AMD’s shares surge on deal to supply AI chips to OpenAI | Technology News

The deal also gives the ChatGPT creator the option to buy upto 10 percent of AMD.

Published On 6 Oct 2025

United States chipmaker AMD will supply artificial intelligence chips to OpenAI in a multi-year deal that would bring in tens of billions of dollars in annual revenue and give the ChatGPT creator the option to buy up to roughly 10 percent of the company.

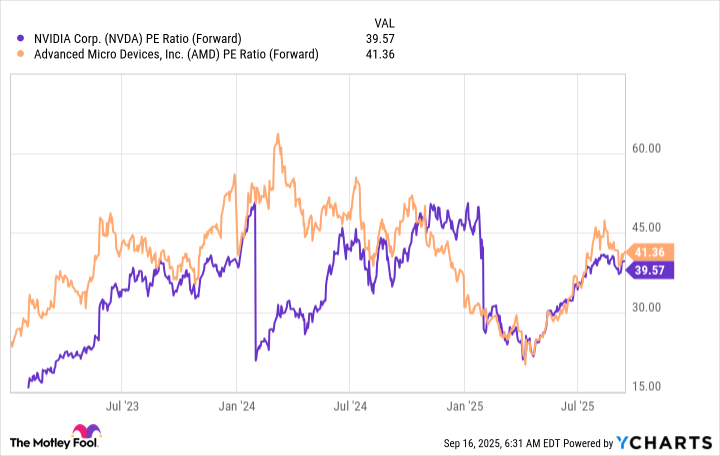

Shares of the chipmaker surged more than 34 percent on Monday when the deal was announced, putting them on track for their biggest one-day gain in more than nine years and adding roughly $80bn to the company’s market value.

Recommended Stories

list of 4 itemsend of list

The deal, latest in a string of investment commitments, underscores OpenAI and the broader AI industry’s voracious appetite for computing power as companies race towards developing AI technology that meets or exceeds human intelligence.

“We view this deal as certainly transformative, not just for AMD, but for the dynamics of the industry,” AMD executive vice president Forrest Norrod told the Reuters news agency.

Deal helps ‘validate technology’

The agreement closely ties the startup at the centre of the AI boom to AMD, one of the strongest rivals of Nvidia, which recently agreed to make substantial investments in OpenAI.

Analysts said it was a significant vote of confidence in AMD’s AI chips and software but is unlikely to dent Nvidia’s dominance, as the market leader continues to sell every AI chip it can make.

AMD executives expect the deal to net tens of billions of dollars in annual revenue. Because of the ripple affect of the agreement, AMD expects to receive more than $100bn in new revenue over four years from OpenAI and other customers, they said.

The chipmaker is expected to report revenue of $32.78bn this year, according to LSEG data. In contrast, analysts are expecting Nvidia to report revenue of $206.26bn for the current fiscal year.

“AMD has really trailed Nvidia for quite some time. So I think it helps validate their technology,” said Leah Bennett, chief investment strategist at Concurrent Asset Management.

Shares of Nvidia dipped more than 1 percent.

OpenAI CEO Sam Altman said the AMD deal will help his startup build enough AI infrastructure to meet its needs.

It was not immediately clear how OpenAI would fund the enormous deal.

OpenAI, which is valued at $500bn, generated approximately $4.3bn in revenue in the first half of 2025 and burned through $2.5bn in cash, according to media reports.

In September, Nvidia announced a deal to supply OpenAI with at least 10 gigawatts worth of its systems.

In contrast with the startup’s deal with AMD where it will take a stake in the chipmaker, Nvidia will invest $100bn in the ChatGPT parent under the terms of the agreement announced in September.

Taking a stake in AMD could give OpenAI “the power to potentially influence corporate strategy. With Nvidia, OpenAI is simply the client and not a part-owner,” said Dan Coatsworth, head of markets at A J Bell.

OpenAI has worked with AMD for years, providing inputs on the design of older generations of AI chips.

The startup and its main backer, Microsoft, announced last month that they had signed a non-binding agreement to restructure OpenAI in to a for-profit entity.

A person familiar with the matter said the deal with AMD does not change any of OpenAI’s ongoing compute plans, including that effort or its partnership with Microsoft.