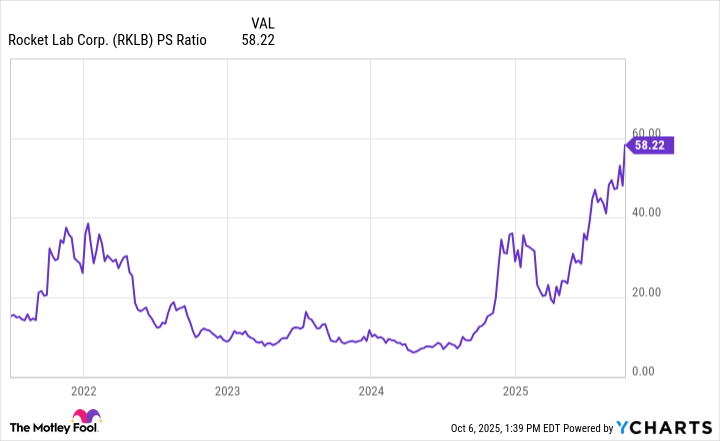

The aerospace company now trades at close to 60 times its trailing revenue.

After a stock skyrockets by around 500% in just 12 months, as Rocket Lab (RKLB -3.21%) has, it’s only natural to wonder if it rose too quickly, and in so doing, has become too overvalued to safely invest in.

The aerospace company has been experiencing tremendous growth in recent years, and investors remain bullish about its potential for even more growth ahead due to its larger new Neutron rocket, which will open up more opportunities for the business in the long run. But with the company’s market cap now hovering around $28 billion, has too much expected growth been priced into the stock? Could shares of Rocket Lab be due for a big decline?

Image source: Getty Images.

Rocket Lab’s stock carries an incredibly high premium

Although Rocket Lab’s business has been growing in recent years, so too have its losses. From 2021 through 2024, its revenue rose from just $62 million to more than $436 million. Its losses didn’t increase at nearly as rapid a pace, but they did rise from $117 million to $190 million.

When a company is in a rapid-growth phase, it’s not usually worried as much about keeping costs in check — the priority is the top line. In that context, short-term losses can be justifiable. But with Rocket Lab, investors are also paying a massive premium; the stock trades at close to 60 times its trailing revenue and 40 times its book value. Paying high multiples for stock can be warranted when there’s low risk and a lot of future growth expected, but Rocket Lab is far from a safe buy given its current levels and its lack of profitability.

Back in 2021, when it first went public, there was plenty of hype around Rocket Lab’s business, but it wasn’t trading at the mammoth premium that it is today.

RKLB PS Ratio data by YCharts.

The company may not be out of growth catalysts just yet

Despite the stock’s high valuation, one factor could still drive it higher: the company’s Neutron rocket. It’s a partially reusable rocket that can carry significantly larger payloads than Rocket Lab’s current Electron rocket. A successful inaugural launch will be a huge milestone for the business, which could lead to even more excitement around this already scorching-hot stock — and unlock more contract opportunities.

That event could, however, also turn into a sell-the-news moment where investors buy up the stock amid the chatter leading up to the launch, and then sell shares right when they might be around their peak, which might happen if and when a successful launch takes place. This is one of the risks with buying speculative stocks — their movements are extremely difficult to predict.

According to analysts, the stock is already heavily overvalued. The consensus 12-month price target of a little more than $42 is 27% lower than the current price. However, a successful Neutron launch could spark a wave of price-target upgrades from analysts.

Rocket Lab is a high-risk, high-potential-reward stock

This week, Rocket Lab’s stock hit a new 52-week high, proving that it’s not running out of steam just yet. And it may hold its momentum as the excitement builds around the upcoming Neutron launch. The closer that gets, the more the stock may rally.

Rocket Lab’s fundamentals, however, don’t support its inflated valuation, and the danger is that with expectations being as high as they are, there is plenty of room for disappointment and for the stock to fall significantly in value. Although it may not have peaked just yet, that doesn’t mean it’s a good buy at its current price. Unless you have a high risk tolerance, you’d probably be better off investing in a more reasonably priced growth stock than Rocket Lab.

David Jagielski has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Rocket Lab. The Motley Fool has a disclosure policy.