Costco Wholesale (COST -0.84%) is one of the most successful retail stocks in history. It launched its IPO in 1985 at a split-adjusted $1.67 per share, meaning it has risen 575-fold during its 40-year trading history. Amid its 205% stock price growth over the last five years, it outperformed the S&P 500 during that time, and one might assume it can surpass the index again in the next five.

Nonetheless, its past performance is not a guarantee that the retail stock will repeat or exceed its returns. Thus, investors need to take a closer look at the company and its financials before making such a determination. Let’s do that now.

Image source: Getty Images.

The state of Costco

Without a doubt, Costco’s business model helps make it one of the world’s most successful retailers. That fee, which is as low as $65 per year in the U.S., allows customers to purchase desired, high-quality bulk goods at a price that is little more than the cost of goods sold plus overhead.

More importantly, it has developed a business culture that seems to work no matter where Costco tries it. As of its fiscal 2025’s third quarter (ended May 11), 629 of Costco’s 914 stores were in 47 U.S. states. Thus, as the U.S. market becomes more saturated, Costco could potentially drive decades of growth in other countries.

This stands in contrast to retailers like Target and Home Depot, which failed to adapt their business cultures to work outside of their home regions. Since both companies lack obvious avenues for higher growth, Costco seems to have the best growth prospects among the brick-and-mortar retailers with nationwide footprints in the U.S.

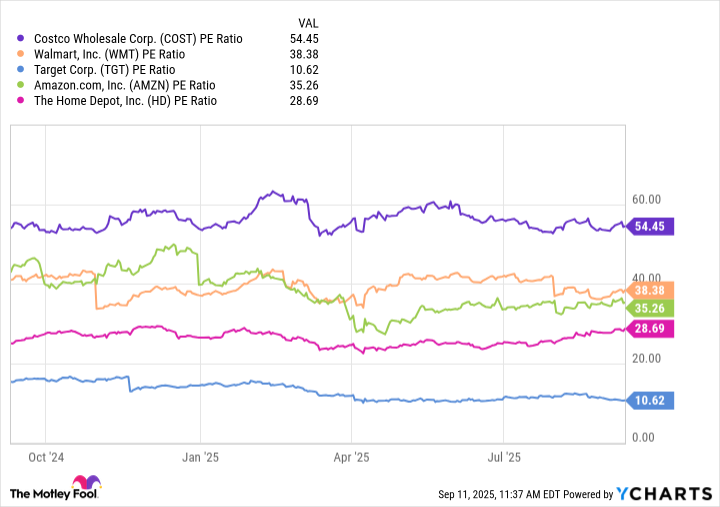

Why some investors might hesitate to buy Costco

Unfortunately for new investors, the investment community already has a wide appreciation of Costco’s success. Its price-to-earnings (P/E) ratio of 54 demonstrates its popularity, which far outpaces its largest competitors’.

COST PE Ratio data by YCharts.

Moreover, in 2025, the earnings multiple briefly exceeded 60, its highest level since the stock market bubble of the late 1990s and early 2000s.

Although Costco is on track for continued prosperity, one must question whether its growth rate justifies the earnings multiple. The company planned to expand by 24 warehouses in fiscal 2025, but that amounts to less than a 3% annual increase.

Additionally, while its financial growth is steady, it remains in the single digits. In the first nine months of fiscal 2025, net sales of $189 billion rose 8% compared to the same period in fiscal 2024.

Although it kept cost and expense growth in check, interest income fell just as its tax burden rose. Thus, its $5.5 billion in net income for the first three quarters of the year rose by 9%.

While such growth levels bode well for the company, one might question whether they justify a 54 P/E ratio. Looking ahead, analysts foresee growth levels taking the forward P/E ratio of 48 and a forward one-year earnings multiple of 43.

At that rate of increase, it could take Costco approximately five years to reach the S&P 500’s average earnings multiple of 31. History shows that Costco tends to beat that average, but even if its P/E ratio fell to 40, it could bode poorly for the company’s five-year growth trajectory.

Where will Costco be in five years?

Given what we know about Costco’s financials, investors should expect Costco to trade at a higher price than it does today, albeit with returns that underperform the S&P 500.

Admittedly, a lot can change in five years, and changes may occur that we cannot predict today. Thus, investors should not discount the possibility of an unforeseen event that either bolsters or undermines the current investment thesis.

Nonetheless, the company’s growth and financials do not appear to justify a 54 P/E ratio. Hence, that earnings multiple is likely to come down over time, reducing the stock’s return. While Costco likely remains a hold for its longer-term investors, people should probably put their existing cash to work elsewhere.

Will Healy has positions in Target. The Motley Fool has positions in and recommends Amazon, Costco Wholesale, Home Depot, Target, and Walmart. The Motley Fool has a disclosure policy.