The cybersecurity giant is seeing strong sales thanks to artificial intelligence.

Investing in cybersecurity stocks makes sense in this digitally dependent world. And now, the importance of protection against cyberattacks is amplified further by the emergence of artificial intelligence (AI).

That’s why some forecasts predict the cybersecurity industry will grow from $194 billion in 2024 to $563 billion by 2032 with generative AI giving companies in the sector a boost. Veteran player Palo Alto Networks (PANW 1.38%) is already seeing AI serve as a tailwind to its business.

Even so, the company’s stock is well off its 52-week high of $210.39 reached at the end of July. Does this create an opportunity to scoop up shares at a discount? Let’s dive into Palo Alto Networks to see if the cybersecurity titan is a worthwhile investment.

Image source: Getty Images.

Palo Alto Networks’ strategic initiatives

Palo Alto’s share price dropped after the company announced on July 30 the impending acquisition of CyberArk for $25 billion. Its stock’s decline was understandable given this is the largest acquisition under Palo Alto Networks CEO Nikesh Arora since he took over the top spot in 2018.

CyberArk focuses on identity security, which ensures only authorized users have access to a company’s systems and data. Acquiring CyberArk was a smart move. Identity security is an area lacking in the Palo Alto Networks platform, and now that hole is filled.

The capability is important in the AI era. Artificial intelligence now executes tasks on behalf of a business, so cybersecurity software must be able to identify which AI are allowed and which might indicate an attack is taking place. CyberArk will enable Palo Alto Networks to do that task.

The acquisition also strengthens the company’s “platformization” strategy, a key component of its long-term business growth. Before Arora’s leadership, Palo Alto Networks sold disparate security products and was known particularly for its firewalls.

Now, the company is pursuing a platform play where its offerings are bought as a complete cybersecurity package. This does away with the need for customers to buy from various vendors, making Palo Alto Networks a one-stop solution.

Palo Alto Networks’ rising fortunes

The platformization approach is working. Palo Alto Networks reported strong 15% year-over-year revenue growth to $9.2 billion in its 2025 fiscal year, ended July 31.

Not only did revenue rise, the cybersecurity giant’s fiscal 2025 operating income grew to $1.2 billion from $683.9 million in the prior year. This demonstrates that Palo Alto Networks is managing its costs well as it grows revenue.

Another area of strength is the company’s balance sheet. It exited the fiscal fourth quarter with total assets of $23.6 billion compared to total liabilities of $15.8 billion. But it’s worth noting that $12.8 billion of those Q4 liabilities represented deferred revenue. This is up-front payments from customers that will be recognized as income once services are delivered.

In addition, the cybersecurity giant expects another year of excellent sales growth in fiscal 2026. Palo Alto Networks is forecasting around $10.5 billion in revenue for the new fiscal year, which would be a 14% increase over 2025’s $9.2 billion.

Making a decision on Palo Alto Networks stock

Despite a crowded field of competitors in the cybersecurity sector, Palo Alto Networks is making moves that strengthen its business, while its platformization strategy is paying off with sales growth. But before deciding to purchase shares, another factor to consider is share-price valuation.

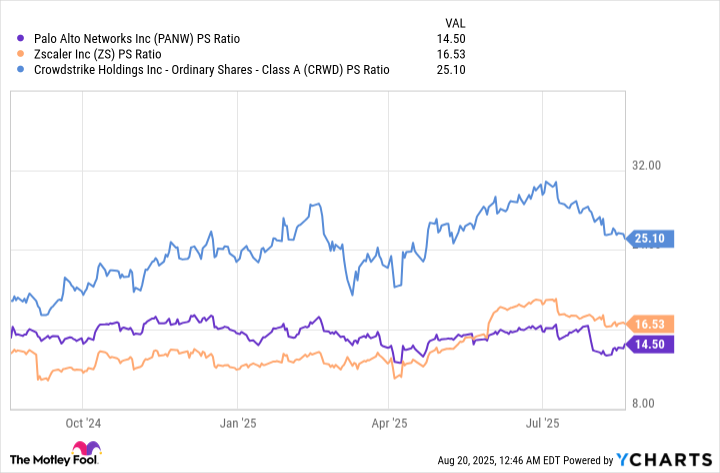

To assess this, here’s a look at the price-to-sales (P/S) ratio for Palo Alto Networks in comparison to major competitors CrowdStrike and Zscaler. The metric measures how much investors are willing to pay for every dollar of revenue generated over the trailing 12 months and is useful for comparing companies that are not profitable, as is the case for CrowdStrike and Zscaler.

Data by YCharts.

The chart shows that Palo Alto Networks possesses the lowest P/S multiple across the trio; as of Aug. 19, it’s lower than it’s been over the past year. This indicates Palo Alto Networks stock is attractively valued.

Contributing to its many strengths, on Aug. 14, Palo Alto Networks announced that its cybersecurity systems are preparing to protect against attacks from quantum computers. While quantum machines are still in the developmental stages, they have the potential to easily slice through today’s digital protections. The announcement illustrates the company’s drive to stay ahead of emerging threats.

With strong sales, healthy financials, and a successful platform that continues to keep pace with an ever-changing tech landscape, Palo Alto Networks possesses the characteristics of a company worth investing in. Add to this a compelling share-price valuation, and now looks like a good time to buy its stock.

Robert Izquierdo has positions in CrowdStrike and Palo Alto Networks. The Motley Fool has positions in and recommends CrowdStrike and Zscaler. The Motley Fool recommends Palo Alto Networks. The Motley Fool has a disclosure policy.