This beaten-down drugmaker is well positioned to turn things around.

One of the great things about equity markets is that excellent stocks can be had at almost any price, making them accessible to most people. Even with $100, it’s possible to find outstanding, growth-oriented companies to invest in. Of course, what qualifies as “the smartest” stock to buy with any amount of money will differ from one investor to the next, depending on factors such as risk tolerance, goals, and investment horizon.

One growth stock trading for well below $100 that can meet many investors’ demands is Novo Nordisk (NVO -2.96%). Here is why the Denmark-based company is an excellent stock to buy right now.

Image source: Getty Images.

A wonderful contrarian opportunity

Quality growth stocks tend to be highly sought after. There is often a higher demand for shares of these companies than are available. That’s why their prices rise. Sometimes, though, these otherwise excellent companies encounter challenges that lead to a sell-off, providing investors with a wonderful opportunity to pick up their shares at a discount.

In my view, that’s what we have with Novo Nordisk. True, the company has faced some challenges, and it has paid for them as shares have remained southbound for over a year. Its financial results haven’t been as strong as expected. It hit a series of surprising clinical setbacks while losing market share to its rival, Eli Lilly.

However, Novo Nordisk’s prospects remain very strong. Novo Nordisk’s claim to fame is that it has been a major player in the diabetes drug market for decades. That remains the case. As of May, it had a 32.6% share of the diabetes market and a 51.9% share of the GLP-1 space. While its hold in these fields declined compared to last year, it remains a dominant force in both.

Novo Nordisk also continues to post competitive financial results for a pharmaceutical giant. The company’s sales for the first half of the year increased by a strong 16% year over year to 154.9 billion Danish kroner ($24.2 billion).

Further, the diabetes and obesity drug markets are rising fast due to several factors. Both conditions have skyrocketed in recent decades, and drugmakers are now developing highly innovative therapies to address them. Novo Nordisk is still at the forefront of this race. Even if the company has a smaller slice of the pie, that’s not a significant problem if the pie is substantially larger.

Can Novo Nordisk continue to launch innovative medicines and stay ahead of most of its peers, excluding Eli Lilly? The company’s pipeline suggests that it can, and could even catch up with its eternal rival. Consider Novo Nordisk’s potential triple agonist (a medicine that mimics the action of three gut hormones), UBT251.

In a 12-week phase 1 study, UBT251 resulted in an average weight loss of 15.1% at the highest dose. The usual caveats regarding early-stage studies apply. Still, UBT251 looks promising, especially since there is no single triple agonist approved for weight loss yet. And that’s just the tip of the iceberg. Novo Nordisk has several other exciting candidates through all phases of clinical development. And those that have already passed phase 3 studies, such as CagriSema, should generate massive sales for the drugmaker.

According to some projections, CagriSema could rack up $15.2 billion in revenue by 2030. Ozempic and Wegovy, Novo Nordisk’s current bestsellers, should also remain among the top-selling medicines in the world through the end of the decade. So, Novo Nordisk’s medium-term outlook seems promising.

There are more reasons to buy

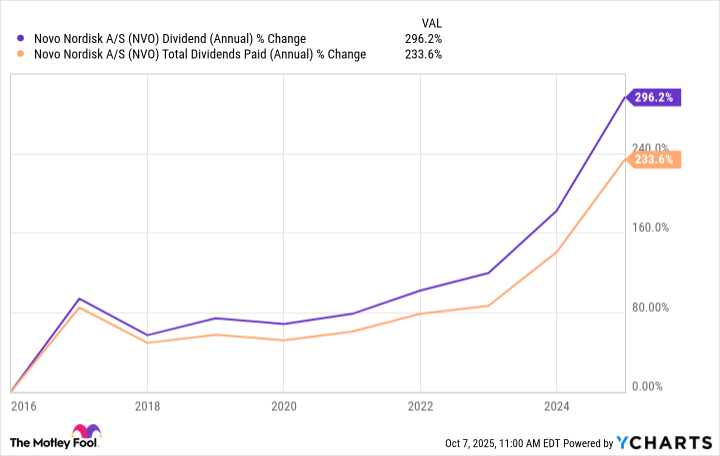

Novo Nordisk appeals to growth-oriented investors, but it is also a great pick for dividend seekers and bargain hunters. For those seeking income stocks, the Denmark-based drugmaker is a great choice, given its strong track record. The company’s forward yield is not exceptional at 2.9% — although that’s much better than the S&P 500‘s average of 1.3% — but Novo Nordisk has consistently increased its dividends over the past decade.

NVO Dividend (Annual) data by YCharts

Finally, Novo Nordisk’s shares are trading at 14 times forward earnings, whereas the average for the healthcare industry is 17.3. Even with the challenges it has faced recently, Novo Nordisk’s strong pipeline and lineup, solid revenue growth, and excellent prospects in diabetes and weight management make the stock highly attractive. The company’s shares are changing hands for about $59, so $100 can afford you one of them.