It’s not been a stellar performer of late. Just take a step back and look at the bigger picture.

Is your portfolio in need of a new growth name? Perhaps a stock that hasn’t raced to a nosebleed valuation thanks to the advent of artificial intelligence? They’re out there. You just have to dig a little deeper to find them, pushing through all the noise being created by the market’s most popular names right now.

One of these hidden gems is a young company called Upstart Holdings (UPST -0.27%). Here’s what it does and why you should consider it now.

What’s Upstart?

You may already be familiar with Upstart, but if you’ve only recently stumbled across this name, here’s the deal. In simplest terms, Upstart is a new kind of credit bureau.

In their infancy, established credit bureaus like Equifax, TransUnion, and Experian did their job well enough with the tools available at the time. All three of them were launched before the advent of the internet, while two of them were created before the invention of anything that might even be considered something akin to a modern-day computer. Verifying an individual’s income and manually keeping track of any late or missed payments back then was actually a pretty impressive achievement.

Image source: Getty Images.

Data storage and information-sharing technology have obviously changed for the better in the meantime. The traditional credit bureaus’ approach to determining credit scores, however, hasn’t. All of them still assign quantified scores to criteria like someone’s payment history, current indebtedness, income, and how old that consumer‘s credit history is.

But there’s now a better way. Using an artificial intelligence algorithm that considers more than 1,600 data points about each and every individual, Upstart can do what traditional credit bureaus simply can’t. That’s come up with a hyper-accurate picture of someone’s actual creditworthiness. And it can do so in a matter of seconds, delivering that information to a potential lender via the internet at any time of day.

Honestly, it’s surprising someone didn’t do it before former Google executive and current CEO Dave Girouard launched the company back in 2012 with fellow former Google executive Anna Counselman and statistical science expert Paul Gu.

Whatever the case, shareholders have been well-rewarded since the company’s initial public offering back in December of 2020. The stock’s up more than 240% from its IPO price of $20, and more than 50% above its first trade on a public exchange.

This is still just the beginning, though. There’s still a ton of upside potential left to tap.

Three reasons to buy Upstart stock

There are several compelling reasons to dive into a stake in Upstart here. But three stand out and are bullish enough in and of themselves.

1. The technology works

It’s not just a meaningless solution to a problem that doesn’t exist. The algorithm works. Upstart’s platform allows for 43% more loan approvals than conventional credit bureaus do. And, one-third of the loans it prompts are made at a lower interest rate than would have been offered through a more traditional approval approach. It’s a win for consumers as well as lenders, not to mention the middlemen that benefit when a would-be borrower qualifies to make a purchase.

2. And lenders are increasingly embracing it

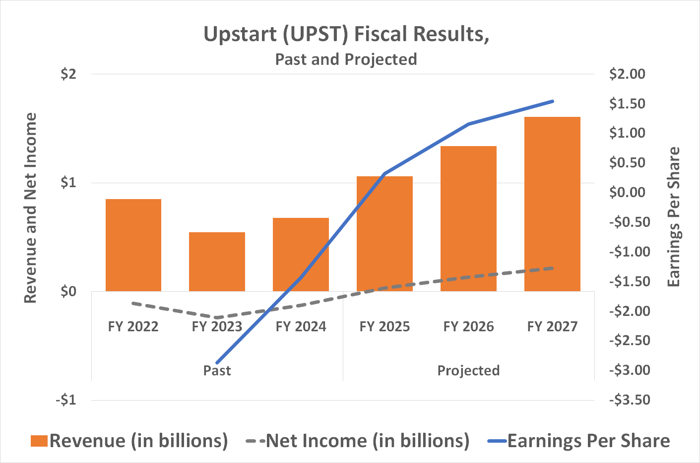

A technology that works is one thing. A technology that the marketplace believes in enough to use is another. In this vein, adoption of Upstart’s technology got the expected slow start. As of the time of its 2020 public offering, only a handful of lenders were using its platform, facilitating $4.1 billion worth of loans in 2021, translating into revenue of $305 million for the company itself.

Last year, though, Upstart’s solution led over 100 lenders to approve nearly $6 billion in loans, translating into revenue of $637 million. The company expects to report a top line of more than $1 billion this year, en route to analysts’ expectation of $1.34 billion revenue next year and 2027 sales of $1.6 billion. Of that $1.6 billion, $216 million of it should be turned into net profit versus this year’s likely near-breakeven.

Data source: Simply Wall St. Chart by author.

3. You can step in at a discounted price

Given the fiscal trajectory here, one would expect Upstart stock to be soaring. And it’s certainly had its bullish moments. But none of those moments have been seen for very long since late last year.

While the company’s shares recovered with the rest of the market following February’s and March’s meltdown, they have not followed through like other stocks have. Rather, they’ve peeled back a bit from July’s high, and are now trading where they were in November. The market is still pretty worried about the economic impact of lingering inflation — a concern Girouard expressed during August’s second-quarter earnings call.

Investors, however, are arguably pricing in too much of this concern. Analysts seem to think so, anyway. The analyst community still supports a consensus target of $78.79 despite the stock’s recent pullback, which is 15% above Upstart shares’ present price. That’s not a bad tailwind to start out a new trade with.

Just don’t lose perspective on what you’re buying into

A promising prospect? Sure. But not one without its risks. Even if its earnings are poised to grow and dramatically widen profit margin rates over the course of the coming couple of years, its net earnings rates are still rather thin. It wouldn’t take much turbulence to do plenty of relative damage to these fragile bullish expectations.

There’s also no real moat to keep would-be competitors from entering the market with a similar credit-scoring technology, including the familiar credit bureaus themselves. Neither is a reason for volatility-tolerant and risk-tolerant investors to avoid Upstart shares, though.

As to the latter, while there’s no significant tangible moat, the lending industry’s disinterest in embracing change effectively serves as one. Upstart has time to continue becoming the dominant name in the AI-powered lending business. With its tech already refined and available, there would be little need for lenders to consider an alternative that isn’t likely to perform any better.

And as to the former, although the young business is still somewhat unpredictable from one quarter or even one year to the next, look five years down the road. Upstart’s platform is superior to alternative credit-scoring tech. Sheer practicality will drive long-term growth here, even if the stock doesn’t reflect this growth with straight-line forward progress.