sought to limit his threat of charging even higher tariff rates.

He said on Thursday there were agreements with other countries, but he declined to name them.

Asked on Friday if countries were happy with the rates set by Trump, US Trade Representative Jamieson Greer said, “A lot of them are.”

The new tariffs also include a 35-percent duty on many goods from Canada, 50 percent for Brazil, and 20 percent for Taiwan. Taiwan said its rate was “temporary” and it expected to reach a lower figure.

The Trump administration said it decided to impose 39-percent tariffs on Switzerland because of what it called the European country’s refusal to make “meaningful concessions” by dropping trade barriers.

“Switzerland, being one of the wealthiest, highest-income countries on Earth, cannot expect the United States to tolerate a one-sided trade relationship,” a White House official said on Friday.

Swissmem, a group representing the mechanical and electrical engineering industries, said it was “really stunned” by the US move. “It’s a massive shock for the export industry and for the whole country,” said Deputy Director Jean-Philippe Kohl.

“The tariffs are not based on any rational basis and are totally arbitrary … This tariff will hit Swiss industry very hard, especially as our competitors in the European Union, Britain and Japan have much lower tariffs.”

Stock market tumbles

But Trump’s new tariffs have created yet more uncertainty, with many details unclear.

Global stock markets stumbled on Friday, with Europe’s STOXX 600 down 1.8 percent on the day and 2.5 percent on the week, on track for its biggest weekly drop since Trump announced his first major wave of tariffs on April 2.

Wall Street also opened sharply lower on Friday.

Reporting from the New York Stock Exchange, Al Jazeera’s Kristen Saloomey explained that US markets were “definitely down” following the tariffs announcement, but the drop was not as bad as what was seen after the first round of tariffs in April.

“When the first round of tariffs were enacted, the market did drop substantially, but then clawed back a lot of the losses about a month later as deals were worked out. A lot of economists are saying that this time around, the market has priced in tariffs,” Saloomey said.

Still, she said, “the concern is still that the underlying fundamentals of the economy are under strain and the full weight of the tariffs” has yet to be seen.

President Donald Trump has unveiled new reciprocal tariffs on imports from dozens of countries, ranging from 10 percent to 41 percent, forging ahead with his efforts to reshape international trade.

On Thursday, the White House issued a statement entitled “Further Modifying the Reciprocal Tariff Rates”, in which some 69 trading partners and their respective “adjusted” tariff rates were listed.

These are changes to import levies since the tariffs announced on April 2 (and later paused until August 1), the day Donald Trump referred to as “Liberation Day”. Rates have dropped for most countries, but not all. Most of the new tariffs will go into effect on August 7.

Imports from roughly 40 countries will face a new 15 percent rate on goods they export to the United States, while other nations’ products will be hit with higher duties. The United Kingdom and Australia will pay 10 percent.

One notable exception from Trump’s latest tariff list is China, the US’s third-largest trading partner. So, what’s the current state of play between the two countries?

How are US-China trade talks going?

Top officials from the US and China failed to agree on extending a 90-day pause on tariffs on Tuesday during the latest round of talks held in Stockholm, Sweden.

Any renewal of the pause, which is due to expire on August 12, will ultimately be up to Trump, US Treasury Secretary Scott Bessent said.

The talks, which took place in Rosenbad, the seat of government where the Swedish prime minister’s office is located, were aimed at defusing a new trade spat between the world’s two biggest economies.

The latest meeting, which was attended by Bessent and Vice Premier He Lifeng for Beijing, concluded just two days after Trump announced a new trade deal with the European Union.

It was the third meeting between the US and China since April, at which point the two sides had slapped each other with tariffs exceeding 100 percent in an escalating trade war.

On May 12, the two agreed a 90-day tariff pause in Geneva, easing a costly logjam which had upended trade. During the pause, US tariffs have been reduced from 145 percent to 30 percent, and Chinese duties from 125 percent to 10 percent.

But without a new trading agreement in place, global supply chains could face renewed turmoil if US and Chinese tariffs restart at triple-digit levels that would amount to a bilateral trade embargo.

What happened at the Stockholm meeting?

After the meeting, China’s deputy commerce minister, Li Chenggang, said both sides were “fully aware of the importance of safeguarding a stable and sound China-US trade and economic relationship”.

He told Chinese media that the two sides had held “candid and constructive exchanges”.

For his part, Bessent told reporters at a briefing on Tuesday that the US had built momentum with recent US agreements with Japan and the EU. He remained sanguine about China.

“Just to tamp down that rhetoric, the meetings were very constructive. We just haven’t given the sign off,” he said.

Bessent stressed that “nothing is agreed until we speak with President Trump”.

The treasury secretary and US Trade Representative Jamieson Greer were due to brief Trump on Wednesday about the Stockholm discussions, he added.

Bessent also said that, given US secondary tariff legislation on sanctioned Russian oil, China could face high tariffs if Beijing continued with its Russian oil purchases.

Technology exports, specifically chips used for artificial intelligence, are understood to have been at the centre of this week’s talks. In particular, US security officials have raised concerns that high-tech American semiconductor chips could be used by China’s military.

In April, Trump was poised to block the export of Nvidia’s H20 chip, which has been designed to comply with Biden-era export curbs. But Trump reversed course following direct appeals from Nvidia Chief Executive Officer Jensen Huang.

In the run-up to this week’s talks, the UK’s Financial Times newspaper reported that Washington had frozen restrictions on technology sales to China to ease negotiations and to avoid retaliation from Beijing in the form of export restrictions on rare earth minerals, as happened in May.

Rare earths are a group of 17 elements essential to numerous manufacturing industries, from auto parts to clean energy technology to military hardware. They are also a central issue for trade talks.

China has long dominated the mining and processing of rare earth minerals, as well as the production of related components, like rare earth magnets.

What was the state of US-China trade before the recent truce?

For years, Trump has criticised Beijing for what he deems to be unfair trade practices – namely, import quotas, government subsidies and tax breaks. He has even argued that the US’s trade deficit with China, which snowballed to $20 trillion between 1974 and 2024, constitutes a national emergency.

When Trump paused reciprocal tariffs on dozens of countries on April 9, he made an exception for China. Beijing, in turn, retaliated with import levies of its own.

Tit-for-tat exchanges quickly snowballed into eye-watering sums. By April 11, US tariffs on Chinese goods had reached 145 percent, while duties on US products entering China had swelled to 125 percent.

Tensions were defused in May, when Bessent and He Lifeng agreed to a truce which slashed respective tariffs by 115 percentage points for three months.

For now, US duties on Chinese products are set at 30 percent while China’s tariffs on the US have dropped to 10 percent.

What will happen next?

This week’s talks may pave the way for a potential meeting between Donald Trump and Chinese President Xi Jinping later in the year, although on Tuesday, Trump denied going out of his way to seek one.

For Thomas Sampson, a professor of economics at the London School of Economics, a face-to-face meeting has “the potential to be significant”. Equally though, it could be “a grip-and-grin style summit, where nothing substantive is discussed”, he told Al Jazeera.

Sampson added that US-China negotiations are more complex than those with other Asian countries, owing to China’s grip on rare earth minerals, in addition to the fact that China “has long been a target of Trump’s”.

For now, Sampson said he believes that the “mood around the [Sweden] talks seems more positive than earlier this year. Both sides, it seems, have stepped back from the brink”. His expectation is for a “more restrained trade war” than before, if one is to resume.

On Friday, White House press secretary Karoline Leavitt said trade talks with China were “moving in the right direction” and that Washington remains in “direct communication” with Beijing.

What other trade deals has Trump concluded in recent weeks?

On top of Trump’s Thursday tariff blitz, the latest US-China talks come after Washington struck deals with both the EU and Japan last week.

Last Sunday, Trump and European Commission President Ursula von der Leyen announced a trade agreement, ending a months-long standoff between two economic giants.

The EU accepted a 15 percent tariff on most of its exports, while the bloc’s average tariff rate on US goods will drop below 1 percent once the deal goes into effect.

Brussels also said it would purchase $750bn in American energy products and invest $600bn more into the US, on top of existing commercial agreements.

France’s Prime Minister Francois Bayrou said the EU had capitulated to Trump’s trade threats, labelling the deal struck on Sunday as a “dark day” for the EU.

The surge comes following announced investments in AI after the company laid off thousands of workers earlier this month.

Microsoft is now the second company ever to surpass $4 trillion in market valuation, following artificial intelligence giant Nvidia.

Microsoft, which is traded under the ticker “MSFT”, is continuing to surge and as of noon in New York City (16:00 GMT) on Thursday, it is up 4.6 percent from the market open.

The technology behemoth said it will spend $30bn in capital spending for the first quarter of the current fiscal year to meet soaring artificial intelligence (AI) demand. Microsoft also reported booming sales in its Azure cloud computing business on Wednesday.

“It is in the process of becoming more of a cloud infrastructure business and a leader in enterprise AI, doing so very profitably and cash generatively despite the heavy AI capital expenditures,” said Gerrit Smit, lead portfolio manager, Stonehage Fleming Global Best Ideas Equity Fund.

Redmond, Washington-headquartered Microsoft first cracked the $1 trillion mark in April 2019.

Its move to $3 trillion was more measured than that of technology giants Nvidia and Apple, with AI-bellwether Nvidia tripling its value in just about a year and clinching the $4 trillion milestone before any other company on July 9.

In its earnings report, revenue topped $76.4bn.

‘Slam-dunk’

“This was a slam-dunk quarter for MSFT [Microsoft] with cloud and AI driving significant business transformation across every sector and industry as the company continues to capitalize on the AI Revolution unfolding front and center,” Dan Ives, senior analyst at Wedbush Securities, said in a note provided to Al Jazeera.

Microsoft’s multibillion-dollar bet on OpenAI is proving to be a game-changer, powering its Office Suite and Azure offerings with cutting-edge AI and fuelling the stock to more than double its value since ChatGPT’s late-2022 debut.

Its capital expenditure forecast, its largest ever for a single quarter, has put it on track to potentially outspend its rivals over the next year.

“We closed out the fiscal year with a strong quarter, highlighted by Microsoft Cloud revenue reaching $46.7bn, up 27 percent [up 25 percent in constant currency] year-over-year,” Amy Hood, executive vice president and chief financial officer of Microsoft, said in a statement.

However, Microsoft’s surge in market value is overshadowed by a wave of layoffs at the tech giant. Earlier this month, the company laid off 9,000 people, representing 4 percent of its global workforce, while doubling down on AI.

Lately, breakthroughs in trade talks between the United States and its trading partners ahead of US President Donald Trump’s August 1 tariff deadline have buoyed stocks, propelling the S&P 500 and the Nasdaq to record highs.

Meta Platforms also doubled down on its AI ambitions, forecasting third-quarter revenue that blew past Wall Street estimates as artificial intelligence supercharged its core advertising business.

The social media giant upped the lower end of its annual capital spending by $2bn – just days after Alphabet made a similar move – signalling that Silicon Valley’s race to dominate the artificial-intelligence frontier is only accelerating.

Microsoft says cyber-espionage campaign ‘poses high risk’ to foreign embassies, diplomats and other groups in Moscow.

Microsoft has accused one of the Russian government’s premier cyber-espionage units of deploying malware against embassies and diplomatic organisations in Moscow by leveraging local internet service providers.

In a blog post on Thursday, Microsoft Threat Intelligence said the campaign by Russia’s Federal Security Service, also known as the FSB, “has been ongoing since at least 2024”.

The effort “poses a high risk to foreign embassies, diplomatic entities, and other sensitive organizations operating in Moscow, particularly to those entities who rely on local internet providers”, Microsoft said.

The analysis confirms for the first time that the FSB is conducting cyber-espionage at the ISP level, according to Microsoft’s findings.

“This means that diplomatic personnel using local ISP or telecommunications services in Russia are highly likely targets of [the campaign] within those services,” the blog post reads.

Microsoft tracked an alleged FSB cyber-espionage campaign that in February targeted unnamed foreign embassies in Moscow.

The FSB activity facilitates the installation of custom backdoors on targeted computers, which can be used to install additional malware, as well as steal data, Microsoft said.

The findings come amid increasing pressure from Washington for Moscow to agree to a ceasefire in its war in Ukraine and pledges from NATO countries to increase defence spending surrounding their own concerns about Russia.

Microsoft did not say which embassies were targeted by the FSB campaign.

The US Department of State, as well as Russian diplomats, did not respond to requests for comment from the Reuters news agency.

Russia has denied carrying out cyber-espionage operations. There was no immediate comment from Moscow on Microsoft’s report on Thursday.

The hacking unit linked to the activity, which Microsoft tracks as “Secret Blizzard” and others categorise as “Turla”, has been hacking governments, journalists and others for nearly 20 years, the US government said in May 2023.

United States President Donald Trump’s tariffs are set to come into effect on August 1. They mark a significant escalation in US trade policy, leading to higher prices for consumers and bigger financial hits for companies.

Trump had initially postponed “reciprocal tariffs”, which he had announced on April 2, giving countries time to reach trade deals with the US.

On Sunday, US Commerce Secretary Howard Lutnick said the August 1 tariffs were a “hard deadline”.

What are the August 1 tariffs?

Several countries are facing a slew of tariffs on August 1. While the situation remains dynamic, different levies are going to hit countries ranging from 15 percent on Japan and the European Union to 50 percent on Brazil.

Who has struck last-minute deals?

Trump has struck a series of bilateral trade deals in the last few days.

With the EU, the US secured $750bn in energy purchases and reduced tariffs on steel via a quota system. In exchange, it lowered auto tariffs from 30 percent to 15 percent, applying the same rate to pharmaceuticals and semiconductors.

Japan committed $550bn in investments targeting US industries such as semiconductors, AI and energy, while increasing rice imports under a 100,000-tonne duty-free quota. It will also purchase US commodities like ethanol, aircraft and defence goods.

Indonesia reportedly agreed to duty-free access for many US products and increased energy and agricultural imports, although Jakarta has only confirmed tariff cuts and key commodity purchases so far.

The United Kingdom gained aerospace and auto export benefits, while granting the US duty-free beef quotas and a 1.4 billion litre ethanol quota.

China saw its reciprocal tariffs slashed from 145 percent to the baseline 10 percent that was imposed on all countries. In addition, there’s a 20 percent punitive tariff for fentanyl trafficking. A temporary pause for the final tariff rate has been extended until August 12 while the two hammer out a deal. China matched the cut and eased non-tariff measures, resuming rare earth exports and accepting Boeing deliveries.

Deals with the Philippines, Cambodia and Vietnam also include tariff adjustments and market access, though not all terms have been confirmed by those governments.

Which sectors are expected to be hit worst?

According to a Reuters news agency tracker, which looks at how companies are responding to Trump’s tariff threats, the first-quarter earnings season saw automakers, airlines and consumer goods importers take the worst hit by tariff threats.

Levies on aluminium and electronics, such as semiconductors, led to increased costs.

“When you start to see tariffs at 20 or more, you reach a point where firms may stop importing altogether,” Joseph Foudy, an economics professor at the New York University Stern School of Business, told Al Jazeera.

“Firms simply postpone major decisions, delay hiring, and economic activity declines,” Foudy added.

Economists widely agree that the impact of tariffs implemented so far has not been fully felt, as many businesses built up their stockpiles of inventories in advance to mitigate rising costs.

In an analysis published last month, BBVA Research estimated that even the current level of US tariffs – including a baseline 10 percent duty on nearly all countries, and higher levies on cars and steel – could slow economic growth and reduce global gross domestic product (GDP) by 0.5 of a percentage point in the short term, and by more than 2 percentage points over the medium term.

Have prices increased?

According to HBS Pricing Lab reports, prices of US-made and imported goods saw modest seasonal declines through early March, with imports falling slightly more. The first 10 percent US tariff on Chinese goods (February 4) had little effect, but prices rose after broader tariffs were imposed on March 4, including a 25 percent tariff on Canadian and Mexican imports and another 10 percent tariff on China. Imported goods prices jumped by 1.2 points, while prices of domestic goods rose by half as much.

After a 10 percent global tariff was announced on April 2, “Liberation Day”, and 145 percent on China on April 10, import prices rose more sharply. A brief price dip followed the May 12 tariff rollback on Chinese goods, but trends resumed by June. Overall, import prices rose about 3 percent since March – small compared to headline tariff rates.

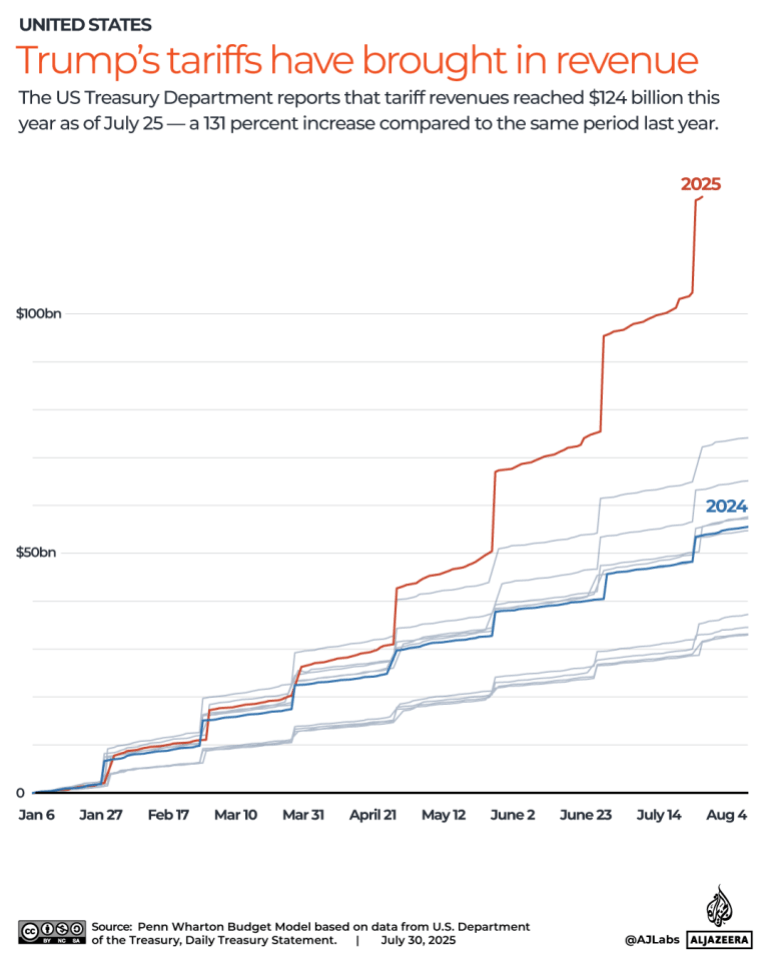

Have tariffs brought in money?

Trump’s tariffs have brought in revenue from higher duties paid by importers. Between January 2 to July 25, the US Treasury Department data shows that the US generated $124bn this year from tariffs. This is 131 percent more than the same time last year.

In early July, Treasury Secretary Scott Bessent said this could grow to $300bn by the end of 2025 as collections accelerate from Trump’s trade campaign.

Oral arguments over United States President Donald Trump’s power to impose tariffs have kicked off before a US appeals court after a lower court ruled he had exceeded his authority by imposing sweeping new levies on imported goods.

The appeals court judges on Thursday sharply questioned whether what Trump calls his “reciprocal” tariffs, announced in April, were justified by the president’s claim of emergency powers.

A panel of all the court’s active judges – eight appointed by Democratic presidents and three appointed by Republican presidents – is hearing arguments in two cases brought by five small US businesses and 12 Democratic-led US states.

The judges on the US Court of Appeals for the Federal Circuit in Washington, DC, pressed government lawyer Brett Shumate to explain how the International Emergency Economic Powers Act (IEEPA), a 1977 law historically used for sanctioning enemies or freezing their assets, gave Trump the power to impose tariffs.

Trump is the first president to use IEEPA to impose tariffs.

The judges frequently interrupted Shumate, peppering him with a flurry of challenges to his arguments.

“IEEPA doesn’t even say tariffs, doesn’t even mention them,” one of the judges said.

Shumate said the law allows for “extraordinary” authority in an emergency, including the ability to stop imports completely. He said IEEPA authorises tariffs because it allows a president to “regulate” imports in a crisis.

The states and businesses challenging the tariffs argued they are not permissible under IEEPA and the US Constitution grants Congress, and not the president, authority over tariffs and other taxes.

Neal Katyal, a lawyer for the businesses, said the government’s argument that the word “regulate” includes the power to tax would be a vast expansion of presidential power.

Tariffs are starting to build into a significant revenue source for the federal government as customs duties in June quadrupled to about $27bn, a record, and through June have topped $100bn for the current fiscal year, which ends on September 30. That income could be crucial to offset lost revenue from extended tax cuts in a Trump-supported bill that passed and became law this month.

“Tariffs are making America GREAT & RICH Again,” Trump wrote in a social media post on Thursday. “To all of my great lawyers who have fought so hard to save our Country, good luck in America’s big case today.”

But economists said the duties threaten to raise prices for US consumers and reduce corporate profits. Trump’s on-again, off-again tariff threats have roiled financial markets and disrupted US companies’ ability to manage supply chains, production, staffing and prices.

Dan Rayfield, the attorney general of Oregon, one of the states challenging the levies, said the tariffs are a “regressive tax” that is making household items more expensive.

Since Trump began imposing his wave of tariffs, companies ranging from carmaker Stellantis to American Airlines, temporarily suspended financial guidance for investors, which has since started again but has been revised down. Companies across multiple industries, including Procter and Gamble, the world’s largest consumer goods brand, announced this week that it would need to raise prices on a quarter of its goods.

The president has made tariffs a central instrument of his foreign policy, wielding them aggressively in his second term as leverage in trade negotiations and to push back against what he has called unfair practices.

Pressure outside trade

Trump has said the April tariffs, which he placed on most countries, are a response to persistent US trade imbalances and declining US manufacturing power. However, in recent weeks, he’s used them to increase pressure on nontrade issues.

He hit Brazil with 50 percent tariffs over the prosecution of former Brazilian President Jair Bolsonaro, a key Trump ally who is on trial for an alleged coup attempt after he lost the 2022 presidential election.

Trump also threatened Canada over its move to recognise a Palestinian state, saying a trade deal will now be “very hard”.

He said tariffs against China, Canada and Mexico were appropriate because those countries were not doing enough to stop fentanyl from crossing US borders. The countries have denied that claim.

On May 28, a three-judge panel of the US Court of International Trade sided with the Democratic states and small businesses that are challenging Trump.

It said IEEPA, a law intended to address “unusual and extraordinary” threats during national emergencies, did not authorise tariffs related to longstanding trade deficits. The appeals court has allowed the tariffs to remain in place while it considers the administration’s appeal. The timing of the court’s decision is uncertain, and the losing side will likely appeal quickly to the US Supreme Court.

The case will have no impact on tariffs levied under more traditional legal authorities, such as duties on steel and aluminium. The president recently announced trade deals that set tariff rates on goods from the European Union and Japan after smaller trade agreements with Britain, Indonesia and Vietnam.

Trump’s Department of Justice has argued that limiting the president’s tariff authority could undermine ongoing trade negotiations while other Trump officials have said negotiations have continued with little change after the initial setback in court. Trump has set a deadline of Friday for higher tariffs on countries that don’t negotiate new trade deals.

There are at least seven other lawsuits challenging Trump’s invocation of IEEPA, including cases brought by other small businesses and California.

Global trade markets remained on edge Thursday as the United States prepared to implement reciprocal tariffs, with the deadline for negotiating a trade deal with Washington fast approaching.

US President Donald Trump has already announced steep trade tariffs for many of the country’s largest trading partners, even as dozens of countries scramble to secure last-minute deals or extensions for negotiations beyond the Friday, August 1 deadline.

Friday’s deadline comes more than 120 days after President Trump’s administration first announced a barrage of tariffs on the world, on the so-called “Liberation Day”.

Despite several delays in imposing tariffs since Trump took office in January this year, his administration looks set to roll out new tariff rates for those countries that fail to clinch a trade deal by the end of today.

So, what will happen tomorrow? Which countries already have deals in the bag? And who is hoping to rescue a last-minute deal?

What will happen on August 1?

As the clock ticks down to August 1, the US’s imposition of a significant round of reciprocal tariffs on imports from various countries marks a pivotal moment in global trade dynamics, experts say.

Trump is adamant he will not be extending this deadline. “THE AUGUST FIRST DEADLINE IS THE AUGUST FIRST DEADLINE – IT STANDS STRONG, AND WILL NOT BE EXTENDED. A BIG DAY FOR AMERICA!!!” Trump posted on his social media platform, Truth Social, on Wednesday.

At midnight Eastern Time tonight, therefore, US Customs and Border Protection will begin enforcing these new duties, which will range from 15 percent to 50 percent – or even higher in some cases – depending on the trading partner, the nature of the goods being traded and whether the trading partner and the US have specific agreements in place.

Additional sectoral tariffs will be applied to certain industries. For example, a 50 percent tariff will be applied to copper, steel and aluminium for most countries, while a 20 percent levy will be applied to pharmaceutical products.

The White House confirmed that Trump will sign new executive orders on Thursday, formally imposing all these higher tariffs. Recipients are likely to include some of the US’s biggest trading partners, like Mexico, Taiwan and Canada.

Many nations facing sweeping new tariffs on all exports to the US are likely to incur immediate economic repercussions along with potential shifts in diplomatic relations.

Tariffs may also cost the US economy. The Yale Budget Lab, a non-partisan policy research centre, noted in its most recent analysis that overseas trade tariffs could cost US households on average an extra $2,400 in 2025, because of higher prices of imported goods.

Meanwhile, industries reliant on imports, such as electronics, pharmaceuticals and clothing, may have to contend with new supply chain disruptions as companies scramble to absorb costs or pass them on to consumers.

President Donald Trump speaks to the media as he meets European Commission President Ursula von der Leyen at the Trump Turnberry golf course in Scotland on Sunday, July 27, 2025 [Jacquelyn Martin/AP]

Why is Trump launching all these new tariffs?

In April, Trump declared a “national emergency” when he announced his “Liberation Day” tariff strategy and imposed an across-the-board 10 percent baseline tariff on all imports, followed by higher, country-specific “reciprocal” tariffs.

The US has large trading deficits with many countries, which Trump believes are deeply unfair.

The Trump administration, therefore, has justified these new rates as being necessary to redress these trade imbalances in order to boost US manufacturing and jobs, even though economists point out that deficits are not direct evidence of unfair trade practices.

Beyond trade, experts note that the Trump administration is leveraging these tariff threats to broader agendas of curbing immigration, combating the opioid and fentanyl crisis, and pressing allies and partners on geopolitical issues, including India’s energy ties with Russia or Brazil’s legal action against Trump ally Jair Bolsonaro.

In the last-minute run-up to the August 1 deadline, Trump’s administration has strong-armed trading partners, including Japan, the European Union, Indonesia and the Philippines, into new deals under which they accept higher US tariffs in exchange for continued market access and investment commitments – and in most cases, a promise not to levy counter-tariffs of their own.

Who already has deals in the bag with the US?

European Union

The EU has agreed to a 15 percent tariff on most of its exports to the US, including cars and pharmaceuticals, in exchange for zero tariffs on select US exports and commitments to buy US gas and increase investments. Initially, Trump had threatened a 30 percent rate.

Japan

Japan has secured a 15 percent reciprocal tariff on its goods exported to the US, reduced from a threatened 25 percent, with Japan promising to invest $550bn in the US economy.

United Kingdom

The UK agreed to a 10 percent tariff rate on its exports to the US. It also received a 25 percent sectoral tariff on steel and aluminium – half the 50 percent being imposed on other countries.

South Korea

A lower 15 percent tariff will apply to South Korean imports to the US, in return for a $350bn investment pledge and zero tariffs on US exports like cars and agricultural products.

Indonesia

Indonesia has negotiated a 19 percent tariff on its exports to the US, down from a threatened 32 percent, by making a commitment to buy US Boeing aircraft and to remove or reduce trade barriers.

Vietnam

Vietnam has agreed to a 20 percent tariff on most exports to the US, with an additional 40 percent levy to be applied to “transshipped” goods – those entering the US via another location – while also agreeing to zero tariffs on US imports like large-engine automobiles.

Philippines

This Philippines has agreed to a 19 percent tariff on its exports to the US, with zero tariffs on US exports to the Philippines, alongside commitments for enhanced military cooperation.

Pakistan

Struck a deal to jointly develop oil reserves with the US, but specific tariff rates on goods remain unclear.

Which big US partners have no deal yet?

None of the US’s top three trading partners – Mexico, Canada, and China – have trade deals in place as of Thursday.

Mexico

Tops the list of trade partners of the US, with nearly $840bn in total trade, driven by sectors including vehicles, electronics and agriculture. With no new deal for August 1, existing tariffs of 25 percent on most imports will persist under earlier 2025 trade war measures, with some exemptions under the United States-Mexico-Canada Agreement (USMCA).

Canada

Ranks second in terms of size with about $700bn, primarily in energy, vehicles, and aerospace products, passing between the two countries. With no deal finalised by the August 1 deadline, Trump has threatened to impose a 35 percent tariff on goods that don’t comply with the USMCA.

China

Third among the top US trade partners, Beijing trades about $532bn with the US, focused on electronics, machinery and consumer goods. With no permanent deal in place, a 30 percent combined tariff will be applied, following an agreed pause until August 12. That followed an earlier escalation to a 145 percent tariff on imports.

US President Donald Trump and Indian Prime Minister Narendra Modi are pictured in a mirror as they attend a joint news conference at the White House in Washington, DC, February 13, 2025 (Nathan Howard/Reuters)

Who is hoping for a last-minute deal?

India

Even a “very good friendship” with Washington could not save India, the world’s most populous nation and fourth-largest global economy, from Trump’s reciprocal tariffs.

On Wednesday, Trump announced a sweeping 25 percent tariff on all Indian goods exported to the US, plus an unspecified penalty for buying energy from Russia, as trade deal negotiations remain unresolved.

Total trade between the US and India was valued at about $130bn in 2024, with US exports to India worth $41.8bn and imports from India at $87.4bn – a trade deficit which Trump will not ignore.

“While India is our friend, we have, over the years, done relatively little business with them because their Tariffs are far too high,” Trump wrote on his Truth Social platform.

Later, in another post, Trump said he did not “care what India does with Russia. They can take their dead economies down together, for all I care.

“We have done very little business with India, their Tariffs are too high, among the highest in the World. Likewise, Russia and the USA do almost no business together,” he wrote. “Let’s keep it that way.”

In a statement, the Indian government said it was studying the implications of these new tariffs and added: “India and the US have been engaged in negotiations on concluding a fair, balanced and mutually beneficial bilateral trade agreement over the last few months.”

The statement further noted that “we remain committed to that objective.” New Delhi signalled what it believes to be potential barriers to the deal by noting that the government “attaches the utmost importance to protecting and promoting the welfare of our farmers, entrepreneurs, and MSMEs”.

Pakistan

India’s neighbouring rival, Pakistan, has seen its stock rise with the Trump administration before and after the military conflict with New Delhi earlier this year.

Trump revealed that the US had concluded a deal with Pakistan, where they will work together on developing oil reserves, but did not announce tariffs. “Who knows, maybe they’ll be selling Oil to India some day!”

Taiwan

Taiwan is also facing a high-stakes deadline, with proposed tariffs set at 32 percent, excluding semiconductors, if no deal is struck by August 1.

Taiwanese officials have engaged in intense negotiations in Washington, spanning four high-level rounds led by Vice Premier Cheng Li‑chun and US counterparts, addressing not only tariff technicalities but also non‑tariff trade barriers, investments and market access. These talks are reportedly pending US approval.

Russian President Vladimir Putin greets Brazilian President Luiz Inacio Lula da Silva before a military parade on Victory Day, marking the 80th anniversary of the victory over Nazi Germany in World War II, in Moscow, Russia, May 9, 2025 [Alexei Nikolsky/Host agency RIA Novosti/Handout via Reuters]

Who has little hope of reaching a deal with the US?

Brazil

The country faces the most punishing tariffs among major US trading partners, with President Trump formally issuing a 50 percent reciprocal tariff on Brazilian imports.

The US actually runs a trade surplus with Brazil of nearly $7.4bn; however, Trump has been unhappy about the prosecution of former President Jair Bolsonaro, who is facing trial for allegedly attempting a coup to overturn his 2022 election loss.

Trump has publicly called the trial a “witch-hunt” and an “international disgrace”, tying his imposition of a 50 percent tariff on Brazilian imports, announced on July 10, directly to this issue.

Brazil’s government responded with alarm. President Lula decried Trump’s measures as “economic blackmail” and negotiations have stalled.

Speaking at a news conference in Washington this week, Pierre-Olivier Gourinchas, the IMF’s chief economist, called for an end to the trade war.

“Restoring stability in trade policy is essential to reduce policy uncertainty. We urge all parties to settle trade disputes and agree on clear and predictable frameworks. Collective efforts should be made to restore and improve the global trading system,” Gourinchas said, indirectly referring to the Trump administration.

The world’s largest consumer goods maker said it will have to raise prices on a quarter of its products starting in August.

Procter & Gamble has said it will need to raise prices on a quarter of the goods it sells in the United States starting this month in order to mitigate costs it has faced because of the tariffs imposed by US President Donald Trump.

On Tuesday, in conjunction with its earnings report, the world’s largest consumer goods maker named Shailesh Jejurikar as its new chief executive officer as the company navigates tariff-driven uncertainty weighing on the sector.

The price hikes have been communicated to retailers such as Walmart and Target and are in the mid-single digits across categories, a spokesperson said, and will be seen on shelves starting in August.

In May, Walmart also announced that it would need to raise prices on goods sold at the big box retailer because of the economic impact of tariffs.

P&G topped fourth-quarter estimates for its earnings report. The Cincinnati, Ohio-based firm reported revenue of $20.89bn for the quarter. Organic sales grew about 2 percent in fiscal 2025, driven by P&G’s portfolio of branded pantry staples, as well as higher pricing, particularly for fresher products. But that comes as growth is expected to slow.

Growth stalls

P&G expects fiscal 2026 annual net sales growth of between 1 percent and 5 percent, largely below estimates of a 3.09 percent growth.

Market growth slowed from where it was at the start of the year in both the US and Europe, and volatile macroeconomic, geopolitical and consumer dynamics were resulting in headwinds that were not anticipated at the start of the year, CFO Andre Schulten said during a call with journalists.

“The consumer clearly is more selective in terms of shopping behaviour in our categories, and we see a desire to find value either by going into larger pack sizes in club channel or online or big box retailers or by lowering the cash outlay,” Schulten said.

The comments from the company reinforce how consumers, particularly in the lower-income category, are seeking value as they look to stretch their household budgets. Packaged food maker Nestle said last week that consumer spending in North America remained weak.

“Given the immense pressure put on US consumers in particular, the organic growth is a very good sign that long-term earnings projections should hold up,” said Brian Mulberry, portfolio manager at Zacks Investment Management.

P&G, which makes household basics spanning from Bounty paper towels to Metamucil fibre supplements, estimated tariffs will increase its costs by about $1bn before tax for fiscal 2026. That compares with projections of between $1bn and $1.5bn made in April.

The company rolled out a restructuring effort in June to exit some brands and cut about 7,000 jobs over the next two years to increase productivity. Prices rose about 1 percent in the fourth quarter, while volumes were flat.

P&G expects fiscal 2026 core net earnings per share growth in the range of $6.83 and $7.09, compared with estimates of $6.99, according to estimates compiled by LSEG.

On Wall Street, the company’s stock over the last five days is down 0.5 percent, down 1.1 percent for the month and since the beginning of the year, it has tumbled 5.15 percent.

The International Monetary Fund has raised its global growth forecasts for 2025 and 2026 slightly, citing stronger-than-expected purchases in advance of an August 1 jump in tariffs imposed by the United States and a drop in the effective US tariff rate to 17.3 percent from 24.4 percent.

In its forecast on Tuesday, it warned, however, that the global economy faced major risks including a potential rebound in tariff rates, geopolitical tensions and larger fiscal deficits that could drive up interest rates and tighten global financial conditions.

“The world economy is still hurting, and it’s going to continue hurting with tariffs at that level, even though it’s not as bad as it could have been,” said Pierre-Olivier Gourinchas, IMF chief economist.

In an update to its World Economic Outlook from April, the IMF raised its global growth forecast by 0.2 percentage point to 3 percent for 2025 and by 0.1 percentage point to 3.1 percent for 2026. However, that is still below the 3.3 percent growth it had projected for both years in January and the pre-pandemic historical average of 3.7 percent.

It said global headline inflation was expected to fall to 4.2 percent in 2025 and 3.6 percent in 2026, but noted that inflation would likely remain above target in the US as tariffs passed through to consumers in the second half of the year.

The US effective tariff rate – measured by import duty revenue as a proportion of goods imports – has dropped since April, but remains far higher than its estimated level of 2.5 percent in early January. The corresponding tariff rate for the rest of the world is 3.5 percent, compared with 4.1 percent in April, the IMF said.

US President Donald Trump has upended global trade by imposing a universal tariff of 10 percent on nearly all countries since April and threatening even higher duties to kick in on Friday. Far higher tit-for-tat tariffs imposed by the US and China were put on hold until August 12, with talks in Stockholm this week potentially leading to a further extension.

The US has also announced steep duties ranging from 25 percent to 50 percent on automobiles, steel and other metals, with higher duties soon to be announced on pharmaceuticals, lumber, and semiconductor chips.

Such future tariff increases are not reflected in the IMF numbers, and could raise effective tariff rates further, creating bottlenecks and amplifying the effect of higher tariffs, the IMF said.

Shifting tariffs

Gourinchas said the IMF was evaluating new 15-percent tariff deals reached by the US with the European Union and Japan over the past week, which came too late to factor into the July forecast, but said the tariff rates were similar to the 17.3 percent rate underlying the IMF’s forecast.

“Right now, we are not seeing a major change compared to the effective tariff rate that the US is imposing on other countries,” he said, adding it was not yet clear if these agreements would last.

“We’ll have to see whether these deals are sticking, whether they’re unravelled, whether they’re followed by other changes in trade policy,” he said.

Staff simulations showed that global growth in 2025 would be roughly 0.2 percentage point lower if the maximum tariff rates announced in April and July were implemented, the IMF said.

The IMF said the global economy was proving resilient for now, but uncertainty remained high and current economic activity suggested “distortions from trade, rather than underlying robustness”.

Gourinchas said the 2025 outlook had been helped by what he called “a tremendous amount” of front-loading as businesses tried to get ahead of the tariffs, but he warned that the stockpiling boost would not last.

“That is going to fade away,” he said, adding, “That’s going to be a drag on economic activity in the second half of the year and into 2026. There is going to be pay back for that front loading, and that’s one of the risks we face.”

Tariffs were expected to remain high, he said, pointing to signs that US consumer prices were starting to edge higher.

“The underlying tariff is much higher than it was back in January, February. If that stays … that will weigh on growth going forward, contributing to a really lackluster global performance.”

One unusual factor has been a depreciation of the dollar, not seen during previous trade tensions, Gourinchas said, noting that the lower dollar was adding to the tariff shock for other countries, while also helping ease financial conditions.

US growth was expected to reach 1.9 percent in 2025, up 0.1 percentage point from April’s outlook, edging up to 2 percent in 2026. A new US tax cut and spending law was expected to increase the US fiscal deficit by 1.5 percentage points, with tariff revenues offsetting that by about half, the IMF said.

It lifted its forecast for the euro area by 0.2 percentage point to 1 percent in 2025, and left the 2026 forecast unchanged at 1.2 percent. The IMF said the upward revision reflected a historically large surge in Irish pharmaceutical exports to the US; without it, the revision would have been half as big.

China’s outlook got a bigger upgrade of 0.8 percentage point, reflecting stronger-than-expected activity in the first half of the year, and the significant reduction in US-China tariffs after Washington and Beijing declared a temporary truce.

The IMF increased its forecast for Chinese growth in 2026 by 0.2 percentage point to 4.2 percent.

Overall, growth is expected to reach 4.1 percent in emerging markets and developing economies in 2025, edging lower to 4 percent in 2026, it said.

The IMF revised its forecast for world trade up by 0.9 percentage point to 2.6 percent, but cut its forecast for 2026 by 0.6 percentage point to 1.9 percent.

Union Pacific has announced its intentions to buy its smaller rival, Norfolk Southern, which would create the first coast-to-coast freight rail operator in the United States and reshape the movement of goods from grains to autos across the US.

The Omaha, Nebraska-based railroad giant announced the proposed $85bn deal on Tuesday.

If the merger is approved, the transaction would be the largest-ever buyout in the railroad sector.

Union Pacific has a stronghold in the western two-thirds of the US, with Norfolk’s 31,382 km (19,500-mile) network that primarily spans 22 eastern states.

The two railroads are expected to have a combined enterprise value of $250bn and would unlock about $2.75bn in annualised synergies, the companies said.

The $320 per share price implies a premium of 18.6 percent for Norfolk from its close on July 17, when reports of the merger first emerged.

The companies said last week on Thursday that they were in advanced discussions for a possible merger.

The deal will face lengthy regulatory scrutiny amid union concerns about potential rate increases, service disruptions and job losses. The 1996 merger of Union Pacific and Southern Pacific had temporarily led to severe congestion and delays across the Southwest.

The deal reflects a shift in antitrust enforcement under US President Donald Trump’s administration. Executive orders aimed at removing barriers to consolidation have opened the door to mergers that were previously considered unlikely.

Surface Transportation Board Chairman Patrick Fuchs, appointed in January, has advocated for faster preliminary reviews and a more flexible approach to merger conditions.

Even under an expedited process, the review could take from 19 to 22 months, according to a person involved in the discussions.

Major railroad unions have long opposed consolidation, arguing that such mergers threaten jobs and risk disrupting rail service.

“We will weigh in with the STB [regulator] and with the Trump administration in every way possible,” said Jeremy Ferguson, president of the SMART-TD union’s transport division, after the two companies said they were in advanced talks last week.

“This merger is not good for labour, the rail shipper/customer or the public at large,” he said.

The companies said they expect to file their application with the STB within six months.

The SMART-TD union’s transport division is North America’s largest railroad operating union with more than 1,800 railroad yardmasters.

The North American rail industry has been grappling with volatile freight volumes, rising labour and fuel costs and growing pressure from shippers over service reliability, factors that could further complicate the merger.

Industry consolidation

The proposed deal has also prompted competitors BNSF, owned by Berkshire Hathaway, and CSX, to explore merger options, people familiar with the matter said.

Agents at the STB are already conducting preparatory work, anticipating they could soon receive not just one, but two megamerger proposals, a person close to the discussions told Reuters on Thursday.

If both mergers are approved, the number of Class I railroads in North America would shrink to four from six, consolidating major freight routes and boosting pricing power for the industry.

The last major deal in the industry was the $31bn merger of Canadian Pacific and Kansas City Southern that created the first and only single-line rail network connecting Canada, the US and Mexico.

That deal, finalised in 2023, faced heavy regulatory resistance over fears it would curb competition, cut jobs and disrupt service, but was ultimately approved.

Union Pacific is valued at nearly $136bn, while Norfolk Southern has a market capitalisation of about $65bn, according to data from LSEG.

As of 12:15pm in New York (16:15 GMT), Union Pacific’s stock is down 3.9 percent, and Norfolk Southern is down 3.2 percent. Competitor CSX is also trending down. The stock has fallen 1.6 percent since the market opened this morning.

As United States President Donald Trump blasts his way through tariff announcements, one thing is clear, experts say: Some level of duties is here to stay.

In the past few weeks, Trump has announced a string of deals – with the European Union, Japan, Indonesia, Vietnam and the Philippines – with tariffs ranging from 15 percent to 20 percent.

He has also threatened Brazil with a 50 percent tariff, unveiled duties of 30 percent and 35 percent for major trading partners Mexico and Canada, and indicated that deals with China and India are close.

How many of Trump’s tariff rates will shake out is anybody’s guess, but one thing is clear, according to Vina Nadjibulla, vice president of research and strategy at the Asia Pacific Foundation of Canada: “No one is getting zero tariffs. There’s no going back.”

Trump’s various announcements have spelled months of chaos for industry, leaving businesses in limbo and forcing them to pause investment and hiring decisions.

The World Bank has slashed its growth forecasts for nearly 70 percent of economies – including the US, China and Europe, and six emerging market regions – and cut its global growth estimate to 2.3 percent, down from 2.7 percent in January.

Oxford Economics has forecast a shallow recession in capital spending in the Group of Seven (G7) countries – Canada, France, Germany, Italy, Japan, the United Kingdom and the US – lasting from the second quarter to the third quarter of this year.

“What we’re seeing is the Donald Trump business style: There’s lots of commotion, lots of claim, lots of activity and lots of b*******,” Robert Rogowsky, professor of international trade at the Middlebury Institute of International Studies, told Al Jazeera.

“That’s his business model, and that’s how he operates. That’s why he’s driven so many of his businesses into bankruptcy. It’s not strategic or tactical. It’s instinctive.”

Rogowsky said he expects Trump to push back his tariff deadline again, after delaying it from April to July, and then to August 1.

“It’s going to be a series of TACO tariffs,” Rogowsky said, referring to the acronym for “Trump Always Chickens Out”, a phrase coined by Financial Times columnist Robert Armstrong in early May to describe the US president’s backpedalling on tariffs in the face of stock market turmoil.

“He will bump them again,” Rogowsky said. “He’s just exerting the image of power.”

Trump’s back-and-forth policy moves have characterised his dealings with some of the US’s biggest trade partners, including China and the EU.

China’s tariff rate has gone from 20 percent to 54 percent, to 104 percent, to 145 percent, and then 30 percent, while the deadline for implementation has shifted repeatedly.

The proposed tariff rates for the EU have followed a similar pattern, going from 20 percent to 50 percent to 30 percent, and then 15 percent following the latest trade deal.

The EU’s current tariff rate only applies to 70 percent of goods, with a zero rate applying to a limited range of exports, including semiconductor equipment and some chemicals.

European steel exports will continue to be taxed at 50 percent, and Trump has indicated that new tariffs could be on the way for pharmaceutical products.

Despite the trade deals, many details of how Trump’s tariffs will work in practice remain unclear.

Whether Trump announces more changes down the track, analysts agree that the world has entered a new phase in which countries are seeking to become less reliant on the US.

“Now that the initial shock and anger [at Trump policies] has subsided, there is a quiet determination to build resilience and become less reliant on the US,” Nadjibulla said, adding that Trump was pushing countries to address longstanding issues that had been untouchable before.

Canada, for instance, is tackling inter-provincial trade barriers, a politically sensitive issue historically, even as it looks elsewhere to increase exports, said Tony Stillo, director of Canada Economics at Oxford Economics.

“It would be foolhardy not to provide to the US, seeing as it’s our largest market, but it also makes us more resilient to provide to other markets as well,” Stillo told Al Jazeera.

Canadian Prime Minister Mark Carney has reached out to the EU and Mexico and indicated his wish to improve his country’s strained relations with China and India.

This month, Canada expanded its exports of liquified natural gas beyond the US market, with its first shipment of cargoes to Asia.

To mitigate the fallout of Trump’s tariffs, Ottawa has been offering relief to Canadian businesses, including automakers, and has instituted a six-month pause on tariffs on some imports from the US to give firms time to re-adjust their supply chains.

There is also “some relief” in the fact that other countries “don’t seem to be imitating the Trump show [by levying their own tariffs]. They’re witnessing this attempt to strong-arm the rest of the world, but it doesn’t seem to be working,” Mary Lovely, the Anthony M Solomon senior fellow at the Peterson Institute for International Economics (PIIE), told Al Jazeera.

But the world is watching how the tariffs will affect the US economy, as “that will also be instructive to other countries”, Lovely said.

“If we see a slowdown, as we expect, it becomes a cautionary tale for others.”

Although the US stock market is near an all-time high, it is heavily weighted towards the “magnificent seven”, said Lovely, referring to the largest tech companies, and that reflects just one part of the economy.

Re-emergence of industrial policy

Trump’s tariffs come on top of other growing challenges for exporters the world over, including China’s subsidy-heavy industrial policy that allows its businesses to undercut its competitors.

“We’ve entered a period of global economic alignment with the reintroduction of industrial policies,” Nadjibulla said, explaining that more and more governments are likely to roll out support for their domestic industries.

“Each country will have to navigate these and find ways to de-risk and reduce overreliance on the US and China.”

Still, countries seeking to support their homegrown industries will have to do so while reckoning with the World Trade Organization and rules-based trade agreements such as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership, Nadjibulla said.

“It will take some tremendous leadership around the world to corral this wild mustang [Trump] before he breaks up the world order,” Rogowsky said.

“But it will break because I do think Donald Trump will drive us into a recession.”

The United States and the European Union have reached a wide-ranging trade agreement, ending a months-long standoff and averting a full-blown trade war just days before President Donald Trump’s deadline to impose steep tariffs.

The EU will pay 15 percent tariffs on most goods, including cars. The tariff rate is half the 30 percent Trump had threatened to implement starting on Friday. Brussels also agreed on Sunday to spend hundreds of billions of dollars on US weaponry and energy products on top of existing expenditures.

Speaking to reporters at his Turnberry golf resort in Scotland, Trump hailed the agreement as the “biggest deal ever made”. “I think it’s going to be great for both parties. It’s going to bring us closer together,” he added.

European Commission President Ursula von der Leyen said the agreement would “bring stability” and “bring predictability that’s very important for our businesses on both sides of the Atlantic”.

Von der Leyen defended the deal, saying the aim was to rebalance a trade surplus with the US. Trump has made no secret of using tariffs to try to trim US trade deficits.

Sunday’s agreement capped off months of often tense shuttle diplomacy between Brussels and Washington although neither side disclosed the full details of the pact or released any written materials.

So how will the deal impact the two sides, which account for almost a third of global trade, and will it end the threats of a tariff war?

What was agreed?

At a news event at Trump’s golf resort, von der Leyen said a 15 percent tariff would apply to European cars, pharmaceuticals and semiconductors – all important products for Europe’s economy.

For his part, Trump said US levies on steel and aluminium, which he has set at 50 percent on many countries, would not be cut for EU products, dashing the hopes of industry in the bloc. Elsewhere, aerospace tariffs will remain at zero for now.

In exchange for the 15 percent tariff rate on EU goods, Trump said the bloc would be “opening up their countries at zero tariff” for American exports.

In addition, he said the EU would spend an extra $750bn on US energy products, invest $600bn in the US and buy military equipment worth “hundreds of billions of dollars”.

Von der Leyen confirmed that the EU would seek to buy an extra $250bn of US energy products each year from now until 2027.

“With this deal, we are securing access to our largest export market,” she said.

At the same time, she acknowledged that the 15 percent tariffs would be “a challenge for some” European industries.

The EU is the US’s largest trading partner with two-way trade in goods and services last year reaching nearly $2 trillion.

How have European leaders responded?

German Chancellor Friedrich Merz welcomed the agreement, saying it avoids “an unnecessary escalation in transatlantic trade relations”.

He said a trade war “would have hit Germany’s export-oriented economy hard”, pointing out that the German car industry would see US tariffs lowered from 27.5 percent to 15 percent.

But French Prime Minister Francois Bayrou called the deal a “dark day” for Europe, saying the bloc had caved in to the US president with an unbalanced deal that spares US imports from any immediate European retaliation.

“It is a dark day when an alliance of free peoples, brought together to affirm their common values and to defend their common interests, resigns itself to submission,” Bayrou wrote on X of what he called the “von der Leyen-Trump deal”.

Wolfgang Niedermark, a board member of the Federation of German Industries trade body, called the deal “an inadequate compromise” with the EU “accepting painful tariffs”.

A 15 percent tariff rate “will have a huge negative impact on Germany’s export-oriented industry”, he said.

Earlier, Benjamin Haddad, France’s European affairs minister, said: “The trade agreement … will bring temporary stability to economic actors threatened by the escalation of American tariffs, but it is unbalanced.”

Echoing that sentiment, Dutch Foreign Trade Minister Hanneke Boerma said the deal was “not ideal” and called on the commission to continue negotiations with Washington.

The European Commission is responsible for negotiating trade deals for the entire bloc.

EU ambassadors will be discussing the agreement with the commission this week.

How was trade conducted before the deal?

On July 12, Trump threatened to impose 30 percent tariffs on EU goods if the two sides couldn’t reach a deal before this Friday, the day a suspension expires on the implementation of what Trump calls his “reciprocal tariffs”, which he placed on nearly all countries in the world.

Those “reciprocal tariffs” are due to come into effect in addition to the 25 percent tariffs on cars and car parts and the 50 percent levy on steel and aluminium products Trump already put in place.

On the European side, it is understood that Brussels would have pushed ahead with a retaliatory tariffs package on 90 billion euros ($109bn) of US goods, including car parts and bourbon, if talks had broken down.

The EU had been a frequent target of escalating trade rhetoric by Trump, who accused the bloc of “ripping off” the US.

In 2024, the US ran a $235.6bn goods deficit with the EU. Pharmaceuticals, car parts and industrial chemicals were among Europe’s largest exports to the US, according to EU data.

How will the deal impact the US and EU?

Bloomberg Economics estimated that a no-deal outcome would have raised the effective US tariff rate on European goods to nearly 18 percent on Friday.

The new deal brings that number down to 16 percent, offering a small reprieve to European exporting firms. Still, current trade barriers are much higher than before Trump took office in 2025.

According to Bruegel, a research group, the average US tariff rate on EU exports was just 1.5 percent at the end of 2024.

William Lee, chief economist at the Milken Institute, told Al Jazeera: “I think the [Trump] strategy has been clear from the very beginning. … It’s brinkmanship. … Either partner with the US or face high tariffs.”

Meanwhile, US Commerce Secretary Howard Lutnick said: “President Trump just unlocked one of the biggest economies in the world. The European Union is going to open its $20 trillion market and completely accept our auto and industrial standards for the first time ever.”

US president and his EU counterpart strike sweeping 15 percent tariff deal to stabilise transatlantic trade.

The United States and European Union have reached a sweeping trade agreement, setting a 15 percent tariff on most goods, averting a major transatlantic trade war that could have rattled global markets.

The announcement came after a private meeting on Sunday between US President Donald Trump and European Commission President Ursula von der Leyen at Trump’s Turnberry golf resort in Scotland.

The deal comes just days before Washington was due to impose 30 percent tariffs on EU imports.

“It was a very interesting negotiation. I think it’s going to be great for both parties,” Trump told reporters. He added that it was “a good deal for everybody… a giant deal with lots of countries”.

Von der Leyen welcomed the deal, saying it would “bring stability; it will bring predictability that’s very important for our businesses on both sides of the Atlantic”.

Trump claimed the EU committed to buying about $750bn worth of US energy, increasing investment in the United States by another $600bn and placing a large order for military equipment. Both leaders confirmed that the agreed tariff rate of 15 percent would apply broadly to automobiles and other goods.

“We have the opening up of all of the European countries,” Trump said. Von der Leyen echoed that, noting that the 15 percent rate was “across the board, all inclusive” and that the European market was effectively now open.

The talks followed months of tense back-and-forth with Trump, who has long accused the EU of unfair trade practices. Just before negotiations began, he called the existing arrangements “a very one-sided transaction; very unfair to the United States”.

Von der Leyen pointed to the combined economic might of the two powers, describing their trade volume as the world’s largest, encompassing “hundreds of millions of people and trillions of dollars”.

She acknowledged Trump’s “tough” reputation as a negotiator, to which he replied: “But fair.”

Trade conflict averted

Earlier this month, negotiations appeared close to collapse when Trump threatened to proceed with the 30 percent tariff unless the EU matched the 15 percent terms he recently struck with Japan. Asked if he would accept anything lower, Trump flatly said, “No”.

Had no agreement been reached, Brussels had prepared a long list of retaliatory tariffs targeting everything from beef and beer to Boeing aircraft and car parts.

German Chancellor Friedrich Merz said that the US-EU deal was a positive move that helped avoid a trade war and a serious blow to the auto sector.

“This agreement has succeeded in averting a trade conflict that would have hit the export-orientated German economy hard,” he said in a statement. “This applies in particular to the automotive industry, where the current tariffs of 27.5 percent will be almost halved to 15 percent.”

Italian Prime Minister Giorgia Meloni said it was “positive” that a trade deal had been reached; however, she needed to see the details, Italian news agency ANSA reported.

Trump and United Kingdom Prime Minister Kier Starmer are expected to meet on Monday, with trade also on the agenda. While a separate US–UK trade framework was unveiled in May, Trump insists the broader agreement is already concluded, though the White House admits some elements remain unfinished.

Trump will travel to Aberdeen on Tuesday to help open a third golf course under the family name. He and his sons are expected to cut the ribbon themselves.

United States President Donald Trump is scheduled to hold crunch talks with European Union chief Ursula von der Leyen in Scotland after weeksof intense trade talks between the two sides as Brussels aims to ink a deal with Washington to avoid a transatlantic trade war.