Meta will pay Alphabet $10 billion over six years for access to Google Cloud’s infrastructure.

The stocks of Google parent Alphabet (GOOGL 3.10%) (GOOG 2.98%) and Meta Platforms (META 2.04%) shot higher in Friday trading. Although most stocks rose because the Federal Reserve strongly hinted at a September cut in interest rates, another factor was likely the announcement of Meta’s cloud deal with Google, as reported by The Information.

Considering the $10 billion size of the deal, one has to assume it is critical, particularly to Alphabet. Still, considering the state of the artificial intelligence (AI) stock, it could serve as a much-needed catalyst for the company’s investors. Here’s why.

Image source: Getty Images.

Terms of the partnership

Under the terms of the deal, Meta will pay Google $10 billion over six years. In exchange, it will receive access to Google Cloud’s storage, server, and networking services, along with other products.

Meta has previously relied on Amazon‘s Amazon Web Services (AWS) and Microsoft‘s Azure for such services. The deal does not necessarily mean it will deal less with these companies. More likely, it speaks to Meta’s insatiable demand for cloud infrastructure as it seeks to become a major player in the AI space.

Additionally, Meta and Alphabet are each other’s largest competitors in the digital advertising market. And in the first half of 2025, 98% of Meta’s revenue came from digital ads. Hence, in a sense, it is remarkable that these two would become partners in a different business.

How it helps Alphabet

However, in another sense, this is a huge step forward for Alphabet’s future. In the first half of this year, Alphabet earned 74% of its revenue from the digital ad market, down from 76% in the same period in 2024. This is also by design, as Alphabet has purchased dozens of businesses unrelated to the digital ad market in its efforts to transition into a more diversified technology enterprise.

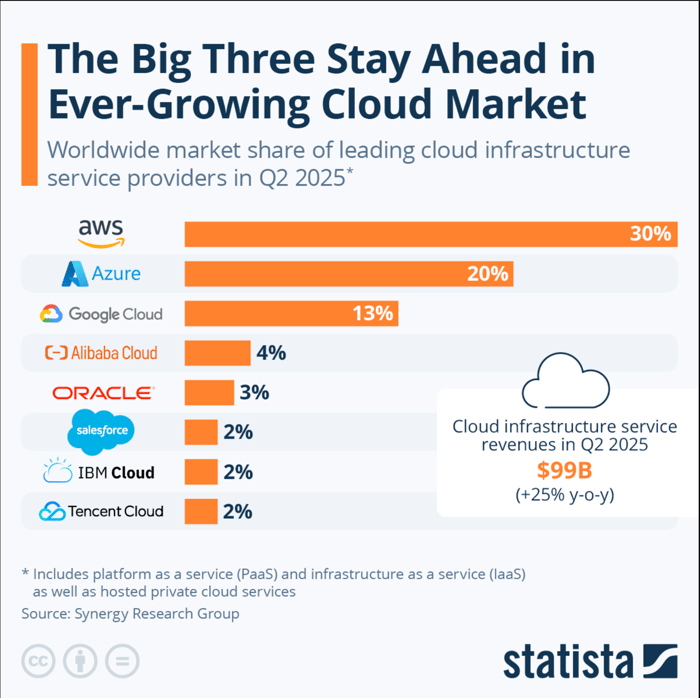

So far, Google Cloud is the only one of these enterprises to appear in Alphabet’s financials. It accounted for 14% of Alphabet’s revenue in the first two quarters of 2025, up from 12% in the same year-ago period.

Additionally, Google Cloud generated over $49 billion in revenue over the trailing 12 months, implying the $10 billion from Meta over six years will make up a relatively small portion of Google Cloud’s business.

Nonetheless, the deal serves as a vote of confidence for Alphabet’s cloud business, one that continues to lag AWS and Azure in terms of market share.

Image source: Statista. Y-o-y = year over year.

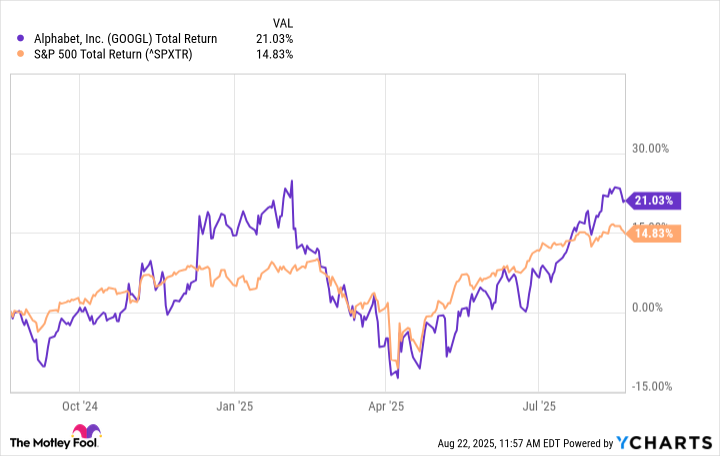

The investor perspective is also crucial. Over the last year, Alphabet stock has outpaced the total returns of the S&P 500 by a significant but not eye-popping margin. However, it may help that Alphabet’s price-to-earnings (P/E) ratio of 22 is the lowest among “Magnificent Seven” stocks. Hence, the Meta deal could prompt investors to look more favorably upon that earnings multiple.

GOOGL Total Return Level data by YCharts.

Furthermore, if the Meta deal prompts other companies to do more business with Google Cloud, it could provide a boost to its market share and, by extension, Alphabet stock.

The Meta deal and Alphabet stock

Ultimately, Meta’s deal with Google Cloud will more than likely take Alphabet stock a leg higher, but investors should expect the effects to be more indirect. Indeed, the deal is remarkable in that it serves as a boost for third-place Google Cloud and is notable since the two companies are direct competitors in each other’s largest enterprises.

Although $10 billion in added business over six years is substantial, Google Cloud generated $49 billion over the last 12 months. Thus, it is a significant but not game-changing boost to the enterprise.

However, the deal may make Google Cloud more attractive to prospective customers, and the low P/E ratio could attract more investors to Alphabet. In the end, those could become the more significant benefits of the deal.

Will Healy has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Alphabet, Amazon, Meta Platforms, and Microsoft. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.