Italian banking group UniCredit has delivered a robust third quarter, underscoring its position as one of Europe’s stronger lenders.

“UniCredit delivered yet another set of record results, with net revenues up 1.2% and costs down 0.1% versus last year,” said CEO Andrea Orcel in a statement.

Net profit came in at €2.6 billion in the third quarter, up 4.7% year-on-year, and above a company estimate of €2.4bn.

Over the first nine months of the year, the bank’s net profits rose by 12.9% to €8.7bn.

“These results reflect disciplined execution, and I am confident that we will continue to build sustainable value for all stakeholders,” said Orcel.

UniCredit also reaffirmed full-year 2025 net profit guidance at €10.5bn and said it planned to distribute at least €9.5bn to shareholders.

Why this matters

In a European banking sector facing low growth, investor pressure, and regulatory hurdles, the results are significant for several reasons.

First, UniCredit’s combination of revenue growth, cost control, and low credit impairments suggests a resilience not always seen among its peers.

Second, the reaffirmation of strong guidance signals management confidence in execution through to year-end despite macroeconomic uncertainties in European and global markets.

Thirdly, the capital position and shareholder-return commitments indicate that the bank is in a position to manage risk and reward investors.

Europe’s banks are navigating reduced margins, regulatory costs, and lacklustre loan demand. Against that backdrop, UniCredit’s cost-income ratio of 37% in the quarter is a standout.

The lender also noted that its medium-term ambitions remain unchanged, standing by a net profit target of above €11 billion for the full-year 2027.

What to watch

Key to delivery will be how UniCredit handles a potential slowdown in areas such as net interest income, which fell 5.4% year-on-year in the quarter, and how it sustains its cost-efficiency edge.

The impact of wider economic weakness in Italy, Germany, and Central and Eastern Europe, all countries with strong UniCredit presence, remains a risk.

Additionally, conversion of its medium-term plans into reality will require continued disciplined execution. This is especially the case as the bank pursues strategic initiatives such as life insurance policy changes in Italy and its takeover of Commerzbank.

UniCredit has built a 26% stake in the German lender over the last year, although Orcel’s advances are facing fierce opposition from the government in Berlin.

At a roundtable at the bank’s headquarters in Cairo, CIB’s leadership team discusses expansion in Africa, commitment to sustainable finance, growing digital banking tools, and the future for the bank.

Global Finance celebrated the 50th anniversary of Commercial International Bank (CIB), Egypt’s largest private sector bank and a driving force in the transformation of Egypt’s banking sector, by holding a roundtable discussion.

The event, hosted at CIB’s headquarters in Cairo, gathered the bank’s top leadership team to discuss the bank’s history, how CIB has positioned itself as the leader in Egypt’s banking sector, and how it will continue to pursue growth while delivering innovative banking services for its clients.

The panel included:

CEO and Executive Board Member Hisham Ezz Al-Arab

Deputy CEO and Executive Board Member Amr El-Ganainy

Group Chief Finance and Operations Officer and Executive Board Member Islam Zekry

Global Markets CEO Omar El-Husseiny

Chief Retail, Commercial Banking, and Financial Inclusion Executive Rashwan Hammady

Hisham Ezz Al-Arab | CEO

Hisham Ezz Al-Arab was reappointed CEO of Commercial International Bank (CIB) – Egypt in September 2024. With over 40 years of international banking experience, he has served as CIB’s chairman (2023-2024), and as Chairman and MD (2002–2020). He also founded and chairs the CIB Foundation, which provides healthcare access for over 7 million underprivileged Egyptian children.

Global Finance: What major milestones has the bank achieved over the past 50 years, and what are some of the lessons learned?

Hisham Ezz Al-Arab: Well, you have to give credit to National Bank of Egypt (NBE) and Chase Manhattan for setting up CIB back in the 1970s, because it changed how commercial banking is being conducted. CIB at the time it was Chase National Bank—was the leader in credit lending. They changed the concept of asset lending into cash flow lending, and that was new. People used to lend against collateral and not against expected cash flow; that was a major change in the way of thinking. This was the tip of the iceberg that led the change. Below that there’s a very solid culture, to accept change, to innovate, to have something new all the time, and that carried on over the years. When I joined the bank in 1999, it was one of the large private sector banks. The management at the time and the board decided that we needed to make what you call a “major change.” We needed to be market leaders, and this was the time the bank made a lot of changes. From 1999 until about 2004, CIB was a market leader, applying all international standards and doing things really not required by domestic regulation but applied internationally.

CIB was the market leader in implementing the Basel III requirements in 2012 for asset liability management, not only for the credit flow and cash flow lending. We started to move to other areas of the commercial economy. Establishing for instance the World Risk Committee, Governance Committee, Immigration Committee, Illumination Committee—all of those things were not required by the Egyptian Law.

In 2005, NBE exited from CIB. We were very meticulous, as a board to make sure that the buyer would add value. And this is where the other journey started, in 2006. A consortium led by Ripplewood in the US became the key shareholders, with three representatives on the board. And this is another era when the bank started to change. We had solid board members who added a lot of value, selecting board members meticulously became a part of our culture. When ADQ bought a stake in CIB back in 2022, the quality of the board members was also outstanding. The critical thing is not the money, it’s the contribution of the board members.

Amr El-Ganainy | Deputy CEO

Amr El-Ganainy has served as deputy CEO and an Executive Board member of CIB since October 2023. He joined CIB in 2004 as general manager, Financial Institutions Group, and he successfully led the department through his strong business relationships in the market on the local and regional fronts.

GF: CIB has a growing presence across Africa with operations in Kenya and Ethiopia. Tell us about this experience and where the opportunities for further cross-border expansion are.

Islam Zekry: CIB’s expansion into Africa reflects our long-term vision to position the bank as a leading regional financial institution, exporting banking excellence into high-growth, strategically relevant markets. Our cross-border growth strategy prioritizes: sustainable value creation over pursuit of scale for its own sake, digital enablement to overcome infrastructure limitations and accelerate access, and facilitation of intra-African trade and investment flows, leveraging Egypt’s pivotal regional position.

Our ultimate objective is to build a resilient, scalable, and commercially viable cross-border banking model that reinforces CIB’s footprint across the continent.

So for an Egyptian bank operating from Cairo, there are two value corridors we can chase. One is the more-than-famous remittance corridor and the other is the East African trade corridor. This is basically the natural expansion for our corporate clients based here in Cairo, and this is where most of the trade exposure for the Egyptian customer is coming from.

Second, the go-to-market was completely different, because when you approach a country like Kenya, where it’s very cloudfriendly, very digitally savvy, very advanced from a payments perspective, we thought what kind of value we could bring to the market? So we brought cash flow lending and enhanced the quality of the payment processes with our global partners. By the end of the year, we will also introduce private and wealth management services.

We are ready to reposition Nairobi as our East Africa headquarters because of huge operational synergies. It’s not about expanding the footprint or putting another flag on the CIB global map; it is about amplifying Cairo and Nairobi’s synergies. We also set an exploration phase in Ethiopia and some other targets on the east coast of Africa, but what matters for us is the value creation.

Islam Zekry | Group Chief Finance and Operations Officer

Islam Zekry is the group chief finance and operations officer at CIB, serving as an Executive Board director and a member of CIB’s Executive Committee and CIB Kenya’s board. He joined CIB in 2004 and became its first chief data officer in 2016, leading data analytics and quant finance platforms.

GF: And where is the room for growth in Africa or elsewhere?

Zekry: We see strong growth potential across East Africa and tradelinked corridors in Northeast Africa. Beyond the continent, the Gulf markets and selected European hubs with strong diaspora links offer promising opportunities in remittances and digital cross-border services.

What differentiates CIB is our ability to combine deep banking expertise with local market insights, digitally enabled platforms tailored for premier banking services and underserved segments, and a client-centric model integrating transaction banking, advisory, and customer advanced and tailored solutions.

As an example, in Kenya, we’re enhancing SME lending through digital partnerships, leveraging the country’s well-developed ecosystem. We’re also advancing digital channels to scale access and deepen client engagement.

Al-Arab: Regional expansion is also about Egyptians outside of Egypt. How can we reach them and how can we facilitate their banking transactions? That’s something that is critical for our future banking services.

GF: Sustainable finance has been a true commitment for CIB. Tell us about the bank’s major achievements in this sector and CIB’s commitment to integrating sustainable finance across the board.

Amr El-Ganainy: CIB launched the first corporate green bond in Egypt, with a value of $100 million. This was a landmark transaction in Egypt and was important in supporting Egypt’s transition to a greener economy. Our aim is to play a pivotal role for all companies, and we are committed to helping the private sector transition to a more carbon-neutral future.

Zekry: At CIB, sustainable finance is not treated as a side initiative, it’s at the core of how we operate and grow.

When we partnered with the IFC to issue Egypt’s first green bond, that was virtually unheard of at the time. Today, that kind of financing is embedded in our business model. In fact, when we launched our five-year strategy just last week, ESG wasn’t a separate chapter, it was present throughout.

As we expand across Africa, a significant share of our growth will come from transitional finance, particularly in agricultural and underserved communities. We’re introducing specialized services in these areas: not just as a development goal, but because they make strong business sense.

Even internally, we’ve evolved how we assess performance. For example, our Green Asset Ratio is now a core part of our capital adequacy review, with a clear target to grow it by additional 1% to 2% annually. That’s how seriously we take it.

And to be clear, this is not just a corporate responsibility exercise. It’s part of our value creation strategy. In fact, transitional finance has been shown to deliver enhanced returns, often generating 50 to 100 basis points above conventional lending. So it’s both impactful and commercially sound.

Omar El-Husseiny | Chief Global Markets Executive

Omar El-Husseiny is the Chief Global Markets at CIB and a member of the Bank’s Executive Committee. As Chief Global Markets, he is responsible for key strategic areas including Financial Institutions, Debt Capital Markets, Treasury, Enterprise Governmental Relations, and Global Transaction Banking, ensuring alignment with the Bank’s broader growth agenda.

Mr. El-Husseiny spent his career at CIB, having joined after completing his Bachelor of Business Administration at the Faculty of Commerce at Cairo University in 2001. He holds an MBA in Banking and Finance from the Maastricht School of Management (MsM) and a Graduate School of Banking Diploma from the University of Wisconsin, Madison. In 2019, he completed the Corporate Finance & Credit Program at J.P. Morgan.

GF: Another item on top of the agenda, naturally, is digital banking and transformation. Walk us through CIB’s digital journey.

Rashwan Hammady: Our penetration of digital products across the base, whether in the consumer part, commercial banking, or SMEs or corporate banking, continues to grow over the past couple years. We’ve reached a stage where digital isn’t just about technology, it’s about understanding human needs and behavior. Our core focus now is reshaping our internal culture to understand and serve the next-generation consumer, those who are digitally native, community-led, and brand-critical. Gen Z and digital entrepreneurs will shape the next 20 years of financial services. Our job is to anticipate, not react to, how they live, earn, and make decisions. We’re embedding design thinking, real-time analytics, and personalization into our operating model. It’s less about digital “products” and more about building bespoke and lifestyle-driven experiences.

Omar El-Husseiny: Combining digital transformation and international expansion is no longer a luxury; as a financial service provider, it’s a must. This is where we see the bank moving forward. This is the only way we can expand locally and internationally, therefore, maximizing shareholder value. One takeaway from the past 50 years is how the bank continuously adapts to evolving trends and developments.

GF: How do you use digital tools to target regional expansion?

Al-Arab: For now, there are certain regulatory requirements that we are working on with the regulator, and when that is completed, it will allow us to provide services for individuals overseas. We want to do it seamlessly: simple, easy. The idea is that you are sitting on your sofa somewhere and you want to send money to your family. You don’t need to go to the bank. You want to pay your bills? You don’t need to travel. You don’t even need to make a phone call. It’s a new lifestyle. If you don’t keep developing, you will be left behind.

One thing I want to stress is that CIB is an Egyptian company. Apple is an American company. Where do you manufacture your product? That’s irrelevant. The idea that because we are an Egyptian company, we have to be local and not use the world to grow our market, is wrong. We have to use the world.

Hammady: We were one of the first players in the mobile wallet space. We’ve acquired more than 1.5 million customers via CIB’s mobile wallet. Our strategy now is more geared towards partnerships; we don’t need to build everything. So that maybe we’ll be the manufacturer of products and digital assets and a partner will be responsible for distribution, service, and access. True financial inclusion isn’t about opening accounts, it’s about changing behavior. We’ve realized that literacy and trust gaps in Egypt require a hybrid approach, yes, but more importantly, we need localized design experience. That’s why we’ve built a partnership model where we develop financial products while distribution and education are handled by partners with community reach.

This is how we unlock scale: regulatory-grade infrastructure with grassroots access. The WE partnership will bring banking to millions of new users. They have more than a thousand branches, and this partnership helps us promote financial inclusion across the country. We are expecting to launch that within the coming six to nine months, and that will cater to millions of customers, especially in non-urban communities, small cities, and villages across the country.

El-Husseiny: Egypt’s economy continues to rely heavily on cash transactions. This reliance places additional pressure on the money supply and constrains tax revenue collection, exacerbating inflation and expanding the budget deficit. Therefore, encouraging financial inclusion and digital transformation benefits CIB and the banking sector and is critical for border economic prosperity.

Rashwan Hammady is chief retail, commercial banking and financial inclusion executive at CIB. With over two decades of experience at the bank, he has spearheaded the launch of several landmark and innovative products and segment propositions, enhancing CIB’s ability to serve its growing customer base of over 3 million clients.

GF: You were mentioning partnerships. Are we talking partnerships with fintechs? With other players? How do you choose your partners?

Hammady: Our philosophy is simple: We build bespoke, compliant, scalable financial infrastructure and services; our partners provide complementary customer reach and engagement. Whether it’s telcoms, e-commerce platforms, or government entities, we choose collaborators who already command trust and attention across Egypt. This allows us to plug into ecosystems where our products become invisible, but indispensable. We’re now scaling this partner-led model not only in Egypt but also as part of our pan-African expansion.

Zekry: Our partnership model is quite unique in that it brings together three core pillars: data, digital, and design.

We’re data-driven, always seeking deeper insights into customer behavior and proactively working to enhance demand capacity. We’re digital by design, using technology to extend our reach and optimize cost-to-serve, especially in high-potential but underserved markets. And we focus strongly on experience design, because we believe that how customers engage with banking still matters, perhaps now more than ever.

When it comes to choosing partners—whether fintechs, infrastructure providers, or even talent networks—we look for alignment on those three dimensions.

We’re also deeply committed to building from the region, for the region. The team here is working tirelessly to reverse the brain drain—attracting top talent from Egypt and across Africa—to help build the banking operating system of tomorrow. We see partnerships as tactical and strategic enablers of long-term innovation.

GF: How is AI opening new doors?

Zekry: While AI has been around conceptually since the 1960s, what’s fundamentally different today is that we’re finally placing these technologies in a meaningful economic and operational context. We’re using AI and data analytics not just to automate, but to understand customer behavior, personalize services, and improve decision-making at scale.

At CIB, we’re investing heavily in building a group-wide data infrastructure: not only in Egypt, but across our African footprint. One clear opportunity lies in streamlining KYC and compliance processes. By creating an integrated data warehouse and sharing verified customer intelligence across our markets, we expect to reduce the cost to serve by 20%-30%. To put that in perspective, I recently came across a study citing EGP2 billion in redundancy costs from duplicative KYC efforts in London’s financial sector. Now imagine the potential savings if we could address that at a pan-African scale. The impact is enormous.

GF: What is the future of CIB?

El-Ganainy: Being Egypt’s largest publicly listed firm and the country’s leading private bank we set our strategy not only to respond to the opportunities emerging today, but to actively shape the Egypt of tomorrow.

We are the leaders in Egypt, and the future is expanding our leadership and investments across Africa and the Middle East.

Zekry: I see CIB evolving into a true business platform: not just in the digital sense, but as a regional and global enabler of investment, innovation, and growth.

We aspire to be a platform that attracts capital, connects businesses, and delivers a new standard of banking experiences—all while being proudly rooted in Egypt. Whether it’s manufacturers expanding from Egypt to the world or clients across Africa and beyond accessing seamless financial services, CIB will be there: facilitating, enabling, and leading.

The future of CIB is not only about being a great bank, but about becoming a trusted gateway to opportunity: for customers, investors, and the economies we serve.

El-Husseiny: I joined the bank 23 years ago, at a time when most of our work was conducted on paper. I’ve taken part in a remarkable transformation, from manual processes to desktop computers, and eventually to digital-first services. CIB will continue to be Egypt’s leading private-sector bank, and our ambition goes beyond national borders. What sets us apart is our ability to adapt to customers’ evolving needs. It’s not just about providing exceptional banking services; it’s about being a trusted financial advisor.

Integrating AI and technologies into our operations is essential. What endures is the customer experience. People will continue to need physical bank branches. CIB has significant room to grow in Egypt. During our strategy process, we asked our staff where they envision the bank in the next 5,10,20, or even 50 years.

The vast majority of our team shared a common vision: we have spent the past 50 years building a strong and successful institution in Egypt, and for the next 50 years, it’s time to expand beyond our borders. As we have developed a proven model, it is time to take that knowledge and expertise abroad, creating shared value through knowledge exchange. Expanding internationally aligns with diversity- a core element of our culture.

We’ve been very successful over the past 50 years in cultivating diversity in Egypt. It’s time to take that success global, where we believe we have the experience and strength to compete.

Hammady: Innovation, for us, is the art of institutional selfdisruption. Over the last decade, CIB has reinvented its business model multiple times: from a corporate-first bank to an inclusive, data-led, multi-segment powerhouse. We are now moving toward a model where the bank is a modular service provider, able to plug into ecosystems across borders. My belief is that our next evolution will see us not only as a bank but as a financial operating system for the region.

Al-Arab: The thing I tell the team and my colleagues is: We are as good as our dreams. You dream small, you remain small. You dream big, you will get there. Be ambitious.

The United States and the United Kingdom announced they have sanctioned a global scam operator based in Cambodia. File Photo by Sascha Steinbach/EPA

Oct. 14 (UPI) — Britain and the United States announced Tuesday that they have together sanctioned a transnational scam organization operating out of Cambodia.

The U.S. Department of Treasury Office of Foreign Assets Control announced it has imposed sweeping sanctions on 146 targets within the Prince Group transnational criminal organization, a Cambodia-based network led by Cambodian national Chen Zhi that operates a global criminal empire through online investment scams.

It also announced that the Financial Crimes Enforcement Network has finalized a rule under the USA Patriot Act to sever the Cambodia-based financial services conglomerate Huione Group from the U.S. financial system. “For years, Huione Group has laundered proceeds of virtual currency scams and heists on behalf of malicious cyber actors,” the press release said.

Covered financial institutions are now banned from opening or maintaining accounts for Huione Group, the Treasury Department said.

“The rapid rise of transnational fraud has cost American citizens billions of dollars, with life savings wiped out in minutes,” said Secretary of Treasury Scott Bessent in a statement. “Treasury is taking action to protect Americans by cracking down on foreign scammers. Working in close coordination with federal law enforcement and international partners like the United Kingdom, Treasury will continue to lead efforts to safeguard Americans from predatory criminals.”

In the U.K., a $16 million mansion owned by the Prince Group has been frozen by the government. Chen Zhi and his network have invested in the London property market, including the mansion, a $133 million office building and 17 apartments in the city. The freeze blocks them from profiting from these buildings.

The organization’s scam centers in Cambodia, Myanmar and other parts of Southeast Asia use fake job ads to lure foreign nationals to compounds or abandoned casinos where they are forced to carry out online fraud or face torture, the British press release said.

The scams often involve building online relationships to convince targets to invest increasingly large sums of money into fraudulent cryptocurrency schemes.

“These sanctions prove our determination to stop those who profit from this activity, hold offenders accountable, and keep dirty money out of the U.K.,” said Fraud Minister David Hanson in a statement. “Through our new, expanded fraud strategy and the upcoming Global Fraud Summit, we will go even further to disrupt corrupt networks and protect the public from shameless criminals.”

South Korea has faced a surge of kidnappings of its citizens in Cambodia. As of August, at least 330 cases were reported, according to data submitted to the National Assembly.

In June, Amnesty International said the Cambodian government has been “deliberately ignoring” human rights abuses including slavery, human trafficking, child labor and torture by gangs. It estimated that there were at least 53 scamming compounds in Cambodia.

In September, the Treasury Department sanctioned scam centers across Southeast Asia that the agency said stole $10 billion in 2024 from Americans via forced labor and violence.

An Iranian Revolutionary Guard jet boat saileed around a seized tanker in 2019. The U.S. Department of Treasury on Tuesday sanctioned people and businesses for “shadow banking” in support of Iran. File Photo by Hasan Shirvani/EPA

Sept. 16 (UPI) — The U.S. Department of Treasury announced Tuesday that it’s sanctioning two Iranian financial facilitators and more than a dozen Hong Kong- and United Arab Emirates-based people and entities for “shadow banking” in support of Iran.

The Treasury Department alleged that these people helped coordinate funds transfers, including from the sale of Iranian oil, that benefited the IRGC-Qods Force and Iran’s Ministry of Defense and Armed Forces Logistics, a press release said.

“Iranian entities rely on shadow banking networks to evade sanctions and move millions through the international financial system,” Under Secretary of the Treasury for Terrorism and Financial Intelligence John K. Hurley said in a statement. “Under President [Donald] Trump’s leadership, we will continue to disrupt these key financial streams that fund Iran’s weapons programs and malign activities in the Middle East and beyond.”

The department said that between 2023 and 2025, Iranian nationals Alireza Derakhshan and Arash Estaki Alivand worked to facilitate the purchase of over $100 million worth of cryptocurrency for oil sales for the Iranian government. Derakhshan and Alivand used a network of front companies in foreign jurisdictions to transfer the cryptocurrency funds, the release said.

The two are now considered “blocked,” meaning all their assets in the United States will be seized, and Americans and their companies can’t do business with them or their businesses.

Besides Derakhshan and Alivand, the department named several other people and businesses that are now blocked from American trade.

Shadow banking is credit intermediation by entities outside the regular banking system, performing bank-like functions, like maturity transformation and liquidity transformation, without the same strict regulatory oversight as traditional banks.

Britain, Germany and France sent a letter in late August to the United Nations Security Council saying they are starting the 30-day process of “snapback” of sanctions against Iran.

The snapback is used to re-impose sanctions on Iran in the event of “significant non-performance” of treaty commitments. The sanctions were suspended under the 2015 Joint Comprehensive Plan of Action nuclear deal.

For years, I kept my emergency fund in the same savings account I opened in high school. It was convenient. I didn’t have to think about it. But when I finally looked at what I was earning in interest, I wanted to kick myself.

Here’s the mistake: Leaving money in a traditional big-bank savings account that pays practically nothing.

The difference in dollars

Let’s do the math with $20,000 in savings:

A typical big-bank account pays around 0.01% APY. Over five years, that balance would earn you about $10 total.

Move that same $20,000 to a high-yield savings account paying 4.00% APY, and you’d earn about $4,330 in interest over five years.

That’s a gap of more than $4,300, just for clicking a few buttons.

Double that balance to $40,000, and you’re looking at nearly $8,700 in lost interest over the same period.

This isn’t about taking risks, it’s about not leaving money on the table.

Why people stick with bad accounts

The number one reason people stick with bad accounts is laziness. It feels easier to leave things where they are. Banks know this, and they’re counting on your indifference. But the truth is, switching to a high-yield savings account takes less than 10 minutes, and plenty of online banks have $0 minimums.

Where your money should go instead

With an HYSA, your money stays safe, liquid, and actually earns a return. It’s the simplest upgrade you can make to put your savings to work.

These accounts pay interest rates that are often 20 to 30 times higher than what big traditional banks offer. It really only does take minutes to open a new account.

One account offering a top-tier APY right now that can be opened with as little as $1 is the NexBank High-Yield Savings Account from Raisin. Earn a jaw-dropping 4.31% APY on your savings and open and operate your account fully online.

NexBank High-Yield Savings Account from Raisin

Member FDIC.

High APY

No monthly service fee

Unlimited ACH transfers

FDIC insured

Deposits and withdrawals can only be conducted via ACH transfer to/from an external bank account (limited to one linked external account)

No checking account offered through Raisin

No branch access; online only

With a 4.31% APY — one of the highest rates on any account we recommend — the NexBank High-Yield Savings Account from Raisin stands out for savers who want serious returns with minimal effort. You only need $1 to open, and FDIC insurance through NexBank keeps your money protected. Raisin’s secure online platform gives you 24/7 access to funds, and there’s even a cash bonus opportunity if you deposit at least $10,000 within 14 days — with higher deposits earning bigger rewards, up to $1,000. It’s a no-fuss, set-it-and-forget-it option for growing your savings at a top rate.

Don’t let laziness cost you

Five years from now, you could be thousands of dollars richer, or you could still be earning pennies because you didn’t bother to switch.

It’s one of the easiest financial wins out there, and you only have to do it once.

HomeMediaExpert PerspectivesTransforming member experience – How Intellect’s strategic acquisition can change the way Canadian credit union members bank

Today’s era of digital transformation enables nimble and innovative tech players to revamp traditional financial services. Intellect Design Arena Ltd. is doing exactly that for Canada’s credit unions – enhancing the industry with a digital banking platform that offers users exciting features and functionality, yet with continuity of service to ensure it remains robust and reliable.

In discussion with Global Finance, Rajesh Saxena, CEO of the consumer banking division of Intellect Design Arena Ltd., explains that the acquisition of Forge Digital Banking Platform from Central 1 is an exciting opportunity to deepen the firm’s footprint in Canada and in the credit union segment of the financial industry.

Intellect Design Arena has been in the Canada market for 12 years, and Central 1’s Forge platform offered a strategic opportunity to expand its fast-growing digital banking platform (eMACH.ai DEP) into the credit union space to enhance and modernise the way credit unions engage and deliver services to their members.

The acquisition of Forge, which served around 170 credit unions nationwide, has accelerated access to a key market segment for Intellect Design Arena. It’s a good fit for both Intellect and Forge customers, who will benefit from transitioning from a legacy technology platform to the very modern eMACH.ai DEP platform with state-of-the-art architecture across APIs, micro services, cloud native and AI. The new platform will enhance the user experience and provide new features and functions that can be used by retail and commercial customers in the credit union sector, such as quick onboarding, digital lending, budget tracking and personal finance management.

At the same time, continuity is key given the mission-critical nature of the platform for the credit unions. To ensure a seamless transition and uninterrupted service for platform customers, Intellect is retaining the Forge platform team, who understand the local market, regulatory matters, business practices, and the SaaS platform and technology. Intellect now offers the best of both worlds – a world class digital banking platform eMACH.ai DEP platform and the familiarity of the Forge team which credit unions already know and trust. With this combination, Intellect is offering a go-to-market in just 12 weeks.

Watch this video to get more insights about how Intellect Design Arena is transforming this segment of Canadian financial services while also creating bandwidth to expand more quickly in the domestic market as new opportunities arise.

Binance is partnering with Spain’s Banco Bilbao Vizcaya Argentaria (BBVA) to allow crypto customers to store their funds with the bank instead of keeping them directly on the crypto exchange, according to reporting by the Financial Times.

The move is aimed at rebuilding trust with investors after Binance was hit with a record fine from US regulators nearly two years ago.

Binance is the world’s largest cryptocurrency exchange by trading volume, and it handles billions of dollars in trades each day across hundreds of cryptocurrencies.

What does this mean for crypto?

BBVA, as a bank, will act as an “independent custodian” or a separate and trusted third party and ensure a greater level of safety when it comes to customers’ funds or assets that are traded through Binance.

As the second largest bank in Spain and praised for its innovation and sustainability, BBVA will act as a security guarantee, giving traders a reduced risk while encouraging them to invest in the high-returns crypto exchange.

By storing them with BBVA, if Binance runs into trouble, like being hacked, declaring bankruptcy or facing regulatory action, the funds would still be safe with BBVA.

Banks are much more closely regulated than crypto exchanges, so BBVA’s obligation to follow compliance rules should lead to more interest in crypto overall.

Essentially, the move is akin to putting your valuables in a safe or a secure bank, instead of being displayed in a storefront as they’re being bought and sold.

Binance trying to clean up its reputation

Binance, the world’s largest crypto exchange, got slammed in 2023 with a record $4.3 billion (€3.69bn) fine after US regulators accused it of not keeping checks on its trading floor.

US officials said Binance allowed shady funds to flow through its exchange and allegedly permitted laundered money to be used, helping its big clients dodge the rules.

Founder Changpeng ‘CZ’ Zhao stepped down and served four months in prison for failing to stop money laundering.

Now, with regulators watching its every move, Binance is trying to clean up its act and by partnering with Spain’s BBVA, hopes to prove it can play by the rules.

In Africa, companies across sectors and markets have an acute need for frictionless payments. Ongoing challenges in moving goods, managing import cycles and distributing products with certainty have made effective Payments, Working Capital and Trade Finance solutions a priority.

Businesses need speed, flexibility, visibility and control of their payment flows. In response, Standard Bank’s OneHub business platform harnesses Artificial Intelligence (AI), machine learning, Cloud-based computing and application programming interfaces (APIs) to integrate payment features within client Apps, systems and architecture.

“Leveraging our deep insights and knowledge about our clients and the sectors and industries within which they operate, we spend a lot of time innovating for bespoke Payments, Working Capital and Trade Finance solutions,” said Crosby.

Giving customers what they need

The OneHub business platform provides more than what Standard Bank alone can deliver. Not only does it enable access to all the bank’s solutions and the bank’s partners’ solutions, it also offers important features that help clients with their Working Capital and Payment cycles.

“We partner with fintechs and other organisations to deliver holistic, best-in-class solutions,” said Crosby. “We find that works very well in staying ahead and being competitive.

This approach reflects his view that in such a competitive landscape, the bank’s strategy should be shaped by client engagement and knowing the customer, which are key components to innovation.

Standard Bank is well-positioned for this, with a footprint in many markets throughout the continent. “We understand the risk very well. We understand the logistics and various mechanisms of the underlying Working Capital cycles. And we play a strong role in financing,” Crosby explained.

Swift and smooth

Digital innovation has become key to complementing this physical presence. For example, it has helped Standard Bank deliver bespoke Payment solutions for the healthcare industry in Ghana to ports authorities in Kenya and across East Africa.

More specifically, the technology architecture and systems the bank uses, play a critical role in creating frictionless Payment solutions that are fast, efficient, reliable and secure – essentials for Transaction Banking.

“We leverage the Cloud because the hyperscalers give us significant computing power as well as other out-of-the-box solutions. When appropriately deployed, it’s a strategy that lowers operating costs, requiring only the purchase of Cloud capacity.”

Crosby Mkhwanazi, Head of Transaction Banking at Standard Bank

Modularised services have also proved effective in keeping the technology architecture dynamic, so the bank can innovate quickly and deliver the right solutions.

Further, Mkhwanazi points to connectivity via APIs and automation – at both the front- and back-end – as other core components for frictionless Payments. This applies either through pre-populating information for efficient web-based Payments or by integrating directly into a client’s system. “That enables clients to lower costs and to achieve near real-time Payments, to the extent possible within the bounds of applicable regulations.”

New partners, new solutions

Understanding what clients need also informs Standard Bank’s future digital transformation agenda within Transaction Banking, driving its innovation cycle.

As a result, solutions for telecom companies are on the horizon, for example. “We are working with telcos around accessing banking infrastructure to deliver Payments to allow for better access into the areas where perhaps, as banks, we haven’t reached before,” said Crosby.

Remittances have swiftly become a cornerstone of foreign currency inflows for many African nations. For Standard Bank, this represents a pivotal opportunity by: reimagining the remittance experience, Standard Bank aims to empower communities and drive broader economic inclusion across the continent. “Not only is it about enhancing accessibility and expanding distribution, but also about ensuring seamless foreign exchange availability and reducing the overall cost of sending money home.” Crosby explained.

Such an ambition reinforces Standard Bank’s broader focus: being a trusted partner in a continent where it has pioneered change for over 160 years, crafting bespoke agile, relevant and market-leading products and services, tailored for clients’ growth and success.

Banco Sabadell shareholders unanimously backed the sale of its UK subsidiary TSB to Banco Santander at an extraordinary meeting on Wednesday.

The deal, valued at a minimum of £2.65 billion (around €3.05 billion), represents a notable gain against the acquisition price. In 2015, Sabadell bought TSB for £1.7 billion, equivalent today to around €1.95 billion.

The approval of this divestment comes at a particularly sensitive time, as the Catalan bank is the target of a hostile takeover bid by BBVA. For this reason, the board of directors needed to obtain the explicit approval of the shareholders before closing any strategic operation of this calibre.

TSB, focused on the UK mortgage market, has been one of the key assets in Sabadell’s defence against the proposed hostile takeover.

The sale of TSB is part of Sabadell’s strategy to strengthen its independent position in the face of the takeover bid launched by BBVA. By divesting TSB, the Catalan bank seeks to reduce its international exposure, simplify its structure and generate liquidity to remunerate its shareholders.

The plan includes an extraordinary dividend of €2.5 billion in 2026, which must be approved this afternoon, plus additional ordinary payments.

This increases the attractiveness of maintaining the bank as an autonomous entity and complicates BBVA’s takeover attempt.

The proposed acquisition has sparked political controversy in Spain and in Brussels. Last month, the European Commission sent Spain a legal warning after the government sought to impose conditions on the merger.

Corporate and investment banking revenues in the Gulf are burgeoning as lenders underwrite the region’s economic transformation.

Lenders like what they are hearing from Gulf region businesses. Corporate and investment banking (CIB), which already accounted for more than half of total banking revenues in the Gulf Cooperation Council (GCC), is expanding at an annual rate of 14%, more than twice the regional average, according to a recent McKinsey study. Lenders expect CIB revenues to reach the $100 billion mark by 2030 as the region deepens its economic transformation.

“All GCC nations are actively working to diversify their economies away from hydrocarbon dependence, which will unlock significant growth opportunities in all sectors,” says Wissam Haddad, CEO of Riyadh-based SICO Capital, which is developing products and services geared toward emerging technologies.

From Saudi Arabia’s Vision 2030 blueprint to the United Arab Emirates’ digital and green ambitions, Gulf countries have embarked on multi-billion-dollar quests to reshape their economies. Countless initiatives across the board are boosting demand for complex financing solutions and banking services. “As governments prioritize large-scale infrastructure, energy transition, and technology-led growth, financial institutions are playing an increasingly strategic role,” says Abbas Husain, global head of Infrastructure and Development Finance at Standard Chartered. “In this environment, financing needs are becoming more sophisticated. There is growing interest in integrated capital solutions that combine bank lending with broader access to capital.” The Gulf ’s CIB client base is broad: from sovereign wealth funds and government-related entities to multinational firms entering the region, high-net-worth individuals, institutional investors, publicly listed companies, and small to midsized enterprises.

“In this environment, financing needs are becoming more sophisticated.”

Abbas Husain, Global Head of Infrastructure and Development Finance, Standard Chartered

“Many are deeply involved in executing national transformation agendas and are at the forefront of innovation, sustainability, and infrastructure development,” Husain notes. “What they increasingly have in common is the need for integrated, forward-looking financial solutions that support complex, multi-market strategies. This extends across debt financing, risk management, and strategic advisory, often with a strong cross-border dimension.”

Capital Markets

As the GCC economies evolve, so too are their capital markets, spanning debt issuance, equity offerings, and M&A, all of which are contributing to the sharp rise in CIB revenues. In the first quarter of 2025, M&A activity surged 66%, to reach $46 billion over 225 transactions, reports Ernst & Young, with the UAE accounting for more than half of all announced deals. The UAE and Saudi Arabian IPO markets have recorded steady growth of 10% to 15% year-on-year over the past decade.

Karim Shoeib, Group CEO, Investment Banking, Al Ramz

“The surge in IPO activity, particularly in the UAE, is creating significant momentum,” says Karim Shoeib, group CEO, Investment Banking, at Al Ramz, a Dubai-based public joint-stock company. “Government-led privatizations and family business listings are expanding the investable universe and generating new opportunities for both institutional and retail clients.” Although the UAE and Saudi Arabia dominate market activity, he advises that investors keep an eye on other countries including Oman and Bahrain, where Al Ramz was recently licensed.

With family-owned businesses making up much of the private sector—around 90% in the UAE and 60% in Saudi Arabia—family listings look to be an important catalyst for capital market activity. The region is on the brink of an unprecedented generational wealth transfer; by 2030, over $1 trillion in assets is forecast to change hands, opening rare opportunities for investors to become shareholders of some of the region’s crown jewels.

A high-profile example is Emirati retail giant Majid Al Futtaim. Following the founder’s death without a will in 2021, years of internal disputes may culminate in an IPO.

“The region is witnessing an increasing number of company listings, strategic projects, a growing preference for more advanced and hybrid debt products, and continued consolidation,” says Haddad, “particularly in fragmented sectors such as hospitality and insurance. Many GCC countries have solid long-term strategic visions that emphasize sectoral diversification and privatization, which we believe will continue to drive robust demand for CIB services.”

Attracting Global Banks

Global financial institutions are ramping up their presence in the GCC. BNY Mellon recently established its regional headquarters in Riyadh, following Goldman Sachs and Citigroup, which were licensed last year.

US private equity firm I Squared Capital has committed $1 billion to Saudi infrastructure projects while Azura, a Monaco-based wealth management firm overseeing $5 billion in assets, is relocating its operations to Abu Dhabi. UBS also is set to open an office in the UAE capital and JPMorgan plans to hire over 100 additional staff to strengthen its already sizable Middle East presence.

“This is healthy and a reflection of the strong fundamentals and future potential of local markets,” Shoeib notes. “We view this development as a natural part of a maturing financial ecosys- tem that continues to evolve in both scale and sophistication.”

Regional banks retain key advantages, including deep client relationships, intimate knowledge of local regulatory environ- ments, and cultural proximity in areas like Islamic finance, but global entrants bring expansive balance sheets and often more advanced digital infrastructure.

Although the presence of global banks intensifies competition, “it also raises industry standards, introduces global best practices, and attracts deeper pools of capital to the region,” notes Haddad. “In many ways, international interest complements our efforts,” he adds, “broadening market participation and expanding the ecosystem rather than threatening it.”

Still, success for local players will demand more than just local familiarity and competitive products.

“To truly succeed in this environment, it is no longer sufficient to be just a source of liquidity,” says Husain, citing his clients’ interest in sustainable finance, digital transformation, and long-term capital structuring. “What differentiates institutions is the ability to offer holistic solutions grounded in local understanding and global reach. Deep relationships, consistent presence, and a track record of delivery are critical. What clients value is a strategic partner that can support them across their full lifecycle, from advisory through to execution and long-term financing.”

Challenges Ahead

Despite strong momentum, the GCC’s CIB sector faces significant headwinds. Geopolitical tensions, oil price volatility, new corporate tax regimes, and rising interest rates weigh on the cost of capital, dampening investor appetite and affecting deal execution timelines.

“Broader geopolitical tensions and global economic shifts, such as inflationary pressures and interest rate cycles, continue to shape investor sentiment across the region,” says Shoeib. “With GCC currencies pegged to the US dollar, navigating these macroeconomic dynamics requires agility and a steady focus on long-term value creation.”

Another structural challenge concerns the availability of qualified human capital and the sector’s ability to keep pace with rapid technological innovation, including generative AI. “The future of corporate and investment banking in the GCC will be shaped by those who can align innovation with execution and combine global connectivity with a strong understanding of regional ambition,” says Husain.

“Financial institutions that can operate across jurisdictions, connect global capital to local opportunity, and provide clarity in a complex landscape are well positioned to lead.” Concurrently, the GCC’s rising capital needs are putting pressure on liquidity. In most countries, credit demand is now outpacing deposit growth, driving loan-to-deposit ratios to historic highs. In Saudi Arabia, the ratio exceeds 100%, with private-sector lending projected to grow by 12% to 14% annually, while deposits are expected to rise by only 8% to 10%. This dynamic creates both opportunities and risks for regional lenders.

“CIBs must overcome funding shortages with record-high loan-to-deposit ratios—nearing or surpassing 100% in half of all GCC countries—which create potential liquidity constraints,” the recent McKinsey study concludes. “In addition, lower interest rates, with more cuts expected this year, are putting pressure on returns, given that approximately 85% of GCC banks’ income is based on interest.”

To maintain growth and profitability, Gulf-based banks will need to adapt. “Success requires banks to consider adjustments that may help them capture opportunities, remain competitive, and maintain recent momentum,” McKinsey argues, suggesting that local players focus on improving cost efficiency, diversify their loan portfolios, deepen their footprint in capital markets and trading, and expand transaction banking and foreign exchange services.

Abstract: Amidst the challenges of digital transformation in developing countries, M-Pesa emerges as a local innovation that successfully empowers communities through mobile phone-based financial services. Launched in Kenya in 2007, M-Pesa expands access to financial services, drives regional economic integration, and opens up new opportunities for small businesses. While offering great potential to expand global financial inclusion, M-Pesa faces challenges such as global fintech competition, digital security risks, and regulatory misalignment between countries. To maintain its relevance, M-Pesa must continue to innovate while remaining rooted in local needs and the principle of inclusivity.

In the midst of global digital transformation, many developing countries face major challenges in accessing and utilizing technology to drive economic growth. Limited infrastructure, low levels of digital literacy, and unequal access to financial services are major obstacles in this process. Despite these challenges, local innovations have emerged that address the specific needs of their communities. One example is M-Pesa, a mobile phone-based financial service introduced in Kenya in 2007. From a simple need for a safe and fast money transfer system in areas with limited access to banks, M-Pesa has grown into a global phenomenon that is changing the face of local and regional economies.

M-Pesa not only offers easy financial transactions for individuals but also opens access to microcredit, insurance, and business payment services (Kagan, 2023). Thus, M-Pesa shows how innovation based on local needs can be a catalyst for inclusive digital transformation. The presence of M-Pesa contributes to economic integration, both at the national level and between countries in the East African region. This service proves that digital solutions designed with local context in mind can address structural challenges, accelerate economic growth, and improve social stability. Through the design of M-Pesa, it can be understood that empowering local innovation is essential in driving sustainable digital transformation for local needs while strengthening economic connectivity in an increasingly digitized world.

M-Pesa: Local Innovation in the Digital Age

In the discourse of digital transformation in developing countries, M-Pesa has become a hot topic of discussion as one of the successful models of innovation based on local needs. Understanding the significance of M-Pesa needs to be seen through the process of formation, development dynamics, and the implications of this innovation on socio-economic structures. M-Pesa emerged in 2007 in Kenya, developed by Safaricom—a subsidiary of Vodafone—as an answer to the lack of access to formal banking services (Wachira & Njuguna, 2023). At the time, the majority of Kenyans, especially in rural areas, did not have bank accounts. This created a need for a simple, cheap, and widely accessible financial system. Herein lies the main strength of M-Pesa, which does not seek to replicate Western banking systems but rather builds solutions that fit local realities. This shows that successful innovation in the digital age is not a mere transplant of global technology but rather a smart contextual adaptation.

The rapid development of M-Pesa brings features from an SMS-based money transfer service to a financial ecosystem that includes bill payments, goods purchases, savings, microloans, and insurance (Schachter, 2018). This transformation not only expands financial services but also disrupts the traditional role of banks, which has been exclusive to the upper middle class. Amidst the praise for M-Pesa’s financial inclusion, there is also criticism about the unequal access to technology. Although based on a relatively simple SMS, the service still requires ownership of a mobile phone and a stable telecommunications network, two things that are unevenly distributed across Kenya and East Africa. This shows that digital innovation, if not accompanied by investment in basic infrastructure, can deepen the gap between those who are connected and those who are left behind. M-Pesa is proof that local innovation can be a lever for structural change. In the current context of globalization, the challenge ahead is to ensure that digital transformation based on local innovation is not just a tool of market integration but also an instrument of sustainable social empowerment.

M-Pesa as an Instrument of Economic Integration

In the era of economic globalization, integration is no longer only determined by the relationship between large countries but also by the ability of lower society groups to connect directly through technology. In this context, M-Pesa emerges as an innovative instrument that accelerates economic integration, especially in the Global South, which has often been marginalized in global finance. M-Pesa accelerates cross-border transactions by providing a simple and fast money transfer solution, even without requiring access to a traditional bank. Services such as Mobile Money Transfer (MMT) enable migrant workers in the East African region to send money to their families at a much lower cost and in a much faster time than conventional financial institutions (Safaricom, 2023).

M-Pesa also opens up opportunities for small businesses to connect with a wider market. With easily accessible digital payment services, micro-merchants can conduct transactions across regions without having to rely on expensive banking infrastructure. This strengthens the position of small businesses as important actors in the global supply chain while encouraging more inclusive, people-based economic growth. Innovations in M-Pesa are able to overcome classic barriers, such as the inability to access credit. With M-Pesa, there is an increase in regional financial connectivity, particularly in East Africa. With widespread adoption in Kenya, Albania, the Democratic Republic of Congo, Egypt, Ghana, India, Lesotho, Mozambique, Romania, and Tanzania, M-Pesa creates a kind of digitally connected regional financial ecosystem (Owigar, 2017). This reduces both domestic and cross-border transaction costs and ultimately increases the efficiency of the region’s economy. In the long term, M-Pesa shows potential to accelerate the formation of a more integrated and competitive regional market.

Opportunities and Challenges of M-Pesa in the Future

Given its multiple successes in revolutionizing financial services in East Africa, M-Pesa has a great opportunity to expand its role in the global digital economy. M-Pesa’s success cannot rely solely on the old model. Continuous innovation and adaptation to new technology trends are key to sustaining M-Pesa. Despite its success in Kenya and several other countries, many other regions in the Global South still face similar problems. By adapting its approach to local characteristics, M-Pesa has the potential to become an inclusive financial platform that transcends regional boundaries and becomes a global player in digital financial inclusion.

While M-Pesa offers great opportunities to expand financial inclusion and strengthen economic integration, it is undeniable that the platform also faces serious challenges that could hinder or even reverse its achievements. When M-Pesa is not managed properly, its success today can become a source of vulnerability in the future. One of the main challenges is the increasing competition from global financial technology companies. With the entry of big players like PayPal and various local fintech startups, the digital financial services market has become increasingly competitive. When M-Pesa fails to innovate or expand services according to the needs of the new digital generation, it will be very risky to be abandoned, especially by the younger generation, who are more sensitive to faster and more flexible technology options. In addition, digital security issues are a threat that cannot be ignored. The growing volume of transactions through M-Pesa makes the platform a potential target for cyberattacks, data theft, and digital fraud. In a context where many users do not yet have strong digital literacy, a security breach can destroy the trust that has been built over the years and worsen the stability of the service.

As M-Pesa expands, differences in legal frameworks and consumer protection between countries are a major obstacle. If there is no alignment in terms of policies, users in certain countries may become more vulnerable to data abuse. In facing the future, M-Pesa must stay true to its core principle of addressing the needs of the community through simple, affordable, and inclusive technology. Consideration of digital risk resilience, the courage to compete fairly, and a commitment to maintaining economic justice in the midst of an increasingly complex digital ecosystem need to be improved. Innovation created from local needs is the key for M-Pesa to survive, not only as a transaction tool but also as the foundation for a more equitable and sustainable digital economy.

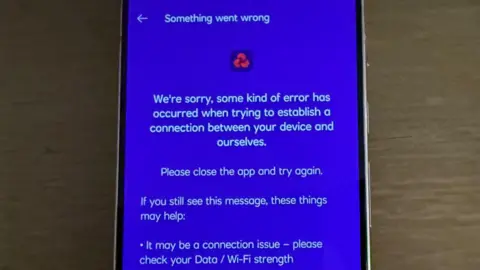

NatWest has apologised after customers were left unable to use its mobile banking app in the UK, preventing some from accessing their bank accounts.

More than 3,000 people have reported problems on outage-checking site Downdetector since the issues first emerged at 0910 GMT.

The firm said on its service status website that its online banking service was still working normally – though this has been disputed by some customers. Card payments are unaffected.

“We are aware that customers are experiencing difficulties accessing the NatWest mobile banking app this morning,” a NatWest spokesperson told the BBC.

“We’re really sorry about this and working to fix it as quickly as possible.”

BBC/NatWest

People saw this message when trying to use online banking on Friday

Customers have taken to social media to complain about the impact the IT failure is having on them.

One person said they had to “put back my shopping because of it”, while another said they were “waiting to go shopping” but couldn’t transfer money to do so.

NatWest has advised customers on social media that it has “no timeframe” for a fix, but said its team is “working hard” to resolve it.

Customers are being advised to access their accounts in other ways if they can – such as through online banking.

However, some people have reported problems with NatWest’s online service too, with one sharing an error message which they said was displayed when they tried to make a payment.

Others have expressed frustration with the bank’s response, with one saying it was “disgraceful” there was no timeframe, while another called it “very poor service“.

“What I don’t get is the bank closes loads of branches ‘to save money’ and forcing people to rely on the app and online banking… but clearly hasn’t invested in a system that works properly,” one angry customer said.

A recurring problem

This is the latest in a long line of banking outages.

According to a report in March, nine major banks and building societies have had around 803 hours – the equivalent of 33 days – of tech outages since 2023.

Inconvenient for customers, outages come at a cost to the banks, too.

The Commons Treasury Committee found Barclays could face compensation payments of £12.5m over outages since 2023.

Over the same period, Natwest has paid £348,000, HSBC has paid £232,697, and Lloyds has paid £160,000.

In April 2025, a familiar tension resurfaced on the global trade stage. The United States, through its 2025 National Trade Estimate (NTE) report, criticized Indonesia’s national QR payment system, QRIS (Quick Response Code Indonesian Standard), and its domestic payment network GPN for allegedly restricting access to foreign firms like Visa and Mastercard. This came at a politically sensitive moment: just as the U.S. announced a 32% reciprocal tariff on Indonesian goods—a move temporarily suspended by the Trump administration for 90 days starting April 9, 2025 (Office of the United States Trade Representative, 2025).

At the center of this trade dispute is a quiet yet transformative success story: Indonesia’s regulator-led push to unify, simplify, and democratize digital payments. While the U.S. frames QRIS as protectionist, many in the Global South see it differently. They see it as sovereignty in code form—a model where innovation doesn’t only emerge from Silicon Valley, but from sovereign policy designed with inclusion, affordability, and national interoperability at its core.

QRIS, launched in 2019 by Bank Indonesia, now boasts over 50 million users and 32 million merchants—92% of whom are MSMEs. Its impact is visible not only in transaction volumes but in the radical reshaping of Indonesia’s informal economy. Through a single interoperable QR standard, QRIS reduced barriers for small vendors, brought millions into the financial system, and enabled digital literacy at scale (Bank Indonesia, 2025; QRIS Interactive, 2025). Features like QRIS TUNTAS and QRIS Antarnegara extend its utility to ATM-like services and cross-border payments with neighboring ASEAN countries (“Riset Sukses QRIS Indonesia”, 2025).

Today, QRIS is accepted not only across Indonesia but also in partner countries including Malaysia, Thailand, Singapore, the Philippines, Vietnam, Laos, Brunei Darussalam, Japan, and South Korea. These regional agreements strengthen QRIS as a payment bridge across Asia, facilitating tourism, trade, and local currency settlements.

In contrast to the U.S. critique, QRIS represents a strategic choice to design for dignity rather than dependence. The lesson here is not anti-global—it is about asserting a model of digital governance where financial infrastructure, when governed wisely, can serve local resilience while remaining open to fair, mutually beneficial cooperation.

In fact, the Indonesian government has consistently expressed openness to global firms—including Visa and Mastercard—being part of the QRIS ecosystem. This reflects a collaborative model that embraces interoperability and innovation, as long as it aligns with the public interest and meets the nation’s inclusive development goals. The QRIS story shows that sovereignty and openness can coexist, and that digital payment systems can be built on principles of both equity and cooperation.

For the Global South, Indonesia’s QRIS success offers five strategic lessons:

Lead with Policy, Not Platforms: Innovation doesn’t have to be outsourced. Sovereign institutions can shape markets when they prioritize public interest over private monopolies.

Standardize Early to Scale Fast: Mandating one interoperable code simplified adoption, removed friction, and prevented early-stage fragmentation.

Subsidize the Small: By waiving merchant fees for low-value transactions, QRIS made itself indispensable to micro-enterprises.

Adaptation Is Innovation: QRIS kept evolving, integrating ATM functions, enabling cross-border payments, and responding to real-world behaviors.

Sovereignty Is Not Isolation: Building domestic rails doesn’t mean closing doors. It means entering global trade with stronger footing.

Data Inclusion Enables Policy Precision: By digitizing informal transactions, QRIS generates more accurate data flows across sectors. This improves transparency, tracks real-time economic activity—especially in the informal sector—and strengthens the foundation for evidence-based policymaking.

This trajectory stands in marked contrast to two other Global South giants: India and China.

In India, the Unified Payments Interface (UPI), launched by the National Payments Corporation of India (NPCI), created a real-time payment system that integrates bank accounts across providers. Its success stems from similar government-led standardization, free or minimal transaction fees, and integration into flagship digital initiatives. UPI has become central to India’s financial inclusion drive, particularly among underbanked rural populations (IJFMR, 2025; NPCI, 2025).

Meanwhile in China, QR payment adoption exploded via a different route: commercial super-apps. Alipay and WeChat Pay dominated over 93% of the market by 2019, offering frictionless experiences integrated into social media and e-commerce platforms. However, their dominance led to walled gardens, until government intervention in 2017 required all non-bank QR transactions to be cleared through a centralized clearinghouse known as Wanglian (REI Journal, 2025; Toucanus Blog, 2025).

This comparison reveals not just different models, but different philosophies:

Indonesia and India: regulator-first, interoperability by design, competition fostered between diverse providers.

China: market-first, innovation by dominance, regulation applied retroactively to rein in systemic risk.

As financial digitalization accelerates worldwide, the choice is no longer between Silicon Valley or state control. The new frontier lies in hybrid governance models rooted in public interest, where local needs shape global partnerships. QRIS is not perfect, but it proves a crucial point: the Global South can chart its own fintech path—inclusive, interoperable, and sovereign—while still welcoming collaboration.

The key is to ensure that such collaborations are not extractive, but mutual. Interoperability with foreign systems can and should be pursued, as long as it doesn’t compromise local resilience or digital sovereignty. Rather than rejecting international cooperation, Indonesia’s QRIS shows how it can be done on equal terms—answering local priorities first.

For many nations in the Global South, digital public infrastructure like QRIS offers not just a financial tool, but a social mission. It is directly aligned with ESG and SDG narratives—advancing financial inclusion, reducing poverty, and promoting economic equity at the last mile. As such, future cooperation—whether with international firms or multilateral agencies—must serve this broader vision: technology as a lever for dignity, not dependency.

And sometimes, that path starts with a simple square of black-and-white code.

Digital banking usage has surged across Europe in the last decade, as the way we bank has been transformed dramatically. The percentage of EU citizens using online banking in the last decade has risen from 42% to 67%, in Spain that number was closer to 75% in 20241.

CaixaBank’s growth in digital channels reflects these trends. The Bank is, by some distance, the leading digital bank in Spain. It has the largest digital customer base, which in 2024 grew from 11.5 million customers to 12.1 million.

The bank’s digital lifestyle platform for younger customers, imagin, has surpassed 3.5 million banking customers – growth of 11% on the previous year, with almost half of CaixaBank’s new customers in the last year being recruited through imagin. Customer loyalty is increasing, with 50% of adults directly depositing their salary into the bank.

At the app user level, which includes all those who do not make financial operations but make use of the imagin app’s non-banking services, the number of imaginers now exceeds 4.5 million.

This data reinforces imagin’s position as a leading neobank and consolidates its position as a leader among young people. According to GfK statistics, imagin has a 48% market share among the main neobanks and fintechs in the 18-34-year-old segment in Spain.

In addition to increasing the number of new users, the platform has also managed to strengthen the loyalty of imaginers. In terms of activity volume, the application has an average of 60 million monthly visits and more than 11 million transactions per month are conducted through Bizum, 15% more than in 2023.

Imagin complemented its portfolio in 2024 with new products such as a fee-free debit card for use abroad, and financing and investment options, making it the only neobank with a complete banking offer tailored to a young and 100% digital audience.

The bank’s hybrid remote assistance service InTouch has more than 3.3 million users. InTouch is a new relationship model that combines remote communication tools (video call, voice call, email, WhatsApp, etc.), with the relationship of trust provided by an expert manager.

CaixaBank is also the leader in traditional website channels: this includes CaixaBankNow, the reference application for CaixaBank customers, and imagin.

Overall, CaixaBank leads in Spanish digital banking with a 45.4% penetration on digital banking users in Spain at year-end 2024.

Spain’s drive for digital

The bank’s digital transformation is to some extent a mirror for Spain’s early adaptation to an increasingly digital and competitive global landscape.

In the latest State of the Digital Decade report outlined by the European Union, Spain stood out thanks to two main strengths, the large number of citizens with basic digital skills (66.2%), compared to the European average (55.6%), and the progress in the use of artificial intelligence by companies (9.2 %) compared to 8% in Europe.

CaixaBank’s recently launched Strategic Plan for 2025-2027 outlines an ambitious vision for the future, fully in line with the country’s determination to maintain leadership in digital innovation.

Among many commitments, the plan earmarks €5 billion in investment towards AI, cloud computing, and automation. This initiative, known as the Cosmos plan, aims to enhance operational efficiency, develop new customer-centric digital services, and strengthen the bank’s technological infrastructure.

Investing in Innovation for the Future

One of the most transformative aspects of CaixaBank’s digital strategy is its integration of AI into customer interactions. AI-powered tools facilitate automated financial recommendations, conversational banking assistants, and enhanced fraud detection, streamlining both user experience and internal operations.

AI-powered tools will allow for automated financial recommendations, conversational banking assistants, and self-service options for customers. The technology will also streamline internal processes, reducing administrative burdens on bank employees while improving decision-making and fraud detection.

A key trend in this shift is the growing emphasis on technological talent, and the concern around this topic is highlighted in The Global Risks Report 2025, published by the World Economic Forum (WEF), where the shortage of skilled talent stands out as one of the key risks businesses must navigate this year. As digital banking evolves, institutions are increasingly expanding their technology hubs to attract specialists in AI, cybersecurity, and cloud computing.

Spain has again emerged as a leader in this space, with financial institutions investing heavily in developing digital capabilities. Technology jobs are growing faster in Spain than anywhere else in the world, according to the Equinix 2023 Global Tech Trends Survey.

CaixaBank, for example, has outlined an ambitious plan to strengthen its technological infrastructure while expanding its tech subsidiary, CaixaBank Tech, which is undergoing significant expansion with a goal to reach a total of 2,000 employees within the next three years. The offices in Barcelona, Madrid, and the new centre in Seville will become talent-attracting technological hubs.

Enhancing Digital and Mobile Banking Services

Digitalisation is not just about cutting-edge AI. The rise of mobile-first banking is reshaping the financial landscape, as consumers increasingly expect seamless, secure, and accessible digital services. Across the industry, banks are investing in mobile platforms to meet the needs of a generation that prefers managing finances on the go.

67% of bank account holders in Spain handle banking via mobile devices, this trend has driven significant innovation, from digital-only banking models to flexible payment solutions that integrate with everyday mobile experiences. And it was way back in 2016 that CaixaBank’s imagin service became the first in the world where all transactions are performed using only apps for mobile phones or social media.

Today, according to data from the bank, more than 30% of in-person purchases made in Spain with CaixaBank cards are now being done via mobile phones. The bank has around 4.4 million customers with cards linked to mobile devices, figures that are on the rise, with more than 800 million transactions in the last 12 months.

Collaboration is key

Partnerships between banks and tech companies are also shaping the next generation of digital transactions. In line with this, and as a further demonstration of the bank’s firm commitment to improving the customer experience, CaixaBank, through CaixaBank Payments & Consumer, has signed a pioneering agreement with Apple.

As a result of this partnership, CaixaBank customers with iOS 18 and iPadOS18 will soon have the option to pay in full or spread the cost over multiple months directly at the point of purchase when paying with their CaixaBank cards in Apple Pay. Customers that decide to choose this option will have the choice to do so when shopping online using Apple Pay and in-app on iPhone, iPad and Apple Watch.

This new functionality will allow customers to see payment options available to them, understand cost including any interest, and choose how they’d like to pay before completing their purchase.

Meeting the needs of a digital-first generation

As digital banking evolves, financial institutions are placing greater emphasis on automation and cybersecurity to enhance efficiency and protect customers. AI-driven analytics are enabling banks to deliver hyper-personalised financial solutions, helping individuals make more informed decisions. At the same time, advanced security frameworks, including real-time fraud detection and AI-powered risk management, are becoming critical in safeguarding digital transactions.

In Spain, financial institutions have been recognised for their strong commitment to digital security. Many banks have implemented next-generation fraud detection systems and encryption technologies to safeguard transactions. CaixaBank, for example, has been acknowledged for its advanced cybersecurity measures, reinforcing the industry’s broader push to ensure secure digital banking experiences.

As Spain’s financial sector continues to embrace digital innovation, its commitment to technology, security, and inclusivity will position it as a leader in shaping the future of banking in an increasingly digital world.