A whole bunch of investors seem to think so… maybe too many.

SoFi Technologies (SOFI 0.02%) is attracting lots of investor attention these days, and understandably so. Its stock up more than 160% from its April low, and higher to the tune of 260% for the past year. That’s huge.

But is it actually the buy the crowd seems to think it is? Yes. And no.

Here’s some food for thought if this ticker’s made its way onto your radar but not yet made its way into your portfolio.

What’s SoFi Technologies?

SoFi is an online bank, except it’s only an online bank; it doesn’t operate any brick-and-mortar branches. That doesn’t mean it can’t offer everything a traditional bank does, though. Checking and savings accounts, investment services, loans, insurance, and credit cards are all in its repertoire.

It’s no mere experiment either. The $30 billion company serves more than 11.7 million customers and boasts $36.3 billion in assets. And of last quarter’s revenue of $855 million (a fairly typical quarter), nearly $98 million of that was turned into net income.

Image source: Getty Images.

Of all these numbers, however, the most impressive is SoFi’s current customer headcount.

While its 11.7 million members pales in comparison to the customer bases of Wells Fargo and Bank of America, it’s incredible for a bank that’s only been chartered since January of 2022. Making this customer count figure even more impressive is the fact that it’s grown every single quarter since the first quarter of 2020, when it was still more of a fintech middleman with a limited number of offerings. In fact, on an absolute basis SoFi’s customer growth is still accelerating rather than slowing down, with last quarter’s year-over-year member growth of 34% carrying its customer count to yet another record-breaking figure of 11.7 million.

The new norm

The company is of course plugged into the massive shift in the way most consumers live their lives. That’s online, and in particular, through their favorite connected device — their smartphone.

A survey commissioned by the American Bankers Association late last year tells the tale. Of the 4,508 adults questioned, only 8% said in-branch visits were their preferred way of handling banking business, while only 4% named telephone calls as their top means of taking care of any banking matters. At the other end of the scale, 22% of respondents reported they were managing their bank accounts using a laptop or PC, while a whopping 55% of these consumers said a mobile app was their favorite banking tool. And it should come as no real surprise that younger people were far more likely than older customers to utilize their digital options.

SoFi’s growth simply reflects this new norm, which of course corresponds with the ongoing aging of digitally native consumers.

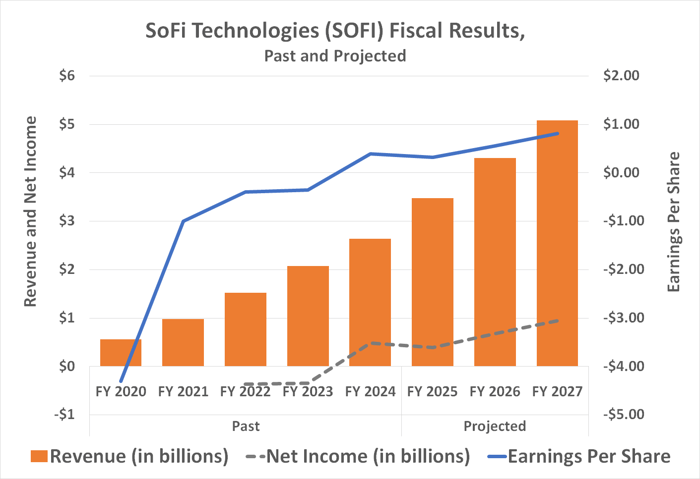

More of the same is in the cards too. Market research outfit Technavio believes the worldwide digital banking business is set to grow at an average annualized pace of more than 16% through 2029. The U.S. market that SoFi Technologies serves is expected to see the most growth during this stretch. For its part, analysts believe SoFi’s top and bottom lines will nearly double between last year and 2027.

Data source: StockAnalysis.com, SimplyWallSt.com, Marketwatch. Chart by author.

The kicker: At least some of this future growth will be driven by the company’s foray into business lines beyond basic banking. In July, for instance, the bank offered access to an expanded lineup of private investments, and earlier this month launched another of its own sponsored exchange-traded funds — the SoFi Agentic AI ETF (AGIQ 0.26%). This willingness to establish new profit centers underscores the idea that the company is casting an ever-widening net.

Right stock, wrong time

So it’s a buy? Not so fast.

There’s never a bad time to buy a good stock, to be clear. But there are certainly better times than others. Right now arguably isn’t the best time to buy this one.

The issue is the sheer scope of SoFi stock’s run-up just since the middle of last year. While its bullishness is understandable, it’s also too much, too fast. Shares have more than doubled in value in just a little over a year, pushing them to a recently reached record that’s more than 20% above the analyst community’s current consensus price target of $20.72.

The stock’s valuation of nearly 50 times next year’s expected per-share earnings of $0.52 is also steep for any stock, but it’s particularly rich for a bank — even one growing as quickly as SoFi Technologies. So interested investors might want to wait for a pullback before plowing in. The good news is, we’ve frequently seen lulls from this ticker before.

Just don’t get too picky if you want to buy in. It’s unlikely you’ll see what you might consider a great price for this stock anytime soon; any modest lull may be all you’re going to get. The growth here is just too strong and the company’s story is too compelling to expect any major pullback from the stock.

Wells Fargo is an advertising partner of Motley Fool Money. Bank of America is an advertising partner of Motley Fool Money. James Brumley has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.