Between the 10th and 15th of every month, the U.S. Bureau of Labor Statistics (BLS) releases the previous month’s inflation data. This information is used by the Social Security Administration (SSA) to calculate the annual cost-of-living adjustment (COLA).

The BLS was slated to release the September inflation report — the final piece of data needed to unveil the 2026 COLA — at 08:30 a.m. ET on Oct. 15. But due to the federal government shutdown, the most-anticipated announcement of the year has been pushed back.

Social Security’s 2026 COLA reveal will occur on Oct. 24

In its simplest form, Social Security’s COLA is the near-annual “raise” passed along to beneficiaries to offset the impact of inflation (rising prices). If benefits weren’t adjusted for the effects of inflation, Social Security recipients would see their income lose buying power most years.

For the last half-century, the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) has served as Social Security’s inflation measuring stick. With more than 200 different spending categories, each with its own unique percentage weightings, the CPI-W can be reported as a single figure by the BLS each month.

The quirk with Social Security’s COLA calculation is that only the months of July, August, and September (the third quarter) matter. The other nine months of the year can be helpful in spotting trends, but they aren’t used in the COLA calculation.

With CPI-W readings from July and August already known, the only puzzle piece missing is September. Unfortunately, most economic data reports from federal agencies are delayed indefinitely during government shutdowns.

However, some BLS staffers are going back to work and will be releasing the September inflation report on Friday, Oct. 24, at 08:30 a.m. ET, according to information provided to CNBC. The SSA will announce the 2026 COLA on Oct. 24, as well.

Based on estimates from nonpartisan senior advocacy group The Senior Citizens League and independent Social Security and Medicare policy analyst Mary Johnson, next year’s COLA is forecast to come in at 2.7% or 2.8%, respectively. This would work out to an extra $54 to $56 per month for the typical retired-worker beneficiary, and $43 to $44 extra each month for the average worker with disabilities and survivor beneficiary.

While little is set in stone — other than the expectation of the BLS reporting the last piece of data needed to calculate the 2026 COLA on Oct. 24 — retirees are very likely getting the short end of the stick with next year’s raise. COLAs have consistently come up short for retirees, and a projected 11.5% increase in the 2026 Medicare Part B premium isn’t going to help.

Image source: Getty Images.

No speculating here! This is the one guaranteed Social Security change for 2026

Though the government shutdown has delayed the release of key pieces of information, such as next year’s COLA, the maximum taxable earnings cap, the maximum monthly payout at full retirement age, and the withholding thresholds tied to the retirement earnings test, there is one Social Security change that’s guaranteed to take place in 2026. However, you’ll have to go to the state level to see it.

Firstly, yes, Social Security benefits may be taxable at the federal and state levels.

Individuals whose provisional income — adjusted gross income (AGI) + tax-free interest + one-half benefits — tops $25,000, or $32,000 for couples filing jointly, can have some of their Social Security income exposed to federal taxation.

When the calendar flips to Jan. 1, 2026, West Virginia will officially become one of 42 states that don’t tax Social Security income.

In the 2022 tax year, West Virginia made Social Security income exempt from state-level taxation for individuals and jointly filing couples with respective AGIs of $50,000 or less and $100,000 or less.

In March 2024, West Virginia’s legislature passed, and its governor signed, a new law that phases out the taxation of Social Security benefits over a three-year period for those folks who didn’t qualify for this previous AGI adjustment.

Beginning in the 2024 tax year, West Virginians who received Social Security benefits and generated more than $50,000 in AGI (or $100,000 in AGI, if filing jointly) saw 35% of their Social Security benefits exempted from state-level taxation. In 2025, this exemption increased to 65% of Social Security income. In 2026, 100% of Social Security income will be exempted at the state level.

West Virginia will join Kansas, Missouri, Nebraska, and North Dakota as states that have shelved the taxation of Social Security benefits since this decade began.

While this has been anything but a normal COLA announcement month for Social Security, the one thing we do know is that Social Security recipients in West Virginia will be all smiles when the new year arrives.

A Social Security dollar simply isn’t what it used to be.

For most retirees, Social Security is more than just a monthly deposit into their bank accounts. It represents a financial lifeline that helps them make ends meet.

In 2023, Social Security lifted more than 22 million people out of poverty, according to an analysis from the Center on Budget and Policy Priorities (CBPP), and 16.3 million of these recipients were aged 65 and over. If Social Security didn’t exist, the CBPP estimates the poverty rate for adults aged 65 and up would jump nearly fourfold, from 10.1% (with existing payouts) to 37.3%.

Meanwhile, 24 years of annual surveys from Gallup show that 80% to 90% of aged beneficiaries lean on their payouts in some capacity to cover their expenses.

For retirees, few announcements have more bearing than the annual cost-of-living adjustment (COLA) reveal in October. Though Social Security payouts are on track to do something that hasn’t been witnessed in almost 30 years, next year’s “raise” appears set to give retirees the short end of the stick, yet again!

Image source: Getty Images.

What is Social Security’s COLA and why might the 2026 reveal be delayed?

The fabled “COLA” you’ve probably been hearing and reading about over the last couple of weeks is the tool the Social Security Administration (SSA) has on its proverbial toolbelt to keep benefits aligned with inflation.

Hypothetically, if a large basket of goods and services that retirees regularly purchase increases in cost by 2% from one year to the next, Social Security benefits would also need to climb by 2%. Otherwise, these folks would see their buying power decline. Social Security’s COLA attempts to mirror the inflationary pressures that program recipients are facing so they don’t lose purchasing power.

This near-annual raise is based on changes to the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which has measured price changes for Social Security since 1975. It has more than 200 individually weighted categories, which allows the CPI-W to be chiseled down to a single figure at the end of each month. These readings can be compared to the prior-year period to determine if prices are collectively rising (inflation) or declining (deflation).

What makes the COLA calculation unique is that only CPI-W readings from July, August, and September (the third quarter) are used to determine the upcoming year’s raise. If the average third-quarter CPI-W reading in the current year is higher than the comparable period last year, prices, as a whole, have risen, and so will Social Security checks in the upcoming year.

The catch with Social Security’s 2026 COLA is that its expected reveal on Oct. 15 may be delayed. The September inflation report is the final puzzle piece needed to calculate the program’s cost-of-living adjustment. However, most economic data releases are delayed during a federal government shutdown, which, in turn, can postpone the Oct. 15 COLA announcement set for 8:30 a.m. ET.

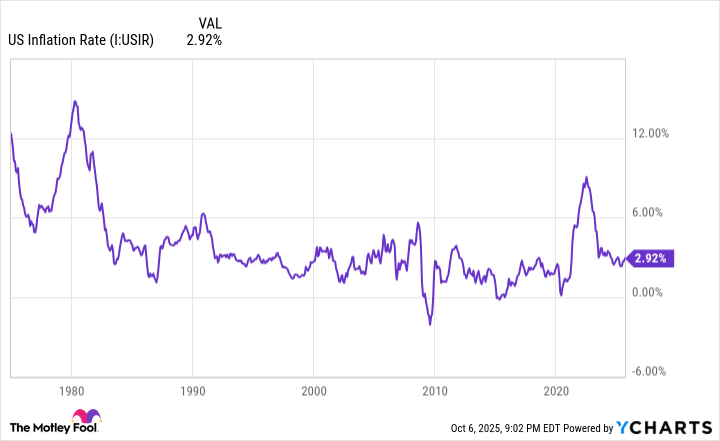

A higher prevailing rate of inflation in recent years has led to beefier annual COLAs. U.S. Inflation Rate data by YCharts.

A first-of-its-century raise is eventually headed retirees’ way

Once the SSA does have the necessary data to calculate and reveal the 2026 COLA, it’s a virtual certainty that beneficiaries will witness history being made.

Over the last four years, Social Security recipients — retired workers, workers with disabilities, and survivor beneficiaries — have enjoyed above-average cost-of-living adjustments. From 2022 through 2025, their Social Security checks grew by 5.9%, 8.7%, 3.2%, and 2.5%, respectively. To put these figures into some sort of context, the average COLA increase over the last 16 years was 2.3%.

Based on two independent estimates that were updated following the release of the August inflation report, a fifth-consecutive year above this 16-year average is expected.

Nonpartisan senior advocacy association The Senior Citizens League (TSCL) has pegged their 2026 COLA forecast at 2.7%, while independent Social Security and Medicare policy analyst Mary Johnson is calling for a slightly higher boost of 2.8%. These two forecasts would imply a roughly $54 to $56 per-month increase in the average retired-worker benefit in the new year.

More importantly, a 2.7% or 2.8% COLA would result in an event that hasn’t been witnessed in almost three decades. From 1988 through 1997, Social Security COLAs vacillated between 2.6% and 5.4%. If the 2026 COLA comes in at 2.5% or above, which looks like a virtual certainty based on independent estimates, it would mark the first time in 29 years that benefits will have risen by at least 2.5% for five consecutive years.

Image source: Getty Images.

The purchasing power of a Social Security dollar isn’t what it used to be

Unfortunately, this potentially history-making moment won’t be fully felt or enjoyed by aged beneficiaries. Though nominal payouts have notably climbed in recent years, the painful reality is that the buying power of Social Security income simply isn’t what it once was.

For example, you might be surprised to learn that the CPI-W isn’t doing retirees any favors. While this index is designed to mirror the inflationary pressures that Social Security’s retired workers are contending with, it has built-in flaws that keep this from happening.

The CPI-W is an index that tracks the cost pressures faced by “urban wage earners and clerical workers,” who, in many cases, are workers under the age of 62. By comparison, 87% of Social Security beneficiaries are 62 and above, as of December 2024.

Aged beneficiaries spend their money differently than workers under the age of 62. Specifically, retirees spend a higher percentage of their budget on medical care services and shelter than younger folks. Even though seniors make up 87% of all Social Security recipients, the CPI-W doesn’t account for the added importance of shelter and medical-care service costs in the COLA calculation.

Furthermore, the trailing-12-month inflation rate for shelter and medical care services has pretty consistently been higher than the annual COLAs beneficiaries have received. According to TSCL, this disparity has played a role in reducing the buying power of Social Security income by 20% from 2010 to 2024. A 2.7% or 2.8% cost-of-living adjustment isn’t going to offset or halt this decline in purchasing power.

To make matters worse, dual enrollees — those receiving Social Security income who are also enrolled in traditional Medicare — are expected to see sizable COLA offsets due to a projected double-digit percentage increase in the Part B premium in 2026.

Part B is the portion of Medicare responsible for outpatient services, and the premium for Part B is commonly deducted from a Social Security recipient’s monthly benefit. An estimate from the 2025 Medicare Trustees Report calls for an 11.5% jump in the Part B premium to $206.20 next year. For lifetime low earners, this increase might gobble up every cent of their projected 2026 COLA.

Regardless of whether or not Social Security’s 2026 COLA is delayed, it’ll mark another year where retirees get the short end of the stick.

Retired-worker beneficiaries can’t seem to catch a break.

The big day for Social Security’s more than 70 million traditional beneficiaries is right around the corner. Assuming the government shutdown doesn’t delay a key data release, on Oct. 15, the Social Security Administration will unveil a multitude of changes for the upcoming year, with the highlight being the 2026 cost-of-living adjustment (COLA).

For retired-worker beneficiaries, who accounted for more than 76% of all traditional Social Security recipients in August, the income they receive from this all-important program is often vital to their financial well-being. Almost a quarter-century of annual surveys from Gallup shows that 80% to 90% of retirees lean on their monthly Social Security check to cover some aspect of their expenses.

Social Security’s cost-of-living adjustment plays an important role for beneficiaries

Before digging into the nitty-gritty of what’s to come for program recipients, it’s imperative to understand why Social Security’s COLA exists.

The best way to view Social Security’s cost-of-living adjustment is as a near-annual “raise” that accounts for the effects of inflation that beneficiaries are contending with. Hypothetically, if a large basket of goods and services regularly purchased by Social Security beneficiaries increased in cost by 3% from one year to the next, Social Security payouts would also need to climb by the same percentage to avoid a loss of buying power. Social Security’s COLA is the raise that attempts to mirror the effects of rising prices (inflation).

Prior to 1975, there was no formula for calculating COLAs on an annual basis. From the very first payout in January 1940 through the end of 1974, only 11 cost-of-living adjustments were enacted by special sessions of Congress.

The near-annual COLAs we’re used to today began in 1975, which is when the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) was adopted as Social Security’s inflationary measure. The CPI-W is reported as a single figure on a monthly basis, which allows for quick year-over-year comparisons to determine if prices are, collectively, rising (inflation) or declining (deflation).

The quirk with Social Security’s COLA is that only three months of readings factor into the calculation: July, August, and September (i.e., the third quarter). If the average third-quarter CPI-W reading in the current year is higher than the comparable period of the previous year, inflation has taken place and beneficiaries are set for a higher payout. Payouts can stay the same year to year; they are not decreased, even if prices in the measured period drop.

A historic expansion of U.S. money supply sent the prevailing inflation rate and Social Security COLAs soaring. US Inflation Rate data by YCharts.

Independent Social Security COLA estimates for 2026 have been narrowed

Following a decade of anemic cost-of-living adjustments during the 2010s, the last four years have featured above-average COLAs. A historic expansion of U.S. money supply during the earlier days of the COVID-19 pandemic led to the highest prevailing rate of inflation in the U.S. in four decades. The result was a 5.9% COLA in 2022, followed by 8.7% in 2023, 3.2% in 2024, and 2.5% in 2025. To add some context to these payout increases, the average COLA over the previous 16 years is 2.3%.

The encouraging news (at least on paper) for Social Security recipients is that the 2026 COLA is on track to do something that hasn’t been witnessed in 29 years. For the first time since 1988 through 1997, the program’s raise is forecast to reach at least 2.5% for a fifth consecutive year. On a nominal-dollar basis, Social Security beneficiaries have seen their payouts notably increase over the last half-decade.

According to nonpartisan senior advocacy group The Senior Citizens League (TSCL), next year’s COLA is projected to come in at 2.7%. Independent Social Security and Medicare policy analyst Mary Johnson, who retired from TSCL early last year, foresees a slightly more robust payout boost of 2.8% in 2026.

If the assumption is made that one of these two forecasts proves accurate, the average monthly benefit for retired workers would climb by approximately $54 to $56 in 2026. Meanwhile, the average worker with disabilities and average survivor beneficiary would both see their monthly Social Security income rise by $43 to $44, respectively.

Image source: Getty Images.

The dreaded lose-lose scenario is looking likely for most retirees in 2026

The first issue relates to the inherent shortcomings of the CPI-W. While near-annual COLAs are a vast improvement compared to Congress passing along raises without rhyme or reason, the CPI-W is itself far from perfect.

As its full name makes clear, the CPI-W tracks the costs “urban wage earners and clerical workers” are facing. These are typically working-age Americans not currently receiving a Social Security benefit. More importantly, urban wage earners and clerical workers spend their money differently than seniors — and adults aged 62 and over make up 87% of Social Security’s traditional beneficiaries.

Older, retired Americans spend a larger percentage of their monthly budget on shelter and medical care services than working-age folks. Not only does the CPI-W not adequately account for the higher weighting retirees place on these two spending categories, but the trailing-12-month inflation rate for shelter and medical care services has been consistently higher than the COLA passed along to program recipients.

Retirees who are dually enrolled in Social Security and traditional Medicare are also set to lose in the upcoming year.

People who are enrolled in traditional Medicare and Social Security almost always have their Medicare Part B premium automatically deducted from their monthly Social Security payout. Part B is the portion of Medicare responsible for outpatient services.

In 2023 and 2024, the Part B premium rose by 5.9% each year. But based on estimates from the June-published Medicare Trustees Report, the Part B premium is forecast to climb 11.5% to $206.20 per month in the upcoming year. There’s little doubt that this is going to partially or fully offset the impact of next year’s Social Security COLA for most dual enrollees.

Even if the cost-of-living adjustment for 2026 surpasses TSCL’s and Johnson’s respective forecasts, it won’t be enough to pull retirees out of this lose-lose scenario in 2026.

We’re about a month away from an official number, but estimates for next year’s COLA are moving higher.

Social Security may be the most valuable retirement asset most Americans have. The pension for retired workers accounted for 20% of families’ total wealth in 2022, according to a study by the Congressional Budget Office. That’s based on a calculation valuing all future payments at present value.

Those future payments get a boost every year, which could make them even more valuable to Americans. The annual cost-of-living adjustment (COLA) helps benefits keep up with inflation. And while we won’t have the official 2026 COLA number until mid-October, it looks like it’ll come in higher than what analysts anticipated at the start of the year.

But a bigger COLA isn’t necessarily reason for Social Security recipients to celebrate. Here’s what retirees need to know.

Image source: Getty Images.

What’s pushing the 2026 COLA higher?

The annual COLA is based on a standard measure of inflation published every month by the Bureau of Labor Statistics called the Consumer Price Index for Urban Wage Earners and Clerical Workers, or CPI-W.

The CPI-W is one of several Consumer Price Index measurements the government publishes. The BLS surveys thousands of businesses and households across the country to collect pricing data on over 200 line items. Those prices are then indexed to a standard price from when the BLS first started collecting data, and weighted according to typical spending patterns of the group the index is supposed to follow. In the case of the CPI-W, the basket of goods represents the spending of working-age adults living in cities.

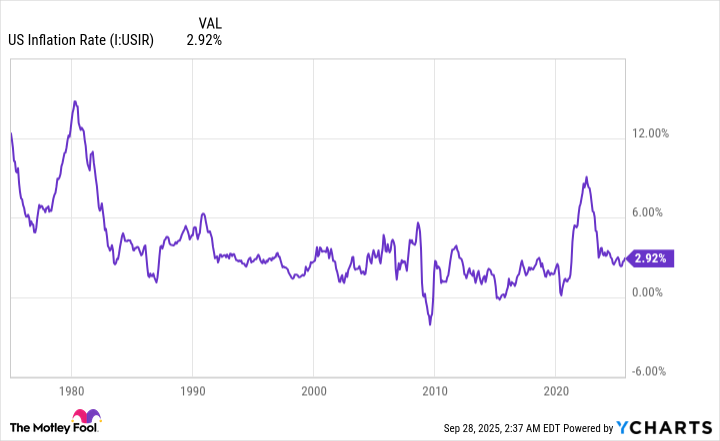

The Social Security Administration calculates the COLA by taking the average year-over-year increase in the CPI-W during the third quarter, i.e. July, August, and September. The BLS just published August’s CPI numbers on Sept. 11, with the CPI-W climbing 2.8% year over year. That follows a 2.5% increase in July. The final reading to determine the 2026 COLA will come out on Oct. 15.

Based on expectations for that reading, both The Senior Citizen’s League and independent analyst Mary Johnson have published their expectations for next year’s COLA. The former expects it to come in at 2.7% while the latter expects retirees to receive a 2.8% bump. Both estimates are higher than the 2.5% initial estimate The Senior Citizen’s League published before the start of the year.

The reasons for a higher COLA are bad news for 70 million beneficiaries

A bigger-than-expected raise is usually great news for those receiving it, but in the case of Social Security’s 70 million beneficiaries, it signals a challenging economic environment.

The biggest challenge is that the CPI-W doesn’t perfectly match the spending of most seniors. Most people don’t spend their money in retirement the same way they did when they were working age. They probably commute less and spend less on new clothing. They probably have different dining habits. And it’s almost certain that their medical bills have climbed higher as they grow older.

To that end, some of the biggest expenses seniors face are climbing faster than the overall CPI-W numbers. Medical care services were notably 4.2% higher this August than the year before. While gasoline prices were down, utilities were way up. Shelter expenses climbed 3.6%. Despite a 2.7% or 2.8% raise coming in January, most seniors have seen their real cost of living climb much more over the past year.

Rising medical costs are most prominently seen in the Medicare Trustees’ estimate for next year’s Medicare Part B premium. They expect the program will have to charge a standard monthly premium of $206.20 next year, an 11.5% increase from 2025. For those keeping track, that far outpaces the expectations for Social Security’s COLA. Beneficiaries age 65 and older enrolled in Medicare will see that amount come right out of their new monthly payments.

The Senior Citizens League contends this situation isn’t unique to this year’s COLA. It ran a study that estimates the buying power of someone’s benefits who started Social Security in 2010 has decreased 20% through 2024.

The best economic environment for Social Security has historically been slow, steady, and predictable inflation. Under the current administration, which has gone back and forth on trade policies numerous times since the start of the year, prices have become anything but predictable. While many businesses have taken preemptive steps to curb and delay the impact of tariffs, the costs will eventually get passed through to consumers. That could result in even more pain for those on a fixed income next year.

While a 2.7% or 2.8% raise might be bigger than anticipated, many seniors may find that it doesn’t go far enough next year.

Sitting still on a plane for too long can cause cramping, bloating and in serious cases, deep vein thrombosis – so here are the best tips to keep comfortable and healthy on a long flight

These tips will make your travel more comfortable (Image: Enes Evren via Getty Images)

Air travel can be a bit of a squeeze, particularly for those of us who aren’t flush enough to splash out on business class. Economy seating can feel rather tight, and enduring this for extended periods can not only cause discomfort but also potentially lead to serious health issues.

Problems such as cramping, bloating, and, in more severe cases, deep vein thrombosis can all result from remaining stationary on a plane for too long. So, if you’re gearing up for a lengthy flight in the near future, it’s crucial to know how to maintain your comfort and well-being.

The pros at Netflights have kindly shared their top tips for making that long-haul journey a tad more bearable.

These changes can make flying easier(Image: laddawan punna via Getty Images)

One of their key recommendations is to rise from your seat and take a stroll every one to three hours. Make a deliberate effort to move about frequently during your flight.

Even something as simple as walking to the loo or standing up for a stretch can help keep you feeling sprightly and prevent stiffness, which is particularly vital on flights exceeding four hours, reports the Express.

Stretching is another crucial aspect, and you can do this right from your seat. Gently roll your neck from side to side, rotate your shoulders forwards and backwards, and carefully twist your spine.

Each of these movements should be repeated three to five times in each direction, but remember to be gentle. These stretches should provide relief, not strain your body.

The third method to tackle swelling and bloating is by raising your feet.

Sitting with your feet flat on the floor for extended periods can lead to discomfort, and travellers may suffer from swollen feet and ankles during long-haul flights.

Airplane travel doesn’t have to be painful(Image: Constantine Johnny via Getty Images)

To mitigate this whilst airborne, elevate your feet.

Resting your feet on your underseat carry-on helps counteract the natural downward flow of fluid in your body, thus reducing discomfort.

Flex your feet, rotate your ankles, or gently stretch your arms and back while seated to maintain blood circulation throughout your body.

Three times in the ninth inning last Friday night in New York, new Dodgers closer Tanner Scott made the same simplistic, save-blowing mistake.

In an inning that saw Scott blow a three-run Dodgers lead — forcing the team into a 13-inning marathon that, despite eventually winning, their overworked bullpen could ill-afford — Scott got to two strikes against a Mets batter, only to leave a mistake pitch over the plate.

To Starling Marte, it was a 1-and-2 fastball up and over the middle, resulting in a leadoff single.

After a one-out walk to Pete Alonso, Scott had Jeff McNeil 2-and-2 before throwing a belt-high heater on the inner half that was ripped for a two-run triple.

Another two-strike count followed to Tyrone Taylor, but Scott’s 1-and-2 slider hung up around the heart of zone, leading to a tying single that marked Scott’s fourth blown save in 14 opportunities this year and raised his ERA to 3.42 — hardly the numbers expected out of an All-Star left-hander signed to a $72-million contract this offseason.

“I think the stuff is still good,” manager Dave Roberts said afterward. “It’s just right now, it just seems like when there is a mistake, they find some outfield grass or put a good swing on it.”

And lately, such mistakes have been coming in more abundance than usual for Scott, highlighting one early-season trend the Dodgers are now working to address.

“Right now, he’s just kind of living in the middle, the midline of the zone,” pitching coach Mark Prior said. “You leave it in that spot, more than likely they’re gonna put a good swing on it.”

Dodgers pitcher Tanner Scott embraces catcher Dalton Rushing after a 3-1 win over the Arizona Diamondbacks at Dodger Stadium on May 21.

(Gina Ferazzi / Los Angeles Times)

For a pitcher who struggled with command issues early in his career — before blossoming into one of the top left-handed relievers in the sport of the last several seasons — Scott is now seemingly suffering from the opposite problem.

So far this year, more than 58% of his pitches have been in the strike zone, a rate that is easily a personal career high (well up from his previous high mark of 52.4% last year) and ranks 18th among qualified big-league relievers.

On top of that, hitters have been on such offerings as well, making contact on 80% of swings against Scott’s pitches over the plate (compared to his 76% career rate) and averaging almost 92 mph of exit velocity on balls put in play (leaving Scott in the seventh percentile of MLB arms when it comes to batted ball contact).

The good news is that Scott has 25 strikeouts and only two walks. Even with his fastball playing a tick down velocity-wise (averaging 96.1 mph this year compared to 97 mph last year), he converted nine of his first 11 save opportunities, squandering only a pair of one-run leads while posting a sub-2.00 ERA through his first 21 appearances.

This past week, however, Scott was knocked around twice: Giving up three runs on two homers to the Arizona Diamondbacks last week (in another game that necessitated extra innings before the Dodgers came back to win) before his ninth-inning meltdown at Citi Field on Sunday.

“He’s actually been pretty good for us,” Roberts said of Scott’s performance overall. “But the last couple, the last two of three, he’s obviously given up leads.”

Scott said his increased aggressiveness in the strike zone has not been by design.

“I don’t even look at it,” he bristled when asked about his rise in in-zone pitch percentage this weekend. “I don’t even look at it.”

But Prior acknowledged it is something on the coaching staff’s radar.

“Obviously, we want strikes; more strikes than balls,” Prior said. “But he gets in situations where he can get into counts, and I think we’re just leaving too many balls in the zone late in counts, instead of going for more miss.”

Friday’s blown save being Exhibit A.

“I’m not putting [guys] away,” acknowledged Scott, whose whiff rate has also dropped to 26.6% this season compared to his 34.7% career average. “I’m not getting the swing-and-miss, and I’m keeping the ball in the zone too much.”

To Prior, it’s even OK if Scott starts “to walk a few more guys,” he said, “[if] in turn he can get more chase out of the zone when you have leverage.”

“He’s still a really good pitcher,” Prior added. “So we’re going to bank on him.”

Dodgers pitcher Tanner Scott throws from the mound against the Arizona Diamondbacks on May 20 at Dodger Stadium.

(Gina Ferazzi / Los Angeles Times)

Right now, the Dodgers don’t have much of a choice.

Fellow high-leverage relievers Evan Phillips (forearm discomfort), Blake Treinen (forearm sprain), Kirby Yates (hamstring strain) and Michael Kopech (shoulder impingement) are all out injured. And while Kopech is on a minor-league rehab assignment, and Yates and Treinen are both beginning throwing programs, Phillips’ absence is starting to become “concerning,” Roberts acknowledged this weekend, with the team’s former ninth-inning fixture now going on three weeks without throwing because of an injury initially expected to keep him out for only the minimum 15 days.

“I’m getting a little kind of concerned,” Roberts said of Phillips, “but hoping for the best.”

It all makes Scott’s performance in save opportunities particularly crucial for the Dodgers right now.

Given the team’s MLB-high bullpen workload this year, Roberts has been forced to be selective when it comes to the usage of the few high-leverage relievers still at his disposal. Having Scott blow games in which the team has already burned its best other relief bullets, and could potentially face the added burden of resulting extra innings, are all taxing side effects the Dodgers are not currently equipped to handle.

“To be quite fair,” Roberts noted of Scott, whose 23 ⅔ innings are only fourth-most in the bullpen, “the other guys have been used a lot more than he has.”

Thus, while Scott might only require simple adjustments, such as better locating his fastball up and out of the zone and more consistently executing his slider in locations that induce more chase, enacting such changes quickly is paramount.

After all, the Dodgers made him one of the highest-paid relievers in baseball this offseason to stabilize their bullpen. And lately, he’s instead been one more source of unneeded flux.