Demand continues to grow for Tenable’s expanding portfolio of cybersecurity solutions.

Enterprises are using artificial intelligence (AI) at an increasing rate, which is creating a new attack surface for hackers to exploit. AI-powered attacks are also on the rise, which calls for highly sophisticated cybersecurity solutions.

Palo Alto Networks and CrowdStrike lead the cybersecurity industry, but they aren’t the only vendors experiencing a surge in demand for their products. Tenable (TENB -1.50%) is a specialist in vulnerability management, helping enterprises thwart the very threats posed by AI.

With a market capitalization of just $3.7 billion, Tenable is still a tiny player in the cybersecurity space. However, the company’s operating results for the recent second quarter of 2025 (ended June 30) revealed accelerating revenue growth, an uplift in guidance, and a record number of high-spending customers.

Tenable stock remains 49% below its 2022 record high, but here’s why it’s time for investors to pay attention to this up-and-coming cybersecurity powerhouse.

Image source: Getty Images.

A vulnerability management specialist

Tenable owns Nessus, which is the cybersecurity industry’s most accurate and most widely deployed vulnerability management platform. It proactively scans devices, networks, and operating systems to identify potential weak points, so they can be patched before malicious actors exploit them.

But Nessus has become an onramp to Tenable’s growing portfolio of other advanced cybersecurity products. The company has consolidated many of them to create a comprehensive exposure management platform called Tenable One, which protects cloud networks, employee identities, endpoints, infrastructure, and more.

Tenable has the world’s largest repository of exposure data, which allows Tenable One to proactively surface and mitigate threats better than any other platform of its kind.

The company also offers a product called AI Exposure, which helps enterprises secure their AI software, AI platforms, and AI agents. It gives managers visibility into how employees are using AI across the organization, and it allows them to build guardrails to reduce risk. This is especially useful when employees are plugging sensitive internal data into large language models (LLMs) from third-party developers.

Accelerating revenue growth and increased guidance

Tenable generated $247.3 million in revenue during the second quarter of 2025, which was comfortably above management’s forecast of $241 million to $243 million. It represented a year-over-year increase of 12%, which marked an acceleration from the 11% growth the company delivered in the first quarter.

The strong result was driven by high-spending enterprises. Tenable had a record 2,118 customers with at least $100,000 in annual contract value during the second quarter, which highlights how important advanced cybersecurity solutions are becoming to large organizations.

Tenable’s recent momentum might be a sign of things to come, because management adjusted its 2025 full-year revenue guidance to $984 million (at the midpoint of the range), which was an increase of $9 million from its previous forecast three months ago.

Management also made further progress at the bottom line during the second quarter. The company suffered a small loss on a GAAP (generally accepted accounting principles) basis, but after excluding one-off and non-cash expenses like stock-based compensation, the company generated an adjusted (non-GAAP) profit of $41.4 million. That figure was up by almost 9% compared to the year-ago period.

Tenable’s ability to deliver accelerating revenue growth without sacrificing profitability is a sign of strong organic demand for its products.

Tenable stock looks attractive at the current level

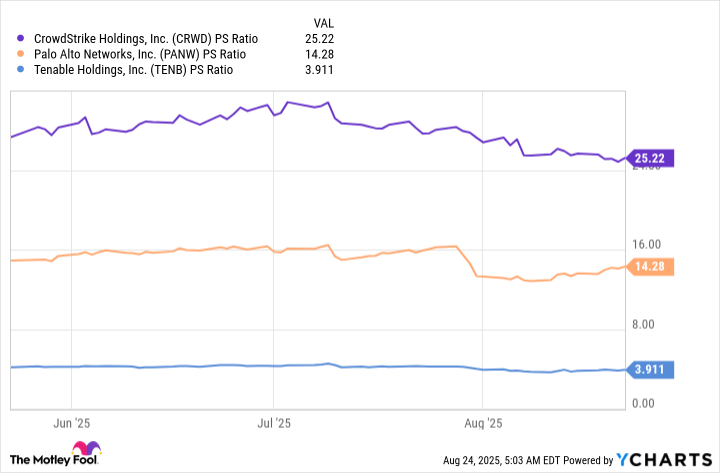

The 49% decline in Tenable stock since 2022, combined with the company’s consistent revenue growth, has pushed its price-to-sales (P/S) ratio down to just 3.9. That is a substantial discount to the valuations of industry leaders like Palo Alto and CrowdStrike:

CRWD PS Ratio data by YCharts

Palo Alto and CrowdStrike operate much larger businesses than Tenable, and they are also delivering faster revenue growth. However, considering Tenable’s momentum right now, I think the valuation gap deserves to be much narrower. Plus, Tenable values its addressable market at $50 billion in the exposure management space alone, and the company’s current revenue suggests it has barely scratched the surface of that opportunity.

As a result, Tenable could be a great long-term buy for investors who are looking to add a cybersecurity stock to their portfolio.

Anthony Di Pizio has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends CrowdStrike. The Motley Fool recommends Palo Alto Networks. The Motley Fool has a disclosure policy.