Dutch Bros stock might’ve doubled in the last year, but I think it’ll keep rising through 2030 and beyond.

While no one can be certain what stocks may or may not “pop” in any five-year window, investors can tilt the odds in their favor by looking for businesses with a long list of potential market-beating catalysts.

I believe the upstart handcrafted beverages chain Dutch Bros (BROS -0.53%) perfectly exemplifies this notion.

Dutch Bros is home to several promising catalysts that could drive its stock price higher between now and 2030.

Although I’m willing to predict that the up-and-coming company could help make investors richer by 2030, Dutch Bros’ current business developments paint an even brighter picture beyond that point.

Image source: Dutch Bros.

Dutch Bros’ numerous catalysts

Dutch Bros’ share price has more than doubled in just the last year alone.

Despite this run, I believe there are five specific reasons why the company has ample room to rise and help make investors richer by 2030.

Dutch Bros is more than just coffee

Far from a traditional hot coffee chain, Dutch Bros generates 87% of its sales from ice or blended drinks. It also receives roughly one-quarter of its sales from its Rebel energy drinks.

This is a powerful differentiator for Dutch Bros, as it caters directly to its youngest and most important (for the long term) customers — Gen Z — who strongly prefer iced, blended, and energy drinks over hot coffee.

Industry experts project the coffee industry to grow 7% by 2030, whereas the energy drink category should grow more than 40% by 2032. This shift toward energy drinks should keep the company front and center on the beverage scene, thanks to its outsized allocation to energy drinks.

Immense store count expansion potential

Dutch Bros has 1,043 locations, but recently announced its stretch goal of 2,029 stores by 2029. While doubling its store count in four years may sound like a reach, the company is on pace to open around 160 in 2025 and plans to grow its new shop count by a mid-teens percentage annually for the next few years.

If management meets this bold goal and maintains its steady cash generation, I would feel terrific about my prediction being accurate.

Best yet, the Dutch Bros growth story doesn’t stop here. Over the long term, the company believes it can reach more than 7,000 locations. Currently operating in just 18 states (but entering five new ones in 2025), Dutch Bros’ growth story should persist well beyond 2030.

With its newest 2024 shops delivering annual unit volumes similar to those built in 2022 or earlier, I’m confident in management’s ability to continue expanding geographically in a profitable manner.

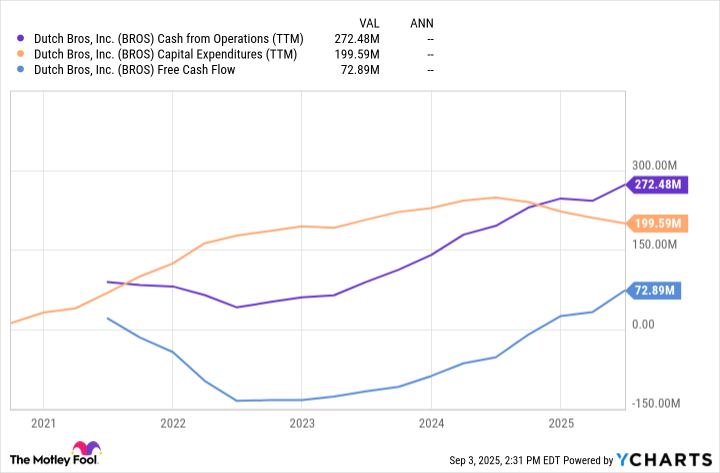

Cash flows are now positive

Perhaps the biggest reason I’m optimistic about Dutch Bros’ ability to enrich our portfolios is that it recently reached breakeven on a free cash flow (FCF) basis.

BROS Free Cash Flow = Cash From Operations-Capital Expenditures data by YCharts

Despite the company’s rapid store count growth (which creates heavy capital expenditures), Dutch Bros has reached positive FCF. Said another way, management can now fund its growth ambitions in-house rather than through debt or shareholder dilution from issuing new shares.

Additionally, if Dutch Bros wasn’t spending heavily on capex (just a thought experiment), it would already be a bona fide cash machine, generating 18 cents of cash from operations for every $1 in sales.

Mobile ordering is still young

While the company’s expansion plans may take center stage in its growth story, Dutch Bros’ recent rollout of mobile ordering at all locations could prove to be a promising growth catalyst on its own.

Customers are rapidly adopting mobile orders, but these orders still only account for 11.5% of the company’s total transactions. Every additional order that switches from being placed in the drive-thru lane to mobile offers throughput improvement for Dutch Bros.

During the company’s second-quarter earnings call, Chief Executive Officer Christine Barone explained that mobile ordering has already delivered an order frequency lift, while also being a popular option in the morning.

Whereas customers may have previously gone without a beverage if their time was limited, the grab-and-go feasibility provided by mobile ordering could help add a number of once-missed sales.

Food options

Dutch Bros currently generates less than 2% of its sales from food. While Starbucks has shown that adding food to a beverages-focused business isn’t the easiest feat to pull off, the fact remains that leading coffee chains generate one-fourth of their sales from food.

Currently, Dutch Bros is piloting a food program that could be fully rolled out by 2026 and is already seeing incremental growth in its morning orders. If the company inches anywhere closer to the industry average of 25% of sales from food, it could be a boon for Dutch Bros’s same-store sales.

Dutch Bros’ valuation

While there is a lot to like about Dutch Bros, its price-to-earnings (P/E) ratio of 199 undoubtedly scares many investors away.

However, this may not be the best valuation to assess the company with. Revisiting the cash from operations figures examined earlier, and comparing them to the company’s market capitalization, Dutch Bros stock trades at 47 times CFO.

Yes, this is still a premium valuation, but for a company with a reasonable chance to double its store count over the next four years, it isn’t excessive in my opinion.

Although the company still has to execute, numerous catalysts indicate that Dutch Bros can help make investors rich by (and more importantly, beyond) 2030.